Last updated on March 29th, 2026 at 08:18 pm

A Guide to Funding Your Revocable Living Trust

What It Means, Why It Matters, and Exactly How To Do It

When you create a Revocable Living Trust, signing the document is only the first step.

If you do not transfer assets into the trust, your estate plan may fail to accomplish its primary goal: avoiding probate and ensuring smooth management if you become incapacitated.

This article explains:

- What “funding” a trust actually means

- Why funding is critical

- How to transfer different types of assets

- How to handle real estate, LLCs, partnerships, and corporate shares

- Common mistakes to avoid

- How our tools simplify the process

- A Guide to Funding Your Revocable Living Trust

- What Does “Funding” a Trust Mean?

- Why Funding Matters

- Funding Real Estate

- How to Transfer Real Property Into Your Trust

- Where Do You File a Quit-Claim Deed?

- Obtaining the Correct Parcel Number

- Why Use a Quit-Claim Deed?

- Using Our Quit Claim Deed Tool

- Funding Bank Accounts

- Brokerage Accounts and Investment Accounts

- Retirement Accounts (Important Exception)

- Life Insurance Policies

- Funding LLC Interests

- How to Transfer LLC Membership to Your Trust

- Our LLC Member Minutes Tool (Coming Soon)

- Funding Business Partnerships

- Funding Corporate Shares

- Personal Property

- Digital Assets

- Common Funding Mistakes

- Should You Transfer Everything?

- The Practical Strategy

- Why This Matters for Business Owners

- Our Philosophy

- Final Thoughts

What Does “Funding” a Trust Mean?

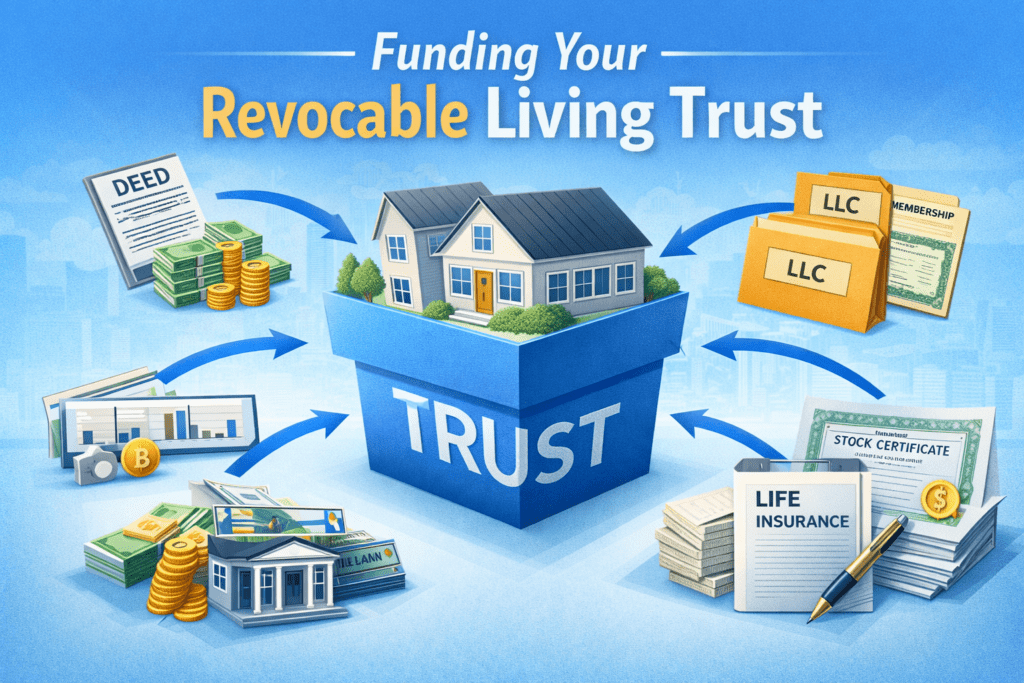

Funding your trust means retitling or assigning ownership of assets from your individual name to the name of your trust.

For example:

Instead of:

Richard Jones

You would hold the title as:

Richard Jones Trustee of the Jones Revocable Living Trust dated January 1, 2026

If the asset remains in your personal name, it is generally not controlled by the trust and may still require probate.

Why Funding Matters

Proper funding accomplishes three major objectives:

1️⃣ Avoids Probate

Assets properly titled in the trust typically avoid court-supervised probate proceedings.

2️⃣ Ensures Continuity During Incapacity

If you become incapacitated, your successor trustee can step in and manage trust-owned assets without court involvement.

3️⃣ Creates Administrative Simplicity

Your successor trustee can manage or distribute assets according to your written instructions without legal obstacles.

Funding Real Estate

Real estate is often the most important asset to transfer.

How to Transfer Real Property Into Your Trust

The standard method is a Quit Claim Deed.

Step-by-Step:

- Prepare a Quit Claim Deed transferring property:

- From: You (individually)

- To: You, as Trustee of your Trust

- Include:

- Full legal property description

- Parcel number

- Proper trust title format

- Required state disclosures

- Sign before a notary.

- Record the deed at the county land records office.

- Verify that the recorded deed reflects the trust as the owner.

Where Do You File a Quit-Claim Deed?

In the United States, real estate records are maintained at the county level.

Depending on your state, the recording office may be called:

- County Recorder

- Recorder of Deeds

- Register of Deeds

- Chancery Clerk

- Land Records Office

Each county manages its own recording system.

How to File

After the deed is:

- Properly prepared

- Correctly formatted

- Signed

- Notarized

You must record it with the county where the property is located.

In many counties, you can mail the notarized document.

However, if you are local to the courthouse, it is often best to deliver it in person. This allows you to:

- Confirm formatting requirements

- Verify margin and page standards

- Ensure the required information is present

- Avoid rejection delays

If the office accepts your deed, ask for a stamped receipt showing the date and time of recording.

Recording is what makes the transfer legally effective against third parties.

Obtaining the Correct Parcel Number

Every property parcel in the United States has a unique identification number, often called:

- Parcel Number

- Tax Parcel ID

- Assessor’s Number

- Property Identification Number

This number is usually listed on:

- Your current deed

- Property tax statements

- County tax assessor website

If you cannot locate your deed:

- Visit your county’s online land records site.

- Search by:

- Property address

- Your name

- Retrieve the legal description and parcel number.

Accuracy matters. An incorrect legal description or parcel number can invalidate the transfer.

Why Use a Quit-Claim Deed?

Many people ask:

Why not use a warranty deed?

There are several types of deeds commonly used in real estate transfers:

1️⃣ General Warranty Deed

Provides the highest level of protection.

The grantor guarantees clear title against all prior claims.

2️⃣ Special Warranty Deed

Provides limited protection.

The grantor guarantees title only during the period they owned the property.

3️⃣ Quit Claim Deed

Provides no warranties.

It transfers whatever interest the grantor currently holds.

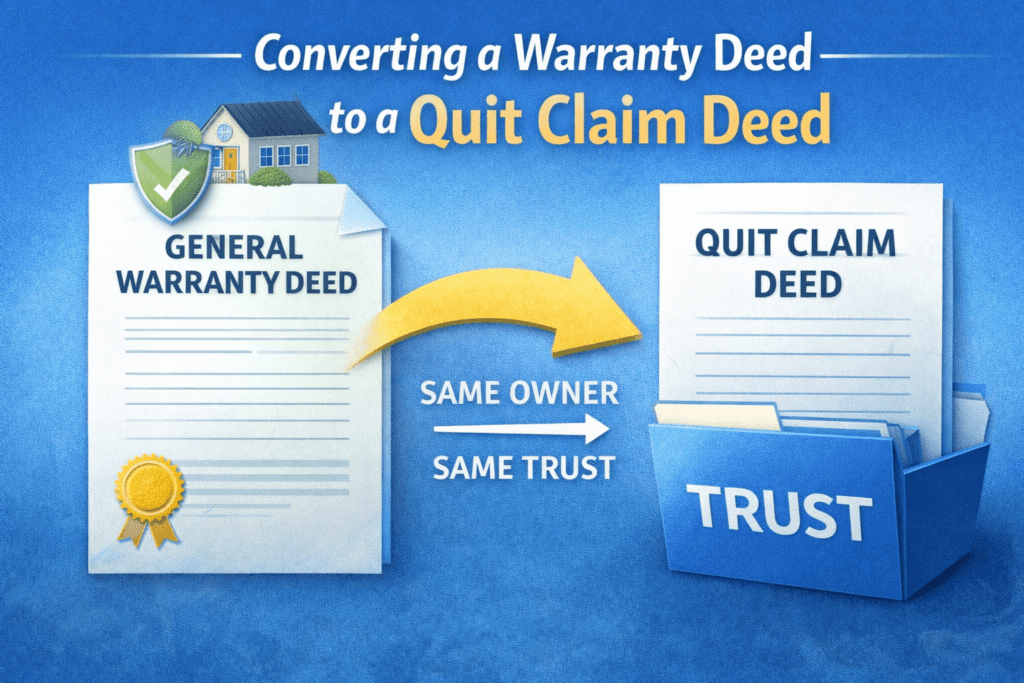

Why a Quit Claim Deed Is Appropriate for Trust Funding

When you originally purchased your property, you likely received:

- A General Warranty Deed

or - A Special Warranty Deed

At that time, a title insurance company insured the property against defects in title.

When transferring your home into your revocable trust, you are:

Essentially transferring the property from yourself individually to yourself as trustee.

Because ownership is not changing to a third party, a Quit Claim Deed is typically appropriate and sufficient.

You are not selling the property.

You are not adding risk.

You are simply changing how title is held.

That is why Quit Claim Deeds are commonly used in estate planning.

Using Our Quit Claim Deed Tool

Members of RetireCoast can use our Quit Claim Deed Generator Tool to:

- Automatically format trustee language

- Insert correct vesting language

- Generate a printable deed

- Reduce drafting errors

- Avoid paying hourly legal drafting fees

This tool does not provide legal advice — but it ensures formatting accuracy and completeness.

Funding Bank Accounts

Most banks allow you to retitle accounts into the trust.

Steps:

- Contact your bank.

- Provide:

- Trust certification or abstract

- Trust name and date

- Open a new account in the trust name or retitle the existing account.

- Update checks and account agreements.

You may wish to maintain:

- Checking account

- Savings account

- Money market accounts

- CDs

Brokerage Accounts and Investment Accounts

Brokerages allow trust registration.

Steps:

- Contact brokerage.

- Provide trust documentation.

- Complete a new account or a change-of-registration form.

- Confirm title reflects trustee capacity.

Common accounts to review:

- Taxable brokerage accounts

- Individual investment accounts

- Non-retirement investment holdings

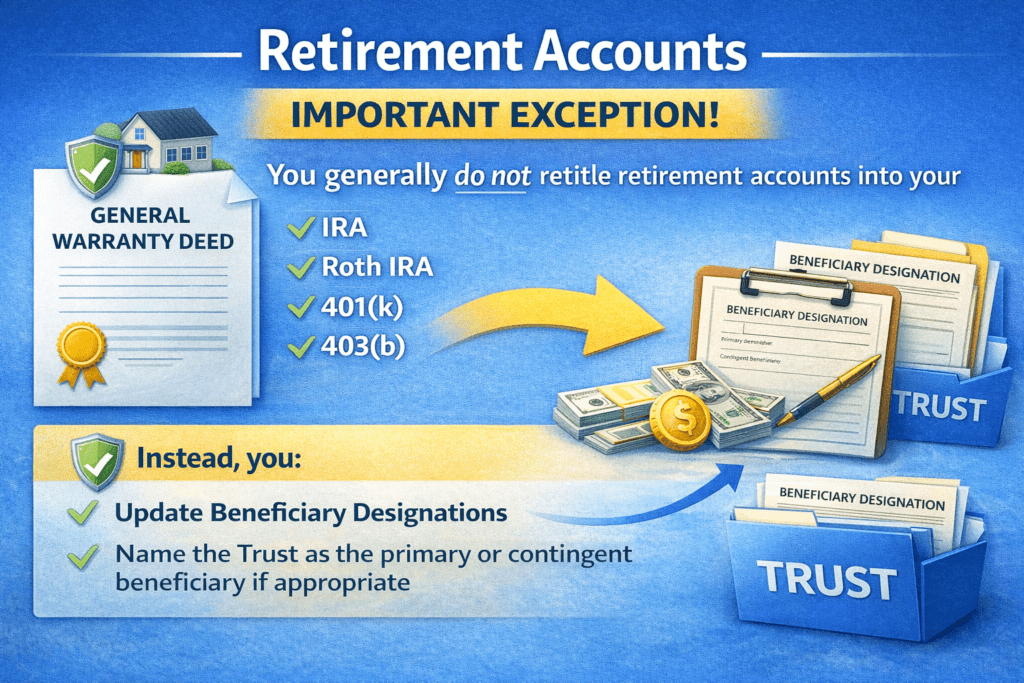

Retirement Accounts (Important Exception)

You generally do not retitle retirement accounts into your trust.

These include:

- IRA

- Roth IRA

- 401(k)

- 403(b)

Instead, you:

- Update beneficiary designations

- Name the trust as the primary or contingent beneficiary if appropriate

Always coordinate retirement planning carefully to avoid tax consequences.

Life Insurance Policies

You typically:

- Do not transfer ownership unless strategic

- Instead, update the beneficiary designation

Options:

- Name your spouse

- Name your trust

- Name children

- Use contingent beneficiaries

Funding LLC Interests

This is one of the most misunderstood areas.

If you own membership in a Limited Liability Company (LLC), you do not transfer the LLC’s real estate or assets individually.

You transfer:

Your membership interest in the LLC

How to Transfer LLC Membership to Your Trust

Step 1: Review the Operating Agreement

Check for restrictions on transfer.

Step 2: Prepare an Assignment of Membership Interest

You assign your ownership percentage to yourself as Trustee.

Step 3: Create Member Minutes

You document:

- Authorization of transfer

- Acceptance of trust as a new member

- Updated membership ledger

Our LLC Member Minutes Tool (Coming Soon)

We are creating a structured tool that will:

- Generate LLC transfer minutes

- Document assignment of membership

- Update ownership records

- Facilitate transfer of partnership interests

- Help transfer corporate shares

This tool can also assist in:

- Transferring business partnership interests

- Transferring shares in a closely held corporation

- Recording board or shareholder consent

Proper documentation protects:

- Liability shield

- Tax classification

- Internal ownership clarity

Funding Business Partnerships

If you are part of a partnership:

- Review the partnership agreement.

- Confirm transfers are permitted.

- Execute Assignment of Partnership Interest.

- Update partnership records.

Our upcoming business transfer documentation tool will help generate:

- Assignment documents

- Partner consent forms

- Meeting minutes

Funding Corporate Shares

For closely held corporations:

- Review shareholder agreement.

- Prepare Stock Assignment.

- Reissue stock certificate to trust.

- Record transfer in corporate ledger.

- Update minutes of meeting.

Failure to update corporate records can invalidate the transfer.

Personal Property

You may transfer:

- Furniture

- Jewelry

- Artwork

- Household goods

Often done through:

General Assignment of Personal Property

This is typically attached as Schedule A to your trust.

Digital Assets

Consider:

- Online accounts

- Crypto holdings

- Domain names

- Revenue platforms

These require:

- Access instructions

- Account inventory

- Possibly assignment documents

Common Funding Mistakes

❌ Forgetting to record the deed

❌ Not updating LLC operating agreements

❌ Failing to change beneficiary forms

❌ Transferring retirement accounts incorrectly

❌ Ignoring corporate stock ledgers

❌ Forgetting out-of-state property

Should You Transfer Everything?

Not necessarily.

Assets often not transferred:

- Vehicles (varies by state)

- Retirement accounts (retitle vs beneficiary)

- Certain small personal items

The Practical Strategy

At RetireCoast, we encourage a structured approach:

- Create the trust.

- Create a written funding checklist.

- Complete real estate transfers first.

- Address business interests.

- Retitle financial accounts.

- Update beneficiary designations.

- Maintain documentation.

Why This Matters for Business Owners

If you own:

- Rental property through an LLC

- Professional practice

- Family business

- Real estate partnerships

Funding is not optional.

Proper documentation:

- Preserves liability protection

- Ensures continuity

- Simplifies succession

- Avoids probate

Our Philosophy

RetireCoast does not provide legal advice.

Our goal is to:

- Educate you

- Provide structured tools

- Help you prepare intelligently

- Reduce unnecessary professional costs

When you walk into an attorney’s office with:

- Completed drafts

- Clear asset list

- Transfer documents prepared

- Minutes drafted

The meeting becomes review instead of preparation.

That can reduce fees substantially.

Final Thoughts

Creating a Revocable Living Trust without funding it is like building a safe and never putting anything inside.

Funding is the step that activates your plan.

Real estate.

LLC interests.

Corporate shares.

Bank accounts.

Brokerage accounts.

Each requires deliberate action.

With proper structure — and the right documentation tools — you can complete the process confidently and efficiently.

Funding your revocable living trust is a powerful step — but preparation matters. Before transferring assets, make sure you understand the structure, trustee responsibilities, and long-term strategy behind your estate plan.

- 📘 Read our complete guide: Revocable Living Trust Master Guide

- 🧭 Carefully evaluate your trustee selection using our member tools available inside the Estate Planning Membership — including the Successor Trustee Evaluator and Trust Funding Guide.

- 🛠️ Access structured estate planning tools designed to help you build, organize, and execute your plan inside the Estate Planning Membership

For additional perspective on passing assets efficiently, see these educational resources:

1) What does it mean to “fund” a revocable living trust?

2) What happens if I create a trust but don’t fund it?

3) Which assets usually should be moved into the trust?

4) How do I transfer real estate into my trust?

5) Where do I record a quit claim deed after it’s notarized?

6) Do I need the parcel number and legal description for a deed transfer?

7) Should retirement accounts be retitled into the trust?

8) How do I move bank or brokerage accounts into the trust?

9) Can an LLC membership interest be transferred into a revocable trust?

10) Why is listing personal property so important?

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}