Gen Z and Millennials are currently the most positive generations when it comes to opportunity, with 48% rating today’s business conditions as “good.” Even more telling, 74% of all small business owners are planning growth in 2025–2026—a clear signal that momentum is building, not slowing. A great time for Millennials starting a business.

Millennials and Gen Z are also catching up fast in ownership mindset. Nearly 49% of Millennials—and a similar share of Gen Z—say they would start a business if the right resources were available, a much higher percentage than older generations. That gap isn’t about ambition; it’s about access, clarity, and knowing where to begin.

If you’re thinking about starting a business, you’re in the right place. This guide is designed to walk you through the process step by step—without hype, pressure, or unrealistic promises. You’ll learn how to think through your goals, validate ideas, manage money, and understand what it actually takes to move forward. And if you decide this is the right time for you, this article will help you do it thoughtfully and on your terms.

Starting a business doesn’t have to mean jumping blindly or taking unnecessary risks. It starts with understanding the landscape, aligning the business with your life, and building from a position of clarity. That’s exactly what this guide is here to help you do.

- Types of Businesses Millennials Are Interested in Starting

- Most Successful Types of Businesses Started by Millennials

- Why Businesses Fail — and What Millennials Can Learn From It

- How Millennials Can Reduce Risk Before They Ever Launch

- Creating a Business Plan That Actually Reduces Risk

- Who Is the Audience for Your Business Plan?

- A Living Document — Not a Fixed One

- Why This Perspective Matters

- What a Business Plan Is (and What It Isn’t)

- Start With the Outcome, Not the Idea

- Define the Problem and the Customer Clearly

- Outline the Offer in Simple Terms

- Address Cash Flow Early — Not After Launch

- Map the Path to the First Milestones

- Plan for Management Before You Feel Overwhelmed

- Build the Exit Into the Plan From Day One

- Why This Section Matters

- Turning the Plan Into Action: How Millennials Starting a Business Should Move Forward

- A Business That Fits the Moment: Starting a Landscaping Business

- Thinking Ahead: Selling the Business as Part of the Plan

- Case Study: James — Building a Landscaping Business the Right Way

- Case Study: Mark — Buying Green Thumb Landscapers From a Retiring Owner

- QUIZ

- FAQ

Types of Businesses Millennials Are Interested in Starting

Millennials (born 1981–1996) show strong entrepreneurial interest, with surveys indicating 66% of older millennials aspire to start a business, often prioritizing flexibility, passion, financial independence, and digital tools.

While current millennial-owned small businesses are still growing (around 16–26% of total owners in 2024–2025 data), their preferences lean toward tech-enabled, online, and service-based ventures rather than purely traditional brick-and-mortar operations.

They frequently start side hustles or digital businesses, but many are also acquiring established “Main Street” businesses from retiring Baby Boomers (e.g., retail shops, services). Motivations include work-life balance, using AI/social media for operations, and aligning with values like sustainability.

Top Business Types and Industries

Based on 2024–2025 reports, surveys, and trends:

| Rank | Business Type/Industry | Why Millennials Are Interested | Examples/Notes |

|---|---|---|---|

| 1 | E-commerce & Online Retail | Low overhead, scalability via platforms like Shopify, aligns with digital natives. High interest in niche markets (e.g., sustainable products). | Dropshipping, subscription boxes, Etsy-style handmade goods. Gen Z/Millennials plan heavy e-commerce expansion (88% of younger owners). |

| 2 | Digital Services & Tech Startups | Tech-savvy; preference for remote/flexible work. Heavy AI adoption (74% see it as critical). | Mobile app development, web design, digital marketing agencies, SaaS tools. |

| 3 | Health, Wellness & Fitness | Focus on personal fulfillment, mental health, and preventative care. Values-driven. | Gyms, yoga studios, wellness apps, personalized coaching, med spas. |

| 4 | Food & Beverage (Niche/Experiential) | Passion for experiences; sustainable/healthy options. Side hustles like food trucks common. | Gourmet food trucks, specialty cafes, plant-based or health-focused eateries. |

| 5 | Professional & Business Services | Stable revenue; often acquired from Boomers. Includes consulting for flexibility. | Accounting, law firms, marketing/consulting, outsourcing support. |

| 6 | Sustainable & Eco-Friendly Ventures | Strong emphasis on social responsibility and planet health. | Green products, circular economy, renewable energy-related small ops. |

| 7 | Content Creation & Social Media-Based | Low startup costs; leverages platforms like TikTok/Instagram for marketing and sales. | Influencer brands, online courses, freelance content agencies. |

| 8 | Acquired Traditional Businesses | Opportunity from Boomer retirements; proven models with modern twists (e.g., digitizing). | Retail stores, franchises, local services (e.g., landscaping, auto repair). |

These preferences reflect a blend of innovation and pragmatism: Millennials favor starting digital/low-cost ventures but are increasingly buying established ones for steady cash flow amid economic uncertainty. Younger millennials overlap with Gen Z trends (e.g., community-focused, AI-integrated), while older ones lean toward acquisitions.

Data sources include Guidant Financial’s 2025 Small Business Trends (showing millennial growth via acquisitions), American Express surveys (tech/social media driving starts), and broader reports emphasizing e-commerce, wellness, and sustainability. Actual starts may vary by region/economy, but digital agility remains a core theme.

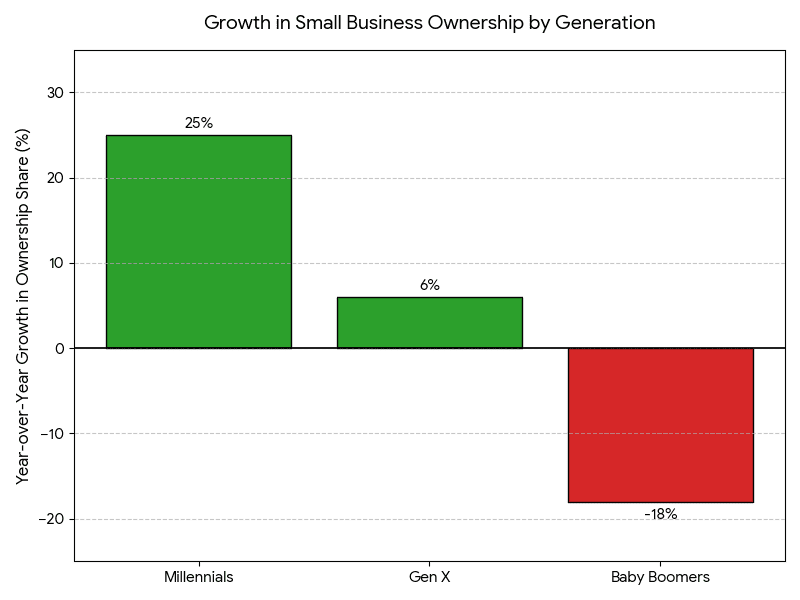

The data illustrates a major demographic shift currently happening in entrepreneurship (often referred to as the “Silver Tsunami”):

Millennials: Experiencing a massive 25% surge in business ownership.

Millennials are currently the fastest-growing demographic of entrepreneurs, driven by a desire for flexibility, purpose-driven work, and independence from traditional corporate structures. Gen X currently makes up the largest total share of small business owners (roughly 49%) and they are continuing to acquire and start new businesses at a healthy rate. Baby Boomers: This drop is largely due to retirement, as older entrepreneurs exit the market by selling their established businesses or passing them down to younger generations. (Note: Generation Z is still emerging in the formal small business space and is heavily focused on freelance or micro-businesses, so year-over-year formal business acquisition/starting data is still stabilizing for that group).

Most Successful Types of Businesses Started by Millennials

Millennials have launched highly successful businesses, particularly in tech-driven and digital sectors, where their digital-native skills enable rapid scaling, innovation, and disruption of traditional industries. Many iconic unicorns (private companies valued at $1B+) were founded by millennials, achieving massive valuations, revenue growth, and global impact as of 2025-2026 data.

Success here measures by:

- Valuation (for startups)

- Revenue growth

- Market disruption

- Profitability in small businesses

While older millennial-founded companies (e.g., from the 2010s) dominate unicorn lists, recent trends show continued strength in AI/tech, alongside profitable small businesses in e-commerce, wellness, and services.

Top Categories of Successful Millennial-Founded Businesses

| Rank | Business Type/Industry | Key Success Metrics & Examples | Why It’s Thriving for Millennials |

|---|---|---|---|

| 1 | Tech Platforms & Social Media | Highest valuations; e.g., Facebook (Meta, founded by Mark Zuckerberg), Airbnb (Brian Chesky), Snapchat (Evan Spiegel), Pinterest (Ben Silbermann). Many exceed $100B valuations. | Digital savvy; network effects drive explosive growth. |

| 2 | E-commerce & Direct-to-Consumer (DTC) | Rapid revenue scaling; e.g., Kylie Cosmetics (Kylie Jenner, billionaire status via social sales), fashion/luxury brands hitting 7-figures quickly. Dropshipping/POD models common for small successes. | Low overhead; leverages Instagram/TikTok for marketing. |

| 3 | Fintech & Payments | High valuations; e.g., Stripe (Collison brothers), Revolut. Global market growth to $324B by 2026. | Solves pain points in banking; appeals to tech-focused millennials. |

| 4 | Health, Wellness & Fitness | Profitable small businesses; gyms, coaching, apps. Industry ~$11.9B in personal training alone (2025). Plant-based/mental health ventures scaling fast. | Values-driven; aligns with personal fulfillment and sustainability. |

| 5 | AI & Software Startups | New unicorns surging; many 2025 entries AI-focused (e.g., Anthropic, Perplexity). Fastest valuation growth. | Tech expertise; AI boom enables quick innovation. |

| 6 | Content Creation & Influencer Brands | 7-figure empires from side hustles; e.g., cookbooks, meal services turning into restaurants. | Low startup costs; social media monetization. |

| 7 | Sustainable & Eco-Friendly | Growing markets; e.g., eco-packaging ($240B+ in 2025), green products. | Emphasis on social responsibility. |

| 8 | Food & Beverage (Niche) | DTC brands like Olipop (high revenue/employee); experiential cafes/food trucks. | Passion for healthy/experiential options. |

These categories reflect a mix of high-valuation unicorns (tech-heavy) and profitable small/medium businesses (service/digital). Many millennials blend both—starting small digitally then scaling or acquiring established firms.

Notable trends in 2025-2026:

- AI dominance in new high-growth ventures.

- Acquisitions of Boomer-owned businesses for steady cash flow.

- Focus on flexibility, remote operations, and purpose.

Data draws from unicorn lists (CB Insights, PitchBook), industry reports (Guidant, Shopify, IBISWorld), and entrepreneur profiles. Success varies by execution, but these types consistently show strong performance for millennial founders.

Why Businesses Fail — and What Millennials Can Learn From It

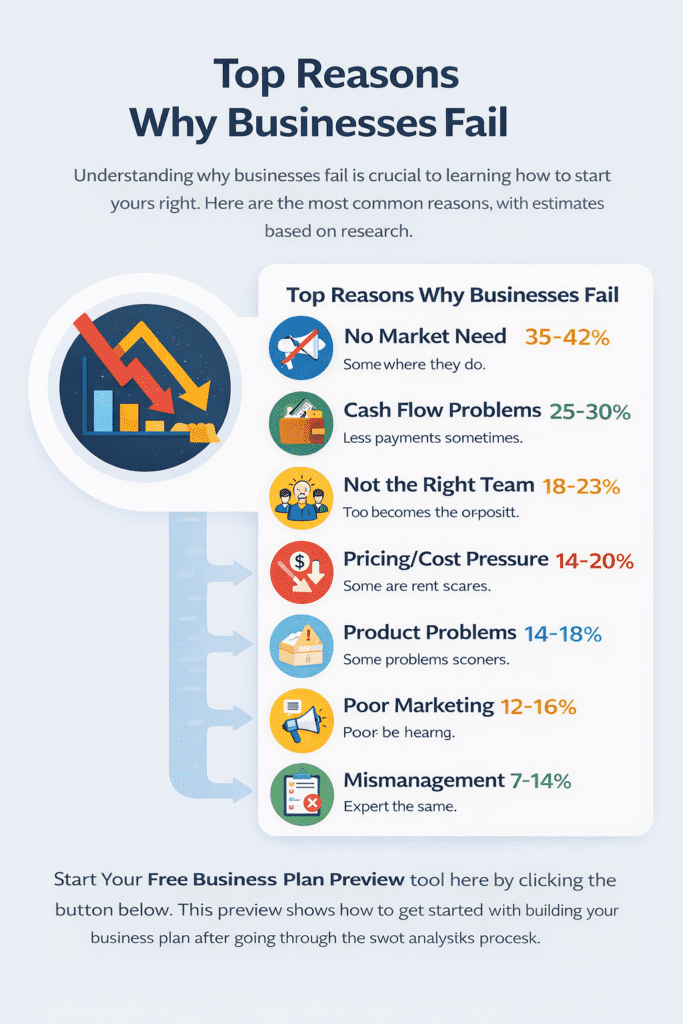

Before moving into planning and execution, it’s important to understand why businesses fail in the first place. Not to discourage you—but to remove the mystery. Most failures don’t happen because the founder wasn’t smart, motivated, or hardworking. They happen because a few predictable issues weren’t addressed early.

Across industries and generations, research from organizations like CB Insights and the SBA shows the same patterns again and again.

Cash Flow Problems (82% of Failures)

Cash flow is the number one reason businesses fail—by a wide margin.

This doesn’t mean the idea was bad or that revenue never existed. It usually means:

- Expenses grew faster than income

- Revenue was inconsistent or seasonal

- Personal and business finances were mixed

- There wasn’t enough margin for mistakes

For Millennials, this is especially relevant because many businesses start as side hustles. Without clear cash-flow tracking, it’s easy to underestimate how much stability the business actually needs.

Key insight:

Profit on paper doesn’t matter if cash isn’t available when bills are due.

No Market Need (35–42%)

The second most common cause of failure has nothing to do with effort—it’s demand.

This happens when:

- A product solves a problem people don’t feel urgently

- The solution is “nice to have,” not necessary

- The idea is built before talking to real customers

Millennials often bring creativity and innovation, but this risk appears when passion replaces validation. The market—not the founder—decides what survives.

Key insight:

Interest and compliments are not the same as willingness to pay.

Competition or Being Outpriced (19–23%)

Some businesses fail because:

- Larger competitors can undercut pricing

- The value proposition isn’t clear

- Customers don’t understand why this option is different

This is especially common in crowded digital spaces where entry costs are low. Without clear positioning, businesses become interchangeable—and price becomes the only lever.

Key insight:

You don’t need to be cheaper. You need to be clearer.

Poor Team or Management (About 23%)

This doesn’t always mean hiring the wrong people. It often means:

- Trying to do everything alone for too long

- Lacking systems and decision frameworks

- Avoiding uncomfortable financial or operational decisions

Millennials often value independence, but isolation can quietly undermine progress. Strong businesses are built on structure, even when teams are small.

Key insight:

Good management is about decisions and systems—not titles.

The Bigger Picture: Failure Is Predictable — and Preventable

What’s important to notice is this:

None of these causes are mysterious. They are known, measurable, and manageable.

This is good news.

It means that starting a business isn’t about luck or timing—it’s about understanding these risks early and building around them. That’s exactly what the next sections will focus on: planning, cash flow awareness, validation, and decision-making frameworks that reduce risk instead of amplifying it.

Most failed businesses didn’t lack ambition. They lacked structure. And structure is something you can build.re than birth year.

What This Tells Us About Millennial Entrepreneurship

Taken together, this research highlights something important: Millennials are not avoiding work or responsibility—they’re redefining how work fits into life. The strong interest in digital services, e-commerce, wellness, and professional services reflects a desire for control, flexibility, and sustainability, not shortcuts.

Just as notable is the growing trend of Millennials buying existing businesses rather than starting from scratch. Acquiring a proven local business from a retiring owner offers predictable cash flow and reduces early risk—especially appealing in uncertain economic cycles. This is a pragmatic shift, not a retreat from innovation.

Another clear theme is tool leverage. Millennials are comfortable using AI, automation, social media, and online platforms to operate leaner businesses with fewer employees and lower overhead. That efficiency changes what “small business” looks like compared to previous generations.

Finally, values matter. Many Millennials want their businesses to reflect personal priorities—whether that’s mental health, sustainability, community impact, or time with family. For this generation, success is not just revenue; it’s alignment.

Why This Matters for the Rest of This Guide

Understanding what Millennials want to build—and why—sets the foundation for everything that follows. The next sections will focus on how to turn these interests into clear goals, realistic plans, and achievable steps, whether you’re starting something new, growing a side hustle, or considering buying an existing business.

You don’t need to follow trends blindly. You need to choose a path that fits your skills, resources, and life—and then build it intentionally. That’s where we go next.

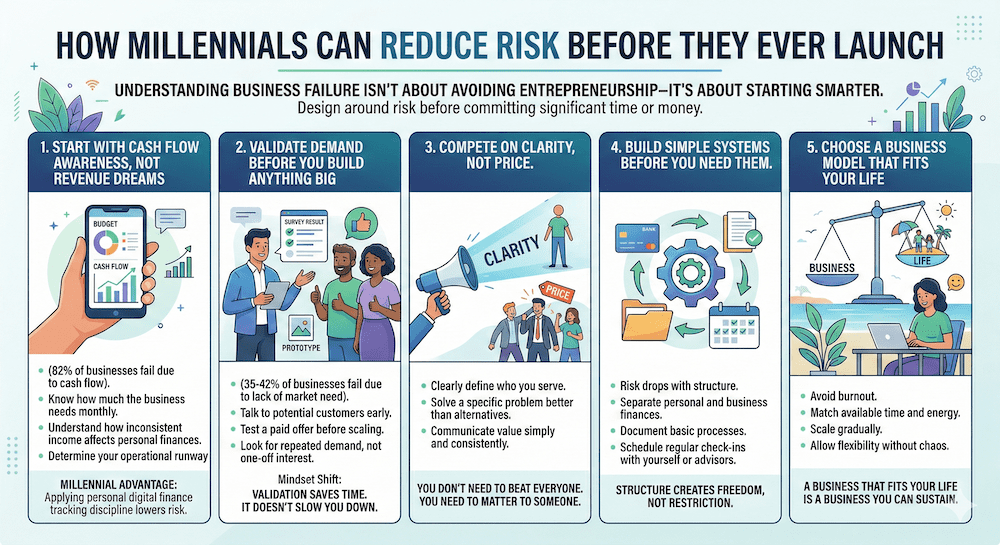

How Millennials Can Reduce Risk Before They Ever Launch

Understanding why businesses fail isn’t about avoiding entrepreneurship—it’s about starting smarter. The most successful Millennial founders don’t eliminate risk; they design around it. The good news is that every major cause of failure we just covered can be addressed before you commit significant time or money.

This section focuses on risk reduction, not perfection.

1. Start With Cash Flow Awareness, Not Revenue Dreams

Since cash flow issues account for 82% of failures, this is where smart planning begins.

Before launching, it helps to know:

- How much the business needs to survive monthly

- How inconsistent income would affect personal finances

- How long you can operate before pressure sets in

This doesn’t require complex spreadsheets. It requires honesty.

Millennial advantage:

Many Millennials already track personal finances digitally. Applying that same discipline to a business—even a side hustle—dramatically lowers risk.

2. Validate Demand Before You Build Anything Big

Because 35–42% of businesses fail due to lack of market need, validation is non-negotiable.

Practical validation looks like:

- Talking to potential customers early

- Testing a paid offer before scaling

- Looking for repeated demand, not one-off interest

If people are willing to pay—even at a small scale—that’s signal. If not, it’s feedback, not failure.

Key mindset shift:

Validation saves time. It doesn’t slow you down.

3. Compete on Clarity, Not Price

With competition and pricing pressure driving many failures, differentiation matters more than ever.

Early-stage businesses reduce risk by:

- Clearly defining who they serve

- Solving a specific problem better than alternatives

- Communicating value simply and consistently

You don’t need to beat everyone. You need to matter to someone.

4. Build Simple Systems Before You Need Them

Poor management rarely looks dramatic at first—it looks like overwhelm.

Risk drops significantly when you:

- Separate personal and business finances

- Document basic processes

- Schedule regular check-ins with yourself or advisors

Millennials often resist structure early, but structure creates freedom, not restriction.

5. Choose a Business Model That Fits Your Life

One reason Millennials burn out is choosing businesses that conflict with real life.

Lower-risk businesses often:

- Match available time and energy

- Scale gradually

- Allow flexibility without chaos

A business that fits your life is easier to sustain—and far more likely to succeed.

Why This Matters Before Writing a Business Plan

Risk reduction isn’t a separate step—it’s the foundation. When you understand cash flow, demand, competition, and capacity, your business plan becomes practical instead of theoretical.

That’s where we go next.

The next section focuses on creating a business plan that reflects your goals and how you’ll actually achieve them—not a document that sits in a folder, but a plan you can use.

Creating a Business Plan That Actually Reduces Risk

After understanding why businesses fail, the next step isn’t motivation — it’s structure.

A business plan, when done correctly, is not a formality or a school assignment. It’s a risk-reduction tool. Every major cause of failure we just discussed — cash flow problems, lack of demand, pricing pressure, and poor management — can be addressed directly through a well-designed plan.

For Millennials, this means building a plan that reflects real goals, real constraints, and real life — not a 40-page document that never gets opened again.

Who Is the Audience for Your Business Plan?

Your business plan isn’t written for just one person — and that’s by design.

First and foremost, you are part of the audience. The plan serves as a guide to keep you focused, grounded, and aligned with the goals you set at the beginning. When things get busy or unclear, it becomes a reference point for decisions.

If you intend to borrow money, your lender may also want to review your plan. They aren’t looking for perfection — they’re looking for signs that risk is understood and mitigated. A clear, realistic plan demonstrates that you’ve thought through cash flow, demand, and repayment.

Potential partners are another important audience. Whether it’s a silent partner, an operational partner, or someone providing capital, they’ll want to understand how the business works, what role they play, and how decisions are made.

In some cases, early creditors may also ask to see a basic plan — especially if you’re requesting trade credit, equipment financing, or extended payment terms.

Another often-overlooked audience is a mentor or advisor. A plan gives experienced people something concrete to react to, critique, and improve. Feedback is far more useful when there’s something written down.

A Living Document — Not a Fixed One

It’s important to remember that a business plan is not set in concrete. It’s a living document. You can — and should — make changes as circumstances evolve.

Having started many businesses over the years, one thing becomes clear very quickly: things change. Markets shift, costs change, opportunities appear, and assumptions get tested. Your ability to adapt isn’t a weakness — it’s a strength.

A good business plan doesn’t lock you into a path. It gives you a framework to adjust intelligently as you learn more.

Why This Perspective Matters

Seeing your business plan as a shared, flexible tool — rather than a static requirement — makes it far more useful. It becomes something you return to, refine, and rely on as the business grows.

That mindset alone helps reduce risk and increases the odds that your business stays aligned with both your goals and reality.

What a Business Plan Is (and What It Isn’t)

A practical business plan is:

- A roadmap for decisions

- A way to test assumptions before money is spent

- A reference point when things feel unclear

It is not:

- A guarantee of success

- A prediction of the future

- Something you finish once and forget

Think of it as a working document, not a finished product.

Start With the Outcome, Not the Idea

Many businesses fail because they start with what they want to do instead of why they’re doing it.

Before outlining services, pricing, or marketing, it helps to define:

- Income goals (monthly and annual)

- Time commitment (hours per week)

- Lifestyle boundaries (nights, weekends, flexibility)

- Risk tolerance (slow and steady vs aggressive growth)

A business that fits your life is easier to sustain than one that only looks good on paper.

Define the Problem and the Customer Clearly

One of the most common failure points is building something without real demand.

A strong business plan answers:

- Who exactly is the customer?

- What problem are they already trying to solve?

- Why do they care enough to pay?

This is especially important for service businesses like landscaping, where demand exists — but competition is real. Clarity here directly reduces the risk of being outpriced or overlooked.

Outline the Offer in Simple Terms

You don’t need a complex product lineup to start.

At a minimum, the plan should clearly state:

- What is being offered

- How it’s priced

- How customers buy

- How the service is delivered

Simple, focused offers are easier to sell, easier to manage, and easier to improve.

Address Cash Flow Early — Not After Launch

Since cash flow issues account for the majority of business failures, this section matters more than revenue projections.

A useful business plan includes:

- Startup costs

- Ongoing monthly expenses

- Expected payment timing

- Break-even estimates

For Millennials starting small or acquiring an existing business, this clarity prevents avoidable stress and rushed decisions.

Map the Path to the First Milestones

Instead of long-range forecasts, focus on near-term checkpoints:

- First paying customers

- First repeat customers

- First month of consistent cash flow

- First decision point (continue, adjust, or pause)

Progress measured in milestones is far more motivating — and realistic — than five-year projections.

Plan for Management Before You Feel Overwhelmed

Poor management rarely looks dramatic at first. It looks like:

- Disorganized finances

- Missed follow-ups

- Burnout

A basic plan should include:

- How money is tracked

- How work is scheduled

- How decisions are reviewed

This doesn’t require a team — just intention.

Build the Exit Into the Plan From Day One

Even early on, it’s worth asking:

- Could this business be sold someday?

- What would make it easier to transfer?

This is especially relevant for businesses like landscaping, which are often sold to new owners or passed along when someone retires.

Thinking about exit early doesn’t mean you’re planning to leave — it means you’re building something with options.

Why This Section Matters

A business plan doesn’t eliminate risk — but it makes risk visible. It forces decisions out of your head and onto paper, where they can be evaluated, adjusted, and improved.

For Millennials, the goal isn’t to build the “perfect” business. It’s to build a resilient one — one that can adapt, grow, or even be sold when the time is right.

In the next section, we’ll walk through how to turn this plan into actionable steps, including validation, budgeting, and using tools to support — not complicate — the process.

Turning the Plan Into Action: How Millennials Starting a Business Should Move Forward

A business plan only creates value when it leads to action. For millennials starting a business, the goal isn’t to plan longer — it’s to move forward deliberately, using the plan as a guide rather than a constraint.

This is where many people stall. They finish a plan, feel productive, and then hesitate. The better approach is to use the plan to identify the next small, low-risk steps that test assumptions and build momentum.

Focus on Execution, Not Perfection

One common mistake among millennials starting a business is waiting for everything to feel “ready.” In reality, clarity often comes after action, not before it.

At this stage, execution should focus on:

- Testing the core offer

- Interacting with real customers

- Generating the first dollars of revenue

- Learning what actually works in your market

Your plan gives direction, but experience refines it.

Validate Before You Expand

The fastest way to reduce risk is to validate assumptions early. That means confirming:

- People will pay

- Pricing makes sense

- Delivery is manageable

- Demand is repeatable

This applies whether you’re starting from scratch or buying an existing business, such as a landscaping operation. Early validation turns theory into evidence and helps prevent wasted time and money.

Use Tools to Support — Not Complicate — the Process

Millennials starting a business often have access to more tools than any generation before them. The key is using them selectively.

Good tools:

- Improve visibility into cash flow

- Save time on administrative work

- Help prioritize decisions

- Reduce mental load

Too many tools, however, create noise. The best systems are the ones you actually use consistently.

Review, Adjust, and Keep Moving

Execution isn’t linear. Some steps will work better than expected; others won’t. That’s normal.

A strong habit to build early is regular review:

- Revisit the plan monthly or quarterly

- Compare expectations to reality

- Adjust pricing, services, or pace as needed

This feedback loop is what separates businesses that adapt from those that stall.

Momentum Comes From Small Wins

For millennials starting a business, progress doesn’t come from big launches — it comes from:

- First customer

- First repeat customer

- First profitable month

- First decision made with confidence

Each step reinforces the next.

Why This Matters Long Term

Taking action with intention sets the tone for everything that follows. Businesses that start with clarity, validation, and flexibility are easier to grow — and easier to sell later if that becomes part of the plan.

In the next section, we’ll look at how to use metrics and simple tracking to make smarter decisions without turning the business into a full-time administrative job.

A Business That Fits the Moment: Starting a Landscaping Business

Not every business idea needs venture capital, complex technology, or years of development. Some of the strongest opportunities for Millennials are practical, local, and immediately cash-flow positive. Landscaping is a great example — and the data backs it up.

Search behavior shows strong interest not only in starting a landscaping business, but also in selling one. That combination matters. It signals demand at both ends of the lifecycle: entry and exit.

Why Landscaping Is Well Suited for Millennials

Landscaping checks many of the boxes Millennials care about when starting a business:

- Low entry costs compared to many other businesses

- Immediate demand in most markets

- Flexible growth (side hustle → full-time business)

- Local, repeat customers

- Simple operations early on

- Clear path to hiring or subcontracting later

For many Millennials, landscaping starts as a weekend or after-work service and evolves into a structured business with predictable cash flow.

Entry Costs Are Manageable and Scalable

Unlike many businesses that require upfront inventory, leases, or technology builds, landscaping can often start with:

- Basic equipment (mower, trimmer, blower)

- Transportation (personal truck or trailer)

- Insurance and basic licensing

- Simple scheduling and invoicing tools

This makes it accessible to younger entrepreneurs who may not want to take on debt or risk personal savings early.

Important:

Low entry cost does not mean low professionalism. The most successful operators treat it like a business from day one.

Demand Is Stable — and Often Recession-Resistant

Landscaping demand is driven by:

- Homeownership

- Rental properties

- HOAs and small commercial properties

- Aging homeowners who no longer do yard work themselves

In many areas, demand is recurring, not one-time. Weekly, bi-weekly, or monthly service contracts create predictable revenue — something many digital businesses struggle to achieve early.

Easy to Start Small — Without Staying Small

Landscaping businesses scale naturally:

- Add services (mulching, cleanup, irrigation, seasonal work)

- Add routes instead of chasing one-off jobs

- Hire part-time help before full crews

- Move from residential to light commercial

Millennials who value flexibility can grow at their own pace without being locked into a single growth model.

Technology Is a Competitive Advantage for Millennials

This is where Millennials often outperform older operators.

Using:

- Online scheduling

- Text/email communication

- Digital invoicing and payments

- Route optimization tools

- Social media for local visibility

…can dramatically improve efficiency and customer retention without increasing overhead. Want a third party reference, check this out: National Association of Landscape Professionals (NALP)

The NALP is a national trade association that represents nearly 100,000 landscape industry professionals. Their members include companies specializing in lawn care, landscape design and installation, tree care, irrigation, and interior plantscaping.

Thinking Ahead: Selling the Business as Part of the Plan

One reason landscaping ranks highly in search interest is that it’s a business people can sell.

That matters.

Many small businesses are started without an exit in mind. Landscaping is different because it often has:

- Transferable customer lists

- Predictable cash flow

- Simple operations

- Tangible assets (equipment, routes)

That makes it attractive to:

- Other operators expanding

- First-time buyers

- Retirees looking for income businesses

Landscaping as an Exit-Friendly Business

Even if you’re just starting, thinking ahead matters.

A landscaping business becomes easier to sell when:

- Customers are on contracts

- Financials are clean and documented

- Owner involvement is reduced

- Systems are repeatable

These are the same principles discussed in the Starting a Business After Retirement hub — just applied earlier in life.

Why This Matters for Millennials

For Millennials, this creates optionality:

- Build income now

- Grow at a sustainable pace

- Decide later whether to:

- Keep it as lifestyle income

- Hire a manager

- Sell it outright

Starting a business doesn’t mean committing forever. The strongest businesses are built with choices in mind.

Connecting the Dots: Start Smart, Exit Smart

Landscaping is just one example, but it illustrates a broader point:

Businesses that are simple, cash-flow focused, and transferable tend to serve entrepreneurs well at every stage of life.

Whether you’re starting your first business or thinking long-term about ownership and exit, the principles are the same. That’s why we also discuss exit strategies — including selling a business — in our Starting a Business After Retirement hub.

The goal isn’t just to start something.

It’s to build something that gives you options.

Case Study: James — Building a Landscaping Business the Right Way

James had thought about starting his own landscaping business for years.

As a teenager, he worked part-time during the summers for a local landscaper. He learned the basics of the business—mowing, trimming, seasonal cleanup, and, just as importantly, how customer relationships worked. Even after he moved on, he stayed in touch with his former boss and would occasionally fill in on a Saturday when extra help was needed.

He didn’t do this because he needed the money. James had a solid full-time job as a machine operator. What kept pulling him back was simple: he enjoyed working outside and liked building things that grew.

The Turning Point

One day, James read an article about starting a business that caught his attention. What stood out most wasn’t the success stories—it was the section explaining why businesses fail.

That’s when he made a decision. Rather than jumping in blindly, James decided to start a part-time landscaping business while keeping his full-time swing-shift job. This allowed him to reduce risk while testing demand and building experience.

Starting Small and Smart

James began with what he already had:

- His own lawnmower

- Basic hand tools

- No debt

His first customers were neighbors. Then friends from work. Word spread quickly.

Before long, weekends were booked. Then evenings. Demand was real, and cash flow was steady.

Planning for Growth — Before It Was Needed

One thing James did early—and did well—was create a business plan. It wasn’t academic or complicated. It focused on:

- Expansion timing

- Additional equipment needs

- When to bring on help

- Revenue and profit targets

- A clear exit from his full-time job

He set a date for when he would leave his job and go all-in—but only if his business hit specific revenue and profit milestones.

Because he had savings, he was able to purchase additional equipment without taking on loans, keeping overhead low and stress manageable.

Scaling With Intention

Within three months, James hired a part-time helper. He did this intentionally, making sure the fit was right before committing further.

By the end of his first year:

- He had two full-time employees

- A large van to transport tools and equipment

- A growing list of recurring customers

Each month, James revisited his plan and budget, checking off milestones and making small adjustments as needed.

Planning for Seasonality

James understood that landscaping is seasonal. Slower winter months were part of the plan—not a surprise.

To fill the gaps, he expanded services to include:

- Larger landscaping projects

- Laying concrete

- Building flower beds and fountains

- Adding architectural elements

- Pressure washing homes, driveways, and commercial buildings

This allowed him to keep revenue flowing even when routine lawn work slowed.

Why James Succeeded

James’ business worked because he addressed the most common failure points early:

- Market demand: He validated demand before scaling

- Cash flow: Protected by planning and a full-time job at the start

- Hiring: Started part-time and expanded carefully

- Pricing: Positioned in the middle of the market, leaving room to adjust

- Product risk: Minimal, because he sold services—not inventory

- Marketing: Strong word-of-mouth supported by a professional website

- Cost control: Avoided unnecessary purchases

- Reserves: Set aside money monthly for equipment repair and replacement

Thinking Beyond the Beginning

Today, James continues to grow his business deliberately. He has already developed an exit strategy, with the expectation that the business will eventually become an attractive opportunity for a buyer to step in and take over.

His story isn’t about luck. It’s about preparation, patience, and understanding risk before it becomes a problem.

James didn’t just start a landscaping business—he built one with intention.

- He validated demand before leaving his full-time job

- He started part-time to reduce financial risk

- He planned growth before it was necessary

- He controlled cash flow and avoided unnecessary debt

- He hired gradually, starting with part-time help

- He priced services realistically, leaving room to adjust

- He chose a business name—Gulf Coast Exceptional Landscaping—that supported a future sale

- He revisited his plan and budget monthly

- He built seasonality into the business model

- He thought about his exit strategy early, even while growing

Case Study: Mark — Buying Green Thumb Landscapers From a Retiring Owner

Mark had always been interested in owning a business, but he approached the idea differently than many first-time entrepreneurs. He wasn’t looking for a concept to test or a market to validate. What he wanted was predictability—a business with existing customers, proven cash flow, and a history he could evaluate.

That opportunity came when he learned that a long-established local landscaping company, Green Thumb Landscapers, was for sale.

Why the Business Was Attractive

Green Thumb Landscapers had been operating successfully for more than twenty years. The owner, a Baby Boomer, was ready to slow down and retire but didn’t want to simply shut the business down. He wanted to transition it to someone who would take care of his customers and continue what he had built.

The business had several qualities that made it appealing:

- Consistent residential and small commercial clients

- Recurring service routes

- Predictable monthly cash flow

- Straightforward operations

- Well-maintained equipment

Just as important, the business name did not include the owner’s personal name. That made it far easier for Mark to envision stepping into ownership without disrupting customer relationships.

A Name That Made Transition Easier

Because the business operated as Green Thumb Landscapers, customers already viewed it as a company rather than an individual. When Mark took over, there was no confusion about “where the old owner went” or whether the business would change simply because ownership changed.

This reinforced a key lesson Mark recognized immediately: businesses that are not built around a single person are far easier to transfer, operate, and eventually sell again.

Flexible Terms and Seller Support

The transaction was structured directly with the owner, not a bank. That flexibility made the purchase possible.

The agreement included:

- A reasonable down payment

- Monthly payments funded by business cash flow

- Seller financing over time

- A transition period with hands-on support

One of the most valuable elements of the deal was the seller’s willingness to stay on part-time during the transition. He personally introduced Mark to each customer, explaining the ownership change and reinforcing continuity.

That gesture went a long way in maintaining trust and retention.

Stepping Into a Working Business

From the first day Mark took over, the business was operating:

- Customers were already scheduled

- Pricing was established

- Revenue was coming in immediately

Instead of spending months marketing or building a customer base, Mark focused on learning the business, understanding seasonal patterns, and improving efficiency without disrupting what already worked.

Improving Without Breaking What Worked

Mark didn’t rush changes. He:

- Maintained existing service levels

- Kept pricing stable early on

- Improved invoicing and scheduling

- Introduced digital payments and communication

- Reduced administrative time with simple tools

Because the foundation was solid, these improvements added value rather than risk.

Thinking Like a Seller From Day One

Even though Mark had just become an owner, he thought ahead.

He began:

- Documenting processes

- Cleaning up financial reporting

- Reducing reliance on any one person

- Maintaining equipment replacement reserves

These steps helped the business run better today—and made it more valuable for a future buyer.

Why This Approach Worked

Mark’s success wasn’t accidental. It came from a few deliberate decisions:

- Buying an existing business instead of starting from scratch

- Choosing a business with a transferable name

- Structuring flexible seller-financed terms

- Leveraging the seller’s customer relationships during transition

- Planning for his own eventual exit early

The Bigger Lesson

Buying a business like Green Thumb Landscapers doesn’t eliminate risk—but it replaces uncertainty with information.

For Millennials who want cash flow, structure, and clarity, acquiring an existing business—especially from a retiring owner willing to help with transition—can be an excellent entry point into business ownership.

Whether you start from zero or step into an established operation, the principles remain the same: plan carefully, manage risk, and always think one step ahead.

- He purchased an established business with existing customers and cash flow

- The business name — Green Thumb Landscapers — made ownership transfer seamless

- Seller financing reduced the need for bank loans and upfront capital

- The seller stayed on part-time to personally introduce Mark to customers

- Mark focused on learning before making changes

- Operational improvements were introduced gradually and thoughtfully

- Processes and financials were documented from the beginning

- Exit strategy thinking started on day one, even as a new owner

- Interactive tools to reduce startup risk

- Guided planning and execution resources

- Decision tools for starting vs. buying a business

- Exit strategy planning and valuation guidance

- Member-only articles and tools focused on maximizing long-term value

QUIZ

FAQ

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}