Introduction: Why Depreciation Is One of the Most Important Concepts You Can Understand

Rental property depreciation is one of the most powerful tax advantages available to real estate investors—but it’s also one of the most misunderstood. Many investors focus on rental income and expenses while overlooking how depreciation can reduce taxable income, increase cash flow, and impact the taxes owed when a property is sold. Understanding rental property depreciation is essential if you want to maximize tax savings, avoid costly mistakes, and build long-term wealth through real estate or business ownership.

- Introduction: Why Depreciation Is One of the Most Important Concepts You Can Understand

- What Is Rental Property Depreciation?

- 2. What Happens at Disposal (The Sale)?

- Step A: Adjusted Basis — How the IRS Tracks Your Asset

- Step B: Calculating the Gain — It’s Not What You Think

- Step C: Depreciation Recapture — Paying Back the “Loan”

- Why This Matters for Planning

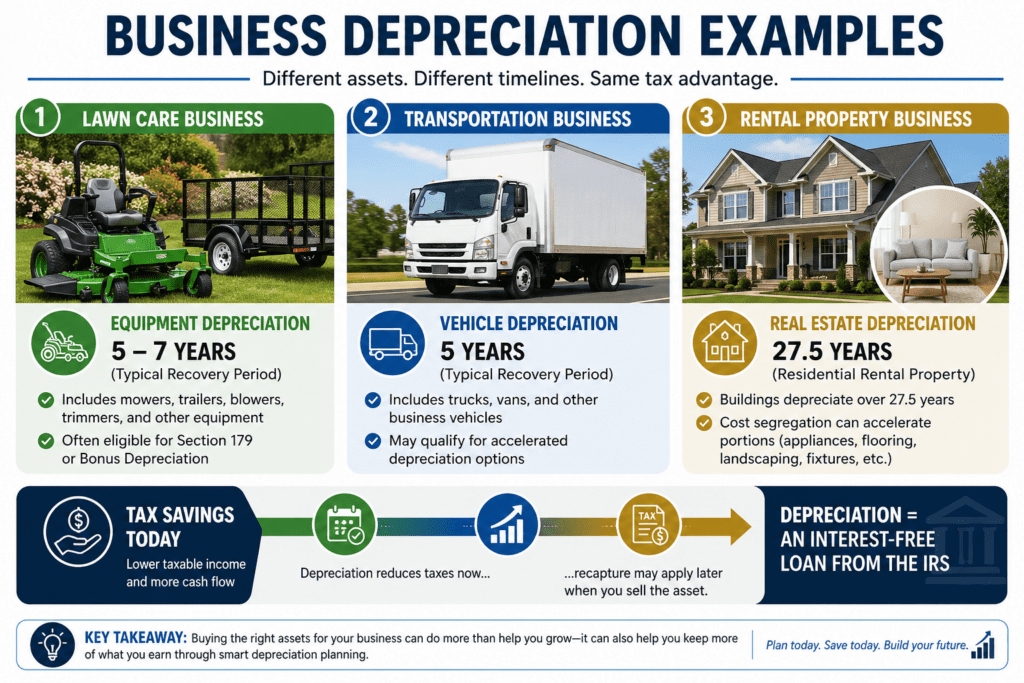

- Business Asset Comparison (Lawn Care Example)

- Important Insight

- Planning Questions to Consider

- Transition to Next Section

- Case Study: Sam’s Lawn Care Equipment — When Depreciation Comes Back

- What This Means for Sam’s Taxes

- 2. Smaller Tools (Under $1,000 Each)

- Summary of Tax Impact

- Summary of Tax Impact

- Why This Case Study Matters

- Key Planning Takeaways

- Questions Sam Should Be Asking

- Case Study: Barbara & Paul — Short-Term Rental Depreciation in Action

- The Purchase and Initial Strategy

- Where Depreciation Becomes Powerful

- The Reality Check They Almost Missed

- A Key Distinction (Without Getting Too Deep Yet)

- What They Did Right

- What They Could Have Done Better

- How Depreciation Helped Them

- The Bigger Lesson

- Transition to Next Article

- Case Study: Barbara & Paul — Understanding Depreciation Before It’s Too Late

- The Real Investment (Beyond the Purchase Price)

- Where Depreciation Changes Everything

- What They Didn’t Realize at First

- Why Planning Depreciation Early Matters

- The Long-Term Consideration

- The Key Lesson

- Looking Ahead

- 3. Case Study: Selling the Property vs. Selling the LLC — What Happens to Depreciation?

- The Key Issue: Depreciation Doesn’t Disappear

- Short Answer: No

- Option 1: Asset Sale (Selling the Property)

- Option 2: Equity Sale (Selling the LLC)

- Why This Happens

- What Actually Changes Between the Two Options

- The Buyer’s Perspective (Important for Pricing)

- Where Depreciation Still Drives the Outcome

- Example Outcome

- What Could Increase Their Yield

- Key Takeaway

- Strategic Insight

- Looking Ahead

- Free Tool

- Quiz

- FAQ

What Is Rental Property Depreciation?

Rental property depreciation is a tax deduction that allows property owners to recover the cost of a rental building over time. Instead of deducting the full purchase price in one year, the IRS requires the cost to be spread over the property’s useful life—typically 27.5 years for residential rental property. This annual deduction reduces taxable income, even though the investor does not incur a cash expense each year.

Quick Example

- Purchase price (building only): $275,000

- Depreciation period: 27.5 years

- Annual deduction: $10,000

➡️ This $10,000 deduction reduces taxable income each year, lowering the investor’s tax liability.

Why It Matters

- Lowers taxable income

- Increases after-tax cash flow

- Defers taxes until the property is sold

- Plays a major role in long-term tax strategy

Key Rule to Remember

Depreciation is required in practice. Even if you don’t take it, the IRS assumes you did and will reduce your basis accordingly when you sell the property.

Most investors focus on cash flow—how much money comes in each month after expenses. But the real advantage of owning rental property or a business often comes from something you don’t actually see on a bank statement.

That advantage is depreciation.

Depreciation is one of the few tools in the tax code that allows you to:

- Reduce your taxable income

- Keep more of your cash

- Build wealth faster over time

And yet, it is widely misunderstood.

Many property owners:

- Don’t fully understand how depreciation works

- Miss deductions they are entitled to

- Or worse, discover too late that they owe taxes on benefits they didn’t even claim

At its core, depreciation is simple:

The IRS allows you to recover the cost of an asset over time because it wears out or becomes obsolete.

But once you go beyond that basic definition, depreciation becomes a strategic tool—one that affects:

- How much tax you pay each year

- Whether your rental shows a profit or loss

- How much you owe when you sell

It also applies far beyond real estate. Whether you own:

- A rental property

- A short-term vacation rental

- Or a business like a lawn care company with equipment and vehicles

The same principles apply.

In this guide, we will walk through depreciation step-by-step—from the basics to advanced strategies—so you can understand:

- How depreciation actually works

- How it reduces your taxes today

- What happens when you sell

- And how to avoid the most costly mistakes

If you understand depreciation correctly, you won’t just be managing expenses—you’ll be actively controlling your tax strategy and long-term financial outcome.

In the early years of a new business—when more money is going out than coming in—this “free loan” of deferred taxes can make the difference between profit and loss.

You must pay it back, but that happens later—typically when you are already profitable and choose to dispose of the asset or exit the business.

I have used depreciation in all of my businesses, and I am thankful for it. Recent changes in the Big Beautiful Bill make this tool even more powerful and worthy of careful planning.

Please take a good look at our Business Membership for some excellent tools that can help you manage depreciation.

2. What Happens at Disposal (The Sale)?

Depreciation provides a powerful benefit while you own an asset—but it is not permanent. When you sell the property or business asset, the IRS essentially reviews what happened over the life of that asset and “settles the score.”

To understand this, you need to understand three key concepts:

- Adjusted Basis

- Total Gain

- Depreciation Recapture

Step A: Adjusted Basis — How the IRS Tracks Your Asset

Each year you take depreciation, the IRS reduces your “book value” (called your basis) in the asset.

Using John’s example:

- Original building value: $275,000

- Annual depreciation: $10,000

- 5 years of ownership: $50,000 total depreciation

➡️ Adjusted Basis = $225,000

This is critical because the IRS no longer views the property as a $275,000 asset. In their eyes, it is now worth $225,000.

Step B: Calculating the Gain — It’s Not What You Think

When John sells the property, the IRS does not compare the sale price to what he originally paid. Instead, they compare it to the adjusted basis.

Example:

- Sale price: $350,000

- Adjusted basis: $225,000

➡️ Total taxable gain = $125,000

This is often surprising to investors because their taxable gain is larger than expected.

Step C: Depreciation Recapture — Paying Back the “Loan”

Remember the earlier concept:

Depreciation is an interest-free loan.

Now the IRS wants part of that loan repaid.

- Total depreciation taken: $50,000

- This portion is taxed separately at recapture rates (up to 25%)

- Remaining gain ($75,000) is taxed at capital gains rates

Why This Matters for Planning

Depreciation is not a loophole—it’s a timing strategy.

You:

- Save taxes during ownership

- Improve cash flow

- Reinvest that savings

Then:

- Pay some of it back later when you sell

Business Asset Comparison (Lawn Care Example)

This same concept applies to business assets like equipment.

If Eric from the lawn care business:

- Buys a mower for $4,000

- Depreciates it over 5 years

- Sells it later for $2,000

The IRS will:

- Compare the sale price to the adjusted basis

- Recapture depreciation as ordinary income

➡️ Even small business equipment follows the same rules as real estate.

Important Insight

Many investors focus only on:

- Purchase price

- Monthly income

But the real financial outcome depends on:

- Depreciation taken

- Adjusted basis

- Tax treatment at sale

Planning Questions to Consider

Before buying—or selling—an asset, you should ask:

- What is my expected depreciation over the holding period?

- How will this affect my adjusted basis?

- What will my taxable gain look like at sale?

- Will I have strategies in place to offset recapture?

Transition to Next Section

Now that you understand how depreciation works over time and at sale, the next step is to understand what actually qualifies for depreciation—and how different types of property are treated.

Case Study: Sam’s Lawn Care Equipment — When Depreciation Comes Back

Depreciation doesn’t just apply to real estate—it also applies to business equipment. And in some cases, the tax impact can be even more immediate and more complex.

Let’s look at Sam, who owns a lawn care business.

Sam’s Purchase Strategy

Sam invests in his business and purchases:

- Commercial mowers and trailer: $16,000

- Smaller tools (trimmers, blowers, hand tools): under $1,000 each

To reduce taxes in his first year, Sam uses:

- Section 179 and/or Bonus Depreciation for the mowers and trailer

- De Minimis Safe Harbor Election for the smaller tools

What This Means for Sam’s Taxes

1. Mowers and Trailer ($16,000 Total)

Because Sam elected immediate depreciation:

- He deducted the full $16,000 in Year 1

- His tax basis is now $0

What Happens When He Sells the Equipment?

Let’s say:

- Sam sells a mower originally purchased for $6,000

- Sale price: $3,000

➡️ Since his basis is $0, the entire $3,000 is taxable

Section 1245 Depreciation Recapture

This gain is not treated as a capital gain.

Instead:

- It is taxed as ordinary income

- This is required under Section 1245 Depreciation Recapture rules

➡️ The IRS is reclaiming the tax benefit Sam received earlier.

Where It Is Reported

Sam must report this on:

- Form 4797

This form is specifically used for the sale of business assets and depreciation recapture.

2. Smaller Tools (Under $1,000 Each)

For smaller tools, Sam likely used the De Minimis Safe Harbor Election, which allows him to:

- Deduct the full cost immediately

- Treat them as supplies instead of depreciable assets

What Happens When He Sells Them?

Since these items were never capitalized:

- There is no depreciation schedule

- No formal recapture calculation

➡️ The proceeds are simply recorded as business income

Where It Is Reported

- On Schedule C (Form 1040)

- As part of normal business revenue

Summary of Tax Impact

Summary of Tax Impact

| Asset Type | Original Cost | Tax Basis After Deduction | Sale Price | Tax Treatment |

|---|---|---|---|---|

| Mowers / Trailer | $6,000+ | $0 | $2,500–$3,000 | Ordinary Income (Recapture) |

| Small Tools | < $1,000 | $0 (Expensed) | $200 | Business Income |

Depreciation recapture on business equipment (like Sam’s mowers) is typically treated as ordinary income—but not subject to self-employment tax when reported correctly on Form 4797.

However, if this income is mistakenly reported on Schedule C as regular business income, it may be subject to self-employment tax, increasing the tax burden unnecessarily.

Proper classification matters. This is one area where good recordkeeping—and sometimes professional guidance—can make a meaningful difference.

Why This Case Study Matters

Sam’s example highlights a critical truth:

- Accelerated depreciation creates immediate tax savings

- But it also creates future taxable income when assets are sold

Key Planning Takeaways

- Immediate write-offs are powerful—but not “free”

- Keep a clear asset log separating:

- Depreciated assets

- Expensed items

- Understand how each asset will be treated at sale

- Plan ahead to avoid unnecessary taxes

Questions Sam Should Be Asking

- Will I sell or trade in equipment later?

- Have I tracked each asset properly?

- Am I reporting recapture correctly?

- Can I offset this income with other deductions?

Strategic Insight

Just like real estate:

👉 Depreciation is a timing strategy, not a permanent tax elimination

Used correctly, it:

- Improves early cash flow

- Supports business growth

Used incorrectly, it:

- Creates unexpected tax liabilities

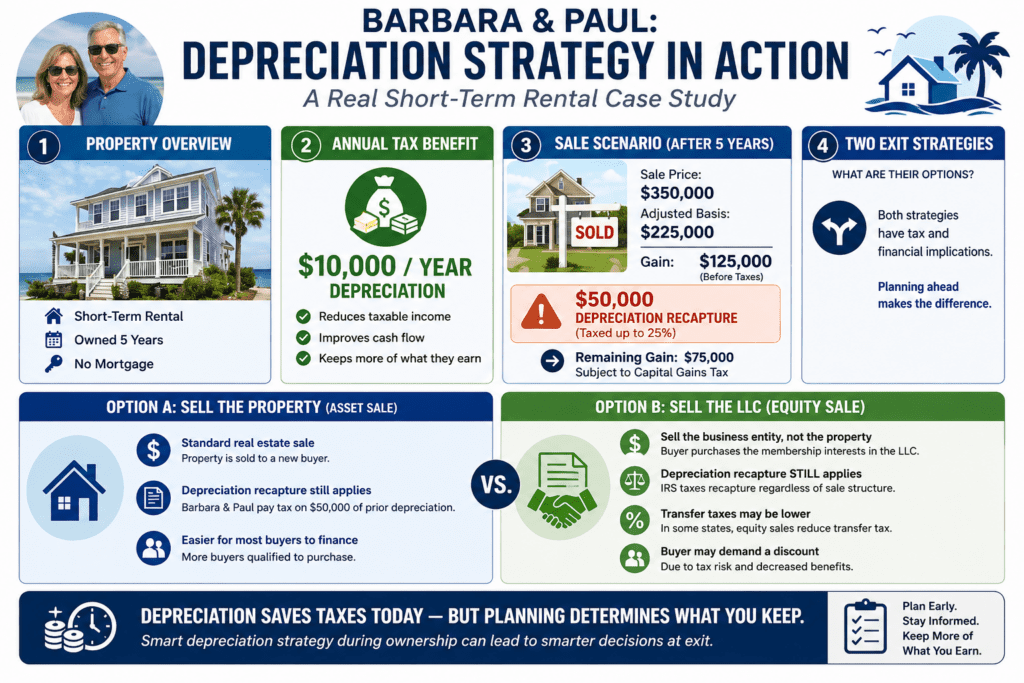

Case Study: Barbara & Paul — Short-Term Rental Depreciation in Action

Barbara and her son Paul decided to purchase a short-term rental property near the beach. They had always wanted a place to visit, and it seemed like a great opportunity to create both family enjoyment and additional income.

They found a:

- 3-bedroom, 2-bath home

- Located about a mile from the beach

- Strong potential for vacation rental income

Excited by the opportunity, they made an offer before fully evaluating all the financial details.

The Purchase and Initial Strategy

After closing, Barbara and Paul:

- Furnished the home for short-term rental use

- Purchased appliances, décor, and outdoor amenities

- Began working with a property manager

Their total investment quickly grew beyond just the purchase price:

- Home (building portion): $320,000

- Furniture, appliances, décor: $40,000+

Where Depreciation Becomes Powerful

Unlike many first-time investors, Barbara and Paul decided to understand the tax side early.

1. Building Depreciation

- $320,000 ÷ 27.5 years

➡️ About $11,600 per year in depreciation

2. Personal Property (Furnishings & Equipment)

Their furniture and equipment:

- Falls into shorter depreciation categories (5–7 years)

- Can often be accelerated

➡️ Potential for much larger deductions in early years

3. Combined Impact

In their first year, they may see:

- Significant depreciation from the building

- Even larger deductions from furnishings

➡️ Result: A tax loss on paper—even if the property produces cash flow

The Reality Check They Almost Missed

Initially, Barbara and Paul were focused on:

- Rental income

- Occupancy rates

- Guest experience

But they had not fully considered:

- How depreciation would affect their taxes

- How the property would be treated by the IRS

- Whether they could actually use the losses created

A Key Distinction (Without Getting Too Deep Yet)

Short-term rentals are unique.

Because Barbara and Paul’s average guest stay is relatively short:

- The property may be treated more like a business than a traditional rental

This creates potential opportunities—but also requirements.

👉 The ability to fully use depreciation losses depends on how involved they are in the operation.

(We will explore this in detail in the next article.)

What They Did Right

After learning more, Barbara and Paul adjusted their approach:

- Stayed involved in key decisions

- Reviewed property performance regularly

- Evaluated improvements that could increase bookings

- Began tracking their time and involvement

What They Could Have Done Better

Like many investors, they initially:

- Focused on the property itself—not the tax strategy

- Didn’t fully model depreciation before purchase

- Underestimated the importance of planning

How Depreciation Helped Them

Even in their first year:

- Depreciation reduced their taxable income

- Helped offset rental income

- Improved overall cash flow

And most importantly:

👉 It gave them flexibility to reinvest into the property

The Bigger Lesson

Barbara and Paul’s experience highlights something critical:

- Buying the property is only the first step

- The real advantage comes from how you structure and manage it

Depreciation is not just a tax concept—it is a planning tool that should be considered:

- Before you buy

- While you operate

- And when you eventually sell

Transition to Next Article

Barbara and Paul created meaningful depreciation benefits—but one important question remains:

👉 Can they use all of those losses today, or will some be limited?

That depends on how the IRS classifies their activity and their level of involvement.

👉 Next: Passive vs. Active Rental Income — When Can You Actually Deduct Your Losses?

Case Study: Barbara & Paul — Understanding Depreciation Before It’s Too Late

Barbara and her son Paul decided to purchase a short-term rental property near the beach. They had always wanted a place to visit, and it seemed like a great opportunity to combine personal enjoyment with income potential.

They found a:

- 3-bedroom, 2-bath home

- Located about a mile from the beach

- Ideal for short-term vacation rentals

Excited about the opportunity, they made an offer quickly and moved forward with the purchase.

The Real Investment (Beyond the Purchase Price)

After closing, Barbara and Paul realized the total investment was more than just the home itself.

They added:

- Furniture and décor

- Appliances

- Outdoor amenities

- Setup costs to make the home rental-ready

Their investment looked like this:

- Building value: $320,000

- Furnishings and equipment: $40,000+

Where Depreciation Changes Everything

Like many first-time investors, Barbara and Paul initially focused on:

- Rental income

- Booking rates

- Property upgrades

But they had not yet fully considered how depreciation would impact their financial results.

1. Building Depreciation

The home itself is depreciated over 27.5 years:

- $320,000 ÷ 27.5

➡️ About $11,600 per year

This alone creates a meaningful annual tax deduction.

2. Furnishings and Equipment (The Hidden Advantage)

Unlike the building, their furniture and equipment:

- Have shorter useful lives (typically 5–7 years)

- Can often be depreciated much faster

This means:

➡️ Larger deductions in the early years

➡️ Greater reduction in taxable income

3. Combined Depreciation Impact

When combined, Barbara and Paul’s depreciation could:

- Offset a large portion of their rental income

- Reduce taxes in the early years

- Improve overall cash flow

In some cases:

➡️ They may show a tax loss on paper, even while generating positive cash flow

What They Didn’t Realize at First

Barbara and Paul made a common mistake:

They evaluated the property based on:

- Purchase price

- Expected rental income

But did not initially model:

- Annual depreciation

- Long-term tax impact

- What happens when the property is sold

Why Planning Depreciation Early Matters

If Barbara and Paul had planned ahead, they could have:

- Estimated their annual depreciation before purchase

- Structured improvements more strategically

- Better understood how furnishings impact early deductions

- Made more informed decisions about upgrades

The Long-Term Consideration

Depreciation is not permanent—it shifts taxes into the future.

When Barbara and Paul eventually sell the property:

- Their basis will be reduced

- Their taxable gain will increase

- A portion of their gain will be subject to depreciation recapture

The Key Lesson

Barbara and Paul’s experience highlights a critical truth:

👉 Depreciation should be part of your decision-making before you buy—not after

It affects:

- Your annual tax position

- Your cash flow

- Your long-term profit

Looking Ahead

Barbara and Paul created meaningful depreciation benefits—but there is one important layer that determines how those benefits are used.

👉 Whether those depreciation losses can be fully used in the current year depends on how the activity is classified and their level of involvement.

We will break that down in the next article.

👉 Next: Passive vs. Active Rental Income — When Can You Actually Use Your Losses?

- Estimate building value (separate land from structure)

- Calculate expected annual depreciation

- Identify potential personal property (furniture, equipment)

- Evaluate cost segregation opportunity

- Estimate total first-year tax impact

- Understand how depreciation affects long-term exit strategy

- Take depreciation every year (do not skip)

- Track all improvements separately from repairs

- Maintain a detailed fixed asset log

- Separate building, equipment, and expensed items

- Review depreciation strategy annually

- Consider upgrades that may qualify for accelerated depreciation

- Calculate adjusted basis (original cost minus depreciation)

- Estimate depreciation recapture exposure

- Review capital improvements that may increase basis

- Understand tax impact of the sale

- Plan timing of sale for tax efficiency

- Consider strategies to offset taxable gain

👉 Download the Depreciation Planning Checklist

3. Case Study: Selling the Property vs. Selling the LLC — What Happens to Depreciation?

Barbara and Paul have owned their short-term rental property for the past five years. The property has produced a modest profit and is owned outright inside an LLC with no mortgage.

Now they are considering two options:

- Sell the property directly (“asset sale”)

- Sell the LLC itself, including the website and booking relationships (“equity sale”)

At first glance, these options may seem very different—but from a depreciation standpoint, they are more similar than most investors expect.

The Key Issue: Depreciation Doesn’t Disappear

Over the past five years, Barbara and Paul have taken depreciation on the property.

This means:

- Their adjusted basis has been reduced

- Their future taxable gain has increased

- A portion of their gain will be subject to depreciation recapture

The critical question is:

👉 Does selling the LLC instead of the property avoid depreciation recapture?

Short Answer: No

Even if Barbara and Paul sell the LLC itself, the IRS still requires them to recognize depreciation recapture.

This is due to a “look-through” concept applied to real estate entities.

Option 1: Asset Sale (Selling the Property)

In a traditional sale:

- The LLC sells the property

- The IRS treats this as the sale of the underlying asset

Tax Impact

- Depreciation taken over 5 years is recaptured

- Taxed at rates up to 25%

- Remaining gain taxed at capital gains rates

Option 2: Equity Sale (Selling the LLC)

In this scenario:

- Barbara and Paul sell their ownership interest in the LLC

- The buyer takes control of the entity

At first glance, this appears to be a simple capital gain transaction.

However:

👉 The IRS still requires recognition of depreciation recapture.

Why This Happens

From a tax perspective:

- The LLC’s underlying asset is still real estate

- The depreciation taken over time still exists

- The IRS “looks through” the entity to the property itself

➡️ Result: Depreciation recapture still applies to the sellers

What Actually Changes Between the Two Options

While depreciation treatment is similar, other factors differ.

Key Differences

| Factor | Asset Sale (Property) | Equity Sale (LLC) |

|---|---|---|

| Depreciation Recapture | Applies | Applies |

| Basis Reset for Buyer | Yes | No |

| Transfer Taxes | Typically higher | Often lower |

| Buyer Risk | Lower | Higher (inherits LLC history) |

| Pricing | Market-driven | May require discount |

The Buyer’s Perspective (Important for Pricing)

In an asset sale:

- The buyer gets a new stepped-up basis

- They can restart depreciation

In an equity sale:

- The buyer inherits the existing basis

- No reset on depreciation

➡️ This often leads buyers to discount the purchase price

Where Depreciation Still Drives the Outcome

Regardless of the structure, Barbara and Paul’s final result depends on:

- Total depreciation taken

- Adjusted basis

- Final sale price

- Portion of gain subject to recapture

Example Outcome

Let’s assume:

- Original building value: $320,000

- Depreciation over 5 years: $60,000

- Adjusted basis: $260,000

- Sale price: $420,000

Tax Impact

- Total gain: $160,000

- Depreciation recapture: $60,000 (up to 25%)

- Remaining gain: $100,000 (capital gains rates)

➡️ This applies whether they sell the property or the LLC

What Could Increase Their Yield

Even though depreciation recapture is unavoidable, Barbara and Paul can improve their outcome by:

- Properly tracking all improvements (which increase basis)

- Understanding how furnishings were depreciated

- Evaluating total transaction costs

- Considering whether business value (website, bookings) adds premium

Key Takeaway

Barbara and Paul cannot avoid depreciation recapture simply by changing how they sell the asset.

👉 Depreciation always follows the asset—even when ownership structure changes.

Strategic Insight

The real decision between:

- Selling the property

- Selling the LLC

Is not about avoiding depreciation recapture.

It is about:

- Pricing

- buyer expectations

- transaction costs

- and overall deal structure

Looking Ahead

Barbara and Paul now understand how depreciation affects their sale.

But there is another important layer:

👉 How the income and losses from this property are treated each year—and whether they were fully usable.

That depends on how the IRS classifies the activity.

👉 Next: Passive vs. Active Rental Income

- Depreciation recapture applies

- Buyer usually receives a stepped-up basis

- Transfer taxes and deed fees may apply

- Cleaner transaction for most buyers

- Often easier to finance and close

- Depreciation recapture still applies

- Buyer may not receive a new depreciation basis

- Some transfer costs may be lower

- Buyer may inherit LLC liabilities

- Buyer may demand a price discount

| Category | Asset Sale | LLC Sale |

|---|---|---|

| Depreciation Recapture | Applies | Still applies |

| Buyer Basis | Usually reset to purchase price allocation | May inherit existing entity basis |

| Transfer Costs | May be higher | May be lower depending on state/local rules |

| Buyer Risk | Lower; buyer gets the property | Higher; buyer may inherit LLC history |

| Pricing Impact | More familiar to buyers | May require a discount |

When you reduce your taxes today through depreciation, you are keeping cash that would have otherwise gone to the government. That cash can be reinvested, used to improve your property, or applied to grow your business.

This concept is known as the time value of money—the idea that money today is more valuable than the same amount in the future because it can be put to work immediately.

Even though some of the tax benefit may be recaptured later, the ability to use that money over time can significantly improve your overall financial outcome.

For a deeper explanation, see this research from The Budget Lab at Yale: Depreciation 101 .

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | Sale |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Annual Depreciation | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | — |

| Tax Savings | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | ✔ | Payback |

| Cumulative Depreciation | 10K | 20K | 30K | 40K | 50K | 60K | 70K | 80K | 90K | 100K | Recapture |

- Reinvestment: If they save $2,500 per year in taxes, that money can be reinvested into upgrades or additional investments.

- Compounding: By Year 10, the value of early tax savings has grown through reinvestment and inflation.

- Nominal vs. Real Dollars: They deduct taxes using today’s more valuable dollars and repay using future dollars reduced by inflation.

- Rate Arbitrage: They may take deductions at higher ordinary income rates (e.g., 24%–32%) while recapture is capped at 25%.

This front-loaded benefit is what makes depreciation such a powerful planning tool.

This means:

- All accumulated depreciation effectively disappears

- No depreciation recapture is owed

- The “loan” is never repaid

Instead of placing the entire building on a 27.5-year (or 39-year) schedule, a study identifies portions of the property that can be depreciated over much shorter time periods.

- 5-Year Assets: Appliances, furniture, carpeting, specialty lighting

- 15-Year Assets: Landscaping, fencing, driveways, pools, outdoor improvements

👉 Instead of receiving small annual deductions over decades, you receive a much larger portion of your “tax benefit loan” upfront.

For qualifying property acquired after January 19, 2025, certain assets may qualify for 100% immediate deduction in the first year.

| Feature | Standard Depreciation | With Cost Seg + Bonus |

|---|---|---|

| Year 1 Deduction | ~$3,600 per $100k | ~$20k–$40k per $100k |

| Primary Goal | Steady deductions | Front-loaded savings |

| Best Use Case | Lower/moderate income | Higher income investors |

- Reinvestment Power: Large upfront tax savings can be used to acquire additional properties

- Acceleration Effect: You benefit from compounding earlier rather than waiting decades

The Catch: Like all depreciation, these deductions are subject to recapture when the property is sold. However, when properly planned, the growth generated from early reinvestment often outweighs the future tax cost.

A “look-back” study allows you to:

- Identify missed accelerated depreciation

- Take a one-time catch-up deduction

- File using IRS Form 3115 (change in accounting method)

| Strategy | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | Year 7 | Year 8 | Year 9 | Year 10 | Sale / Recapture |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Standard 27.5-Year Depreciation | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $10K | $100K subject to recapture |

| Cost Segregation + Bonus Depreciation | $80K | $8K | $8K | $8K | $8K | $8K | $8K | $8K | $8K | $8K | Higher early recapture exposure |

| Cash Flow Impact | Big tax savings upfront | Lower | Lower | Lower | Lower | Lower | Lower | Lower | Lower | Lower | Plan before sale |

Free Tool

We’ve created a free tool that walks you through the decision process step-by-step and helps you evaluate:

- Whether to expense or depreciate an asset

- Section 179 vs bonus depreciation

- First-year tax impact

- Cash flow vs long-term tax strategy

The full depreciation toolkit is available inside the Business Membership.

| Feature | Free Lite Tool | Business Membership |

|---|---|---|

| Single Asset Analysis | ✔ | ✔ |

| Compare Expense vs Depreciation | ✔ | ✔ |

| Section 179 & Bonus Comparison | ✔ | ✔ |

| Multiple Asset Tracking | — | ✔ |

| Full Depreciation Schedule | — | ✔ |

| Cost Segmentation Planning | — | ✔ |

| Long-Term Tax Strategy Modeling | — | ✔ |

| Download / Print Reports | — | ✔ |

| Designed For | Quick decisions | Full strategy & planning |

👉 Result: You pay tax on depreciation you never received.

👉 Result: Unexpected tax bill when you sell the property or asset.

👉 Result: Disallowed deductions or penalties.

👉 Result: Large recapture later with no offsetting strategy.

👉 Result: Incorrect reporting, missed deductions, or overpaying taxes.

👉 Result: Slower cash flow growth and missed reinvestment opportunities.

👉 Result: Lost deductions or higher tax exposure.

It affects:

- How much tax you pay this year

- How much cash you keep in the business

- How quickly you can reinvest

- How much gain you may recognize when you sell

- How much depreciation recapture may apply later

But depreciation should never be treated casually. Once depreciation begins, you need to track it, report it properly, and understand how it affects your adjusted basis and future sale.

Quiz

FAQ

1. What is depreciation for business and rental property?

2. How does depreciation reduce my taxes?

3. What is depreciation recapture?

4. Can I skip taking depreciation?

5. What is the difference between Section 179 and bonus depreciation?

6. What is a cost segregation study?

7. Is depreciation always a good strategy?

8. How does depreciation apply to business equipment?

9. What happens if I sell a fully depreciated asset?

10. Can depreciation be used to offset other income?

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

![The Best Places to Buy Property for Airbnb Rental [2023]](https://retirecoast.com/wp-content/uploads/2022/06/best-places-to-buy-property-1-1-440x264.png)

{kind=link}