- Author Introduction Audio

- A Generational Shift in How Retirement Is Viewed

- Step 1: Think in Timelines, Not Labels

- Step 2: Understand Your Retirement Income Reality

- Step 3: Explore “What If” Scenarios Without Pressure

- Retirement Accounts Are Tools, Not Rules

- Why Retirement Planning Can Stay Light

- A Calmer Path to the Golden Years

- Millennial Financial Lab — When Curiosity Turns Into Confidence

- Frequently Asked Questions

- 1. Do I really need to start retirement planning this early?

- 2. How much should Millennials be saving for retirement right now?

- 3. Can I plan for retirement if I’m still paying off student loans?

- 4. What role does Social Security play for Millennials?

- 5. What if I change jobs a lot?

- 6. What’s the difference between the free calculators and the Millennial Financial Lab?

- 7. Is the Millennial Financial Lab only about retirement?

- 8. Do I need a financial advisor before using these tools?

- 9. How often should I revisit my retirement planning?

- 10. Is the Millennial Financial Hub just for Millennials?

Author Introduction Audio

For many young people, retirement planning for millennials still feels heavy—something reserved for baby boomers, financial experts, or a distant future version of yourself. Between student loan debt, rising housing costs, and a volatile job market, it’s easy to see why retirement savings often feel less urgent than day-to-day financial challenges.

But here’s the good news: retirement planning doesn’t have to be rigid, overwhelming, or all-or-nothing. For younger generations—including Millennials and Gen Z—it can be lighter, more flexible, and far more personal.

This guide introduces retirement planning as a way to build options, not pressure—so you can move toward long-term goals while still living your life now.

A Generational Shift in How Retirement Is Viewed

Previous generations often followed a familiar script: work full time, rely on employer pensions, retire around a fixed retirement age, and depend heavily on Social Security as a government benefit.

Younger workers inherited a different reality.

Many Millennials entered the workforce during or just after the Great Recession, navigating stagnant wages, rising student debt, and fewer traditional workplace retirement plans. Gen Xers experienced some of these shifts too, but Millennials and Gen Z are more likely to change jobs, build side hustles, or combine full-time work with part-time work over a long run career.

That doesn’t mean retirement security is out of reach—it simply means the path looks different.

Step 1: Think in Timelines, Not Labels

Instead of asking “When will I retire?”, a more useful question is:

“How early do I want flexibility in my financial future?”

Retirement planning works best when it’s treated as a timeline rather than a single finish line. Life expectancy is increasing, careers are less linear, and many retirement savers expect some form of paid work well into their later years.

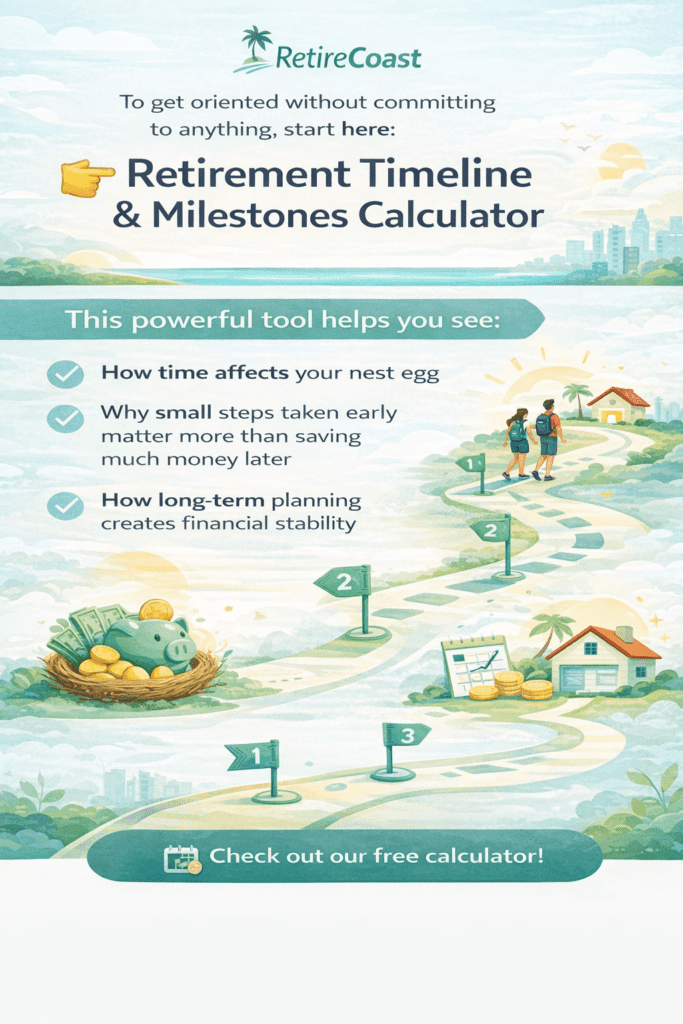

To get oriented without committing to anything, start here:

👉 Retirement Timeline & Milestones Calculator

https://retirecoast.com/retirement-timeline-milestones-calculator/

This powerful tool helps you see:

- How time affects your nest egg

- Why small steps taken early matter more than saving much money later

- How long-term planning creates financial stability

It’s not about hitting a number—it’s about understanding how the long term works in your favor.

Step 2: Understand Your Retirement Income Reality

Many younger workers worry that Social Security may not fully support a comfortable retirement—and retirement research backs up those concerns. A recent study shows that most younger generations expect retirement income to come primarily from self-funded retirement accounts rather than social safety nets.

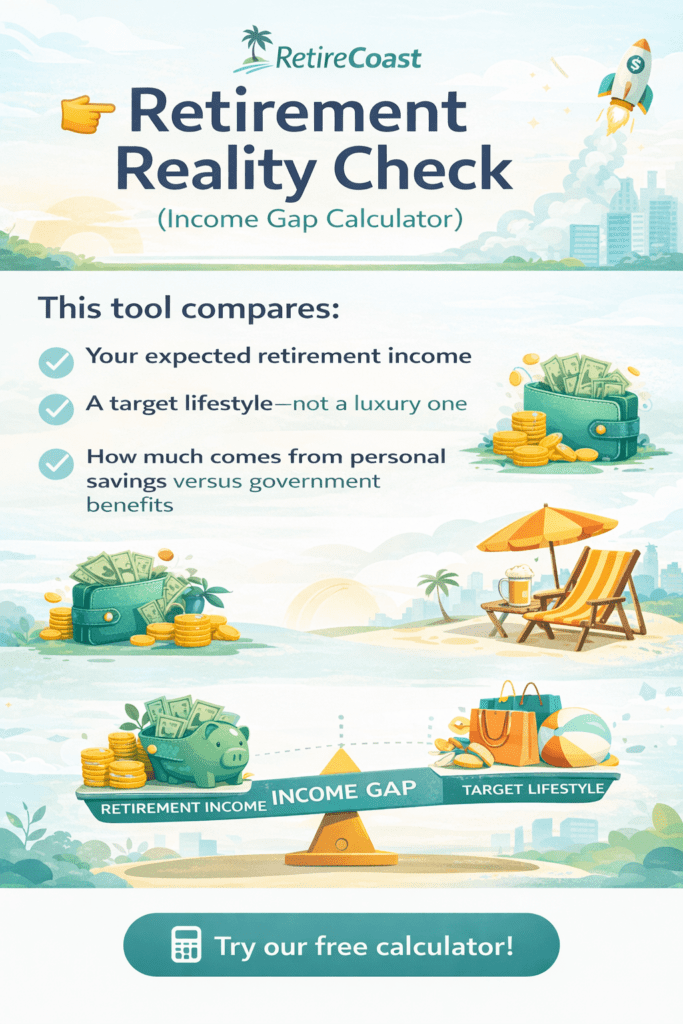

Instead of guessing, it helps to look at the numbers calmly.

👉 Retirement Reality Check (Income Gap Calculator)

https://retirecoast.com/retirement-reality-check-income-gap-calculator/

This tool compares:

- Your expected retirement income

- A target lifestyle—not a luxury one

- How much comes from personal savings versus government benefits

For some, the gap is smaller than expected. For others, it simply highlights where flexibility—or extra money later—could help. Either way, clarity beats anxiety.

Step 3: Explore “What If” Scenarios Without Pressure

This is where retirement planning becomes empowering instead of stressful.

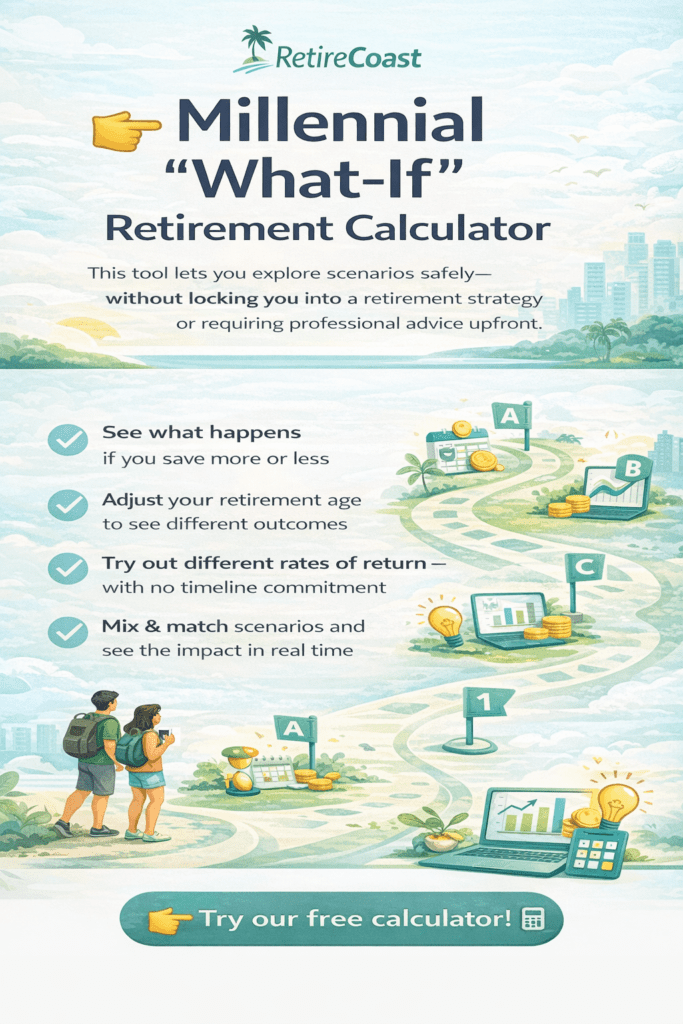

What if you:

- Increase retirement savings slightly after student loans are paid?

- Pick up a side hustle for a few years?

- Work part-time later instead of fully retiring?

- Adjust asset allocation rather than contribution levels?

Small financial decisions can have outsized effects over the long run.

👉 Millennial “What-If” Retirement Calculator

https://retirecoast.com/retirement-planning-millennials-what-if-calculator/

This tool lets you explore scenarios safely—without locking you into a retirement strategy or requiring professional advice upfront.

You will probably move through several jobs over your working years. One of the most important things to remember is that your 401(k) goes with you—it should never be left behind.

When I sold my company to a Fortune 500 firm, we discovered that many former employees—mostly younger people—had left years earlier and never rolled over their 401(k) accounts. When the company plan was later terminated as part of the sale, the retirement provider was unable to locate several of them. Their funds were ultimately turned over to the state.

Years later, I received a call from one former employee trying to track down their retirement money. The required legal efforts had already been made to find them, but it was too late.

Don’t let this happen to you. Never cash out these funds. When you change jobs, ask your new employer’s retirement plan administrator to help you roll your account properly so your retirement savings stay intact and working for your future.

Don’t guess at your Social Security benefits—create (or review) your free my Social Security account to see your record and current estimate. Older generations didn’t have this visibility; you do. Add a quick check-in once or twice a year alongside your 401(k), Roth IRA, and HSA so your plan stays grounded in real numbers, not assumptions.

Retirement Accounts Are Tools, Not Rules

Employer-sponsored retirement plans like 401(k)s remain one of the best ways to build long-term financial security, especially when employer contributions offer what is essentially free money. Roth IRAs and traditional IRAs can also play a role, particularly for those with changing income or nontraditional work.

Investment options like mutual funds, exchange-traded funds, and target date funds help simplify asset allocation, especially for digital natives who prefer automation. The stock market will fluctuate, but time—not timing—is the most reliable advantage retirement savers have.

You don’t need to master every detail of personal finance. Financial education works best when it’s gradual and practical.

Why Retirement Planning Can Stay Light

Retirement readiness doesn’t require perfection. It requires awareness.

Many Millennials juggle:

- Student loans and credit cards

- Emergency fund priorities

- Higher education costs

- Building disposable income later than older generations

That’s normal.

A secure retirement is built through:

- Consistent habits

- Periodic check-ins

- Adjusting financial decisions as life changes

Financial advisers and certified financial planners can help later—but early planning doesn’t require expert advice. It requires curiosity and a willingness to look ahead.

A Calmer Path to the Golden Years

Retirement planning doesn’t have to be intimidating, delayed, or overly technical. It can start with understanding time, exploring scenarios, and building confidence—without pressure to “get it right.”

Start early. Keep it light. Stay flexible.

That’s how younger workers build a financial future that supports both today and the years ahead.Explore the Tools

What-If Scenarios for Millennials

https://retirecoast.com/retirement-planning-millennials-what-if-calculator/

Timeline & Milestones

https://retirecoast.com/retirement-timeline-milestones-calculator/

Retirement Reality Check

https://retirecoast.com/retirement-reality-check-income-gap-calculator/

Millennial Financial Lab — When Curiosity Turns Into Confidence

The free calculators you’ve used here are designed to help you get oriented—without pressure or commitment. They’re meant to answer the first questions most Millennials have about retirement, income gaps, and long-term planning. But they’re only the beginning.

The Millennial Financial Lab is where exploration turns into informed decision-making. Inside the Lab, you’ll find more comprehensive calculators and long-term decision tools designed to help you test real-life scenarios—career changes, timing tradeoffs, savings priorities, and big life moves—without guesswork.

Membership also includes access to curated free articles, additional free calculators, and tools that go well beyond retirement into everyday financial and lifestyle decisions.

For a very modest subscription fee, the Millennial Financial Lab delivers thousands of dollars’ worth of practical financial and life-planning tools—built to help you make better decisions over time, not rush you into them. If you’re ready to move from “just getting oriented” to building clarity across your financial life, the Lab is designed to grow with you.

Is this quiz a test?

No. It’s a short orientation tool that helps you choose the best next calculator to try.

Which tool should I start with if I’m overwhelmed?

Start with the Timeline & Milestones Calculator to get the big picture without committing to anything.

What if I’m worried about Social Security estimates?

Use the Reality Check calculator to compare expected income to a realistic lifestyle target, then decide what to explore next.

What does the “What-If” calculator do?

It lets you safely explore scenarios (like savings changes or retirement age adjustments) without locking you into a strategy.

Do I need a financial advisor before using these tools?

No. These tools are designed to build clarity first. Professional advice can come later if you want it.

How does the Millennial Financial Lab fit in?

The free calculators help you get oriented. The Lab is where you can go deeper with long-term decision tools and more comprehensive calculators.

Frequently Asked Questions

1. Do I really need to start retirement planning this early?

You don’t need a full plan—but starting early gives you options. Even small steps taken now can create flexibility later, especially as your income and priorities change over time.

2. How much should Millennials be saving for retirement right now?

There’s no single “right” number. What matters most is understanding how time affects your savings and how different choices impact your long-term financial future. That’s why exploratory tools often work better than rigid rules.

3. Can I plan for retirement if I’m still paying off student loans?

Yes. Many Millennials balance student loan payments with retirement savings. Even modest contributions—especially through workplace retirement plans—can help keep long-term goals moving forward while you manage current obligations.

4. What role does Social Security play for Millennials?

Social Security is likely to be part of retirement income, but most younger generations don’t expect it to be the only source. Reviewing your Social Security record helps you plan based on real numbers instead of assumptions.

5. What if I change jobs a lot?

That’s normal. Many Millennials and Gen Z workers change jobs more frequently than previous generations. Retirement accounts like 401(k)s can usually be rolled over, allowing your savings to move with you as your career evolves.

6. What’s the difference between the free calculators and the Millennial Financial Lab?

The free calculators help you get oriented—showing timelines, income gaps, and “what-if” scenarios without pressure. The Millennial Financial Lab goes further, offering deeper decision tools, expanded calculators, and long-term planning resources designed to grow with you.

7. Is the Millennial Financial Lab only about retirement?

No. While retirement planning is a core focus, the Lab also includes tools and resources for broader financial and lifestyle decisions—like career changes, savings priorities, and long-term tradeoffs that affect your overall financial stability.

8. Do I need a financial advisor before using these tools?

Not at all. These tools are designed to help you explore scenarios and build clarity on your own. Many people use them to better understand their situation before deciding whether professional advice makes sense later.

9. How often should I revisit my retirement planning?

A quick check-in once or twice a year is usually enough, or anytime something changes—like a new job, higher income, or major life decision. Retirement planning works best as an ongoing process, not a one-time task.

10. Is the Millennial Financial Hub just for Millennials?

The Hub is designed with Millennials in mind, but the concepts—flexibility, long-term thinking, and low-pressure planning—are helpful for anyone who wants a calmer, more modern approach to personal finance.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}