Last updated on December 17th, 2025 at 02:29 pm

Why You Should Buy Your Retirement Home Before You Retire

Buying your retirement home before you retire might be one of the smartest and most strategic decisions you can make. Many retired people wait until they’re no longer working to think about where to live in their golden years, but purchasing a new home earlier can reduce financial strain, lower long-term housing costs, and provide peace of mind as you approach retirement.

Whether you consider it a second home, vacation home, or your future retirement property, buying in advance offers several advantages that align with your retirement plans and future needs. It’s a good option for those with a steady income, retirement savings, and a clear idea of where they want to live during their retirement years.

Why Buy Your Retirement Home Early?

There’s one very good reason to purchase your future home before you leave the workforce: it’s easier to qualify for a new mortgage with a low debt-to-income ratio and steady income.

✅ Employment Income = Easier Approval

Lenders view W-2 income as more reliable than income derived solely from retirement accounts, retirement income, or rental property. Even with a strong credit score, qualifying for a mortgage can become more challenging once you’re on a fixed income.

If you’re still working, you may qualify for a better interest rate, a lower monthly mortgage payment, and a longer loan term, all while you continue building your retirement funds.

Lenders want a steady income that meets the debt-to-income ratio. Your salary is excellent proof that you can afford the property. Many people think that because they have a large amount in savings that this is good enough; it usually is not.

Lenders will look at the income that your savings will generate and use a portion of that to help meet the debt-to-income ratio. The fact that you have lots of money is not what they are looking for.

It’s the stability of income. This is the key reason to buy while you are employed. This article is one of several about buying a house. Do some research, starting with the many articles on this site about financing and more. In particular, use the “debt-to-income ratio” calculator contained in the article to determine if you qualify to buy another home if you owe on your existing home. This is an important first step.

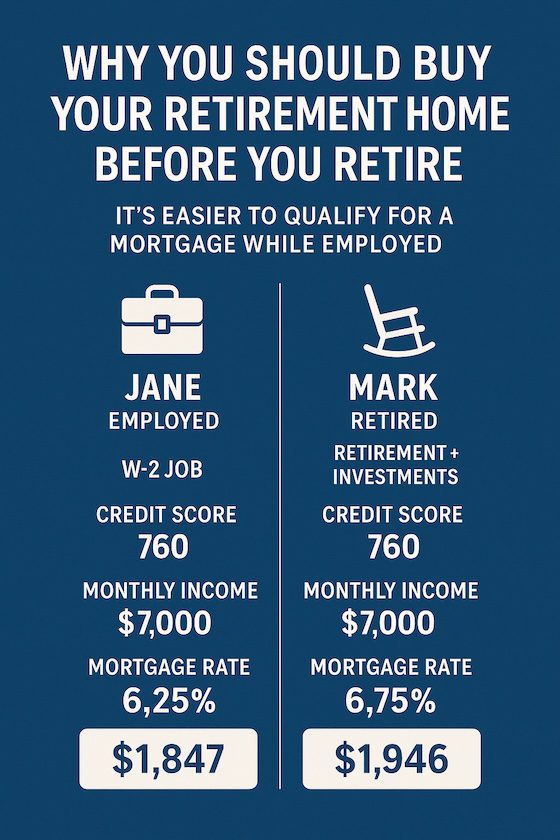

📉 Rate Differences: Working vs. Retired

Let’s look at two hypothetical borrowers applying for a 30-year fixed-rate mortgage on a $220,000 retirement house: *Rates as of Nov 2025. For personalized quotes, contact a retiree-specialized broker.

💡 Insight: $57/mo savings for Jane; $20K+ over 30 years because she is still employed.

↳ Logan-Anderson Gulf Coastal Realtors (free consult)

Even though they have identical monthly income and credit scores, Mark pays nearly $100 more per month because mortgage lenders treat retirement income as less stable. That’s a difference of $36,000 over 30 years.

This example below shows the complete picture with escrow included:

| Borrower | Income Type | Interest Rate | P&I | Property Taxes | Insurance | Total Monthly Cost |

|---|---|---|---|---|---|---|

| Jane | W-2 Job | 6.75% | $1,946 | $250 | $217 | $2,413 |

| Mark | Social Security + IRA | 7.25% | $2,047 | $250 | $217 | $2,514 |

Note: Assumes 20% down payment to avoid mortgage insurance. Property taxes are estimated at $3,000/year and homeowners insurance at $2,600/year.

🧮 Mortgage Payment Calculator: Plan Your Retirement Home Budget

Before buying your retirement home, it’s essential to understand what your monthly housing costs will be—not just the mortgage, but also property taxes, insurance, and other expenses. This calculator helps you estimate your total monthly payment based on your real inputs.

How to Use This Calculator:

- Enter your expected home price and down payment.

- Provide the loan interest rate, term, and estimated annual costs like property taxes and insurance.

- You can also include flood insurance and mortgage insurance, if applicable.

- The calculator will show your monthly breakdown and total cost.

- Use the Print button to save a copy for your records or review with your financial advisor.

💡 Tip: Adjust the inputs to compare different housing options, down payment sizes, or mortgage rates to find the best fit for your retirement plans.

Mortgage Payment Calculator

Monthly Payment Breakdown

Principal & Interest: $0.00

Property Taxes: $0.00

Homeowners Insurance: $0.00

Flood Insurance: $0.00

Mortgage Insurance: $0.00

Total Monthly Payment: $0.00

Note: Assumes 20% down payment avoids mortgage insurance.

Things to Consider When Buying Your Retirement Home

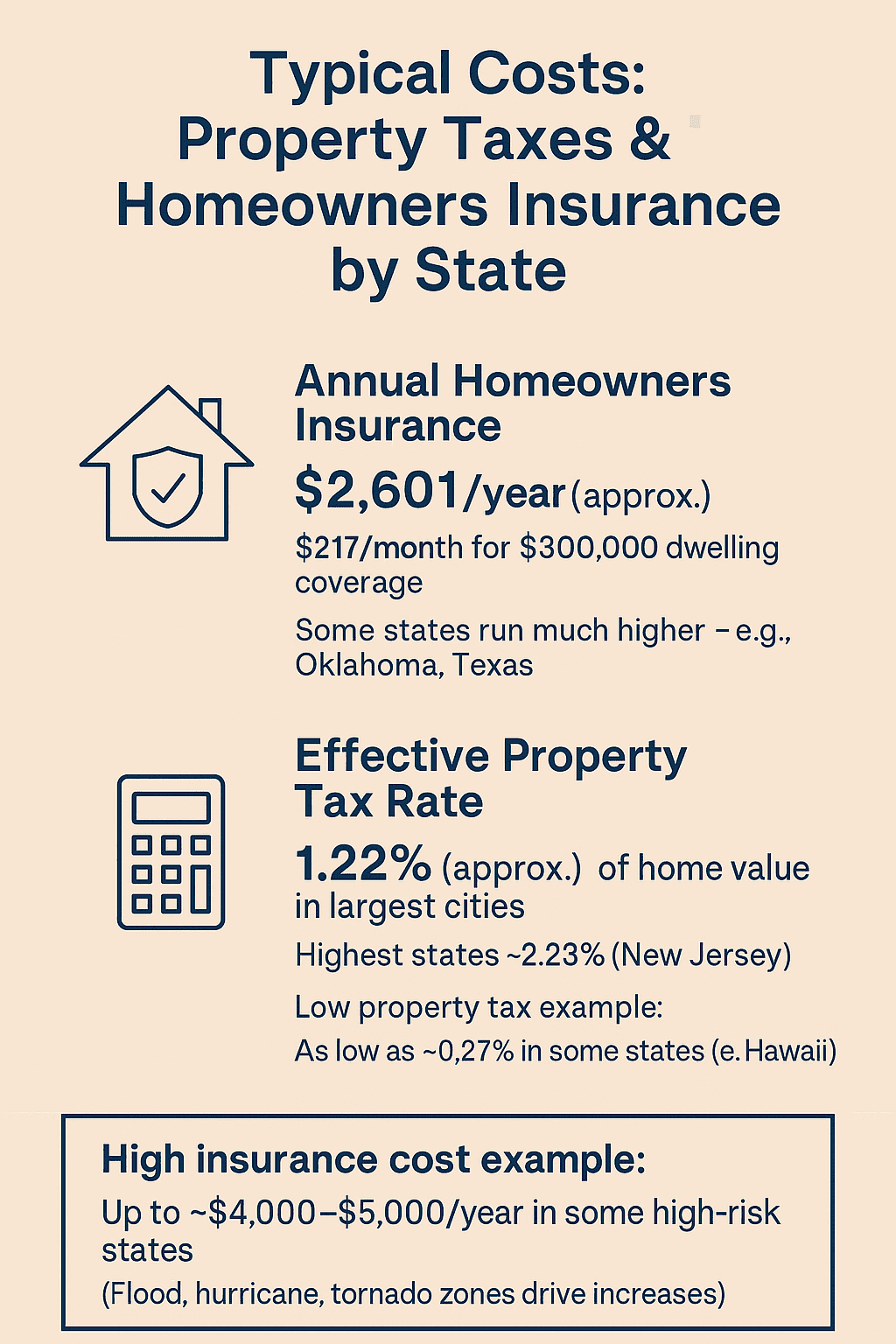

Purchasing your retirement home requires more than simply calculating your monthly mortgage payments. Careful planning includes a deeper look at all long-term costs and the ongoing expenses that come with owning a new home—whether it’s a second home or your future primary residence.

🧾 Total Monthly Housing Expenses

- Your monthly payment includes principal, interest, and escrow for property taxes and homeowners' insurance.

- Even if your new mortgage is eventually paid off, insurance and property taxes will continue—and likely increase over time.

- Consider the trend in real estate prices and local tax policies to forecast long-term affordability.

💵 State Tax Considerations

- Some states (like Mississippi) do not tax retirement income, while others (like California) tax pensions, Social Security, and IRA withdrawals.

- Ask: What is the state income tax rate on retirement accounts?

- Also, check sales tax and vehicle registration fees, as these vary widely and impact your monthly budget.

🔧 Maintenance & Repairs

- Every home requires repairs and ongoing maintenance, regardless of age.

- Estimate annual costs for:

- HVAC service

- Roof upkeep

- Lawn care /landscaping

- Appliance replacement

- Many retired people underestimate this financial strain—budget accordingly.

🔎 Hidden and Future Needs

- Will you need to make home improvements (e.g., fewer stairs, ramps)?

- Are there medical facilities nearby?

- How will your mobility or health affect your ability to maintain a larger home or yard?

Taking the time to fully evaluate these long-term costs can help you avoid surprises and ensure your retirement years are spent in the right place. Consider working with a certified financial planner and an experienced real estate agent to make the best decision for your future needs get to factor in these expenses, but over time, home improvements and repairs can cost thousands—even in your golden years.

2026 Insurance Realities: Gulf Coast wind/flood policies will be up 16% by 2027; Mississippi Strengthen Homes grants cover $10K mitigations. "Build higher, stay out of floodplains."

💡 Pro Tip: When you’re ready to explore listings before you retire, work with a broker who specializes in second-home mortgages and 55+ communities. → [Browse current Gulf Coast retirement listings with Logan-Anderson Gulf Coastal Realtors]

🧾 What If You’re Self-Employed or a Freelancer?

Obtaining a mortgage without a W-2 job can be more difficult—but it’s definitely not impossible. If you're self-employed, a freelancer, a gig worker, or a small business owner, you don’t receive a paycheck or W-2, which means lenders will scrutinize your income documentation more closely.

Still, many retired people, self-employed individuals, and early retirees secure financing for a retirement home, second home, or investment property every day. Here’s what you need to know:

✅ The Good News:

- If you're already retired and receive Social Security, a pension, or retirement income, these are treated similarly to W-2 income by many mortgage lenders.

- Having a low debt-to-income ratio, a strong credit score, and solid retirement accounts or retirement savings will help your case.

- A larger down payment (20% or more) can offset other risk factors.

📋 What Lenders Expect from Self-Employed Borrowers:

To qualify for a mortgage without a job, lenders typically require:

- Two full years of federal tax returns (usually Schedule C or business returns)

- Consistent or rising income over the 2-year period

- Proof of ongoing work or contracts (for freelancers or gig workers)

- Business license (if applicable)

- Bank statements verifying steady income and financial reserves

- Possibly a letter from your CPA confirming self-employment status

💡 DSCR Loans: An Alternative Option

A type of loan often offered to self-employed individuals is a DSCR loan (Debt Service Coverage Ratio). These loans are primarily based on the income generated by the property rather than your personal income. They are commonly used for investment property purchases or vacation rentals, and are a great way for self-employed buyers to qualify without extensive tax documentation.

Tip: DSCR loans don’t require W-2s or pay stubs, but the property must meet certain income-to-expense criteria to qualify. They’re especially helpful if you're buying a retirement property that you intend to rent short-term before moving in.

🧮 Try the DSCR Loan Calculator

💡 Want a lender who accepts DSCR? → Browse DSCR-friendly Gulf Coast listings with Logan-Anderson Gulf Coastal Realtors. Try the DSCR loan calculator at Logan-Anderson Gulf Coastal Realtors.

🧠 Pro Tip:

Before applying, work with a certified financial planner or mortgage broker who understands the self-employed borrower profile. Careful planning will improve your chances of securing a competitive interest rate, avoiding financial strain.

Buying your future home as a self-employed or retired borrower is very possible—it just requires a bit more documentation and planning. The earlier you prepare, the better your chance of success.

Financial Strategies to Afford It While You Work

A smart move is to align your future plans with your current financial situation. Here are some strategies:

- If you’ve reached retirement age (66–67), consider starting Social Security and using those benefits toward your monthly payments.

- Downsize from your current home and invest the equity into your retirement property.

- Consult with a certified financial planner or real estate agent to understand your options.

- Use a home equity line of credit or home equity loan on your current house to help fund your new property.

- Borrow up to $50,000 from your retirement accounts for a down payment, if your plan allows. Borrowing from a 401(k) allows up to $50K, but must repay within 5 years to avoid taxes—use IRS Pub 575 for details.

How long will my savings last? A good article to review here.

Consider Renting or Using the Home Occasionally

One important decision to make after buying your retirement home is whether or not to rent it out before you move in permanently. Your decision should depend on your financial stability, how long it will be before you relocate, and whether the home will be furnished.

If you plan to use the home as a vacation home, you may choose not to rent it—even on a short-term basis. Many retirees prefer to keep the space private and available for occasional visits as they prepare for their full transition.

However, if you won’t be moving for several years and you don’t plan to furnish the home right away, long-term renting (6–12 months or more) may be a good option. You could also consider a month-to-month lease, giving you flexibility to reclaim the property when needed.

If you decide to rent your future home, especially from a distance:

- Hire a property manager to oversee maintenance, collect rent, and handle tenant issues.

- Be aware that short-term rentals—while attractive in tourist areas—require full furnishings and constant upkeep. Frequent guest turnover can wear down furniture and appliances, possibly requiring refurbishment before you move in.

My recommendation: Don’t buy your retirement home if you can’t afford to keep it without relying on rental income.

People who depend on rent to cover their mortgage or costs risk financial trouble if tenants don’t pay or cause property damage. Always plan conservatively and ensure your retirement savings or monthly income can cover expenses—rented or not.

Buying Far From Home? Hire a Property Manager

If your new location is far from your current home, hiring a property manager is a good idea. They can:

- Maintain landscaping and monitor for security issues

- Help manage vacation rentals or tenant relations

- Provide inspections before and after storms

This is especially important if your new home is located in a region prone to weather events.

My Experience Buying Before Retirement

We started planning years before retirement. California’s real estate prices and long-term costs didn’t align with our future needs, so we looked elsewhere. First, we tried Las Vegas. We bought a new home in a planned community and thought we’d found the right place.

After a year, we realized it wasn’t meeting our changing needs—we missed greenery, water, and a slower pace. So, we sold it (at a profit) and purchased our future retirement home on the Mississippi Gulf Coast. Because I was still working, I had no problem qualifying for a second home mortgage.

The biggest difference? Flexibility. We were able to course-correct, sell the first home, and find a better option before retirement.

We also made updates:

- Installed security cameras and a Ring doorbell

- Added a lawn sprinkler system

- Worked with a neighbor who helped with yard care and kept an eye on the property

This process gave us both financial stability and peace of mind.

Gen X? Check out this article about budget planning for retirement.

Want to compare retirement accounts that can help reduce taxes now or later? Use this guide to understand the most common tax-advantaged options and how they typically work.

Read the guide →After Closing on Your Retirement Home

Your future home will become a reflection of your long-term plans. Many choose to sell or donate furniture from their current house and start fresh. Shopping for new furnishings can be invigorating, especially as your tastes evolve.

It also reduces your monthly housing expenses during the move. Shipping heavy items like a 30-year-old recliner or worn-out lawnmower often costs more than replacing them.

Benefits of refreshing your space:

- Modernize for mobility issues

- Choose fewer stairs or smaller spaces

- Express your current style

- Enjoy a new chapter with a clean slate

Plan Ahead for the Physical Move to Your Retirement Home

Use your early visits to research medical facilities, vehicle registration, local services, and retirement community options.

Things to take care of before your move:

- Change your Social Security address

- Update your Medicare insurance provider for your state

- Obtain new driver’s licenses

- Change vehicle insurance and registration

- Transfer medical and dental records

- Learn the local tax and property tax structure

- Notify banks, credit cards, and investment firms

- Explore Medicare Part B costs in your new state

- Register to vote in your new area

- Explore home improvements or renovations for accessibility

Tackling these items early reduces stress and ensures a smooth transition into your later years.

What to Do with Your Existing House When You Move

One of the important decisions you’ll need to make when buying your retirement home is what to do with your current house. If you don’t need the funds from selling it right away, renting it out can be a good option that provides extra income and builds long-term wealth.

But there are trade-offs—especially if the home is far from your new location.

✅ Pros of Renting Your Existing Home:

- Ongoing monthly income that can help offset your new mortgage or supplement your retirement income

- Retains property for potential appreciation in a rising real estate market

- Allows you to diversify your retirement plans with investment property income

- Keeps your options open if you ever want to return

❌ Cons of Keeping a Distant Property:

- Difficult to manage if it's far from your retirement house

- May require hiring a property manager for maintenance and tenant issues

- Ongoing expenses include property taxes, insurance, and repairs

- Risk of vacancies or problematic tenants

- Ties up equity you could use for financial stability or home improvements in your new home

Renting your current home can be part of a smart long-term plan, but only if it aligns with your goals, time, and resources. Always consult with a financial advisor to decide whether selling or renting better supports your retirement savings and lifestyle.

My suggestion is that you not rely on rental income. There are too many variables, including potential periods of vacancy. If you believe that values will increase and you can afford to make payments, or you own the property outright, you will be in a better position to weather any low or non-income issues. I sold mine after I moved to my retirement home.

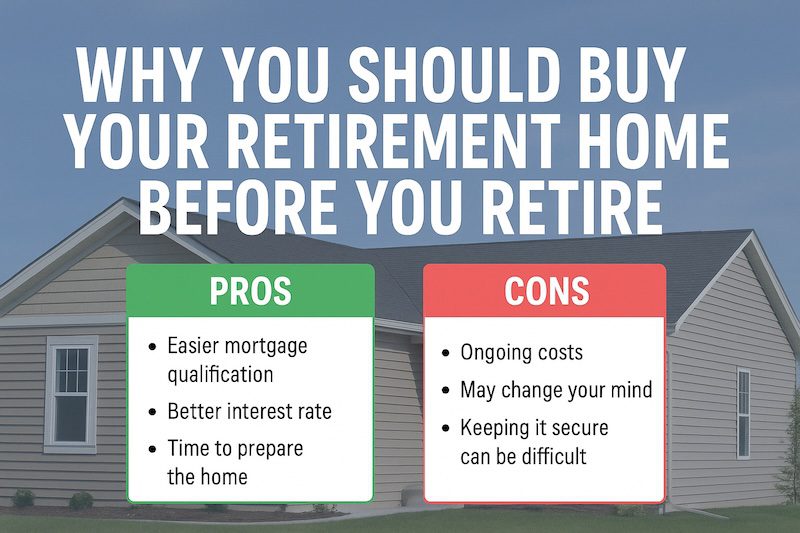

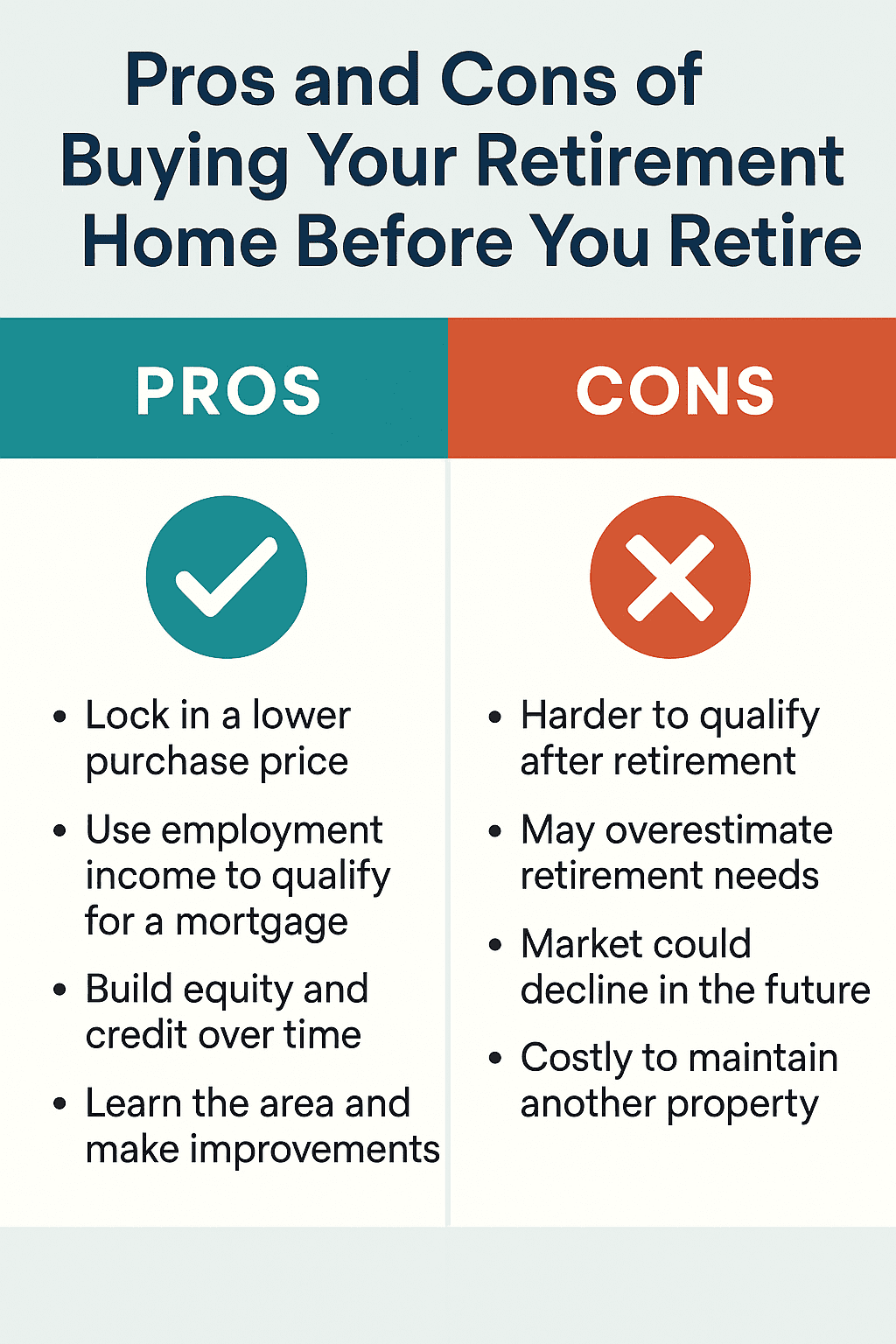

Pros and Cons of Buying Before You Retire

✅ Pros

- Easier approval with steady income

- Lower interest rates and monthly mortgage payments

- Use as an investment property or a rental property

- Lock in lower real estate market prices

- Tailor the new home to your future plans

- May reduce long-term costs and financial strain

- Improves access to financial resources and planning time

- Potential for equity to increase

❌ Cons

- Carrying two mortgages for a while

- Added monthly housing expenses before you move

- May require help from a financial advisor

- May complicate taxes or insurance in the short term

Final Thoughts: Plan Early, Live Better

Buying your retirement home before retirement might be the best approach to preparing for the years ahead. With careful planning, guidance from a real estate agent or financial advisor, and a clear understanding of your financial situation, you can find your dream home, reduce stress, and enjoy your golden years in the right place.

Don’t wait for the last thing on your checklist. Starting early gives you flexibility, stability, and the freedom to enjoy your new property when the time is right.

🌴 Consider Retiring on the Mississippi Gulf Coast: Here’s Why

If you're looking for a peaceful, affordable, and enriching place to enjoy your retirement years, the Mississippi Gulf Coast should be at the top of your list. Whether you're planning a move from a high-cost state or simply want to enjoy life at a more relaxed pace, this region offers a unique blend of lifestyle, value, and opportunity.

✅ Top 10 Reasons to Retire on the Mississippi Gulf Coast

- Affordable Housing Costs – Homes are significantly more affordable than in many other coastal or retirement destinations.

- No State Tax on Retirement Income – Mississippi does not tax pensions, 401(k), IRA withdrawals, or Social Security.

- Mild Climate Year-Round – Enjoy warm weather without the extreme heat of the Southwest or the cold of the North.

- Rich Coastal Culture – From seafood festivals to art galleries, the region has a thriving cultural scene.

- Access to Medical Facilities – Multiple hospitals, VA centers, and clinics are available throughout the region.

- Natural Beauty & Outdoor Living – Miles of coastline, bayous, and parks perfect for boating, fishing, hiking, and birdwatching.

- Low Property Taxes – One of the lowest effective property tax rates in the country.

- Strong Retirement Communities – Plenty of 55+ communities and retirement-friendly developments.

- Convenient Travel Access – Nearby airports, Amtrak, and I-10 make travel easy for retirees and visiting family.

- Slower Pace of Life with Big-City Perks – Gulfport, Biloxi, and Ocean Springs offer restaurants, shopping, and entertainment without the congestion of a major metro.

🏡 Home Price Comparison: Mississippi vs. Florida & North Carolina

One of the biggest differences in choosing your retirement location is the cost of housing. In Mississippi, the average home value is just $200,000—that’s 40%–50% lower than national averages and more than 100% lower than in Florida and North Carolina. Here’s a simple comparison:

| State | Median Home Price | Compared to MS |

|---|---|---|

| Mississippi (MS) | $200,000 | — |

| Florida (FL) | $417,000 | +108% |

| North Carolina (NC) | $380,000 | +90% |

💡 Smart Move: Lower housing costs in Mississippi give you more flexibility in your retirement budget—whether you want a larger home, lower monthly mortgage, or extra money for travel or investments.

🏠 Planning a Visit? Start Here

If you are planning to visit the area where you want to retire, such as the Mississippi Gulf Coast, I recommend you stay at a vacation home property. There are many to choose from on the Mississippi Gulf Coast.

When you're ready to start your home search, consult Logan-Anderson Gulf Coastal Realtors.

Feel free to browse our current listings and see what's available on our website: GulfCoastalRealtors.com.

📚 Want to Learn More?

Please read other articles on this blog about retirement strategies, investment planning, and living on the Mississippi Gulf Coast.

Here are two of our most popular articles:

- 🌟 Why I Decided to Retire in Ocean Springs, Mississippi

- 🌟 Why You Need to Retire on the Mississippi Gulf Coast

- 🌟 What happens when you finish paying off your house

- 🌟 The complete guide to home buying costs and benefits

- 🌟 How to improve your credit score for a mortgage

These articles share personal insights and practical advice that can help you make one of life’s most important decisions with confidence.

Frequently Asked Questions About Buying a Retirement Home Before You Retire

1. Why should I buy a retirement home before I retire?

Buying early lets you lock in current prices, qualify with your employment income, and prepare your home gradually while still working.

2. What are the financial benefits of buying early?

You may secure lower interest rates, spread mortgage payments across more working years, and build equity before retirement begins.

3. Can I qualify for a mortgage more easily while still employed?

Yes. Steady W-2 income helps you qualify for larger loans and better rates than relying solely on retirement income later.

4. How do mortgage lenders view retired borrowers vs. working borrowers?

Lenders prefer employment income. Retired borrowers must prove income from Social Security, pensions, or investments, often with more documentation.

5. Can I use my 401(k) or IRA for a down payment?

Yes, but with restrictions. You may borrow from a 401(k) or use a self-directed IRA. Always consult a financial advisor first.

6. Should I sell my current home before buying a retirement home?

Not always. Some keep their current home for flexibility, while others sell to free up cash and reduce carrying two mortgages.

7. Can I rent out the retirement home until I move in?

Yes. Many buyers rent the home as a vacation rental or long-term lease to cover expenses and generate income until retirement.

8. Should I buy during a buyer’s market?

Yes. Purchasing when prices dip can increase equity growth and reduce competition from other retirees later.

9. Should I downsize before retiring?

Downsizing early lowers costs, reduces upkeep, and lets you use equity from your current home for retirement needs.

10. How does buying early affect my retirement planning?

It provides stability, removes future housing uncertainty, and allows you to budget more accurately for retirement expenses.

11. What if I change my mind about the location?

Buying early gives flexibility. You can sell, rent, or adjust plans without pressure once you reach retirement age.

12. What should I consider when choosing a retirement location?

Evaluate cost of living, healthcare access, taxes, climate, proximity to family, and retirement-friendly amenities.

13. Should I consider states with lower taxes?

Yes. States like Mississippi and Florida offer tax advantages that can stretch retirement income further.

14. Can I get a second home mortgage if I buy early?

Yes, but terms differ from primary mortgages. Lenders may require larger down payments and higher rates.

15. What home improvements should I make before moving in full-time?

Common updates include flooring, painting, security systems, and accessibility upgrades to fit long-term needs.

16. How can buying early help me get to know the community?

Owning before retirement gives time to build friendships, join local clubs, and test lifestyle fit before settling permanently.

17. What paperwork should I update when relocating?

Update your Social Security, Medicare provider, vehicle registration, driver’s license, insurance, and credit card billing addresses.

18. What are the risks of buying before retirement?

Market shifts, unexpected job loss, or lifestyle changes may affect your ability to keep or enjoy the property long-term.

19. How should I factor in healthcare access?

Proximity to hospitals, specialists, and senior services should be a top priority when selecting your retirement home location.

20. What ongoing costs should I plan for?

Include property taxes, HOA fees, maintenance, insurance, and utilities when calculating retirement housing costs.

21. Can I treat the retirement home as an investment?

Yes. Early ownership allows rental opportunities, potential appreciation, and diversification of your retirement portfolio.

22. How far in advance should I buy before retiring?

Many buy 5–10 years early, allowing time to pay down debt, make improvements, and test the community.

23. Should I consult both a financial planner and a real estate agent?

Yes. Coordinating professional advice ensures your purchase aligns with both your housing and retirement goals.

24. Is buying early a good idea for everyone?

No. Those with unstable jobs, limited savings, or uncertain retirement plans may benefit from waiting.

25. What is the single biggest advantage of buying before retirement?

Peace of mind. You’ll know your future home is secured, reducing stress and allowing you to focus on enjoying retirement.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}