Last updated on December 17th, 2025 at 02:23 pm

Will You Be Financially Secure in 20 Years?

Will your retirement savings be enough?

Will your income support the lifestyle you actually want—not just getting by, but living well?

As a member of Generation X, you have about 20 years or less to shape the retirement you’ll live with for decades. The good news: You still have time. The better news: you don’t have to guess.

This article, combined with our Gen X budget planning tool, other calculators, and related guides on RetireCoast, is designed to help you move from uncertainty to a real, flexible plan.

The budget planning tool is available at the end of this article. Scroll down and click the large button to access it once you’ve read through how to use it most effectively.

For a broader roadmap to everything we cover here, be sure to read:

- Gen X Retirement Guide: https://retirecoast.com/gen-x-retirement-guide/

- Gen X – Only 20 Years to Retirement: Get Planning Now: https://retirecoast.com/gen-x-only-20-years-to-retirement-get-planning-now/

- Gen X FAQ: https://retirecoast.com/gen-x-faq/

- Gen X Fear of Running Out of Money: https://retirecoast.com/gen-x-fear-running-out-of-money/

Why Gen X Needs a Different Kind of Retirement Plan

Gen X faces a unique combination of pressures:

- Limited or no traditional pensions

- Student loan debt (their own or their children’s)

- Aging Baby Boomer parents who may need support

- Inflation and elevated cost of living

- Market volatility and uncertainty around Social Security

If you’re just starting, or restarting, your planning, the Gen X Retirement Guide is an excellent companion to this article:

https://retirecoast.com/gen-x-retirement-guide/

One of the most dangerous myths is that “expenses drop dramatically in retirement.” For many, they don’t. Some child-related costs disappear, but:

- Housing, taxes, insurance, and utilities remain

- Healthcare and prescription costs go up

- Travel, hobbies, and family support often replace work-related expenses

That’s why a realistic, numbers-based budget matters so much. The budget tool you’ll use here is not about perfection; it’s about clarity and honesty.

Want to compare retirement accounts that can help reduce taxes now or later? Use this guide to understand the most common tax-advantaged options and how they typically work.

Read the guide →Time to Take Financial Responsibility

If you’re around age 50 (or beyond), you likely have about 20 years to fix past mistakes and build momentum.

Maybe you’ve:

- Relied on credit cards a little too often

- Used home equity for lifestyle spending instead of assets

- Delayed saving because “retirement is far away”

If that sounds familiar, you’re not alone—and you are exactly who this article is written for.

A key companion article if you’ve been feeling anxiety about all this is:

https://retirecoast.com/gen-x-fear-running-out-of-money/

The goal isn’t to make you feel guilty. The goal is to give you a path forward.

A Personal Lesson Worth Sharing

There was a period in my life when I wasted money simply because I could. I bought new cars frequently, didn’t worry about depreciation, and paid little attention to how much cash quietly disappeared through taxes, registration fees, and losses on resale.

I wasn’t struggling financially — but I also wasn’t being intentional. As retirement planning became more real, it finally hit me: I wasn’t spending money, I was burning future income.

The change was simple but powerful. I kept vehicles longer, focused on maintenance instead of replacement, and redirected those dollars into savings and investments. The result wasn’t sacrifice — it was stability.

The biggest lesson? Retirement planning isn’t about deprivation. It’s about deciding what truly matters — and letting your money support that decision instead of quietly working against you.

Start With Where Your Money Really Goes

Before we talk about Social Security, investments, trusts, or business income, we have to start with something basic: Where is your money actually going?

The budget planning tool in this article helps you:

- List and organize your current expenses

- Estimate what will change in retirement—and what won’t

- Identify spending “leaks” that can be redirected into savings

- Compare different retirement locations or housing choices

For common questions about budgeting, timing, and Gen X planning, read:

https://retirecoast.com/gen-x-faq/

To ground your income estimates, always use official Social Security projections:

https://www.ssa.gov/retirement

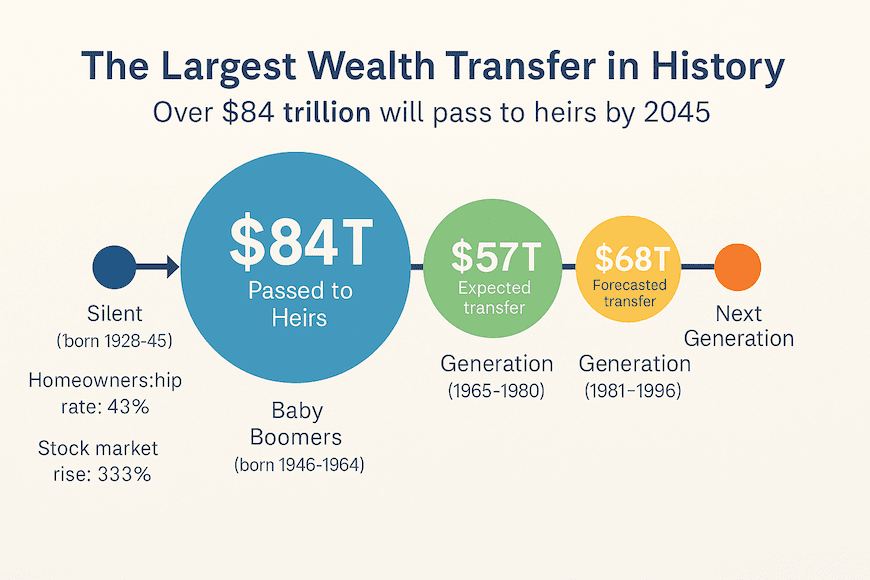

While You’re Planning, the Largest Wealth Transfer in History Is Underway

While you’re busy planning for retirement, something big is already happening:

The largest wealth transfer in history.

Trillions of dollars are expected to move from Baby Boomers to younger generations, and Gen X is positioned to be a major beneficiary. That might show up as:

- Inherited property

- Investment accounts

- Business interests

- Cash or other assets

The important question isn’t just if you’ll receive an inheritance—it’s whether your plan is ready to manage it wisely.

We explore this in depth in our legacy and wealth-transfer article, which also ties into the upcoming 250th anniversary of the United States:

- What 1776 Teaches Retirees About Legacy Planning:

https://retirecoast.com/what-1776-teaches-retirees-about-legacy-planning/

That article compares economic and social conditions in 1776 to those of today and shows how people have always had to think about legacy, value, and what they pass on to the next generation.

How the Largest Wealth Transfer Affects Gen X

Generation X is positioned to be a major beneficiary of the largest wealth transfer in history. Learn how it may impact your retirement, taxes, and legacy planning.

Read the Legacy Planning ArticleInflation, Cost of Living, and Your Future Buying Power

Inflation is not an abstract concept—it’s the slow erosion of your spending power over time. Even modest inflation can dramatically change what your savings will buy by the time you’re 70 or 75.

In our 1776 legacy planning article, we also dig into:

- Historical price changes

- How societies adapt to rising costs

- What retirees can learn from earlier generations

You don’t control inflation—but you must plan for it.

One critical step is to run your numbers through an inflation lens using our tools in the Calculators Hub, including the inflation calculator.

See How Inflation Affects Your Retirement Savings

Inflation quietly reduces purchasing power over time. Use the RetireCoast Inflation Calculator to understand its impact on your savings and retirement income.

Use the Inflation CalculatorBudgeting Alone Isn’t Enough: Legacy and Trust Planning

A solid retirement budget is essential—but it’s not the whole story.

If you’re part of Gen X, especially if you expect to receive or pass on assets, you should also be thinking about:

- How your assets will be managed if you become incapacitated

- How your estate will pass to heirs

- How to avoid unnecessary delay, conflict, and cost

One of the most flexible tools for this is the Revocable Living Trust. It can:

- Help keep your estate out of probate

- Provide continuity in case of incapacity

- Improve privacy

- Make it easier for heirs to manage and distribute assets

Our article on trusts explains the major trust types and when a revocable living trust might make sense in your planning:

- Trusts – Which Type Is the Best for You Now?

https://retirecoast.com/trusts-which-type-is-the-best-for-you-now/

Should a Revocable Living Trust Be Part of Your Plan?

Retirement planning isn’t only about income and expenses. Learn how a revocable living trust may fit into your retirement, legacy, and asset protection strategy.

Learn About Revocable Living TrustsRetireCoast Calculators: Going Beyond the Budget

The budget tool in this article is a powerful start, but RetireCoast has built a full lineup of calculators designed to help you test and refine your plan from multiple angles.

Some key tools to explore:

- Retirement Income From Savings Calculator

See how long your savings may last and how much monthly income they can realistically support.

https://retirecoast.com/retirement-income-from-savings-calculator/ - Inflation & financial calculators in the Calculators Hub

A central place to explore retirement, real estate, and personal finance calculators.

https://retirecoast.com/calculators-hub/ - Gen X–focused tools embedded in the Gen X Retirement Guide

One of our favorite calculators is embedded directly into this article:

https://retirecoast.com/gen-x-retirement-guide/

And remember: not everyone fully retires. Many Gen Xers decide to start a business or side venture in retirement to create more flexible income. For that, see:

- The Best Business I Can Start After Retirement:

https://retirecoast.com/the-best-business-i-can-start-after-retirement/

Explore Retirement & Financial Planning Calculators

The budget tool is just the start. Use RetireCoast calculators to estimate retirement income, test savings scenarios, and make informed decisions with real numbers—not guesses.

Visit the RetireCoast Calculators HubHow Much Monthly Income Can Your Savings Produce?

This calculator shows how long your savings may last and what level of income they could realistically support in retirement.

Try the Retirement Income CalculatorConsidering Income After Retirement?

Many Gen Xers plan to transition—not stop—working in retirement. Learn what types of businesses are realistic, flexible, and retirement-friendly.

Explore Retirement Business IdeasContinue With the Gen X Retirement Guide

One of our most useful retirement calculators is embedded directly into the Gen X Retirement Guide—with step-by-step explanation.

Read the Gen X Retirement GuideHow to Use the Gen X Budget Planning Tool

Here’s how to get the most out of the budget tool provided at the end of this article.

Step 1: Capture Today’s Reality

First, assume you’re retiring tomorrow. This doesn’t mean you will; it just gives you a baseline.

- Enter your current income (W-2 and other income).

- Enter your current expenses, but leave out child-related costs that will not be present in retirement.

- Include your existing 401(k), IRA, savings, and investments so you can see where you stand.

Save this version as your “today” snapshot.

Step 2: Project 20 Years Forward

Next, make a copy of the tool (File → Make a copy in Google Sheets) and:

- Adjust your income based on realistic expectations.

- Add your expected Social Security benefit using the SSA website:

https://www.ssa.gov/retirement - Update retirement account balances based on steady contributions and conservative growth.

- Change expenses to reflect what will be different at 70—paid-off cars, different housing, fewer child expenses, possibly higher medical costs.

You can also compare two different locations or housing choices using the tool’s side-by-side structure.

Case Study: Mark & Lisa – Planning Ahead From 50

To see what this looks like in practice, let’s look at one realistic Gen X couple.

Mark (50) and Lisa (48) aren’t behind, but they’re not “set” either. They have:

- $350,000–$450,000 in combined retirement savings

- A mortgage with about 15 years left

- Some auto debt and minor credit card balances

- Modest savings outside retirement accounts

- No formal trust or legacy plan

Instead of guessing, they start by using a budget planning tool—just like the one in this article—to get a clear picture of where their money is actually going and what their retirement might look like at 70.

[[INSERT: MARK & LISA SNAPSHOT HTML HERE]]

(Use the “Gen X Retirement Case Study — Mark & Lisa” snapshot box here.)

Over the next 20 years, they:

- Gradually increase 401(k) and IRA contributions

- Pay down and eliminate high-interest debt

- Consider downsizing and relocation options

- Use the budget tool annually to update their numbers

- Use the Retirement Income From Savings Calculator to test how long their savings may last:

https://retirecoast.com/retirement-income-from-savings-calculator/

By age 70, they’ve:

- Paid off their mortgage

- Accumulated about $1.4M–$1.8M in their retirement portfolio

- Delayed Social Security to maximize benefits ($42,000–$55,000/year combined)

- Created a revocable living trust and updated estate documents

Their total retirement income (portfolio withdrawals plus Social Security) is about $85,000–$110,000 per year, enough to fund a comfortable, flexible lifestyle and withstand periods of higher inflation.

They aren’t “lucky”—they are prepared.

Case Study: Kevin – Starting Late at 52 and Catching Up

Not everyone starts at 50 with several hundred thousand saved.

Kevin doesn’t get serious about retirement planning until age 52. At that point, he has:

- About $165,000–$225,000 in retirement savings

- A paid-off or nearly paid-off car

- Modest but creeping lifestyle expenses

- No real budget, no trust, and growing anxiety about being behind

Kevin could have panicked or given up. Instead, he chose structure and discipline.

He starts with the budget planning tool, listing every expense honestly. Then he models inflation and uses the Calculators Hub tools to stress-test different savings rates and timelines:

https://retirecoast.com/calculators-hub/

Gen X Late-Start Retirement Case Study — Kevin

52

70

$165,000 – $225,000

18% – 25% (with catch-up contributions)

Retained car 10+ years

Reduced discretionary spending 15%–20%

5% – 6% annually

$950k – $1.25M

$36,000 – $48,000 / year

$70,000 – $90,000 / year

“Kevin didn’t retire wealthy — he retired prepared. Late starters don’t need perfection. They need discipline and time.”

Over the next 15–18 years, Kevin:

- Forgoes frequent lifestyle upgrades (no new car just to “keep up”)

- Keeps his vehicle for 10+ years, investing $8,000–$12,000 per year into retirement instead of replacement

- Uses catch-up contributions and increases his savings rate to 18%–25% of his income

- Models 3%–4% inflation and conservative 5%–6% investment growth

- Becomes completely debt-free

By age 70, Kevin has:

- Built a portfolio of about $950,000–$1.25M

- Maximized his Social Security benefit (~$36,000–$48,000 per year)

- Covered his housing costs with only taxes and insurance

- Created a basic trust and legacy plan

His retirement income falls around $70,000–$90,000 per year, not flashy—but secure, even in the face of inflation and market volatility.

Two Different Starting Points, Both Successful Outcomes

To make it easy to compare, here’s a side-by-side view of Mark & Lisa and Kevin:

Gen X Retirement Case Study — Realistic Numbers

50

70 (Full Social Security)

$350,000 – $450,000

12% – 18% of income (ramped over time)

Paid off by age 65

3% – 4% long-term average

5% – 6.5% average annual return

$1.4M – $1.8M

$42,000 – $55,000 / year

$85,000 – $110,000 / year

$0 mortgage (taxes & insurance only)

Revocable Living Trust established

The important takeaway:

- Mark & Lisa benefit from starting earlier and more comfortably

- Kevin proves that even a late start can succeed with discipline and the right tools

Neither path requires perfection. Both require intentional, repeated planning.

Gen X Retirement Planning: Two Realistic Paths

| Planning Element | Mark & Lisa | Kevin |

|---|---|---|

| Starting Age | 50 | 52 |

| Initial Savings | $350k–$450k | $165k–$225k |

| Savings Strategy | Gradual increases | Aggressive catch-up |

| Lifestyle Adjustments | Debt reduction, downsizing options | No new car, reduced discretionary spend |

| Trust & Legacy Planning | Early implementation | Added mid-planning |

| Portfolio at Age 70 | $1.4M–$1.8M | $950k–$1.25M |

| Outcome | Comfortable, flexible | Secure, resilient |

A Personal Lesson, A Practical Tool, and Your Next Steps

We’ve covered a lot:

- Budgeting and honest expense tracking

- Inflation and cost-of-living realities

- The largest wealth transfer in history

- Social Security timing

- Legacy planning and trusts

- Real-world case studies at different starting points

- Tools and calculators to test your plan

Now it’s your turn.

- Use the budget tool below to capture your current numbers.

- Project forward 20 years, modeling inflation and income realistically.

- Run scenarios with the Retirement Income From Savings Calculator and inflation tools in the Calculators Hub.

- Read the Gen X series articles linked throughout this page to deepen your understanding.

- Consider legacy and trust planning so your hard work benefits the people and causes you care about.

Finally, scroll down to access your Free Gen X Retirement Budget Planning Tool and start turning concern into a concrete plan.

This is where real planning begins—for you, not just in theory, but in your actual numbers.

Gen X Retirement Planning FAQ

Is 50 or 52 too late to start retirement planning?

No. Many Gen Xers begin serious retirement planning in their early 50s. With disciplined budgeting, catch-up contributions, and realistic assumptions, starting at 50 or even 52 can still lead to a financially secure retirement.

How much money does Gen X need to retire?

There is no single number. Most Gen X retirement plans combine Social Security, retirement savings, and possibly additional income. A realistic budget, inflation modeling, and conservative withdrawal planning matter more than hitting a specific portfolio size.

Do expenses really go down in retirement?

Some costs disappear, but many remain. Housing, insurance, healthcare, and transportation often continue, while travel and lifestyle spending can increase. That’s why Gen X retirement planning must be based on realistic budgets.

Why is inflation such a big risk for Gen X retirees?

Inflation reduces purchasing power over time. Even modest inflation can significantly affect long-term retirement income, which is why Gen X retirement plans should always include inflation assumptions and scenario testing.

Should Gen X consider creating a trust?

Many Gen X households benefit from a revocable living trust, especially when real estate or inherited assets are involved. Trusts can help avoid probate, provide continuity, and simplify legacy planning, but they should be evaluated in the context of your full financial plan.

Is Social Security enough for retirement?

For most Gen Xers, Social Security is a foundation—not a complete solution. Delaying benefits can increase lifetime income, but retirement security typically requires additional savings and careful planning.

Open Your Free Gen X Retirement Budget Planning Tool

Use this interactive Google Sheets budget planner to map out your expenses, income, and retirement scenarios over the next 20 years. After opening the sheet, click File → Make a copy to save your own private version.

📊 Open the Gen X Budget Planning ToolDiscover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}