Last updated on June 19th, 2026 at 01:55 pm

Introduction: What Is an Estate Planning Portfolio?

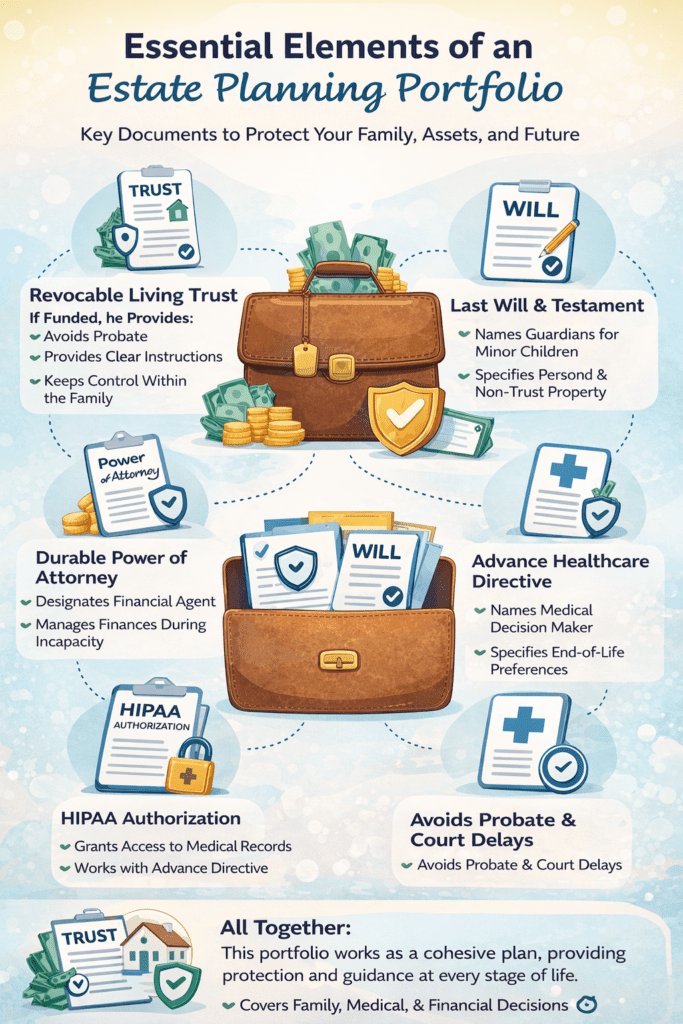

An estate planning portfolio is not a single document—it’s a coordinated system of legal tools designed to protect your assets, guide decisions during incapacity, and ensure your wishes are carried out after death.

Many people mistakenly believe that creating a will alone is enough. In reality, relying on just one document often leaves dangerous gaps—gaps that can create confusion, delay, legal costs, and even family conflict.

A complete estate planning portfolio typically includes:

- Revocable Living Trust

- Last Will and Testament

- Durable Power of Attorney

- Advance Healthcare Directive

- HIPAA Authorization

- Introduction: What Is an Estate Planning Portfolio?

- 1. Revocable Living Trust

- 2. Last Will and Testament

- 3. Durable Power of Attorney

- 4. Advance Healthcare Directive

- 5. HIPAA Authorization

- 6. How These Documents Work Together

- 7. Common Estate Planning Mistakes

- 8. Who Needs an Estate Planning Portfolio?

- 9. How to Get Started

- 10. Final Thoughts

- FAQ

- PODCAST

Each document serves a distinct purpose. Together, they form a comprehensive plan that protects both your financial and personal interests.

Real-world consequence of incomplete planning:

Without the right documents in place:

- Courts may decide who manages your finances

- Medical providers may refuse to share information with loved ones

- Assets may go through probate (costly and time-consuming)

- Family members may disagree on your wishes

The goal of this guide is to help you understand how these documents work together—and why a complete portfolio matters.

1. Revocable Living Trust

What It Is

A revocable living trust is a legal structure that holds your assets during your lifetime and distributes them after your death—without going through probate.

You typically serve as your own trustee while alive and capable. You also name a successor trustee to step in if you become incapacitated or pass away.

What It Does

- Avoids probate for assets placed in the trust

- Allows seamless management during incapacity

- Provides clear instructions for distribution of assets

- Maintains privacy (unlike probate, which is public)

What It Does NOT Do

A common misconception is that a trust does everything. It does not:

- Replace the need for a will

- Eliminate taxes in most cases

- Automatically control assets not placed into the trust

- Replace powers of attorney or healthcare directives

When You Need It

A revocable living trust is especially valuable if you:

- Own real estate

- Have multiple assets or accounts

- Want to avoid probate delays

- Want continuity if you become incapacitated

- Value privacy in your estate

How It Works with Other Documents

The trust is the centerpiece, but it relies on other documents:

- A will acts as a backup for assets outside the trust

- A power of attorney manages non-trust financial matters

- A healthcare directive covers medical decisions

Pamela and Harrison have an estate that looks a great deal like many others. They own a home with several hundred thousand dollars in equity, an $80,000 RV that is fully paid for, a substantial HSA, Roth IRAs, and a brokerage account. Like many parents, their primary goal was straightforward: they wanted their adult children to inherit their property with as little confusion, delay, and expense as possible.

As they began learning more about estate planning, Pamela and Harrison discovered that simply intending for their children to receive everything was not the same as putting a workable legal plan in place. They became concerned about the possibility that, without proper written instructions, their family could face unnecessary court involvement, delays, and added expense after their deaths.

After reviewing their options, they decided to create a Revocable Living Trust as a central part of their estate plan. They understood that a trust could help provide structure, continuity, and a smoother transfer process for the assets they intended to pass on. Just as importantly, it gave them a way to clearly express their wishes while they were both living and able to make those decisions thoughtfully.

Once the trust was completed, Pamela and Harrison included a copy of it in their broader estate planning portfolio. They also made sure their adult children knew the document existed and understood the general purpose behind it. That step alone helped remove uncertainty. Everyone in the family had a clearer picture of what Pamela and Harrison wanted and how their planning was organized.

For Pamela and Harrison, the revocable living trust was not their entire plan. It was one important element in a complete estate planning portfolio designed to protect their assets, communicate their wishes, and make life easier for the people they love.

2. Last Will and Testament

Role in a Trust-Based Plan

Even if you have a trust, you still need a last will and testament.

In a modern estate planning portfolio, the will serves as a safety net—often called a pour-over will—to ensure any assets not placed in your trust are directed into it after death.

Key Functions of a Will

- Names guardians for minor children

- Provides backup asset distribution instructions

- Appoints an executor to manage probate (if necessary)

Understanding Probate

Probate is the court-supervised process of distributing assets after death.

Without proper planning:

- Probate can take months (or longer)

- Legal fees can reduce the estate

- Proceedings become public record

A trust minimizes probate—but the will ensures nothing is left unaccounted for.

After creating their Revocable Living Trust, Pamela and Harrison initially believed their estate plan was complete. Like many people, they assumed they needed either a trust or a will—not both. As they continued researching estate planning, they discovered that each document serves a different purpose, and one does not replace the other.

They learned that a Last Will and Testament plays a critical supporting role—even in a trust-based plan. Their will became the document that addressed situations their trust could not fully cover.

One of the most important functions of their will was naming who would be responsible for raising minor children. While Pamela and Harrison’s children are currently adults, they recognized how essential this would have been earlier in life—and how critical it is for families with younger children. A trust does not formally appoint guardians; only a will provides that legal authority.

Their will also allowed them to be very specific about personal property. Items such as jewelry, family heirlooms, and sentimental belongings are often not titled assets and are not always clearly addressed inside a trust. By using their will, Pamela and Harrison could clearly direct who should receive these items, reducing the likelihood of confusion or disagreements later.

- Names guardians for minor children

- Covers personal property not formally titled

- Captures assets not transferred into the trust

- Acts as a backup (often called a “pour-over will”) to support the trust

Another key realization was that not every asset is always perfectly placed into a trust. Accounts may be overlooked, newly acquired property may not yet be transferred, or small items may remain outside the trust structure. Their will ensures that any of these assets are still directed according to their overall plan.

For Pamela and Harrison, adding a Last Will and Testament completed an important gap in their estate planning portfolio. It provided clarity, backup protection, and ensured that even the smallest details—like personal belongings—were handled exactly as they intended.

3. Durable Power of Attorney

What It Does

A durable power of attorney (DPOA) gives someone authority to manage your financial affairs if you become unable to do so.

This includes:

- Paying bills

- Managing bank accounts

- Handling investments

- Signing documents

Immediate vs. Springing

- Immediate: Effective as soon as signed

- Springing: Only takes effect upon incapacity

Many choose immediate powers for practicality, but safeguards can be added.

If you appoint someone under a power of attorney, it’s important they understand managing someone else’s finances responsibly.”

Why This Is Critical

Without a durable power of attorney:

- Your family may need to go to court to obtain guardianship

- Financial decisions may be delayed

- Bills and obligations could go unpaid

This document is often overlooked—but it is one of the most important in your estate planning portfolio.

As Pamela and Harrison continued building their estate planning portfolio, Harrison raised an important question: “What happens if one of us can’t manage things for a period of time?”

He explained that he had been reading about estate planning and discovered that one of the most serious—and most common—mistakes people make is failing to plan for incapacity. While many assume these situations only occur later in life, Harrison learned that incapacity can happen at any time due to an accident, illness, or sudden medical emergency.

His concern was practical. If one or both of them became unable to act, someone would still need to pay bills, manage accounts, and handle financial responsibilities. Without a plan in place, even simple tasks could become complicated or delayed.

Pamela immediately connected this to a personal experience. She recalled when her grandmother passed away and the difficulties her grandfather faced. Some of their assets were not jointly owned, and as a result, her grandfather was unable to access certain accounts—including a trust account—without going through additional legal steps.

- Incapacity can happen at any age—not just in retirement

- Not all assets are jointly accessible

- Bills, taxes, and obligations continue regardless of health

- Without proper authority, loved ones may face legal barriers

That conversation led Pamela and Harrison to create a Durable Power of Attorney. This document gave a trusted individual the legal authority to step in and manage financial matters if either of them became incapacitated.

By adding this document to their estate planning portfolio, they addressed a risk that many people overlook. It ensured that, no matter what happened, someone they trusted could act quickly and responsibly—without court involvement or unnecessary delays.

4. Advance Healthcare Directive

What It Is

An advance healthcare directive allows you to:

- Appoint someone to make medical decisions on your behalf

- Provide instructions for medical care if you cannot communicate

Living Will vs. Healthcare Proxy

- Living Will: Specifies your wishes for end-of-life care

- Healthcare Proxy: Appoints someone to make decisions

Most comprehensive directives include both.

For additional guidance, review official advance care planning guidance from medical experts.

Why It Matters

In medical emergencies:

- Decisions must be made quickly

- Family members may disagree

- Doctors need clear legal authority

This document ensures your wishes are respected and reduces emotional burden on loved ones.

As Pamela and Harrison continued building their estate planning portfolio, they decided it was important to involve their three adult children in the conversation. While many aspects of estate planning are straightforward, one topic stood out as more personal and difficult to discuss: their wishes for medical care if they were unable to communicate.

Together, they introduced the idea of creating an Advance Healthcare Directive. Rather than leaving these decisions uncertain, Pamela and Harrison wanted to clearly express their preferences while they were both able to do so thoughtfully and without pressure.

After careful discussion, they agreed on an important principle. If they were in a condition where recovery was not reasonably expected, they did not want life-sustaining treatment to be continued indefinitely. More specifically, they expressed that if two qualified physicians determined that there was no reasonable expectation of recovery or meaningful quality of life, they did not wish to be kept alive through artificial or extraordinary measures.

- Their preferences regarding life-sustaining treatment

- Conditions under which treatment should be limited or withdrawn

- The importance of medical confirmation from multiple physicians

- That their wishes were about dignity, not withholding care unnecessarily

Equally important was deciding who would be responsible for making medical decisions if either of them could not. This required thoughtful consideration, not only of trust but also of who would be able to handle difficult decisions under emotional circumstances.

By the end of their family discussion, Pamela and Harrison had chosen the child they felt best suited to act as their healthcare agent. This decision gave their entire family clarity and reduced the possibility of disagreement or uncertainty in an already stressful situation.

For Pamela and Harrison, creating an Advance Healthcare Directive was not just about legal planning—it was about communication. By expressing their wishes clearly and involving their family in the process, they ensured that their values would be understood and respected when it mattered most.

5. HIPAA Authorization

What It Is

A HIPAA authorization allows designated individuals to access your medical information.

Without it, healthcare providers may legally refuse to share information—even with close family members.

Why It’s Essential

Even if you have a healthcare directive:

- Your agent may still need access to medical records

- Family members may need updates during emergencies

This document removes barriers to communication when it matters most.

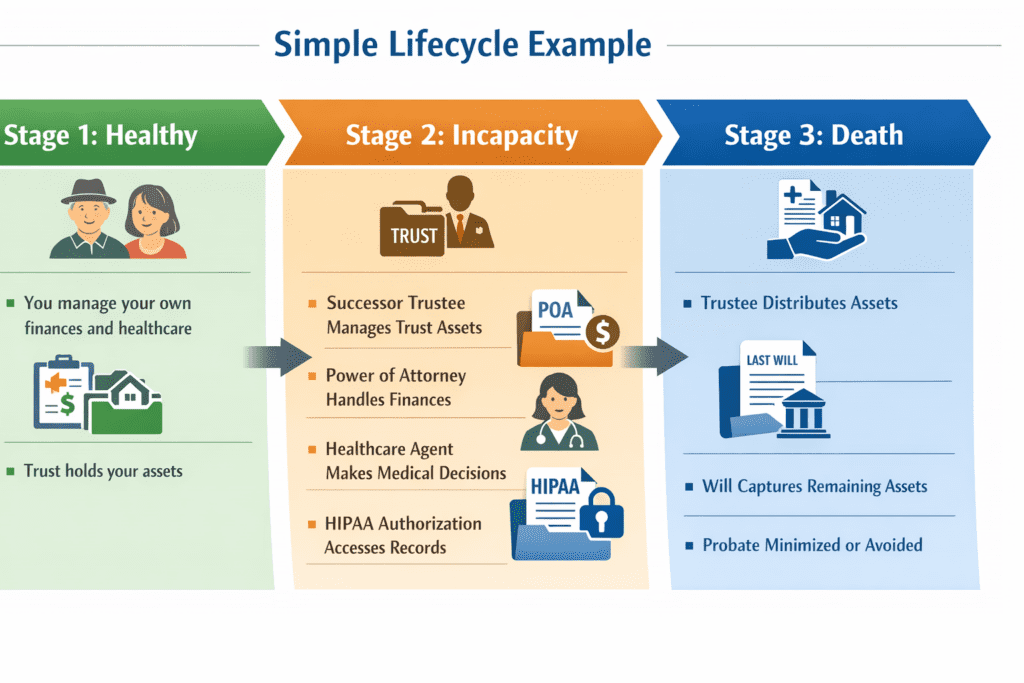

6. How These Documents Work Together

An estate planning portfolio is not a collection of separate documents—it is a coordinated system.

Simple Lifecycle Example

Stage 1: Healthy

- You manage your own finances and healthcare

- Trust holds your assets

Stage 2: Incapacity

- Successor trustee manages trust assets

- Power of attorney handles financial matters outside the trust

- Healthcare agent makes medical decisions

- HIPAA authorization allows access to records

Stage 3: Death

- Trustee distributes assets according to the trust

- Will captures any remaining assets

- Probate is minimized or avoided

Each document activates at the right time—ensuring continuity without court intervention.

7. Common Estate Planning Mistakes

1. Only Having a Will

A will alone often leads to probate and delays.

2. Not Funding a Trust

Creating a trust is not enough—you must transfer assets into it.

3. Not Updating Documents

Life changes (marriage, divorce, children, new assets) require updates.

4. Choosing the Wrong Agent or Trustee

The wrong person can create more problems than having no plan at all.

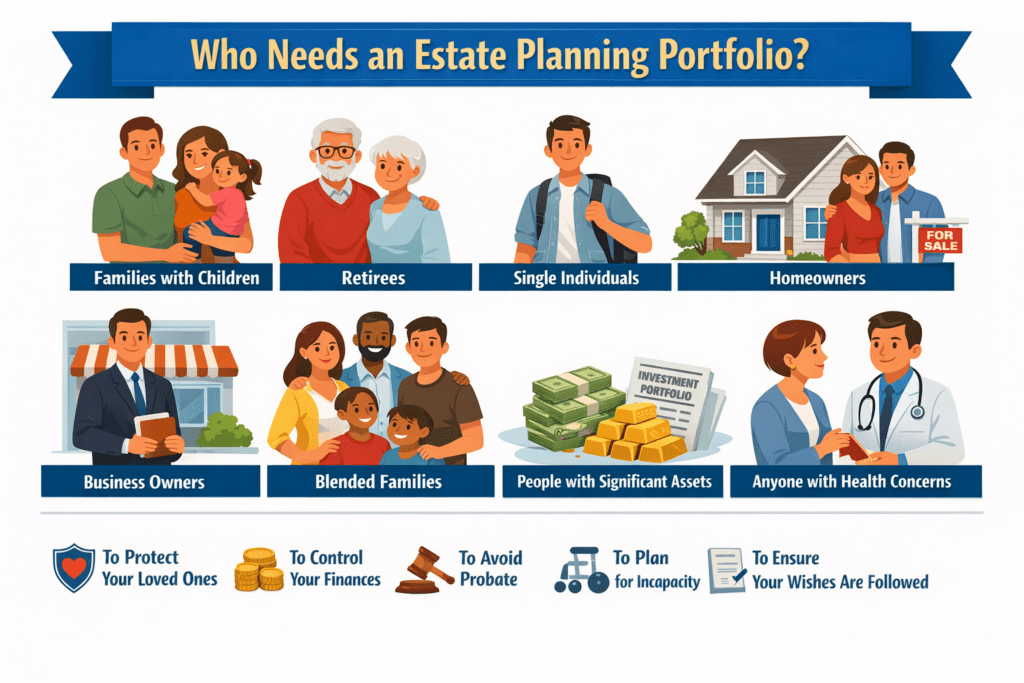

8. Who Needs an Estate Planning Portfolio?

Retirees

- Protect accumulated wealth

- Simplify transfer of assets

- Avoid probate delays

Millennials with Assets or Families

- Protect children

- Plan for unexpected incapacity

- Establish long-term financial structure

Business Owners

- Ensure continuity of operations

- Define ownership transitions

- Protect business assets

Property Owners

- Avoid probate on real estate

- Simplify transfers across states

- Maintain control of property

9. How to Get Started

Estate planning does not need to begin with an attorney—it should begin with clarity.

A practical approach:

- Understand each document

- Organize your assets and decisions

- Prepare a structured draft

- Then seek professional review

The RetireCoast Approach (Preparation First)

The RetireCoast Estate Planning Membership is designed to help you:

- Build a structured revocable living trust draft

- Prepare your durable power of attorney

- Develop your healthcare directive framework

- Organize decisions before legal review

This preparation can:

- Reduce legal costs

- Improve clarity

- Help you ask better questions

👉 Learn more:

- https://retirecoast.com/estate-planning-membership/

- Member access: https://retirecoast.com/estate-dashboard/

10. Final Thoughts

An estate planning portfolio is about more than documents—it’s about control, clarity, and protection.

When done correctly, it:

- Protects your family

- Preserves your assets

- Reduces legal complexity

- Ensures your wishes are honored

The most important step is simply getting started.

FAQ

What is an estate planning portfolio?

A coordinated set of legal documents designed to manage your assets, healthcare decisions, and legacy.

Do I need both a trust and a will?

Yes. A trust handles most assets, while a will acts as a backup and names guardians.

What happens if I don’t have a power of attorney?

Your family may need court approval to manage your finances.

Is a healthcare directive the same as a living will?

A healthcare directive often includes a living will and a medical decision-maker.

Why is HIPAA authorization important?

It allows your chosen individuals to access your medical information.

Can a trust avoid probate?

Yes, for assets properly transferred into the trust.

When should I update my estate plan?

After major life changes such as marriage, divorce, or new assets.

Do millennials need estate planning?

Yes, especially if they have assets, children, or financial responsibilities.

What is the biggest mistake people make?

Failing to fund their trust or relying only on a will.

How do I start?

Begin by understanding the documents and organizing your decisions before consulting an attorney.

PODCAST

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}