For many Americans, retirement is about more than leaving a career behind. It is an opportunity to pursue long-held dreams, create a new lifestyle, and invest in something tangible that can be enjoyed every day. Let’s discuss a small farm retirement investment.

One dream that consistently appears among retirees is owning a small farm. Whether it is a mini farm, hobby farm, homestead, or small income-producing property, many people wonder if buying acreage can provide both financial benefits and a better quality of life.

The question is not whether farming can be rewarding. The question is whether a small farm retirement investment makes financial sense compared to other ways retirees can invest their savings.

Unlike stocks, bonds, mutual funds, or rental properties, a small farm offers potential returns that go beyond annual income and appreciation. It may also provide food production, inflation protection, recreational opportunities, family gathering space, and a lasting legacy for future generations.

However, a farm can also require significant capital, ongoing maintenance, and long-term commitment. Many retirees discover that the economics of a small retirement farm are very different from the farmland investment returns often discussed by financial publications.

- Thinking About a Retirement Farm? Start Here.

- Part of the RetireCoast Farming After Retirement Series

- What This Article Will Cover

- Common Questions About Small Farm Retirement Investments

- What Makes Something a Good Retirement Investment?

- Small Farm vs. Farmland Investments: Understanding the Difference

- How Farmland Has Historically Performed as an Investment

- The Six Sources of Return From a Retirement Farm

- The One Big Beautiful Bill Act May Significantly Benefit Retirees Starting a Farm

- Not Every Return Is Measured in Dollars

- Common Investment Questions About Retirement Farms

- Retirement Farm vs. Stocks, Bonds, Rental Property, and Farmland REITs

- How Much of Your Retirement Savings Should Be Invested in a Farm?

- The Risks of Investing in a Retirement Farm

- Can You Buy a Retirement Farm Using Retirement Accounts?

- So, Is Buying a Small Farm a Good Investment for Retirement?

- 🌾 Retirement Farm Investment Quiz

- Final Questions Before Buying a Retirement Farm

Thinking About a Retirement Farm? Start Here.

This article is part of RetireCoast’s comprehensive series exploring the opportunities, challenges, financial considerations, and lifestyle realities of owning a farm later in life.

Is Buying a Small Farm a Good Retirement Investment? focuses on the financial side of the decision, including capital appreciation, farm income, cash flow, inflation protection, risk, and how a farm compares to traditional retirement investments.

For a complete understanding of the topic, we strongly recommend reading our companion pillar article:

📖 Farming After Retirement: Business or Lifestyle?

The pillar article examines farm types, retirement lifestyle considerations, business opportunities, startup planning, land selection, and the realities of transitioning from a traditional career into agriculture. Together, these articles provide one of the most comprehensive resources available for retirees considering a second act as a farmer, homesteader, or rural landowner.

Part of the RetireCoast Farming After Retirement Series

This article is part of RetireCoast’s comprehensive series on farming and retirement planning.

While this article focuses specifically on whether a farm is a good financial investment, readers should also review our companion guide:

Farming After Retirement: Business or Lifestyle?

That article examines the broader retirement-farming decision, including lifestyle considerations, farm business opportunities, startup planning, land selection, and the realities of operating a farm after leaving a traditional career.

Together, these two articles provide a more complete understanding of what it means to purchase, operate, and potentially profit from a retirement farm.

What This Article Will Cover

In this guide, we will evaluate a small farm as an investment asset.

We Will Examine

- How small farms create financial returns

- Historical farmland appreciation

- Income opportunities available to retirees

- Risks that can affect farm ownership

- How farms compare to stocks, bonds, and rental properties

- Whether a farm can help protect against inflation

- Situations where a farm may or may not be a wise retirement investment

What This Article Will Not Cover

This article is not a guide to starting a farm business.

We will not discuss farm startup plans, crop selection, livestock management, or beginning farmer programs in detail because those topics are already covered extensively in our companion article.

Instead, our focus is simple:

Is Buying a Small Farm a Good Retirement Investment?

The answer depends on how you define investment success, how much of your retirement savings you plan to commit, and what role you expect the property to play during your retirement years.

Common Questions About Small Farm Retirement Investments

Before buying acreage, retirees should look beyond the dream of country living and evaluate whether the farm works as an investment. These three questions help frame the financial side of the decision.

Is buying a small farm a good investment for retirement?

A small farm can be a good retirement investment if it supports your financial goals, risk tolerance, and long-term plans.

Unlike stocks or mutual funds, a farm may provide land appreciation, rental income, farm income, reduced living costs, and personal enjoyment.

The risk is that property taxes, maintenance, insurance, equipment, and market conditions can reduce or eliminate cash flow.

How much income can a small farm generate?

Small farm income varies widely depending on acreage, location, soil quality, water access, and the owner’s business model.

Some farms generate income through leasing land, livestock, specialty crops, farm stays, timber, agritourism, or value-added products.

Many hobby farms produce little or no net income, especially during the early years of ownership.

Is farmland a better investment than the stock market?

Farmland and the stock market serve different purposes inside a retirement portfolio.

Agricultural land may offer stable returns, capital appreciation, inflation protection, and diversification.

Stocks and mutual funds usually provide greater liquidity and may offer higher returns over certain investment horizons.

What Makes Something a Good Retirement Investment?

Before evaluating a small farm, it helps to define what makes any investment successful during retirement.

Many retirees focus solely on annual returns. While returns matter, a retirement investment should be evaluated using several different criteria.

A farm that produces modest income but significantly improves quality of life may be a better investment for one retiree than a higher-return asset that provides no personal enjoyment. The key is understanding what you expect the investment to accomplish.

Income Generation

Many retirees depend on investment income to supplement Social Security, pensions, retirement accounts, and personal savings.

Traditional investments often generate income through:

- Dividends

- Interest payments

- Rental income

- Capital distributions

A small farm may generate income through agricultural production, leasing land to local farmers, agritourism, timber sales, livestock, or other farm-related activities. However, unlike many traditional investments, farm income can fluctuate significantly from year to year.

Capital Appreciation

Capital appreciation refers to an asset increasing in value over time.

Many farmland investments have historically benefited from rising farmland values, particularly in desirable agricultural regions and areas experiencing population growth.

For retirees purchasing agricultural land, appreciation may ultimately become a larger source of return than annual cash flow. The value of land can increase even during years when farm income is limited.

Inflation Protection

Inflation remains one of the greatest threats to long-term financial security.

Unlike paper assets, farmland ownership provides exposure to tangible assets that may increase in value as prices rise throughout the economy. Agricultural land, commodity prices, and food production often benefit from long-term global demand driven by population growth.

Many long-term investors view farmland as one of several alternative assets that can help preserve purchasing power during periods of elevated inflation.

Liquidity

Liquidity refers to how quickly an investment can be converted into cash.

Stocks, mutual funds, and many retirement funds can often be sold within days. A farm may take months to sell depending on market conditions, geographical location, and buyer demand.

Retirees should carefully consider liquidity needs before committing a large portion of their retirement portfolio to farmland ownership.

Risk and Volatility

Every investment carries risk.

Stock market investments are subject to market volatility. Bonds can be affected by interest rates. Real estate investments may experience local market declines.

A small farm faces its own unique risks, including weather events, changing commodity prices, property taxes, maintenance expenses, and fluctuations in local land prices.

Lifestyle Value

This final category is where retirement farms differ from many other investments.

A farm can provide personal satisfaction, recreational opportunities, privacy, food production, family gathering space, and a connection to the land. While these benefits may not appear on a financial statement, they often influence investment decisions just as much as income or appreciation.

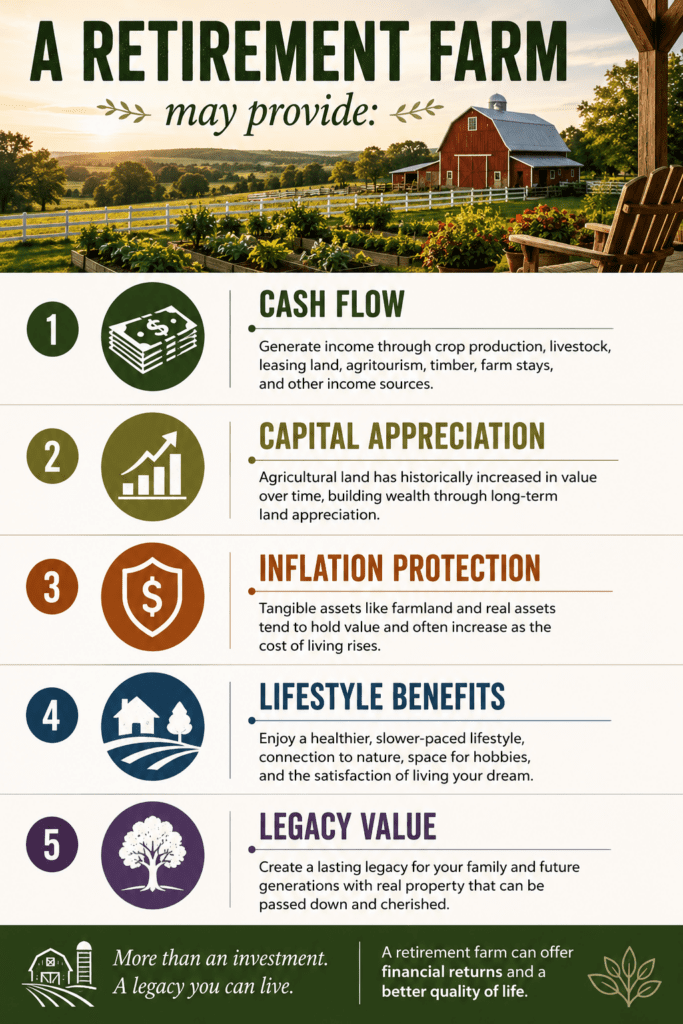

Evaluating the Complete Return

When retirees compare a small farm to traditional asset classes, they should consider more than simple investment returns.

A retirement farm may provide:

- Cash flow

- Capital appreciation

- Inflation protection

- Lifestyle benefits

- Legacy value

The challenge is determining whether those combined benefits justify the investment compared to alternatives such as stocks, bonds, rental property, farmland REITs, or other income-producing assets.

In the next section, we’ll examine how farmland investments have historically performed and why a small retirement farm is very different from the large-scale agricultural investments often discussed by institutional investors.

Small Farm vs. Farmland Investments: Understanding the Difference

One of the biggest mistakes retirees make when researching farmland investments is assuming that all agricultural land produces similar returns.

When financial publications discuss the performance of farmland investments, they are often referring to large-scale agricultural operations owned by institutional investors, pension funds, agricultural investors, or farmland REITs. These investments may consist of hundreds or even thousands of acres devoted to crop production and managed by experienced farm operators.

Most retirees are not purchasing that type of property.

Instead, they are typically considering:

- Small farms

- Hobby farms

- Mini farms

- Homesteads

- Mixed-use rural properties

- Small agricultural land holdings

The economics can be very different.

What Institutional Investors Are Buying

Large farmland investments are usually selected based on financial performance.

Institutional investors often evaluate:

- Historical farmland values

- Agricultural production potential

- Commodity prices

- Cash flow from leases

- Long-term capital appreciation

- Global demand for food and agricultural products

The focus is almost entirely on financial returns.

These investors are not concerned with enjoying the property, raising a garden, or creating a family gathering place.

What Most Retirees Are Buying

A retirement farm is often both an investment and a lifestyle asset.

In addition to financial considerations, retirees frequently evaluate:

- Proximity to family

- Quality of life

- Privacy

- Recreational opportunities

- Space for livestock or gardening

- Long-term retirement plans

This creates a unique investment profile that cannot be measured solely by annual returns.

The Value of Farmland vs. The Value of a Retirement Farm

The value of farmland is often driven by agricultural productivity.

The value of a retirement farm may also be influenced by:

- Residential improvements

- Scenic views

- Recreational opportunities

- Access to healthcare

- Nearby towns and services

- Future development potential

A 20-acre retirement farm near a growing community may appreciate very differently from 20 acres of isolated agricultural land.

Why This Distinction Matters

Many articles compare farmland investments to the stock market and conclude that agricultural land has historically produced stable returns.

While that may be true, retirees should understand that owning farmland directly is different from investing in farmland through mutual funds, farmland REITs, pension investments, or other alternative assets.

The returns from a retirement farm are likely to come from multiple sources, including:

- Capital appreciation

- Farm income

- Rental income

- Inflation protection

- Lifestyle benefits

- Legacy value

Evaluating only one of those factors may lead to a poor investment decision.

The Retirement Farm Investment Mindset

The question should not simply be:

“Will this farm outperform the stock market?”

A better question is:

“Will this farm strengthen my retirement portfolio while helping me achieve the lifestyle I want during retirement?”

That distinction is what separates a retirement farm from most traditional investments.

In the next section, we’ll examine the five primary ways a retirement farm can generate value and potentially improve both financial security and quality of life.

| Investment | Income Potential | Appreciation | Effort Required |

|---|---|---|---|

| Dividend Stocks | Moderate | Moderate | Low |

| Rental Property | Moderate | Moderate | Medium |

| Small Farm | Low to High | Moderate | High |

| Bonds | Low | Low | Very Low |

| CDs | Low | None | Very Low |

How Farmland Has Historically Performed as an Investment

Farmland has attracted investors for generations because it represents one of the world’s most essential tangible assets. While stocks, bonds, and other traditional asset classes rise and fall with market sentiment, agricultural land is tied to something more fundamental—the production of food.

People may postpone buying a new car or vacation, but global demand for food continues regardless of economic conditions. That reality has helped support the long-term value of farmland throughout much of the United States history.

Why Investors Are Interested in Farmland

Many long-term investors view farmland investments as an attractive alternative to traditional investments.

Farmland has several characteristics that appeal to both institutional investors and individual investors:

- Limited supply of quality agricultural land

- Growing world population

- Ongoing demand for agricultural production

- Potential for capital appreciation

- Opportunities for cash flow through leasing

- Inflation protection

- Portfolio diversification

These factors have caused farmland ownership to attract attention from pension investment managers, farmland REITs, agricultural investors, and retirement-focused investors seeking alternative assets.

The Value of Farmland Has Generally Increased Over Time

While farmland values can fluctuate based on commodity prices, interest rates, government policies, and local economic conditions, the long-term trend has generally been upward.

The value of farmland is often influenced by:

Agricultural Productivity

Land capable of producing crops efficiently typically commands higher prices.

Geographical Location

Properties near growing communities may benefit from both agricultural and development demand.

Water Availability

Reliable water sources can significantly affect the value of agricultural land.

Economic Conditions

Interest rates, inflation, and farm profitability can all influence land prices.

For many owners, capital appreciation becomes one of the most important contributors to overall returns.

Farmland vs. the Stock Market

Comparisons between farmland and the stock market often appear in investment discussions.

Supporters of farmland investing point to:

- Lower volatility

- Stable returns

- Inflation resistance

- Tangible ownership

Supporters of equities emphasize:

- Greater liquidity

- Historically higher long-term returns

- Easier diversification

- Lower maintenance requirements

The reality is that both asset classes serve different purposes within a retirement portfolio.

A diversified investment portfolio may include stocks, mutual funds, real estate, and agricultural investments rather than relying exclusively on one asset class.

Why Retirees Should Be Careful With Historical Data

Many studies that discuss farmland investments focus on large-scale agricultural operations.

These properties are often leased to professional farm operators and managed primarily for financial performance.

Most retirees considering small farms, hobby farms, or mixed-use rural properties are purchasing something very different.

A retirement farm may generate returns through:

- Land appreciation

- Rental income

- Farm income

- Reduced living expenses

- Lifestyle benefits

- Legacy value

As a result, historical farmland performance should be viewed as useful context rather than a guarantee of future returns.

| $500,000 Investment | Typical Income | Effort |

|---|---|---|

| Dividend ETF | Passive | Low |

| Bonds | Passive | Low |

| Rental Property | Moderate | Medium |

| Small Farm | Variable | High |

Past Performance Does Not Guarantee Future Results

Every investment decision involves risk.

Changes in interest rates, government policies, commodity prices, local land prices, and economic conditions can affect future farmland values.

Successful retirement planning requires evaluating both the opportunities and risks associated with any major investment.

The good news is that a retirement farm may offer multiple sources of return that extend beyond simple financial performance. Understanding those potential sources of value is the next step in determining whether a farm belongs in your retirement portfolio.

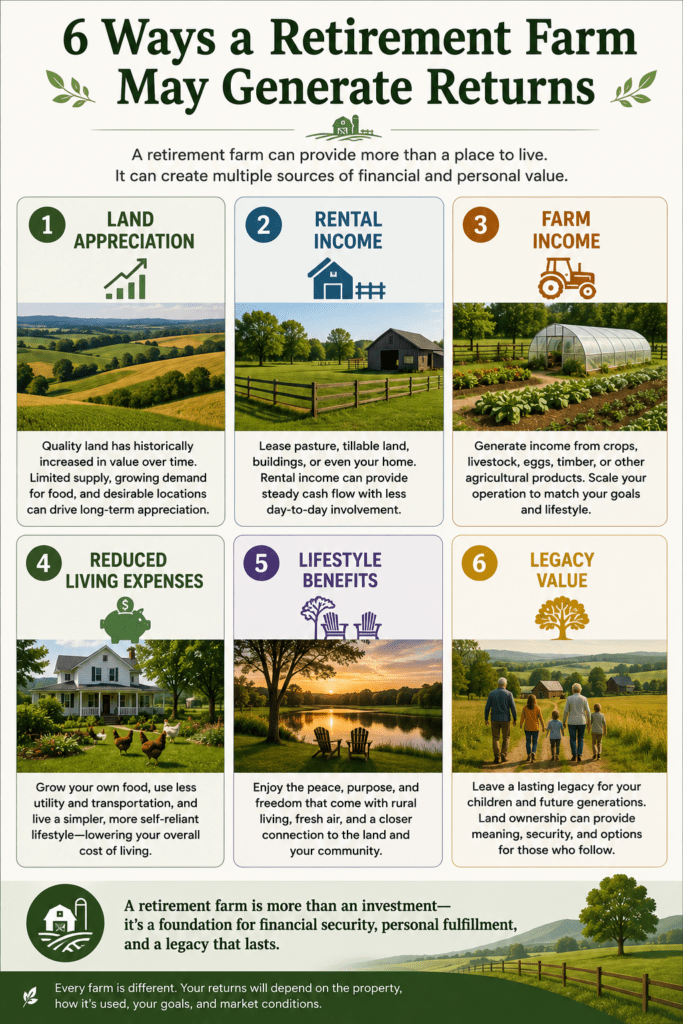

The Six Sources of Return From a Retirement Farm

Many people evaluate a retirement farm the same way they would evaluate a stock, bond, or rental property.

That approach can lead to poor decisions because a retirement farm often creates value in multiple ways at the same time.

A farm may produce income, appreciate in value, reduce living expenses, improve quality of life, and create a lasting family asset. Understanding all six sources of return can help retirees make better investment decisions.

1. Land Appreciation

Historically, quality agricultural land has generally increased in value over long periods.

Several factors can influence appreciation, including:

- Population growth

- Development pressure

- Limited supply of agricultural land

- Improvements to the property

- Local economic conditions

For many owners, capital appreciation becomes one of the largest contributors to long-term wealth creation.

A retirement farm located near a growing community may experience significantly different appreciation than a remote rural property.

2. Rental Income

Not every acre of a retirement farm must be personally operated.

Some owners generate rental income by leasing:

- Pasture land

- Crop acreage

- Hunting rights

- Storage buildings

- Equipment space

- Residential structures

Rental income can provide relatively steady cash flow while reducing the owner’s day-to-day involvement in agricultural activities.

3. Farm Income

Some retirees choose to actively produce income from the property.

Potential farm income sources include:

- Livestock

- Specialty crops

- Beekeeping

- Timber production

- Agritourism

- Farm stays

- Produce sales

The amount of income varies significantly based on acreage, market conditions, and the owner’s level of involvement.

Unlike many passive investments, farm income often requires management, planning, and ongoing effort.

4. Reduced Living Expenses

This source of return is often overlooked.

A retirement farm may help reduce household expenses through:

- Homegrown food

- Livestock products

- Firewood

- Reduced recreation costs

- Lower transportation expenses in some situations

While these savings may not appear as income, they can improve overall retirement cash flow and financial security.

5. Lifestyle Benefits

Many retirees purchase a farm for reasons that have little to do with financial returns.

Common lifestyle benefits include:

- Privacy

- Open space

- Outdoor recreation

- Gardening

- Connection to nature

- Personal fulfillment

These benefits are difficult to quantify but often play a major role in the investment decision.

6. Legacy Value

Unlike many financial assets, farmland can become a multigenerational asset.

Many owners hope to pass property to children, grandchildren, or other family members.

A farm may provide:

- Family gathering space

- Estate planning opportunities

- Long-term wealth preservation

- A tangible legacy

For some retirees, legacy value is every bit as important as annual returns.

The One Big Beautiful Bill Act May Significantly Benefit Retirees Starting a Farm

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, contains some of the most significant agricultural and tax policy changes in years. While the legislation does not specifically target retirees, several provisions heavily favor new and beginning farmers, making it particularly attractive for individuals considering farming as a second career or retirement venture.

If you are purchasing your first farm after retirement, these provisions may help reduce startup costs, lower financial risk, improve cash flow, and increase the overall return on your investment.

The legislation extends the definition of a Beginning Farmer or Rancher (BFR) to individuals with no more than 10 crop years of farming experience.

- Additional 5% premium subsidy during the first two crop years

- Additional 3% premium subsidy in year three

- Additional 1% premium subsidy in year four

- Improved affordability of crop insurance during startup years

The law restores 100% bonus depreciation for qualifying assets placed into service through 2030. This means qualifying farm equipment, machinery, buildings, and certain improvements may be deducted immediately rather than depreciated over many years. For example, a retiree purchasing a tractor, implements, greenhouse systems, or other qualifying assets may be able to deduct the entire cost in the year of purchase.

The Section 179 deduction limit has increased to $2.5 million. This provision gives farm owners significant flexibility to expense equipment and infrastructure purchases against farm income rather than recovering those costs over a long period of time.

A new provision under Internal Revenue Code Section 139L allows certain lenders to exclude 25% of interest income from qualifying agricultural and rural real estate loans. Because lenders receive favorable tax treatment, the program encourages financing for agricultural land purchases and rural property development. For retirees seeking to acquire farmland, this may improve loan availability and potentially support more competitive financing terms.

Most farms operate as:

- Sole proprietorships

- LLCs

- S-corporations

The legislation also provides temporary tax relief for older Americans. For tax years 2025 through 2028:

- Single taxpayers age 65 and older may qualify for an additional $6,000 deduction.

- Married couples age 65 and older may qualify for an additional $12,000 deduction if both spouses qualify.

If you decide to purchase a farm, visit your local USDA Farm Service Agency (FSA) office as one of your first steps. Ask specifically about registration as a Beginning Farmer or Rancher (BFR). Many retirees qualify because the designation is based on farming experience, not age. Registration may open the door to crop insurance incentives, financing programs, technical assistance, and other benefits designed to improve your chances of success.

Tax laws and USDA program rules change frequently. Always consult qualified tax, legal, agricultural, and financial professionals before making major investment decisions.

Not Every Return Is Measured in Dollars

One retiree may purchase a farm primarily for income.

Another may focus on appreciation and wealth preservation.

A third may value the lifestyle and family benefits more than any financial return.

The most successful retirement farm investments typically balance several of these return categories rather than relying on a single source of value.

The next question becomes even more important:

How does a retirement farm compare to other investment choices such as stocks, bonds, rental property, and farmland REITs?

Common Investment Questions About Retirement Farms

Once retirees understand the potential sources of return from a farm, the next step is evaluating how much to invest, whether the property can support itself financially, and what risks should be considered before making a purchase.

How much of my retirement savings should be invested in a farm?

There is no universal percentage that works for every retiree. The answer depends on your retirement income needs, risk tolerance, other investments, and overall financial security.

Many financial professionals encourage diversification rather than concentrating all retirement funds in a single asset.

Retirees should carefully consider liquidity needs, healthcare expenses, and long-term financial obligations before committing a substantial portion of their retirement portfolio to farmland ownership.

Can a small farm pay for itself?

Some small farms generate enough cash flow to cover property taxes, insurance, maintenance, and operating expenses.

Others produce supplemental income while still requiring contributions from retirement income or savings.

The ability of a farm to pay for itself depends on acreage, location, income opportunities, management decisions, and market conditions.

What is the biggest financial risk of owning a retirement farm?

For many retirees, the greatest financial risk is overestimating income while underestimating expenses.

Property taxes, equipment purchases, repairs, fencing, insurance, utilities, and maintenance costs can quickly exceed expectations.

Another significant risk is reduced liquidity. Unlike stocks or mutual funds, a farm may require months to sell if cash is needed unexpectedly.

Thinking About Financing a Retirement Farm?

Many retirees assume they must pay cash for a farm. In reality, financing options may include USDA programs, Farm Credit lenders, conventional banks, seller financing, home equity strategies, and specialized Beginning Farmer loan programs.

The type of financing available often depends on the property’s size, intended use, income potential, and whether the buyer plans to operate a farm business.

RetireCoast is preparing a detailed guide that will explore farm financing options specifically for retirees and late-career buyers.

Retirement Farm vs. Stocks, Bonds, Rental Property, and Farmland REITs

Every dollar invested in a retirement farm is a dollar that cannot be invested somewhere else.

That does not mean a farm is a bad investment. It simply means retirees should compare it against other available opportunities before making a major commitment.

The goal is not to identify a single “best” investment. The goal is to determine which investment best supports your retirement planning objectives.

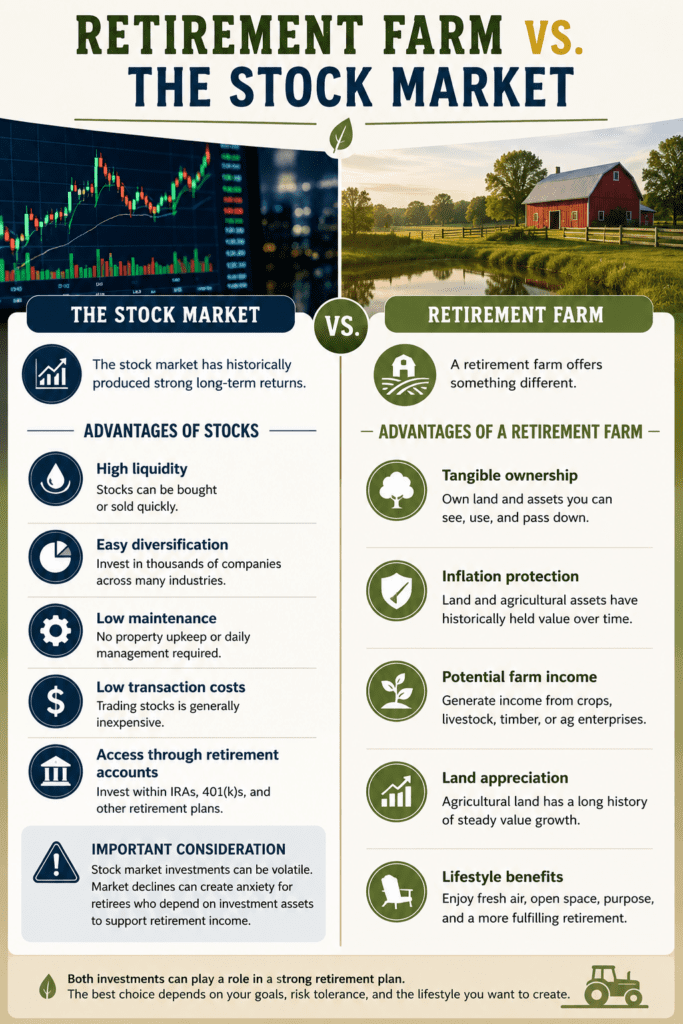

Retirement Farm vs. The Stock Market

The stock market has historically produced strong long-term returns.

Stocks offer several advantages:

- High liquidity

- Easy diversification

- Low maintenance

- Low transaction costs

- Access through retirement accounts

However, stock market investments can be volatile. Market declines can create anxiety for retirees who depend on investment assets to support retirement income.

A retirement farm offers something different.

Advantages may include:

- Tangible ownership

- Inflation protection

- Potential farm income

- Land appreciation

- Lifestyle benefits

The tradeoff is lower liquidity and higher management requirements.

Retirement Farm vs. Bonds

Many retirees rely on bonds for stability and income.

Bonds may provide:

- Predictable payments

- Lower volatility

- Simplicity

- Portfolio diversification

The challenge is that bond returns are heavily influenced by interest rates and inflation.

Agricultural land has historically appealed to investors seeking a hedge against inflation because the value of land and agricultural products often rises over time.

For retirees concerned about preserving purchasing power, farmland ownership may offer advantages that fixed-income investments cannot.

Retirement Farm vs. Rental Property

Rental property is often the closest comparison to a retirement farm.

Both involve:

- Real estate ownership

- Property taxes

- Insurance

- Maintenance

- Potential cash flow

Rental properties generally produce more predictable income.

Retirement farms often provide additional benefits that rental properties cannot offer, including:

- Food production

- Agricultural income opportunities

- Recreational value

- Personal use

- Legacy value

The best choice depends on whether the retiree prioritizes income, lifestyle, or a combination of both.

Retirement Farm vs. Farmland REITs

Farmland REITs allow investors to gain exposure to agricultural land without owning or managing property directly.

Advantages include:

- Liquidity

- Professional management

- Diversification

- Lower capital requirements

Disadvantages include:

- No personal use of the property

- No direct control

- Management fees

- Market-driven share prices

For retirees seeking pure investment exposure, farmland REITs may be worth considering.

For retirees who want to own land, enjoy rural living, and potentially create multiple sources of return, direct farmland ownership may be more attractive.

The Lifestyle Premium

This is where retirement farms become difficult to compare with traditional investments.

A stock certificate does not provide:

- A place for grandchildren to visit

- Fresh eggs from your chicken coop

- A vegetable garden

- A fishing pond

- A workshop

- Open space and privacy

Those benefits have real value even though they do not appear on an annual investment statement.

Many retirees willingly accept slightly lower financial returns in exchange for a significantly improved quality of life.

Which Investment Is Best?

There is no universal answer.

The best investment depends on:

- Retirement income needs

- Available capital

- Health considerations

- Investment horizons

- Family goals

- Risk tolerance

- Desired lifestyle

For some retirees, stocks and mutual funds remain the best choice.

For others, rental property offers the ideal balance of income and appreciation.

For those seeking financial security, tangible assets, inflation protection, and a more meaningful retirement lifestyle, a carefully selected small farm may prove to be one of the most rewarding investments they ever make.

Before making that decision, however, retirees should understand the risks that can affect both farm profitability and long-term investment returns.

How Much of Your Retirement Savings Should Be Invested in a Farm?

One of the most common questions retirees ask is not whether they should buy a farm, but how much of their retirement savings should be committed to one.

Unfortunately, there is no universal answer.

The right allocation depends on your retirement income sources, health, risk tolerance, investment portfolio, and long-term goals.

A farm can be a valuable asset, but it should strengthen your financial security rather than place it at risk.

Avoid the “All-In” Mistake

Many people fall in love with the idea of owning a farm.

Some consider selling most of their investments, purchasing acreage outright, and relying on the property to support their retirement.

While this approach occasionally works, it significantly increases concentration risk.

Unexpected events such as medical expenses, declining land values, poor farm income, or changing family circumstances can place tremendous pressure on a retiree who has committed most of their wealth to a single property.

Diversification remains one of the most effective risk-management strategies available to investors.

The 10% Approach

Some retirees allocate a relatively small portion of their retirement portfolio to agricultural land.

In this scenario, the farm serves primarily as:

- A diversification tool

- An inflation hedge

- A recreational property

- A future retirement option

The majority of retirement assets remain invested in traditional asset classes such as stocks, bonds, mutual funds, and retirement accounts.

This approach typically provides the greatest financial flexibility.

The 25% Approach

A quarter of a retirement portfolio is often enough to purchase a modest rural property in many parts of the United States.

This approach allows retirees to gain meaningful exposure to farmland ownership while maintaining substantial liquidity and diversification.

Many investors view this range as a balanced compromise between financial opportunity and risk management.

The 50% Approach

For retirees planning to live on the property, a farm may become both a residence and a major investment.

At this level, the property often serves multiple purposes:

- Primary residence

- Lifestyle asset

- Agricultural investment

- Legacy asset

While many successful retirement farm owners fall into this category, the decision requires careful planning because a large percentage of net worth becomes tied to a single property.

The 100% Approach

Some retirees consider investing nearly all available capital into farmland ownership.

In most situations, this creates substantial risk.

A farm is not a highly liquid asset.

Selling quickly may be difficult during unfavorable market conditions.

In addition, retirees still need access to capital for:

- Healthcare

- Long-term care

- Emergencies

- Family obligations

- Major repairs

Owning a valuable farm while lacking accessible cash can create financial stress.

Retirement Income Matters

The percentage invested in a farm becomes less important when retirees have reliable income from other sources.

Examples include:

- Social Security

- Pensions

- Rental income

- Dividend income

- Retirement account withdrawals

The more stable income sources available, the easier it may be to own agricultural land without relying heavily on farm income.

Ask a Better Question

Instead of asking:

“How much farm can I afford?”

Ask:

“How much farm can I comfortably own while preserving my financial security?”

That subtle difference often leads to better decisions.

The goal is not simply to acquire land.

The goal is to build a retirement that balances financial stability, lifestyle satisfaction, and long-term peace of mind.

There Is No Perfect Percentage

Some retirees will be happiest with a five-acre hobby farm.

Others may thrive on fifty acres of productive agricultural land.

The best allocation is the one that supports your retirement goals without creating unnecessary financial risk.

A retirement farm should improve your life, not become a source of financial anxiety.

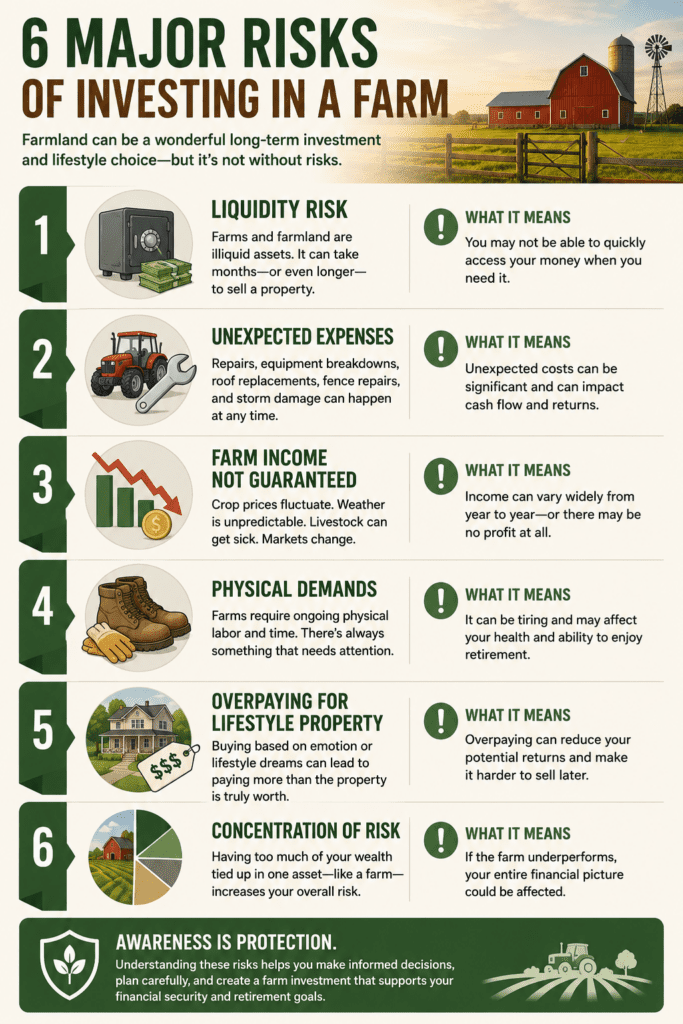

The Risks of Investing in a Retirement Farm

Every investment carries risk.

A retirement farm may provide income, appreciation, inflation protection, and lifestyle benefits, but it is not a guaranteed path to financial success.

Understanding the risks before buying can help retirees avoid expensive mistakes.

1. Liquidity Risk

A retirement farm is not a stock or mutual fund.

If you need cash quickly, selling a farm may take months or even years, depending on market conditions and the geographical location of the property.

Retirees should avoid investing funds they may need for:

- Medical expenses

- Long-term care

- Emergencies

- Major home repairs

- Family obligations

Liquidity is often the biggest difference between farmland ownership and traditional retirement investments.

2. Unexpected Expenses

Many first-time farm owners underestimate costs.

Common expenses include:

- Property taxes

- Insurance

- Equipment

- Fencing

- Utilities

- Road maintenance

- Building repairs

- Animal care

A farm can require significant capital even when no major agricultural activities are taking place.

Retirees should maintain adequate reserves for unexpected repairs and maintenance.

3. Farm Income Is Not Guaranteed

Many retirement buyers assume farm income will offset ownership costs.

Sometimes it does.

Sometimes it does not.

Factors that can affect farm income include:

- Weather

- Commodity prices

- Local demand

- Input costs

- Disease

- Government policies

A retirement farm should be able to stand on its own financially even if projected income is lower than expected.

4. Physical Demands

One of the most overlooked risks has nothing to do with money.

It is physical capability.

Many retirees enjoy gardening, livestock, and outdoor projects. However, agricultural activities often involve lifting, walking, bending, climbing, and working in extreme weather.

A property that feels manageable at age 60 may feel very different at age 75.

Smart retirees plan for the future rather than only their current abilities.

5. Overpaying for Lifestyle Property

A beautiful farm can create emotional decision-making.

Buyers sometimes pay premium prices for:

- Scenic views

- Historic barns

- Waterfront features

- Recreational amenities

There is nothing wrong with paying for lifestyle benefits.

The mistake occurs when buyers convince themselves that every dollar spent is an investment rather than recognizing that part of the purchase may be a personal benefit.

6. Concentration Risk

A farm is often one of the largest purchases a retiree will ever make.

Putting too much of a retirement portfolio into a single asset increases risk.

Even valuable assets can experience periods of stagnant growth or declining values.

Diversification remains an important principle of retirement planning regardless of the investment being considered.

Risk Can Be Managed

The good news is that most farm ownership risks can be reduced through planning.

Successful retirement farm owners typically:

- Purchase appropriate acreage

- Maintain emergency reserves

- Avoid excessive debt

- Start small

- Develop realistic income expectations

- Learn before they invest heavily

The goal is not to eliminate risk.

The goal is to understand it and make informed investment decisions.

The Bottom Line on Risk

A retirement farm is neither a guaranteed success nor a guaranteed mistake.

Like any major investment, outcomes depend on the property selected, the purchase price, financial preparation, and the owner’s expectations.

For retirees who approach the decision realistically, a small farm can become both a valuable asset and a highly rewarding part of retirement.

Should You Buy a Small Farm?

Every retirement situation is different.

A farm that is a perfect fit for one retiree may be completely wrong for another. Factors such as income, health, available capital, farming experience, risk tolerance, and long-term goals all influence the decision.

To help readers evaluate their own situation, RetireCoast created the free Retirement Farm Suitability Assessment Tool.

The assessment takes only a few minutes to complete and provides a personalized score based on factors commonly associated with successful retirement farm ownership.

Take the Free Assessment

Retirement Farm Suitability Assessment

Use this free tool to estimate whether buying a mini farm after retirement fits your health, budget, lifestyle, and long-term goals.

Case Study: Harry and Jennifer’s Retirement Farm Success Story

Harry and Jennifer spent years discussing what they wanted retirement to look like.

Both had enjoyed successful careers, but they knew they wanted something more meaningful than simply stopping work and watching television. They envisioned a small farm where the family could gather, grandchildren could visit, and they could spend their retirement years creating something lasting.

Several years before retirement, they began researching what farm ownership would actually require.

They read books, attended agricultural workshops, visited local farms, and enrolled in community college courses covering basic agriculture, gardening, and animal husbandry. Rather than assuming enthusiasm alone would make them successful, they committed themselves to learning.

As part of their planning process, they carefully evaluated the six major risks associated with retirement farm ownership.

They considered liquidity risk and made sure they maintained substantial retirement savings outside the farm purchase. They planned for unexpected expenses by creating a dedicated reserve fund. They understood farm income was not guaranteed and developed conservative financial projections. They selected a manageable property that would remain practical as they aged.

They avoided overpaying for a “dream property” and instead focused on buying a productive farm at a reasonable price. Finally, they made certain that the purchase would not consume all of their retirement assets.

Financially, they were well positioned.

Over their careers they had accumulated significant savings in their 401(k) plans, maintained healthy HSA balances, and owned a California home that had appreciated substantially over the years.

They developed a written retirement farm business plan and used it to evaluate potential properties.

After selecting the region where they wanted to retire, they worked with a local real estate agent who specialized in rural properties. Together, they toured several ten-acre farms that already included homes, barns, fencing, and established infrastructure.

Armed with realistic expectations, financial resources, and a growing knowledge of agriculture, they consulted with their adult children and ultimately decided to move forward.

The first year was challenging.

They spent countless hours repairing fences, improving soil, planting crops, caring for animals, and learning the realities of operating a small farm. There were mistakes, unexpected costs, and long days, but there were also successes.

By the end of their first growing season, Harry and Jennifer were selling vegetables, eggs, and specialty products at local farmers’ markets. They also established relationships with several local restaurants interested in purchasing fresh produce.

Their farm did not make them wealthy.

What it did accomplish was equally important.

By the end of the first year, the operation generated enough income to cover virtually all of its operating expenses. The property continued to appreciate in value, their family visited regularly, and they found tremendous satisfaction in building something together.

Looking back, Harry and Jennifer agreed that their greatest advantage was not money, land, or even farming experience.

It was the time they invested in planning, education, and developing realistic expectations before purchasing their farm.

Their story demonstrates an important lesson for anyone considering a small farm retirement investment: success rarely comes from buying the perfect property. It usually comes from becoming the kind of owner who is prepared to succeed.

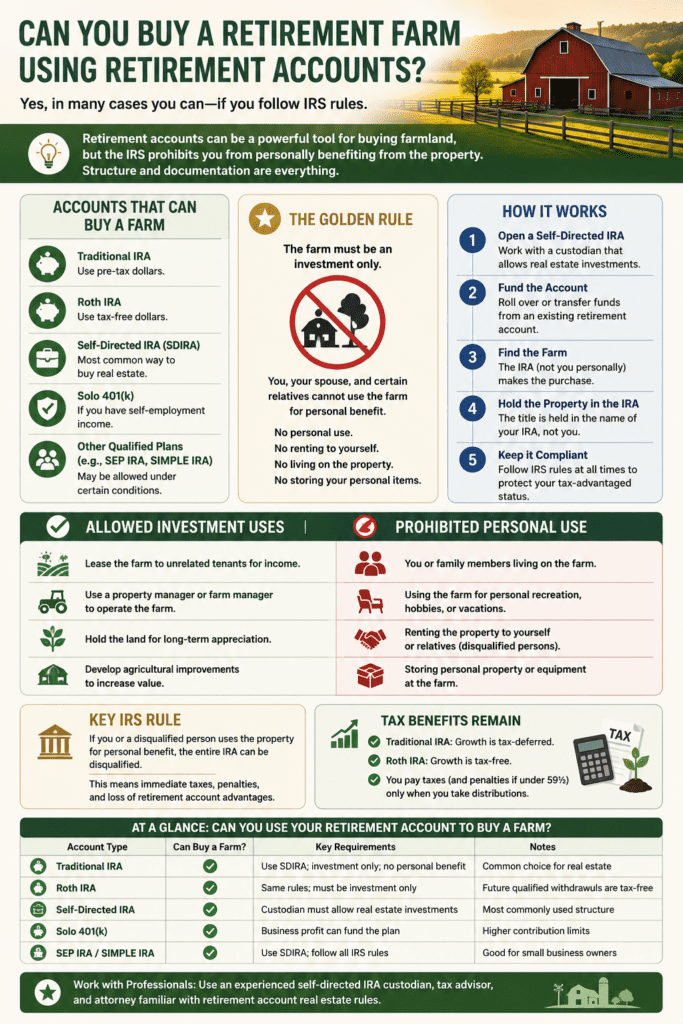

Can You Buy a Retirement Farm Using Retirement Accounts?

Many retirees are surprised to learn that certain retirement accounts can invest in farmland and other alternative investments.

However, the rules are far more complicated than many people realize.

Self-Directed IRAs and Agricultural Land

A self-directed IRA allows investors to purchase assets beyond traditional stocks, bonds, and mutual funds.

Depending on the custodian and account structure, investments may include:

- Agricultural land

- Rental property

- Raw land

- Certain private investments

- Alternative assets

Some investors use self-directed IRAs specifically to acquire farmland investments as part of a diversified retirement portfolio.

The Biggest Limitation

The IRS has strict rules regarding personal use.

If a self-directed IRA owns a farm:

- You cannot live on the property.

- You cannot personally operate the farm.

- You cannot use the property for personal recreation.

- Certain family members may also be restricted from using the property.

These restrictions are designed to prevent prohibited transactions.

Why Most Retirement Farms Do Not Belong in an IRA

Most retirees considering a retirement farm want to:

- Live on the property

- Raise livestock

- Garden

- Enjoy the rural lifestyle

- Use the land personally

Those goals generally conflict with retirement account ownership rules.

As a result, most retirement farms are purchased outside retirement accounts using personal funds, financing, or proceeds from other investments.

Farmland Investment vs. Retirement Farm Ownership

This distinction is important.

An investor purchasing agricultural land through a self-directed IRA is typically seeking:

- Capital appreciation

- Rental income

- Portfolio diversification

- Passive investment exposure

A retiree purchasing a small farm is usually seeking:

- Lifestyle benefits

- Personal enjoyment

- Farm income opportunities

- Legacy value

- Rural living

These are very different objectives.

Consult Qualified Advisors Before Proceeding

Retirement account rules can be complex.

A prohibited transaction may result in penalties, taxes, and unintended consequences.

Before using retirement funds to purchase agricultural land, consult qualified tax, legal, and financial professionals familiar with self-directed IRAs and farmland ownership.

For Most Retirees, the Question Is Simpler

The real question is often not whether a retirement account can buy a farm.

The better question is whether owning a farm aligns with your retirement goals, financial situation, and desired lifestyle.

For many retirees, the greatest value of a small farm comes from the ability to enjoy and use the property personally—something that retirement account ownership may prevent.

So, Is Buying a Small Farm a Good Investment for Retirement?

After examining the potential returns, risks, tax advantages, financing options, and ownership structures, we can finally answer the question posed by this article.

The answer is that a small farm retirement investment can be an excellent choice for the right person under the right circumstances.

It can also be a costly mistake if purchased for the wrong reasons.

A Small Farm Is Often a Good Investment When:

You Have Adequate Retirement Income

Retirees who already receive income from Social Security, pensions, investments, or retirement accounts often have the flexibility to enjoy the benefits of farmland ownership without depending entirely on farm income.

This allows the property to function as both an investment and a lifestyle asset.

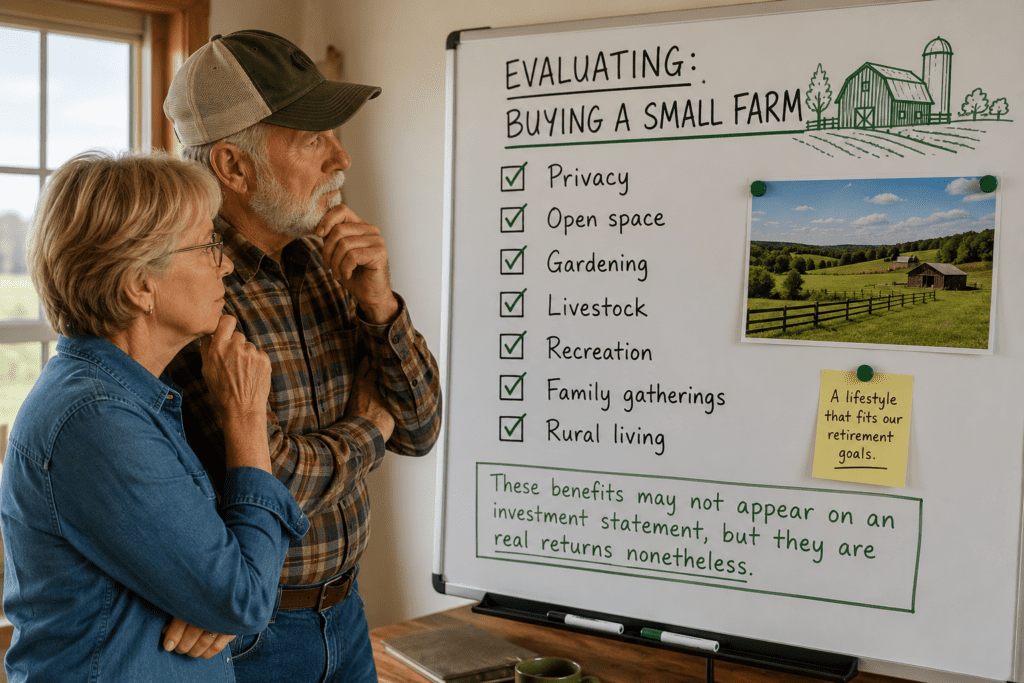

You Value More Than Financial Returns

Many retirees place significant value on:

- Privacy

- Open space

- Gardening

- Livestock

- Recreation

- Family gatherings

- Rural living

These benefits may not appear on an investment statement, but they are real returns nonetheless.

You Have a Long-Term Perspective

Agricultural land tends to reward patience.

Retirees who view a farm as a long-term investment often experience the greatest benefits from appreciation, inflation protection, and legacy value.

A Small Farm May Not Be a Good Investment When:

You Need Immediate Cash Flow

Many farms require years to reach their full income potential.

If monthly cash flow is the primary objective, other investments may provide more predictable results.

You Are Investing Most of Your Retirement Savings

Concentrating too much wealth into a single property increases risk.

A farm should strengthen financial security rather than threaten it.

You Dislike Ongoing Property Management

Even hobby farms require maintenance.

Buildings age.

Fences break.

Roads require repairs.

Equipment eventually needs replacement.

Ownership involves responsibility.

The Most Successful Retirement Farm Owners Share Common Traits

Over the years, I have noticed that successful retirement farm owners tend to:

- Buy appropriate acreage

- Maintain emergency reserves

- Avoid excessive debt

- Continue learning

- Start smaller than originally planned

- Maintain realistic expectations

- Focus on both lifestyle and financial returns

Most importantly, they understand that a retirement farm is rarely just an investment.

It is also a lifestyle decision.

My Verdict

If your goal is simply to maximize investment returns, a small farm may not be your best option.

If your goal is to combine financial security, tangible assets, inflation protection, lifestyle benefits, and legacy value, a carefully selected farm may become one of the most rewarding purchases of your retirement years.

The best retirement investments improve both your balance sheet and your quality of life.

For many retirees, a small farm accomplishes exactly that.

Test Your Knowledge: Retirement Farm Investment Quiz You’ve explored the benefits, risks, tax advantages, financing considerations, and investment potential of retirement farms. See how much you’ve learned before taking the Retirement Farm Suitability Assessment.🌾 Retirement Farm Investment Quiz

How much have you learned about evaluating a small farm as a retirement investment? Test your knowledge below.

Why I Enjoy Writing About Retirement Farms

My first effort at writing about small farms has been a success. Not only has the article attracted a surprising number of readers, but I thoroughly enjoyed researching and creating it. The response confirmed something I suspected all along—many people approaching retirement are seriously considering a second act that includes land, agriculture, and a simpler way of life.

As a real estate broker, I have shown small farms to prospective buyers over the years. Some were looking for a hobby farm, others wanted a homestead, and a few hoped to create a small business. What they all had in common was a dream, and I have always enjoyed helping people explore the possibilities.

Farming is also part of my family’s history. My mother’s family arrived from Germany in the 1830s and became farmers. Farms remain in the family today. Growing up, I listened to stories about spending summers on the family farm—working hard, playing hard, and enjoying the kind of fresh food that rarely makes it to a grocery store shelf.

Those stories helped shape my appreciation for rural life and the people who choose it. They also inspired me to look deeper into whether farming can be a practical retirement path for modern Americans.

I hope you find value in both this article and our companion guide, Farming After Retirement: Business or Lifestyle?. Together they represent my effort to provide some of the most complete and practical information available for people considering a retirement farm, a homestead, or a new agricultural adventure later in life.

Retirement Farm Suitability Assessment

Use this free tool to estimate whether buying a mini farm after retirement fits your health, budget, lifestyle, and long-term goals.

Final Questions Before Buying a Retirement Farm

After evaluating the benefits, risks, financing options, and investment potential, many retirees still have a few final questions before deciding whether farmland ownership belongs in their retirement plan.

How many acres do I need for a retirement farm?

The ideal size depends on your goals. Some retirees are perfectly happy on five to ten acres, while others prefer larger properties that support livestock, hay production, or recreational activities.

Bigger is not always better. Many first-time farm owners discover that managing additional acreage increases costs, maintenance, and workload without significantly improving their lifestyle or investment returns.

Should I buy farmland now or wait for lower prices?

Timing any market is difficult. Farmland values, interest rates, commodity prices, and local economic conditions can all influence purchase opportunities.

Most successful retirement farm owners focus less on short-term market timing and more on finding the right property at a reasonable price that supports their long-term goals.

What is the biggest mistake retirees make when buying a farm?

The most common mistake is purchasing too much property too quickly. Many buyers underestimate maintenance costs, physical demands, and ongoing responsibilities.

Starting with a manageable property and expanding later, if necessary, is often a safer and more enjoyable approach than overcommitting from the beginning.

Thinking About a Retirement Farm? Start Here.

This article is part of RetireCoast’s comprehensive series exploring the opportunities, challenges, financial considerations, and lifestyle realities of owning a farm later in life.

Is Buying a Small Farm a Good Retirement Investment? focuses on the financial side of the decision, including capital appreciation, farm income, cash flow, inflation protection, risk, and how a farm compares to traditional retirement investments.

For a complete understanding of the topic, we strongly recommend reading our companion pillar article:

📖 Farming After Retirement: Business or Lifestyle?

The pillar article examines farm types, retirement lifestyle considerations, business opportunities, startup planning, land selection, and the realities of transitioning from a traditional career into agriculture. Together, these articles provide one of the most comprehensive resources available for retirees considering a second act as a farmer, homesteader, or rural landowner.

🌾 Continue Your Retirement Farming Journey

Buying a farm is about more than acreage and investment returns. It is a decision that affects your finances, lifestyle, family, and retirement goals for years to come.

Before you make a final decision, explore the complete RetireCoast Farming After Retirement Series and take our free Retirement Farm Suitability Assessment to see how your goals, finances, and expectations align with farm ownership.

RetireCoast helps retirees evaluate major lifestyle and financial decisions through in-depth guides, calculators, assessments, and planning resources.

Reducing your tax burden is only one piece of a successful financial strategy. Building wealth, protecting assets, planning your estate, and creating additional income streams often require a deeper level of education and planning than a single article can provide.

To help our readers take the next step, RetireCoast now offers three premium membership programs designed to provide advanced tools, calculators, guides, and planning resources.

Choose the Membership That Fits Your Goals:

-

💼 Business Builder Membership

Designed for entrepreneurs, retirees starting businesses, real estate investors, and small business owners seeking strategies to increase income, improve operations, and legally reduce taxes. -

🛡️ Estate Planning Membership

Focused on wealth preservation, trusts, asset protection, estate planning, inheritance strategies, and protecting assets for future generations. -

📈 Millennial Financial Lab

Built specifically for Millennials and younger professionals seeking practical guidance on investing, retirement planning, debt reduction, major purchases, and long-term wealth building.

Many members find that more than one program fits their needs. For those who want access to every tool, calculator, guide, and membership resource across the RetireCoast platform, we offer an All-Access Membership that provides a substantial discount compared to purchasing all three memberships separately.

Whether your goal is reducing taxes, protecting assets, starting a business, preparing for retirement, or creating a lasting legacy, RetireCoast memberships provide the tools and guidance to help you move forward with confidence.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}