Updated June 2026: This comprehensive guide explains the latest tax brackets, standard deductions, senior deductions, retirement contribution limits, Roth IRA conversion opportunities, Required Minimum Distribution (RMD) rules, and 18practical strategies designed to help reduce your 2026 federal income taxes.

Navigating 2026 federal income taxes (returns due in 2027) can feel overwhelming, but with the right knowledge and a proactive approach, you can reduce your tax burden and keep more money in your pocket.

Whether you’re a family supporting dependents, a retiree utilizing enhanced senior deductions, a business owner taking advantage of tax incentives, or an investor benefiting from favorable capital gains rates, smart tax planning remains one of the most effective ways to build and preserve wealth.

This guide to 2026 federal income taxes was created in June 2026 using the most current information available at the time of publication. However, Congress can pass new tax legislation, and the Internal Revenue Service may issue new regulations, rulings, or interpretations before taxpayers must file their 2026 federal income tax returns by April 15, 2027.

```html id="tax-changes-2026"Many taxpayers assume the major tax changes arrived in 2026. In reality, much of the foundation was established when the One Big Beautiful Bill Act (OBBBA) was signed into law on July 4, 2025. The law retroactively affected the 2025 tax year and created a second wave of changes that become fully effective in 2026.

Here are five of the most important changes taxpayers should understand when comparing 2025 and 2026:

1️⃣ Higher Standard Deductions in 2026

The standard deduction increased again for 2026 due to inflation adjustments.

- Single Filers: Increased from $15,750 to $16,100

- Married Filing Jointly: Increased from $31,500 to $32,200

These higher deductions reduce taxable income for millions of taxpayers.

2️⃣ The New $6,000 Senior Deduction Continues

One of the most significant tax changes began in 2025 and continues into 2026.

- Eligible taxpayers age 65 and older may claim an additional deduction of up to $6,000.

- Married couples where both spouses qualify may receive up to $12,000 in additional deductions.

This deduction is available in addition to the traditional age-65 standard deduction increase.

3️⃣ No Tax on Tips and Overtime Remains in Effect

The new deductions for qualifying tip income and overtime compensation first appeared in 2025 but continue into 2026.

Many taxpayers should pay special attention to payroll withholding because employers may still be adjusting systems to accommodate the new rules.

Remember that some states may not follow the federal treatment of tips and overtime income.

4️⃣ New Limits on Gambling Loss Deductions

This is one of the largest tax changes that is truly new for 2026.

Prior to 2026, taxpayers could generally deduct gambling losses up to the amount of their winnings.

Beginning in 2026, itemizing taxpayers may generally deduct only 90% of gambling losses up to the amount of their gambling winnings.

This change could significantly affect frequent gamblers and professional gambling activities.

5️⃣ Popular Clean Energy Tax Credits Are Ending

Several widely used clean-energy tax incentives are being phased out much sooner than originally expected.

Many taxpayers will lose access to benefits such as:

- New Clean Vehicle Credits

- Used Clean Vehicle Credits

- Energy Efficient Home Improvement Credits

- Certain Residential Energy Credits

For many programs, vehicles must be acquired or property placed in service before December 31, 2025, to qualify.

Tax law changes

Because tax laws can change during the year, we encourage readers to bookmark this page and check back periodically.

Any significant updates affecting 2026 federal income taxes, including tax brackets, deductions, credits, retirement account rules, Roth IRA conversions, Required Minimum Distributions (RMDs), and other planning opportunities, will be highlighted here as we become aware of them.

The most successful taxpayers do not wait until filing season to think about taxes. Instead, they plan throughout the year, taking advantage of deductions, credits, retirement contributions, and other strategies that can legally reduce their federal income tax liability.

This guide will help you understand the rules, identify opportunities, and make informed decisions that may help you keep more of your hard-earned money.

🧠 2026 Federal Income Taxes Quiz

Test your knowledge of the 2026 federal income tax rules and see how much you learned from this guide.

Question 1: Which retirement account is generally not subject to Required Minimum Distributions (RMDs) during the owner's lifetime?

A. Traditional IRA

B. SEP IRA

C. Roth IRA

D. SIMPLE IRA

Answer: C. Roth IRA

Roth IRAs generally do not require lifetime RMDs for the original account owner.

Question 2: What is one of the primary benefits of a Roth IRA conversion?

A. Eliminates all taxes forever

B. Creates tax-free retirement income if requirements are met

C. Eliminates Social Security taxes

D. Increases Required Minimum Distributions

Answer: B. Creates tax-free retirement income if requirements are met

Roth IRA conversions may help reduce future taxable retirement income and future RMDs.

Question 3: Why should employees receiving tips monitor their pay stubs carefully under the new No Tax on Tips rules?

A. Tips are never taxable

B. Employers may withhold more tax than necessary

C. Tips no longer need to be reported

D. Social Security taxes disappear

Answer: B. Employers may withhold more tax than necessary

Payroll systems may not fully reflect the new federal deduction rules.

Question 4: Which of the following may reduce your federal taxable income?

A. Contributing to a Traditional IRA

B. Contributing to an HSA

C. Contributing to a 401(k)

D. All of the above

Answer: D. All of the above

All three may provide tax benefits depending on your circumstances.

Question 5: Why do many retirees perform Roth IRA conversions before RMDs begin?

A. To increase Medicare premiums

B. To reduce future Required Minimum Distributions

C. To eliminate investment risk

D. To avoid reporting income

Answer: B. To reduce future Required Minimum Distributions

Reducing Traditional IRA balances can lower future RMDs and future taxable income.

Question 6: Which retirement accounts are generally subject to RMD rules?

A. Traditional IRAs

B. SEP IRAs

C. SIMPLE IRAs

D. All of the above

Answer: D. All of the above

Traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k)s, and many other retirement plans are subject to RMD requirements.

Question 7: True or False: State tax laws always match federal tax laws.

A. True

B. False

Answer: B. False

States frequently have different deductions, exemptions, credits, and tax rates than the federal government.

Question 8: What is one potential benefit of the new American-made vehicle interest deduction?

A. It may be available even if you take the standard deduction

B. It eliminates all vehicle costs

C. It applies to every vehicle sold worldwide

D. It eliminates sales taxes

Answer: A. It may be available even if you take the standard deduction

This makes the deduction particularly valuable for taxpayers who do not itemize.

Question 9: Why are Health Savings Accounts (HSAs) considered powerful tax-planning tools?

A. Contributions may be tax deductible

B. Earnings may grow tax free

C. Qualified medical withdrawals may be tax free

D. All of the above

Answer: D. All of the above

HSAs offer what many financial experts call a "triple tax advantage."

Question 10: What is often the biggest mistake taxpayers make regarding tax planning?

A. Planning too early

B. Ignoring taxes until filing season

C. Contributing to retirement accounts

D. Tracking expenses

Answer: B. Ignoring taxes until filing season

Many tax-saving opportunities require action throughout the year rather than at filing time.

📊 Your Score

8–10 Correct: Excellent! You have a strong understanding of 2026 federal income tax planning.

5–7 Correct: Good job. Review the sections on retirement planning, Roth conversions, and tax-saving strategies.

0–4 Correct: Consider rereading the article and using the RetireCoast calculators to strengthen your tax-planning knowledge.

NEW FOR 2026: HIGHER STANDARD DEDUCTIONS AND ENHANCED SENIOR TAX BENEFITS

The federal tax rules for 2026 include inflation-adjusted tax brackets, larger standard deductions, increased retirement contribution limits, and continued enhanced deductions for many taxpayers age 65 and older.

A married couple filing jointly may qualify for:

- Standard Deduction: $32,200

- Additional Age 65+ Deduction

- Additional Senior Deduction of up to $12,000 for qualifying couples

Combined, many retired couples may be able to shield a significant amount of income from federal taxation before considering other deductions and credits.

Effective tax planning is one of the easiest ways to improve your financial situation. There is no reason to pay more federal income tax than legally required, and there is also no reason to have substantially more withheld from your paycheck than necessary to meet your tax obligations.

Many taxpayers unknowingly provide the government with an interest-free loan throughout the year by over-withholding taxes from their paychecks. While receiving a large refund may feel rewarding, it often means that money could have been working for you throughout the year instead.

Proper planning can help you:

- Reduce your overall tax burden.

- Adjust withholding to better match your actual tax liability.

- Improve monthly cash flow.

- Plan for retirement distributions and Roth conversions.

- Evaluate business and investment opportunities.

- Avoid unpleasant tax surprises at filing time.

Visit our Calculator Hub to access a growing collection of free tax, retirement, investment, business, and financial planning calculators designed to help you make informed decisions throughout the year.

For readers seeking more advanced planning tools, scenario analysis, and wealth-preservation resources, our premium membership programs provide access to additional calculators, guides, and decision-making tools that go far beyond basic tax preparation.

WHY TAX PLANNING MATTERS NOW

The best tax strategies are implemented throughout the year—not in April when the return is due.

Many tax-saving opportunities require action before December 31, including:

- Retirement plan contributions

- Roth IRA conversion strategies

- Tax-loss harvesting

- Charitable giving

- Small business purchases

- Health Savings Account contributions

Waiting until tax season often means the opportunity has already passed.

REQUIRED MINIMUM DISTRIBUTIONS (RMDS) CONTINUE TO IMPACT RETIREES

If you have Traditional IRAs, SEP IRAs, SIMPLE IRAs, or employer-sponsored retirement plans, Required Minimum Distributions (RMDs) may affect your tax situation.

For most retirees:

- RMD age is now 73

- Individuals born in 1960 or later begin RMDs at age 75

- Failure to take required distributions can result in significant IRS penalties

Proper planning can reduce the tax impact of RMDs while helping preserve retirement assets.

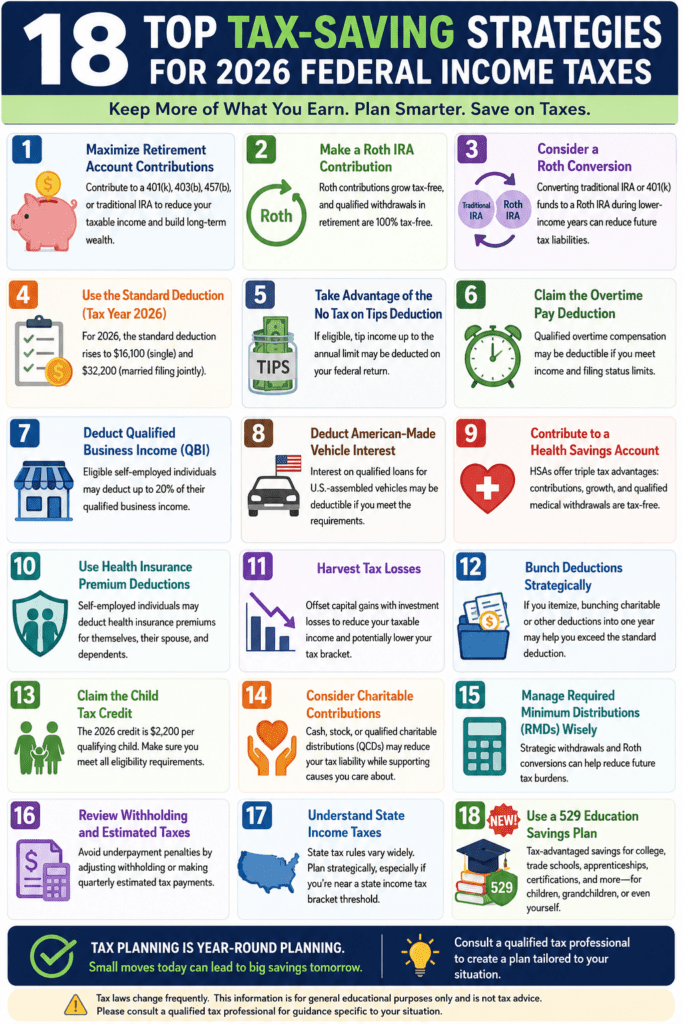

18 PRACTICAL TAX-SAVING STRATEGIES FOR 2026

This guide outlines 18 practical tax-saving strategies that may help reduce your federal income tax liability for 2026, including:

- Retirement account optimization

- Child Tax Credits

- Education credits

- Long-term capital gains planning

- Roth IRA conversions

- Health Savings Accounts

- Small business deductions

- Strategic charitable giving

- RMD planning

Whether you are employed, retired, self-employed, or operating a small business, understanding these opportunities can help you legally minimize taxes and improve your financial future.

FEDERAL INCOME TAX BRACKETS FOR 2026

The Internal Revenue Service adjusts federal income tax brackets annually for inflation.

Single Filers

| Tax Rate | Taxable Income |

|---|---|

| 10% | $0 – $12,400 |

| 12% | $12,401 – $50,400 |

| 22% | $50,401 – $105,700 |

| 24% | $105,701 – $201,775 |

| 32% | $201,776 – $256,225 |

| 35% | $256,226 – $640,600 |

| 37% | Over $640,600 |

Married Filing Jointly

| Tax Rate | Taxable Income |

|---|---|

| 10% | $0 – $24,800 |

| 12% | $24,801 – $100,800 |

| 22% | $100,801 – $211,400 |

| 24% | $211,401 – $403,550 |

| 32% | $403,551 – $512,450 |

| 35% | $512,451 – $768,700 |

| 37% | Over $768,700 |

These annual adjustments help prevent taxpayers from being pushed into higher tax brackets solely because of inflation.

STANDARD DEDUCTION FOR 2026

The standard deduction remains one of the most valuable tax benefits available to taxpayers.

2026 Standard Deduction Amounts

| Filing Status | Deduction |

|---|---|

| Single | $16,100 |

| Married Filing Jointly | $32,200 |

| Head of Household | $24,150 |

Many taxpayers will benefit more from claiming the standard deduction than itemizing deductions.

ENHANCED SENIOR DEDUCTIONS FOR 2026

Taxpayers age 65 and older may qualify for additional deductions beyond the standard deduction.

Additional Senior Deduction

| Filing Status | Additional Deduction |

|---|---|

| Single Age 65+ | Up to $6,000 |

| Married Couple Both Age 65+ | Up to $12,000 |

Combined with the standard deduction, many retirees can exclude a substantial amount of income from taxation.

This provision is subject to income limitations and phase-outs for higher-income taxpayers.

One of the most significant tax changes for retirees is the new Enhanced Senior Deduction. Depending on your income and filing status, this deduction could substantially reduce your taxable income and federal tax bill.

Use our free Form 1040-SR Tax Forecast Tool to estimate:

- Taxable Social Security benefits

- IRA and retirement account withdrawals

- Pension and annuity income

- The impact of the new senior deduction

- Your estimated refund or amount owed

Updated for 2026 tax planning and retirement income forecasting.

RETIREMENT CONTRIBUTION LIMITS FOR 2026

Retirement plans remain one of the most effective tax-saving tools available.

IRA Contribution Limits

- Traditional IRA: $7,500

- Roth IRA: $7,500

- Catch-Up Contribution (Age 50+): Additional $1,100

Employer Retirement Plans

- 401(k), 403(b), and TSP Plans: $24,500

- Catch-Up Contribution (Age 50+): $8,000

- Special Catch-Up (Age 60-63): $11,250

The ability to defer taxes today while building future retirement assets makes these accounts a cornerstone of effective tax planning.

```htmlMany retirees discover that starting a business after retirement can be an excellent way to create additional income, stay active, pursue a passion, and potentially benefit from valuable tax advantages. Whether you are considering a consulting business, online business, vacation rental operation, real estate investment company, or another venture, proper planning can significantly improve your chances of success.

At RetireCoast, we have created an extensive series of articles dedicated to helping retirees navigate the process of launching, managing, and growing a business during retirement.

Explore These Resources:

-

📚 Starting a Business After Retirement Complete Series

Explore our comprehensive collection of articles covering business formation, financing, taxes, marketing, operations, and long-term planning.

View the Complete Series -

💼 Business Builder Membership

Gain access to advanced business tools, calculators, templates, planning resources, and guides designed specifically for entrepreneurs, retirees, and small business owners.

Learn More About the Business Builder Membership

If you have ever considered starting a business after retirement, our article series and Business Builder Membership may be exactly what you are looking for.

STARTING A BUSINESS AFTER RETIREMENT: TAX BENEFITS

Starting a business after retirement can provide both additional income and substantial tax advantages.

Potential benefits include:

- Deductible startup costs

- Home office deductions

- Business vehicle deductions

- Retirement plan contributions

- Health insurance deductions

- Qualified Business Income (QBI) deductions

- Travel and mileage deductions

- Equipment depreciation

- Professional service deductions

- Family employment opportunities

For many retirees, even a small part-time business can create legitimate deductions that reduce overall tax liability while generating supplemental income.

As always, consult with a qualified tax professional before implementing any tax strategy.

2026 Federal Income Taxes Strategy #1: Maximize Retirement Contributions

One of the most effective ways to reduce your 2026 federal income taxes is by maximizing contributions to tax-advantaged retirement accounts.

Contributions to Traditional IRAs and employer-sponsored retirement plans may reduce your taxable income while helping build long-term retirement security.

Traditional IRA Contributions and 2026 Federal Income Taxes

A Traditional IRA may provide an immediate tax deduction depending on your income and participation in an employer retirement plan.

For 2026:

- IRA Contribution Limit: $7,500

- Catch-Up Contribution Age 50+: Additional $1,100

The immediate deduction can lower your current-year federal income taxes while allowing investments to grow tax deferred.

Roth IRA Contributions and Future Federal Income Taxes

Although Roth IRA contributions are not deductible today, qualified withdrawals during retirement are completely tax free.

A Roth IRA may be particularly attractive if you believe your tax rate will be higher in the future.

Employer Retirement Plans and 2026 Federal Income Taxes

For 2026:

- 401(k), 403(b), and TSP Contribution Limit: $24,500

- Catch-Up Contribution Age 50+: $8,000

- Enhanced Catch-Up Age 60-63: $11,250

Retirement plan contributions remain one of the largest legal opportunities to reduce federal taxable income.

2026 Federal Income Taxes Strategy #2: Use the Standard Deduction and Senior Deductions

The standard deduction is the simplest way to reduce taxable income without tracking itemized expenses.

Standard Deduction for 2026 Federal Income Taxes

For 2026:

| Filing Status | Standard Deduction |

|---|---|

| Single | $16,100 |

| Married Filing Jointly | $32,200 |

| Head of Household | $24,150 |

Most taxpayers benefit from taking the standard deduction rather than itemizing.

Senior Deductions and 2026 Federal Income Taxes

Taxpayers age 65 and older may qualify for additional deductions.

For qualifying retirees:

- Up to $6,000 additional deduction for eligible individuals.

- Up to $12,000 additional deduction for eligible married couples.

Combined with the standard deduction, many retirees can significantly reduce taxable income before considering additional tax credits or deductions.

When Itemizing May Reduce Federal Income Taxes

Itemizing may still be beneficial if your deductible expenses exceed the standard deduction.

Common itemized deductions include:

- Mortgage interest

- State and local taxes

- Charitable contributions

- Qualified medical expenses

Always compare both methods before filing.

2026 Federal Income Taxes Strategy #3: Claim the Child Tax Credit

The Child Tax Credit remains one of the most valuable tax benefits available to families.

Child Tax Credit and 2026 Federal Income Taxes

Eligible taxpayers may receive a credit for each qualifying child under age 17.

Tax credits are particularly valuable because they reduce taxes dollar for dollar rather than merely reducing taxable income.

Example of Child Tax Credit Savings

Consider a married couple with two qualifying children.

If eligible for the full credit, they could potentially reduce their federal tax bill by thousands of dollars.

Families should verify income limitations and eligibility requirements before claiming the credit.

Other Family Tax Benefits

Additional benefits may include:

- Child and Dependent Care Credit

- Adoption Credits

- Earned Income Tax Credit

These credits can substantially reduce federal income taxes for qualifying households.

2026 Federal Income Taxes Strategy #4: Take Advantage of Education Tax Credits

Education credits continue to provide valuable tax savings for students, working adults, and retirees pursuing additional education.

Lifetime Learning Credit and 2026 Federal Income Taxes

The Lifetime Learning Credit may provide up to $2,000 per tax return.

Eligible expenses generally include:

- Tuition

- Required fees

- Books and supplies required for coursework

Unlike some education credits, the Lifetime Learning Credit can be claimed for an unlimited number of years.

Continuing Education and Tax Savings

Many individuals take courses to:

- Improve job skills

- Transition into retirement businesses

- Learn technology skills

- Pursue certifications

The Lifetime Learning Credit can help offset these educational expenses while reducing federal income taxes.

Our article Tax Planning for Gen X Retirees can help you navigate a complicated tax advantaged landscape.

2026 Federal Income Taxes Strategy #5: Use Long-Term Capital Gains Tax Rates

Investors often overlook one of the most powerful tax planning opportunities available.

Long-Term Capital Gains and 2026 Federal Income Taxes

Assets held for more than one year generally qualify for long-term capital gains treatment.

Long-term gains are typically taxed at lower rates than ordinary income.

Current long-term capital gains rates remain:

- 0%

- 15%

- 20%

depending upon taxable income.

Why Holding Investments Longer May Reduce Federal Income Taxes

Selling investments after holding them for more than one year may significantly reduce taxes compared to short-term trading.

Short-term gains are taxed at ordinary income tax rates, which can be substantially higher.

Example of Capital Gains Tax Savings

Suppose an investor sells stock after holding it for two years.

Instead of paying ordinary income tax rates, the gain may qualify for a lower long-term capital gains rate, potentially saving thousands of dollars.

Strategic investment holding periods remain one of the easiest ways to legally reduce federal income taxes.

For SEO, the next section should cover Strategies #6–#10:

- HSA and FSA Contributions

- Tax Loss Harvesting

- Filing Status Optimization

- State Tax Planning

- Additional Retirement Plan Contributions

These naturally support your RetireCoast audience of retirees, investors, and small business owners.

Many people like you are discovering that a Health Savings Account (HSA) is far more versatile than they initially realized. While HSAs were originally designed to help pay medical expenses, they have evolved into one of the most powerful long-term wealth-building and tax-planning tools available.

For investors who have already maxed out their Roth IRA and 401(k) contributions, an HSA can provide another opportunity to save and invest using valuable tax advantages.

- ✅ Contributions may be tax deductible.

- ✅ Investment earnings can grow tax free.

- ✅ Qualified medical withdrawals are tax free.

Because of this unique combination, many financial planners and retirement experts consider the HSA to be one of the most tax-efficient accounts available. In fact, some experts argue that it may be the best of all tax-advantaged accounts because it combines features of both Traditional IRAs and Roth IRAs while providing additional benefits for healthcare expenses.

Read our detailed guide:

👉 Tax-Advantaged Retirement Accounts

https://retirecoast.com/tax-advantaged-retirement-accounts/

This article explains how HSAs, Roth IRAs, Traditional IRAs, 401(k)s, SEP IRAs, and other retirement accounts compare, helping you determine which accounts may best fit your long-term financial goals.

2026 Federal Income Taxes Strategy #6: Maximize HSA and FSA Contributions

Health care costs continue to rise, making tax-advantaged medical accounts more valuable than ever.

Health Savings Accounts and 2026 Federal Income Taxes

Health Savings Accounts (HSAs) provide a triple tax advantage:

- Contributions may be tax deductible.

- Earnings grow tax free.

- Qualified withdrawals are tax free.

For 2026:

| Coverage Type | Contribution Limit |

|---|---|

| Self-Only Coverage | $4,400 |

| Family Coverage | $8,750 |

| Catch-Up Contribution (Age 55+) | Additional $1,000 |

Many financial professionals consider HSAs one of the best tax-saving tools available.

Flexible Spending Accounts and 2026 Federal Income Taxes

Flexible Spending Accounts (FSAs) also allow taxpayers to pay qualified medical expenses with pre-tax dollars.

For 2026:

- Maximum Employee Contribution: $3,400

- Maximum Carryover: $680

These accounts can reduce taxable income while helping cover medical expenses throughout the year.

2026 Federal Income Taxes Strategy #7: Use Tax-Loss Harvesting

Market declines can create valuable tax planning opportunities.

Tax-Loss Harvesting and 2026 Federal Income Taxes

Tax-loss harvesting involves selling investments that have declined in value to offset gains from profitable investments.

Potential benefits include:

- Offsetting capital gains

- Reducing taxable investment income

- Lowering overall federal income taxes

Capital Loss Rules

Taxpayers may generally:

- Offset unlimited capital gains

- Deduct up to $3,000 annually against ordinary income

- Carry excess losses forward to future tax years

Avoid the Wash Sale Rule

The IRS wash sale rule may disallow losses if substantially identical securities are repurchased within 30 days before or after the sale.

Careful planning is essential when using this strategy.

People Also Ask About 2026 Federal Income Taxes

Can I reduce my 2026 federal income taxes without itemizing deductions?

Yes. Most taxpayers now claim the standard deduction rather than itemizing. However, there are still many ways to reduce your tax burden, including contributing to retirement accounts, Health Savings Accounts (HSAs), utilizing Roth IRA conversion strategies, claiming available tax credits, and taking advantage of certain above-the-line deductions that may be available even if you use the standard deduction.

How can retirees legally reduce their 2026 federal income taxes?

Retirees may be able to reduce federal income taxes through strategic Roth IRA conversions, Qualified Charitable Distributions (QCDs), careful management of Required Minimum Distributions (RMDs), tax-efficient withdrawal strategies, and by taking advantage of enhanced senior deductions.

Proper planning before RMDs begin can often produce significant long-term tax savings.

Will state income taxes follow the same rules as my federal tax return?

Not necessarily. State income tax laws frequently differ from federal tax laws. Some states do not recognize certain federal deductions, exemptions, or credits. For example, a deduction allowed on your federal return may still be taxable at the state level. Taxpayers should review both federal and state tax rules when developing a tax planning strategy.

These three questions target strong search intent and fit naturally into the article:

- reduce taxes without itemizing

- retiree tax planning

- state vs federal tax differences

All three are common Google “People Also Ask” topics related to income taxes.

2026 Federal Income Taxes Strategy #8: Optimize Your Filing Status

Your filing status affects nearly every aspect of your tax return.

Filing Status and 2026 Federal Income Taxes

The primary filing statuses include:

- Single

- Married Filing Jointly

- Married Filing Separately

- Head of Household

- Qualifying Surviving Spouse

Choosing the correct status can significantly impact tax liability.

Married Filing Jointly vs. Married Filing Separately

Most married couples benefit from filing jointly because of:

- Larger standard deductions

- More favorable tax brackets

- Access to additional credits and deductions

However, filing separately may occasionally be advantageous when:

- One spouse has unusually high medical expenses.

- Income-based repayment plans are involved.

- Certain liability concerns exist.

Head of Household Benefits

Single taxpayers supporting dependents may qualify for Head of Household status.

Benefits may include:

- Lower tax rates

- Higher standard deductions

- Increased eligibility for certain credits

Reviewing filing status annually can reduce federal income taxes and improve tax efficiency.

```html id="state-tax-warning"

Many taxpayers focus almost exclusively on their federal income taxes and overlook an important fact: state income tax laws do not always mirror federal tax laws. A deduction, exemption, or credit available on your federal return may not be available on your state return.

For example, the new federal deduction for qualifying tip income may reduce federal taxes for eligible workers, but some states have indicated they will continue taxing tips under state law. California is one example where taxpayers may still face state income taxes on tip income even though they receive favorable treatment at the federal level.

- ✅ Review both federal and state tax rules.

- ✅ Verify whether deductions are recognized by your state.

- ✅ Understand how retirement income is taxed.

- ✅ Check state treatment of Social Security benefits.

- ✅ Review state taxation of tips, capital gains, and business income.

- ✅ Consider local income taxes where applicable.

One reason for the massive internal migration occurring across the United States is that many individuals and retirees are moving away from high-tax states and relocating to areas with lower overall tax burdens. For some households, the savings can amount to thousands of dollars per year.

Several states impose no state income tax, while others provide favorable treatment for retirement income, pensions, Social Security benefits, and IRA withdrawals. These differences can have a significant impact on long-term wealth preservation.

2026 Federal Income Taxes Strategy #9: Plan for State Income Taxes

Although this article focuses on federal income taxes, state tax planning can have a significant impact on your overall financial picture.

State Tax Planning and 2026 Federal Income Taxes

Several states do not impose a state income tax.

Examples include:

- Florida

- Texas

- Tennessee

- Nevada

- Wyoming

- South Dakota

Retirees often consider relocating to lower-tax states to improve cash flow and preserve retirement assets.

Retirement Income Tax Treatment

State tax treatment varies significantly.

Some states:

- Exempt Social Security benefits.

- Exempt pension income.

- Exempt IRA and 401(k) withdrawals.

Mississippi remains one of the most retirement-friendly states because qualified retirement income is generally exempt from state income taxation.

Relocation and Tax Savings

For retirees considering a move, evaluating both federal and state tax consequences can provide substantial long-term savings.

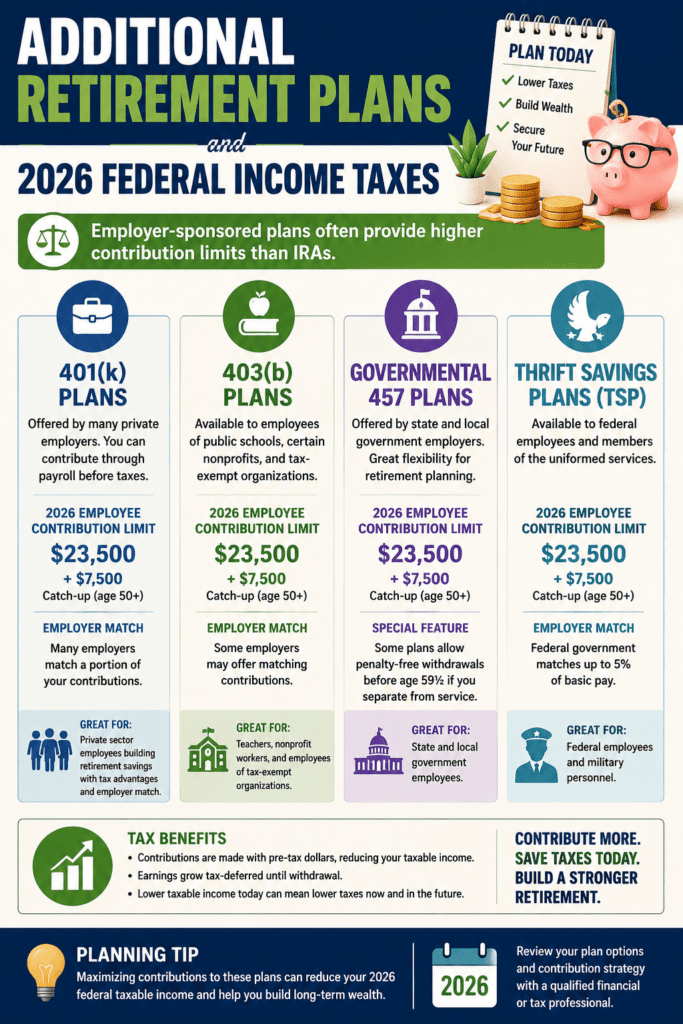

2026 Federal Income Taxes Strategy #10: Use Additional Retirement Plans to Reduce Taxes

Many taxpayers focus only on IRAs and overlook other powerful retirement savings options.

Additional Retirement Plans and 2026 Federal Income Taxes

Employer-sponsored plans often provide higher contribution limits than IRAs.

Examples include:

- 401(k) Plans

- 403(b) Plans

- Governmental 457 Plans

- Thrift Savings Plans (TSP)

Contributions generally reduce taxable income in the year they are made.

Self-Employed Retirement Plans

Business owners and self-employed individuals may have access to additional opportunities.

Popular options include:

SEP IRA

A SEP IRA allows business owners to contribute a percentage of business income into a retirement account while receiving valuable tax deductions.

Solo 401(k)

Solo 401(k) plans often provide the highest contribution limits for self-employed individuals with no employees.

Benefits include:

- Large tax deductions

- Potential Roth options

- Catch-up contributions

Why Retirement Plans Remain Powerful Tax Tools

Contributions reduce current taxable income while investments continue growing tax deferred.

For many taxpayers, maximizing retirement contributions remains one of the most effective strategies for reducing 2026 federal income taxes while building long-term financial security.

The next section should cover Strategies #11–#15:

- Roth IRA Conversions

- Charitable Contribution Strategies

- Required Minimum Distribution (RMD) Planning

- Hiring Family Members in a Business

- Working With a Tax Professional

Those sections fit especially well with your RetireCoast audience and will naturally lead into the expanded Roth conversion and RMD discussions later in the article.

2026 Federal Income Taxes Strategy #11: Consider Strategic Roth IRA Conversions

Many retirees and near-retirees overlook one of the most powerful long-term tax planning opportunities available.

Roth IRA Conversions and 2026 Federal Income Taxes

A Roth conversion occurs when funds are moved from a Traditional IRA or qualified retirement account into a Roth IRA.

The amount converted becomes taxable income in the year of the conversion, but future qualified withdrawals become tax free.

When a Roth Conversion May Reduce Future Federal Income Taxes

A Roth conversion may make sense when:

- You are temporarily in a lower tax bracket.

- You have recently retired.

- You have experienced a reduction in income.

- You expect tax rates to increase in the future.

- You want to reduce future Required Minimum Distributions (RMDs).

Benefits of Roth Conversions

Potential advantages include:

- Tax-free retirement withdrawals

- Reduced future RMDs

- Greater retirement income flexibility

- Tax-free growth

- Improved estate planning opportunities

Many retirees gradually convert portions of their Traditional IRA balances over several years to avoid moving into higher tax brackets.

2026 Federal Income Taxes Strategy #12: Consider Charitable Contributions Carefully

Giving to charity can support worthy causes, strengthen communities, and help organizations that perform valuable work. However, taxpayers should understand that recent tax law changes have significantly reduced the tax benefits previously associated with charitable giving for many Americans.

Warning: Charitable Giving Tax Laws Have Changed

Many taxpayers grew accustomed to receiving substantial tax deductions for charitable contributions. However, changes in tax law, combined with larger standard deductions, mean that far fewer taxpayers now receive a meaningful federal income tax deduction for their charitable donations.

This does not mean you should avoid charitable giving. It simply means that charitable contributions should be made because you support the cause—not because you expect a significant tax deduction.

Before making large donations, consider how the current tax rules may affect your specific situation.

Charitable Contributions and 2026 Federal Income Taxes

Some taxpayers who itemize deductions may still qualify for charitable contribution deductions when donating to eligible organizations.

Potentially deductible contributions may include:

- Cash donations

- Securities and stocks

- Real estate

- Certain personal property

Always retain documentation supporting your contributions, including receipts, acknowledgments, and appraisals when required.

Larger Standard Deductions Have Reduced the Value of Many Charitable Deductions

Because standard deductions have increased substantially, many taxpayers no longer itemize deductions.

As a result, charitable contributions often provide little or no direct federal tax benefit.

For many households, charitable giving should now be viewed primarily as a personal, religious, or community-support decision rather than a tax-reduction strategy.

Bunching Charitable Contributions

Some taxpayers continue to use a strategy known as “bunching.”

Instead of making similar donations every year, they combine multiple years of charitable giving into a single tax year.

This approach may allow them to:

- Exceed the standard deduction threshold

- Itemize deductions in that year

- Potentially recover some tax benefits that would otherwise be lost

However, taxpayers should carefully review current tax rules before relying on this strategy.

Donor-Advised Funds

Donor-Advised Funds (DAFs) remain a popular planning tool for individuals with substantial charitable goals.

Potential benefits include:

- Simplified charitable administration

- The ability to make grants over time

- Centralized recordkeeping

- Potential tax benefits for qualifying taxpayers

However, taxpayers should not assume that contributions to a DAF will automatically result in significant tax savings under current law.

Qualified Charitable Distributions May Still Benefit Retirees

Retirees age 70½ and older may wish to consider Qualified Charitable Distributions (QCDs) from their IRAs.

A QCD allows funds to be transferred directly from an IRA to a qualified charity.

Potential benefits include:

- Satisfying Required Minimum Distribution (RMD) requirements

- Reducing taxable income

- Supporting charitable causes

For many retirees, QCDs may provide more tax value than traditional charitable contribution deductions.

The Bottom Line on Charitable Giving and 2026 Federal Income Taxes

Charitable giving remains an important personal and community decision. However, taxpayers should recognize that many of the federal income tax benefits that once accompanied charitable donations have been reduced or eliminated for a large percentage of Americans.

Support the causes you believe in, but do not assume that charitable contributions will significantly reduce your federal income taxes. Always review current tax laws and consult a qualified tax professional before making major charitable giving decisions based on expected tax benefits.

For taxpayers with substantial charitable goals, DAFs can be highly effective planning tools.

2026 Federal Income Taxes Strategy #13: Plan Carefully for Required Minimum Distributions (RMDs)

Required Minimum Distributions continue to be one of the most important retirement tax issues.

RMD Planning and 2026 Federal Income Taxes

Most taxpayers must begin taking RMDs from traditional retirement accounts at age 73.

Individuals born in 1960 or later generally begin RMDs at age 75.

Accounts subject to RMDs include:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- 401(k) Plans

- 403(b) Plans

Why RMD Planning Matters

RMD withdrawals are generally taxed as ordinary income.

Large distributions may:

- Push retirees into higher tax brackets

- Increase taxation of Social Security benefits

- Increase Medicare premium surcharges

- Reduce eligibility for certain tax benefits

Qualified Charitable Distributions (QCDs)

Taxpayers age 70½ or older may transfer funds directly from an IRA to a qualified charity.

Benefits include:

- Satisfying RMD requirements

- Excluding the distribution from taxable income

- Supporting charitable organizations

For many retirees, QCDs provide one of the most effective methods for managing RMD-related taxes.

2026 Federal Income Taxes Strategy #14: Hire Family Members in Your Business

Business owners may create legitimate tax savings opportunities by employing family members.

Family Employment and 2026 Federal Income Taxes

When structured properly, wages paid to family members may:

- Create a business deduction

- Shift income into lower tax brackets

- Provide retirement savings opportunities for family members

Potential Benefits of Hiring Children

Children may perform legitimate services such as:

- Filing documents

- Administrative assistance

- Website maintenance

- Social media management

- Marketing support

Compensation must be reasonable and supported by proper records.

Retirement Benefits for Family Members

Employment income may allow family members to:

- Contribute to Roth IRAs

- Build retirement savings early

- Learn valuable financial skills

This strategy can provide benefits to both the business owner and family members. Want to know more about how to manage your business, check out our Business Membership.

2026 Federal Income Taxes Strategy #15: Work With a Qualified Tax Professional

Even taxpayers who prepare their own returns can benefit from professional guidance.

Tax Professionals and 2026 Federal Income Taxes

A qualified tax professional may help identify:

- Tax credits

- Deductions

- Retirement planning opportunities

- Roth conversion strategies

- Business tax savings

- Estate planning opportunities

Why Professional Guidance Matters

Tax laws change frequently.

A tax professional can help ensure that you:

- Remain compliant with IRS rules

- Avoid costly mistakes

- Take advantage of available tax-saving opportunities

The Value of Year-Round Tax Planning

Many taxpayers only meet with a tax professional during filing season.

However, the greatest tax savings often occur when planning takes place throughout the year rather than after the year has ended.

Proactive planning can help reduce 2026 federal income taxes while supporting long-term financial goals.

2026 Federal Income Taxes Strategy #16: Understand the New No Tax on Tips Rules

One of the most significant tax law changes affecting millions of workers is the new federal deduction for qualifying tip income.

This provision creates opportunities for tax savings, but it also creates new planning challenges because the deduction operates outside many traditional tax planning strategies.

Workers who receive tips should pay close attention to how this new law affects their personal situation.

Why the No Tax on Tips Law Matters

For years, employees who received tips generally paid federal income taxes on those earnings.

Under the new law, qualifying taxpayers may be able to deduct eligible tip income from federal taxable income, potentially reducing their federal income tax liability.

For workers in restaurants, hospitality, tourism, personal services, transportation, and other tip-based occupations, this could result in substantial tax savings.

Interactive Tool Included

This article contains a free No Tax on Tips Calculator that can estimate your potential federal tax savings.

Tax Planning and the No Tax on Tips Law

This new deduction introduces a unique challenge.

Many payroll systems and withholding formulas were designed before the law was enacted.

As a result, some employers may continue withholding federal income taxes as if tip income remains fully taxable.

This can lead to employees having significantly more tax withheld during the year than is ultimately required.

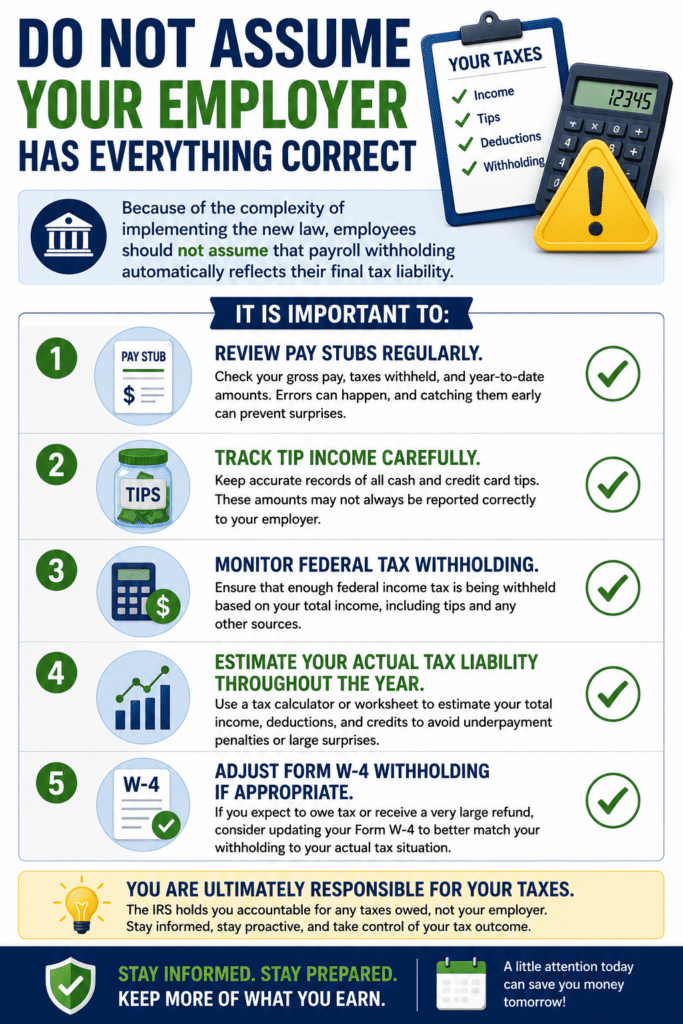

Do Not Assume Your Employer Has Everything Correct

Because of the complexity of implementing the new law, employees should not assume that payroll withholding automatically reflects their final tax liability.

It is important to:

- Review pay stubs regularly.

- Track tip income carefully.

- Monitor federal tax withholding.

- Estimate your actual tax liability throughout the year.

- Adjust Form W-4 withholding if appropriate.

Taking the initiative may improve monthly cash flow and reduce the likelihood of overpaying taxes throughout the year.

State Income Taxes May Still Apply

The federal government and state governments operate under separate tax systems.

Even if qualifying tip income receives favorable federal treatment, some states may continue to tax tip income under state law.

For example, states such as California have indicated that they may continue taxing tip income for state income tax purposes regardless of federal treatment.

As a result, taxpayers may find themselves in the unusual position of:

- Receiving a federal tax benefit.

- Still owing state income taxes on the same income.

Workers should review the rules applicable to their state and avoid assuming that federal and state tax treatment will be identical.

Recordkeeping Remains Important

The new law does not eliminate the need for accurate records.

Employees should continue maintaining records of:

- Reported tips

- Credit card tips

- Cash tips

- Employer tip reports

- Payroll records

Good documentation can help support deductions and simplify tax preparation.

The Bottom Line on No Tax on Tips

The new federal deduction for qualifying tip income may provide meaningful tax savings for millions of workers. However, because payroll systems, withholding calculations, and state tax laws may not immediately align with the new federal rules, taxpayers should remain proactive.

Carefully monitoring withholding, tracking tip income, and understanding your state’s treatment of tips may help you avoid overpaying taxes and improve your overall tax planning strategy for 2026.

2026 Federal Income Taxes Strategy #17: Consider the New American-Made Vehicle Interest Deduction

A new tax benefit may be available to taxpayers who purchase qualifying American-made vehicles and finance the purchase.

This deduction is particularly noteworthy because it may be claimed even if you do not itemize deductions.

Why This Deduction Matters

Historically, taxpayers claiming the standard deduction generally received little or no tax benefit from personal vehicle loan interest.

Under the new law, qualifying taxpayers may be able to deduct eligible vehicle loan interest associated with certain American-made vehicles.

For many buyers, this creates a tax benefit that did not previously exist.

This Deduction Is in Addition to the Standard Deduction

One of the most important features of this new tax provision is that it may be claimed in addition to the standard deduction.

In other words, taxpayers generally do not need to choose between:

- Claiming the standard deduction, or

- Claiming the qualifying vehicle interest deduction.

Eligible taxpayers may be able to claim both.

This makes the deduction especially valuable because most Americans now use the standard deduction rather than itemizing deductions.

Potential Tax Savings

For taxpayers financing a qualifying vehicle, deductible interest may reduce taxable income and lower federal income taxes.

The actual tax savings will depend on:

- The amount of interest paid

- Your tax bracket

- Income limitations

- Vehicle eligibility requirements

Verify Vehicle Eligibility

Not every vehicle qualifies.

Taxpayers should verify:

- The vehicle was manufactured in the United States.

- The vehicle meets all federal requirements.

- Income limitations do not apply.

- The financing arrangement qualifies under IRS rules.

Because this is a relatively new tax provision, additional IRS guidance may be issued in the future.

Tax Planning Opportunities

If you are already planning to purchase a vehicle, the deduction may influence your decision when comparing:

- American-made vehicles versus imported vehicles

- Financing versus cash purchases

- New versus replacement vehicles

For some taxpayers, the deduction may reduce the effective cost of financing.

Keep Good Records

Taxpayers claiming this deduction should retain:

- Purchase agreements

- Financing documents

- Annual loan statements

- Records showing interest paid during the year

Proper documentation will be important if questions arise regarding eligibility.

The Bottom Line on the American-Made Vehicle Deduction

The new deduction for interest paid on qualifying American-made vehicles represents one of the more unusual tax benefits available in 2026. Because it may be claimed in addition to the standard deduction, it provides a tax benefit that many taxpayers would not otherwise receive.

If you are considering purchasing a new vehicle, review the current IRS guidance and eligibility requirements carefully. The deduction may help reduce your federal income taxes while supporting American manufacturing.

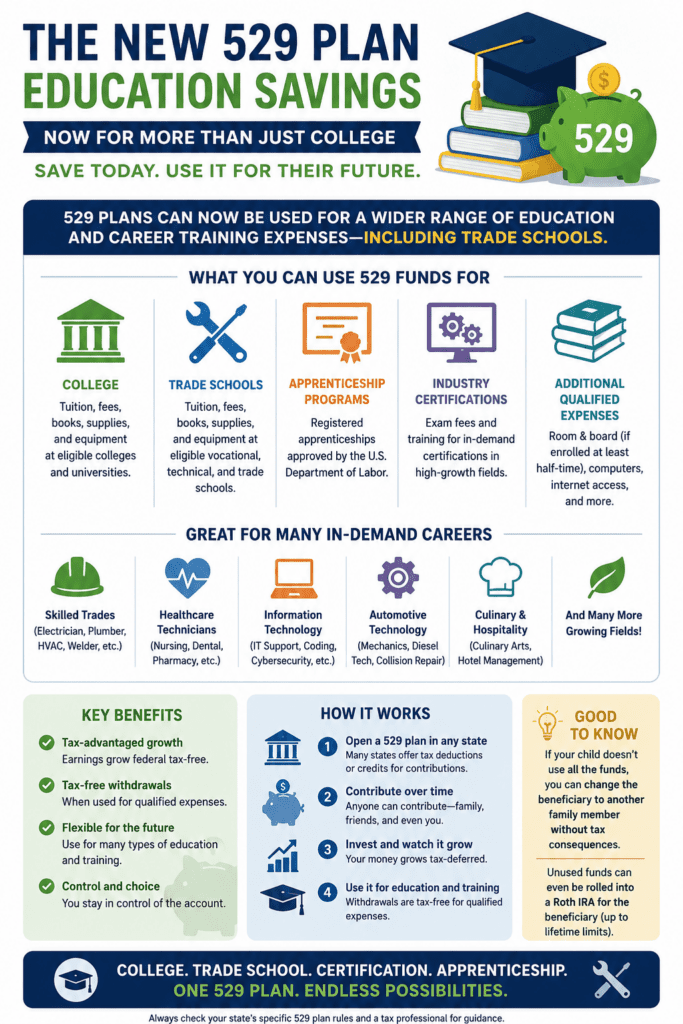

2026 Federal Income Taxes Strategy #18: Use a 529 Education Savings Plan

A 529 plan is one of the most powerful tax-advantaged savings vehicles available for education and career training expenses.

Why 529 Plans Matter

Contributions are made with after-tax dollars, but investments grow tax free and qualified withdrawals are generally tax free.

529 Plans Are No Longer Just for College

Many taxpayers are surprised to learn that 529 plans can now help fund:

- College tuition

- University expenses

- Trade schools

- Vocational training

- Registered apprenticeships

- Industry certification programs

- Certain K–12 education expenses

Potential Tax Benefits

A properly used 529 plan can provide:

- Tax-free investment growth

- Tax-free qualified withdrawals

- Potential state tax deductions or credits

- Flexible beneficiary changes

New Flexibility

If the original beneficiary does not use all of the funds, the account owner may be able to:

- Change beneficiaries

- Transfer funds to another family member

- Under certain circumstances, roll unused funds into a Roth IRA for the beneficiary (subject to federal rules and limits)

The Bottom Line

A 529 plan can be an excellent way to save for future education and career training expenses while benefiting from tax-free growth. Because eligible expenses now extend well beyond traditional college programs, 529 plans have become a valuable tax-planning tool for families preparing children and grandchildren for a wide range of career paths.

Quick Recap of the Top 18 Strategies for Reducing 2026 Federal Income Taxes

- Maximize Retirement Contributions

- Use the Standard Deduction and Senior Deductions

- Claim the Child Tax Credit

- Use Education Credits

- Leverage Long-Term Capital Gains Rates

- Maximize HSA and FSA Contributions

- Use Tax-Loss Harvesting

- Optimize Filing Status

- Plan for State Income Taxes

- Use Additional Retirement Plans

- Consider Roth IRA Conversions

- Use Charitable Contribution Strategies

- Plan Carefully for RMDs

- Hire Family Members in Your Business

- Work With a Qualified Tax Professional

- Understand the No Tax on Tip Rules

- New American Made Vehicle Interest Deduction

- Use a 529 Education Savings Plan – Trade schools and more

Each of these strategies can potentially reduce your tax liability, improve retirement security, and help preserve more of your hard-earned wealth.

The next major section should be the expanded “Strategic Roth IRA Conversions After Age 59½” section, updated for 2026 tax brackets and incorporating the new enhanced senior deductions and retirement income planning opportunities. That section can easily be 1,000–1,500 words and is one of the strongest SEO sections in the entire article.

Reducing your tax burden is only one piece of a successful financial strategy. Building wealth, protecting assets, planning your estate, and creating additional income streams often require a deeper level of education and planning than a single article can provide.

To help our readers take the next step, RetireCoast now offers three premium membership programs designed to provide advanced tools, calculators, guides, and planning resources.

Choose the Membership That Fits Your Goals:

-

💼 Business Builder Membership

Designed for entrepreneurs, retirees starting businesses, real estate investors, and small business owners seeking strategies to increase income, improve operations, and legally reduce taxes. -

🛡️ Estate Planning Membership

Focused on wealth preservation, trusts, asset protection, estate planning, inheritance strategies, and protecting assets for future generations. -

📈 Millennial Financial Lab

Built specifically for Millennials and younger professionals seeking practical guidance on investing, retirement planning, debt reduction, major purchases, and long-term wealth building.

Many members find that more than one program fits their needs. For those who want access to every tool, calculator, guide, and membership resource across the RetireCoast platform, we offer an All-Access Membership that provides a substantial discount compared to purchasing all three memberships separately.

Whether your goal is reducing taxes, protecting assets, starting a business, preparing for retirement, or creating a lasting legacy, RetireCoast memberships provide the tools and guidance to help you move forward with confidence.

STRATEGIC ROTH IRA CONVERSIONS AND 2026 FEDERAL INCOME TAXES

One of the most effective long-term tax planning strategies available to retirees is a carefully planned Roth IRA conversion program.

Many retirees spend years accumulating assets in Traditional IRAs, 401(k) plans, SEP IRAs, and other tax-deferred retirement accounts. While these accounts provide valuable tax deductions during working years, every dollar withdrawn in retirement is generally taxed as ordinary income.

A Roth IRA conversion allows retirees to gradually move money from taxable retirement accounts into an account that can potentially provide tax-free income for the remainder of their lives.

More People Also Ask About 2026 Federal Income Taxes

Is it better to receive a large tax refund or adjust my withholding?

Many taxpayers enjoy receiving a large refund, but a refund simply means you paid more tax during the year than was necessary. In many cases, adjusting your withholding to more closely match your actual tax liability can improve monthly cash flow and allow you to save, invest, or pay down debt throughout the year rather than waiting for a refund.

Are Roth IRA conversions worth considering in retirement?

For many retirees, Roth IRA conversions can be a powerful tax-planning tool. By converting portions of a Traditional IRA to a Roth IRA during years when taxable income is relatively low, retirees may reduce future Required Minimum Distributions (RMDs), create tax-free retirement income, and potentially lower their lifetime tax burden. The strategy is not appropriate for everyone, but it is often worth evaluating.

Can moving to another state reduce my overall tax burden?

Yes. State tax laws vary widely across the country. Some states impose no income tax, while others provide favorable treatment for retirement income, pensions, Social Security benefits, and IRA withdrawals. For retirees and high-income taxpayers, relocating from a high-tax state to a more tax-friendly state can sometimes save thousands of dollars per year in taxes.

How does the new No Tax on Tips law affect tax planning?

The new federal deduction for qualifying tip income may reduce federal taxable income for eligible workers. However, some employers may continue withholding taxes based on older payroll systems, and some states may still tax tip income. Workers who receive tips should carefully monitor pay stubs, track tip income, and estimate their actual tax liability throughout the year.

Can I claim the American-made vehicle interest deduction if I take the standard deduction?

In many cases, yes. One of the most attractive features of the new American-made vehicle interest deduction is that it may be available in addition to the standard deduction for qualifying taxpayers. Because eligibility rules and income limitations apply, taxpayers should review current IRS guidance before relying on the deduction.

What is one of the biggest tax mistakes retirees make?

One of the most common mistakes is waiting too long to plan for Required Minimum Distributions (RMDs). Large Traditional IRA balances can eventually create substantial taxable income, potentially increasing federal taxes, Medicare premiums, and the taxation of Social Security benefits. Early planning, including Roth conversions and strategic withdrawals, may help reduce these future tax burdens.

These six additional questions target high-value searches related to refunds, Roth conversions, relocation, tips, vehicle deductions, and retirement tax planning.

How Roth IRA Conversions Affect 2026 Federal Income Taxes

A Roth conversion occurs when funds are transferred from a Traditional IRA or qualified retirement account into a Roth IRA.

The amount converted becomes taxable income during the year of the conversion.

However, once the funds are inside the Roth IRA:

- Future growth is tax free.

- Qualified withdrawals are tax free.

- No lifetime Required Minimum Distributions apply to the original account owner.

- Beneficiaries often receive favorable tax treatment.

The goal is not necessarily to avoid taxes completely. The goal is to pay taxes when rates are lower and avoid paying them later when rates may be higher.

Why Retirees Should Consider Roth Conversions

Many retirees experience a temporary period of lower taxable income.

Common examples include:

- Recently retired individuals before Social Security begins.

- Retirees delaying pension income.

- Individuals between retirement and RMD age.

- Taxpayers experiencing a temporary reduction in income.

These years often provide an excellent opportunity to perform Roth conversions at relatively low tax rates.

The Retirement Tax Window

Many financial planners refer to this period as the retirement tax window.

The retirement tax window generally begins when employment income ends and closes when:

- Social Security benefits begin.

- Pension income begins.

- Required Minimum Distributions start.

- Other taxable income increases.

For some retirees, this window may last several years.

Those years can provide valuable opportunities to move retirement assets into a Roth IRA while remaining in lower federal tax brackets.

Using Current Tax Brackets to Manage 2026 Federal Income Taxes

A common strategy involves converting only enough money each year to remain within a desired tax bracket.

For example, a retiree may decide to remain within the 12% or 22% federal tax bracket.

Instead of converting an entire IRA at once, smaller annual conversions can be performed.

Benefits may include:

- Lower lifetime taxes

- Better control over Medicare premiums

- Reduced taxation of Social Security benefits

- Lower future RMDs

This approach often provides significantly better results than a single large conversion.

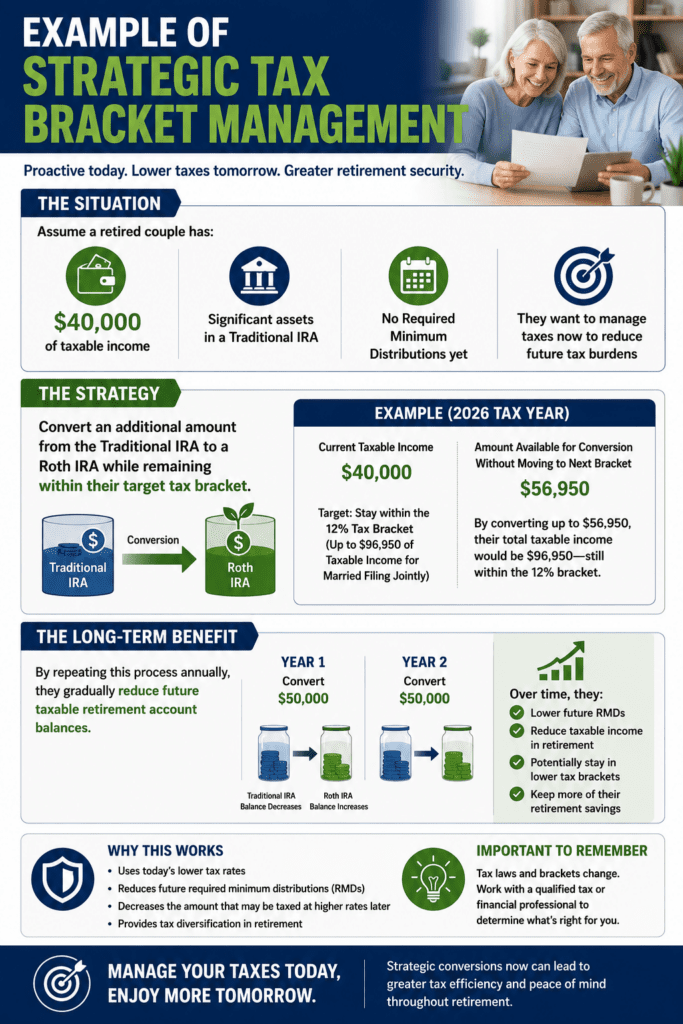

Example of Strategic Tax Bracket Management

Assume a retired couple has:

- $40,000 of taxable income

- Significant assets in a Traditional IRA

- No Required Minimum Distributions yet

They may decide to convert an additional amount into a Roth IRA while remaining within their target tax bracket.

By repeating this process annually, they gradually reduce future taxable retirement account balances.

How Roth Conversions May Reduce Future Required Minimum Distributions

One of the largest benefits of Roth conversions is reducing future Required Minimum Distributions.

Traditional retirement accounts eventually become subject to mandatory withdrawals.

Those withdrawals often create additional taxable income.

Large RMDs can:

- Increase federal income taxes

- Increase Medicare Part B premiums

- Increase Medicare Part D premiums

- Cause additional Social Security benefits to become taxable

Converting funds before RMDs begin may substantially reduce these future tax burdens.

Example

Suppose an individual reaches age 73 with:

- Traditional IRA Balance: $1,500,000

The resulting RMD could create significant taxable income every year.

If that same individual had gradually converted portions of the account over a ten-year period, future RMDs could be dramatically lower.

Roth IRAs and Medicare Premium Planning

Many retirees are surprised to discover that Medicare premiums are income based.

Higher income can trigger Income-Related Monthly Adjustment Amounts (IRMAA).

These surcharges can substantially increase:

- Medicare Part B premiums

- Medicare Part D premiums

Careful Roth conversion planning may help retirees manage future income levels and potentially reduce Medicare-related expenses.

Watch the Two-Year Lookback Rule

Medicare generally looks back two years when determining premium surcharges.

A large Roth conversion today could temporarily increase Medicare costs in a future year.

This does not necessarily mean conversions should be avoided.

It simply means the conversion amount should be carefully planned.

Estate Planning Benefits of Roth IRAs

Roth IRAs often provide significant estate planning advantages.

Beneficiaries generally receive:

- Tax-free distributions

- Simplified tax reporting

- Greater flexibility

Many retirees intentionally convert portions of their retirement accounts to create a more tax-efficient inheritance for children and grandchildren.

Leaving Tax-Free Assets to Heirs

Consider two inherited accounts:

- Traditional IRA

- Roth IRA

The beneficiary of the Traditional IRA may owe income taxes on withdrawals.

The beneficiary of the Roth IRA generally receives tax-free distributions if applicable rules are satisfied.

This difference can be substantial over time.

Common Roth Conversion Mistakes

While Roth conversions can be powerful, several common mistakes should be avoided.

Converting Too Much in One Year

Large conversions may:

- Push taxpayers into higher tax brackets

- Increase Medicare premiums

- Trigger additional taxes

Smaller annual conversions are often more efficient.

Ignoring State Income Taxes

State tax consequences vary.

Before converting, taxpayers should evaluate both federal and state tax impacts.

Using IRA Funds to Pay Conversion Taxes

Whenever possible, many financial planners recommend paying conversion taxes from non-retirement assets.

Using IRA funds to pay taxes reduces the amount that can continue growing tax free inside the Roth account.

When Roth Conversions May Not Be Appropriate

A Roth conversion is not automatically beneficial for everyone.

Situations where caution may be warranted include:

- Current tax rates are unusually high.

- Significant medical deductions are unavailable.

- Cash is not available to pay conversion taxes.

- The taxpayer expects substantially lower future tax rates.

Every situation should be analyzed individually.

Key Takeaways About Roth Conversions and 2026 Federal Income Taxes

A carefully designed Roth conversion strategy can:

- Reduce future Required Minimum Distributions.

- Create tax-free retirement income.

- Improve retirement cash-flow flexibility.

- Potentially reduce lifetime federal income taxes.

- Provide valuable estate planning benefits.

For many retirees, the years between retirement and the start of Required Minimum Distributions represent one of the best opportunities to improve long-term tax efficiency.

Before implementing a Roth conversion strategy, consider consulting with a qualified tax professional or financial advisor who can evaluate your specific circumstances and help determine the appropriate conversion amount for your situation.

The next major section should be “Required Minimum Distributions (RMDs) Explained for 2026 Federal Income Taxes”, followed by the updated 2026 IRS Tax Deadline Calendar, and then the conclusion. That will complete the article and give you several strong SEO sections targeting retirees.

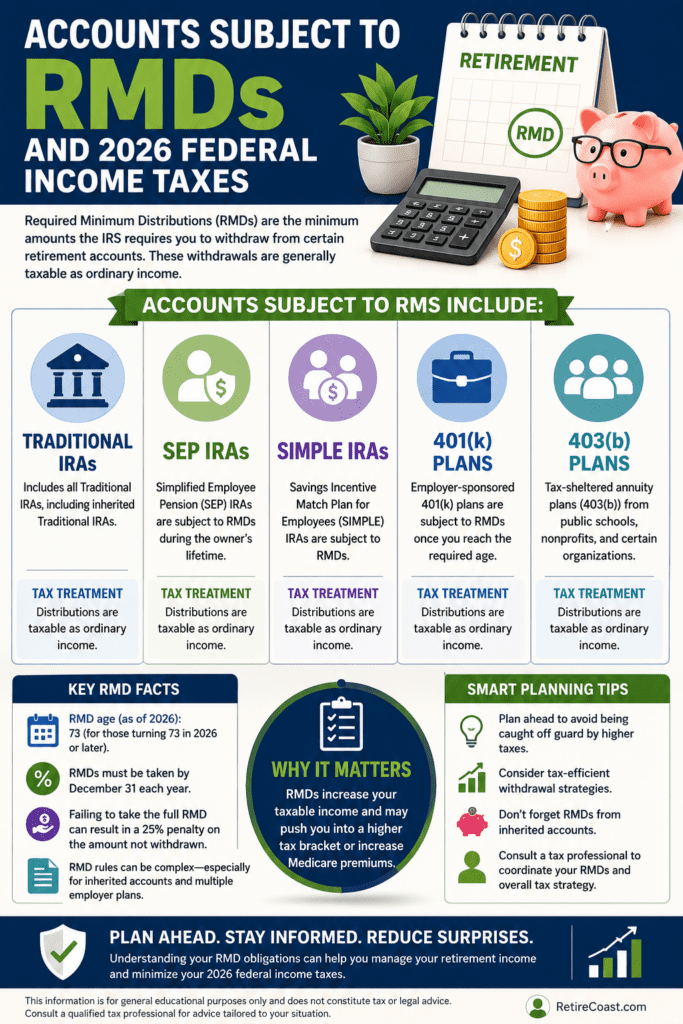

REQUIRED MINIMUM DISTRIBUTIONS (RMDS) AND 2026 FEDERAL INCOME TAXES

Required Minimum Distributions (RMDs) are one of the most important tax issues facing retirees. Understanding how they work can help you avoid costly penalties and reduce the impact they may have on your 2026 federal income taxes.

Many retirees spend decades building retirement savings in tax-deferred accounts. Eventually, the Internal Revenue Service requires those funds to be withdrawn and taxed.

What Is a Required Minimum Distribution?

A Required Minimum Distribution is the minimum amount that must be withdrawn each year from certain tax-advantaged retirement accounts once you reach the required age.

These withdrawals are generally taxable as ordinary income.

The purpose of the RMD rules is simple: retirement accounts receive valuable tax benefits during the accumulation years, but Congress intends those funds to eventually be taxed.

Which Retirement Accounts Are Subject to RMDs?

Required Minimum Distributions generally apply to:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- 401(k) Plans

- 403(b) Plans

- Most employer-sponsored retirement plans

Accounts Not Subject to Lifetime RMDs

Roth IRAs remain one of the few retirement accounts that are not subject to Required Minimum Distributions during the original owner’s lifetime.

This advantage is one reason many retirees consider strategic Roth IRA conversions.

When Do RMDs Begin?

The age at which Required Minimum Distributions begin depends upon your date of birth.

Current RMD Rules

| Birth Year | RMD Age |

|---|---|

| Born Before 1960 | Age 73 |

| Born 1960 or Later | Age 75 |

The first RMD must generally be taken no later than April 1 of the year following the year you reach your required starting age.

After the first distribution, future RMDs must normally be taken by December 31 each year.

How RMDs Affect 2026 Federal Income Taxes

Every dollar withdrawn through an RMD generally becomes taxable income.

This additional income can create several consequences.

Increased Federal Income Taxes

The most obvious effect is a higher federal tax bill.

Large retirement account balances can generate substantial Required Minimum Distributions.

Taxation of Social Security Benefits

Additional income from RMDs may cause more of your Social Security benefits to become taxable.

Depending upon your overall income, up to 85% of Social Security benefits may be included in taxable income.

Medicare Premium Surcharges

Higher income levels may trigger Income-Related Monthly Adjustment Amounts (IRMAA).

These surcharges can increase:

- Medicare Part B premiums

- Medicare Part D premiums

Many retirees are surprised to discover that retirement account withdrawals can indirectly increase healthcare costs.

How Are RMDs Calculated?

The Internal Revenue Service uses two primary factors:

- Your retirement account balance on December 31 of the previous year.

- Your IRS life expectancy factor.

Basic RMD Formula

RMD = Retirement Account Balance ÷ IRS Life Expectancy Factor

Example Calculation

Assume:

- Traditional IRA Balance: $500,000

- IRS Life Expectancy Factor: 26.5

Calculation:

$500,000 ÷ 26.5 = $18,868

In this example, the taxpayer would be required to withdraw approximately $18,868 during the year.

The actual factor varies based upon IRS life expectancy tables.

What Happens If You Miss an RMD?

Failing to take a Required Minimum Distribution can be expensive.

IRS Penalties

Current law generally imposes:

- A 25% penalty on the amount not withdrawn.

- Potential reduction to 10% if corrected promptly and properly reported.

Even with reduced penalties, failing to take an RMD can be costly.

For that reason, retirees should carefully monitor distribution deadlines.

Can You Withdraw More Than the Required Minimum?

Yes.

The RMD represents the minimum withdrawal requirement.

You may withdraw additional funds if needed.

However, withdrawals from Traditional IRAs and similar retirement accounts generally remain fully taxable as ordinary income.

Additional withdrawals may:

- Increase tax liability.

- Increase Medicare premiums.

- Increase taxation of Social Security benefits.

For this reason, many retirees carefully manage withdrawals throughout retirement.

Qualified Charitable Distributions and 2026 Federal Income Taxes

One of the most effective strategies available to retirees is the Qualified Charitable Distribution (QCD).

What Is a Qualified Charitable Distribution?

A QCD allows eligible taxpayers to transfer funds directly from an IRA to a qualified charitable organization.

Benefits include:

- Satisfying all or part of an RMD.

- Excluding the transfer from taxable income.

- Supporting charitable causes.

Why QCDs Are Valuable

Many retirees no longer itemize deductions because of the larger standard deduction.

A Qualified Charitable Distribution may provide tax benefits even when charitable contributions would otherwise produce no deduction.

For charitably inclined retirees, QCDs can be an extremely effective tax planning tool.

Strategies for Managing RMDs and 2026 Federal Income Taxes

Several planning techniques may reduce future RMD-related tax burdens.

Strategic Roth IRA Conversions

Converting portions of a Traditional IRA into a Roth IRA before RMD age may:

- Reduce future RMDs.

- Create tax-free retirement income.

- Improve estate planning flexibility.

Gradual Withdrawals Before RMD Age

Some retirees intentionally withdraw retirement funds before RMDs begin.

This may help smooth taxable income over multiple years rather than concentrating income later in retirement.

Charitable Planning

Qualified Charitable Distributions may help reduce taxable income while satisfying charitable objectives.

Tax Bracket Management

Monitoring annual income levels may help retirees avoid moving into higher federal tax brackets.

Key Takeaways About RMDs and 2026 Federal Income Taxes

Required Minimum Distributions are an unavoidable reality for many retirees.

However, with proper planning, retirees can often:

- Reduce future RMD balances.

- Manage tax brackets more effectively.

- Control Medicare premium surcharges.

- Improve cash flow flexibility.

- Preserve more retirement assets.

Understanding RMD rules before they begin can help retirees make smarter decisions and avoid unnecessary taxes.

IRS TAX DEADLINES CALENDAR FOR 2026

The Internal Revenue Service operates on strict deadlines. Missing a filing or payment deadline can result in penalties and interest charges.

The following calendar highlights some of the most important federal tax dates for individuals during 2026.

| Date | Deadline | Description |

|---|---|---|

| January 15, 2026 | Final Estimated Tax Payment for 2025 | Pay fourth-quarter estimated taxes for 2025 income. |

| April 15, 2026 | Individual Tax Return Due | File your 2025 Form 1040 or request an extension. |

| April 15, 2026 | IRA Contribution Deadline | Last day to make IRA contributions for tax year 2025. |

| April 15, 2026 | First Quarter Estimated Tax Payment | Pay estimated taxes for first-quarter 2026 income. |

| June 15, 2026 | Second Quarter Estimated Tax Payment | Pay estimated taxes for second-quarter 2026 income. |

| September 15, 2026 | Third Quarter Estimated Tax Payment | Pay estimated taxes for third-quarter 2026 income. |

| October 15, 2026 | Extended Return Deadline | Final filing deadline for taxpayers who requested an extension. |

| December 31, 2026 | RMD Deadline | Most retirees must complete Required Minimum Distributions by this date. |

| January 15, 2027 | Fourth Quarter Estimated Tax Payment | Pay estimated taxes for fourth-quarter 2026 income. |

Retirees, investors, and business owners should consider adding these dates to their calendars to avoid costly penalties and missed opportunities.

CONCLUSION: SMART PLANNING FOR 2026 FEDERAL INCOME TAXES

Federal income taxes are not something that should be considered only during filing season.

The most successful taxpayers plan throughout the year.

Whether you are maximizing retirement contributions, managing Required Minimum Distributions, utilizing Roth IRA conversions, harvesting investment losses, claiming valuable tax credits, or operating a business, proactive tax planning can help you preserve more of your hard-earned money.

The tax code continues to evolve, and Congress frequently considers changes that may affect deductions, credits, retirement accounts, and tax rates. Staying informed can help you take advantage of opportunities as they arise.

For retirees, investors, and small business owners, even modest planning decisions can result in significant long-term savings.

Most importantly, remember that every taxpayer’s situation is unique. Before implementing major tax strategies, consult with a qualified tax professional who can evaluate your specific circumstances and help develop a personalized plan.

The goal is simple: legally minimize your tax burden, maximize after-tax income, and keep more of your money working for your future.

Tax laws change frequently, and the Internal Revenue Service periodically issues new regulations, guidance, notices, and interpretations. The following government resources can help you verify current tax rules and obtain official information directly from the source.

-

Internal Revenue Service (IRS)

Official IRS website for tax forms, publications, tax law updates, and taxpayer assistance. -

IRS Forms and Instructions

Download current tax forms, instructions, schedules, and publications. -

IRS Newsroom

Latest IRS announcements, tax law updates, and guidance. -

IRS Retirement Plans Information

Official guidance regarding IRAs, Roth IRAs, 401(k) plans, SEP IRAs, SIMPLE IRAs, and retirement plan contribution limits. -

IRS Required Minimum Distribution (RMD) Information

Current RMD rules, deadlines, and calculation guidance. -

IRS Credits and Deductions

Official information regarding tax credits and deductions available to individuals and families. -

IRS Tax Withholding Estimator

Estimate federal withholding and determine whether adjustments to Form W-4 may be appropriate. -

Social Security Administration (SSA)

Official information regarding Social Security benefits and retirement planning. -

Medicare

Official Medicare website with information about premiums, enrollment, and healthcare coverage. -

U.S. Department of the Treasury

Federal financial policies, tax administration information, and Treasury announcements. -

Congress.gov

Track proposed and enacted federal tax legislation directly from Congress. -

USA.gov Tax Information

Federal government tax resources and taxpayer assistance links.

Reading about tax-saving strategies is a great first step. Building a personalized plan is where the real value begins. Whether your goals involve reducing taxes, preserving wealth, starting a business, planning your estate, or creating a long-term retirement strategy, RetireCoast memberships provide advanced decision-making tools designed to help you make informed financial choices.

Why guess at what you want to achieve when you can use proven planning tools to evaluate options, compare scenarios, and create a roadmap for the future?

Choose the Membership That Fits Your Goals

-

💼 Business Builder Membership