The best way to create a strong revocable living trust is to understand it thoroughly. This was created for you in February 2026.

This master guide explains each major clause, decision point, and structural element in plain English — so you can build with clarity instead of guesswork.

This is not legal advice. It is structured education designed to help you think clearly and prepare responsibly.

Author Introduction (Optional Listening)

Before you begin, you may find it helpful to listen to this short introduction explaining how to use this master guide alongside the Revocable Living Trust Builder.

The goal is not just to fill out a document — but to understand it well enough to create a strong, adaptable trust that can evolve with your life.

- Author Introduction (Optional Listening)

- Video Revocable Living Trust overview

- SECTION I

- The Foundation of Control: What It Means to Create a Revocable Living Trust

- 1. The Legal Architecture

- 2. What “Revocable” Truly Means

- 3. Retaining Control While Changing Title

- 4. The Grantor’s Central Role

- 5. Trust Funding: The Step Many People Miss

- 6. The Living Document Concept

- 7. Why This Foundation Matters

- Transition to Section II

- SECTION II

- Trustee Structure and Incapacity Standards

- 1. Initial Trustee — You Remain in Control

- 2. Successor Trustee — Who Steps In and When?

- 3. Incapacity Standards — One Doctor or Two?

- 4. Co-Trustees and Institutional Trustees

- 5. Trustee Responsibilities After Death

- 🔹 Transition to Data Gathering Section

- SECTION III

- Beneficiary Structure: Who Receives What and How

- 1. Primary Beneficiaries — The First Level of Distribution

- 2. Contingent Beneficiaries — The Backup Plan

- 3. Per Stirpes vs. Per Capita — Why It Matters

- Why Most Revocable Living Trusts Use Per Stirpes

- SECTION IV

- Distribution Control and Protective Clauses

- 1. The Spendthrift Clause

- 2. The No-Contest Clause

- 3. The Residue Clause

- 4. Intentional Exclusion and Disinheritance

- Transition

- SECTION V

- Intentional Disinheritance, Pretermitted Heirs, and Drafting Clarity

- 1️⃣ The Concept of a Pretermitted Heir

- 2️⃣ A State Law Example: Mississippi’s Framework

- 3️⃣ Omission vs. Intentional Disinheritance

- 4️⃣ Why Every Family Member Should Be Considered

- Section VI

- Professional Drafting Strategies to Prevent Disputes

- Advice Regarding Family Members

- Advice Regarding Business Partners

- The Structural Lesson

- SECTION VII

- Funding the Trust: Turning Structure Into Reality

- 1️⃣ Real Estate (Primary Residence, Rental Property, Land)

- 2️⃣ LLC Interests and Business Ownership

- 3️⃣ Bank Accounts

- 4️⃣ Brokerage and Investment Accounts

- 5️⃣ Retirement Accounts (IRAs, 401(k)s)

- 6️⃣ Transfer-on-Death (TOD) and Payable-on-Death (POD) Accounts

- 7️⃣ Tangible Personal Property

- 8️⃣ Why Funding Matters

- 🔹 Funding Flow Summary

- 📥 Downloadable Funding Checklist (Single PDF)

- SECTION VIII

- Advanced Planning Considerations: Legal, Tax, and Structural Realities

- 1. Fiduciary Duties of the Trustee

- 2. Tax Reality of a Revocable Living Trust

- 3. When to Review and Update Your Trust

- 4. Minor Children and Structured Distributions

- 5. Special Needs Planning

- 6. Coordination With Other Legal Documents

- 7. Business Interests and Asset Management

- 8. Privacy and Public Record

- 9. The Limits of a Revocable Living Trust

- 10. General Information Disclaimer

- SECTION IX

- Common Mistakes When Creating a Revocable Living Trust

- 1️⃣ Failing to Fund the Trust

- 2️⃣ Inconsistent Beneficiary Designations

- 3️⃣ Choosing the Wrong Successor Trustee

- 4️⃣ Ignoring State Law Differences

- 5️⃣ Overlooking Business Interests

- 6️⃣ Not Updating the Trust After Major Life Events

- 7️⃣ Assuming a Revocable Trust Provides Asset Protection

- 8️⃣ Failing to Communicate With Family Members

- 9️⃣ Treating the Trust as a Substitute for All Other Documents

- 10️⃣ Improper Execution

- Transition to Next Section

- SECTION X

- Execution and Administration: Making Your Revocable Living Trust Legally Effective

- 1️⃣ Proper Execution Requirements

- 2️⃣ The Difference Between “Valid” and “Functional”

- 3️⃣ Trustee Authority During Life

- 4️⃣ Successor Trustee Activation

- Case Study: Choosing the Right Successor Trustee

- The Five Factors They Considered

- The Outcome

- The Structural Lesson

- 5️⃣ Certificate of Trust

- 6️⃣ Safe Storage and Communication

- 7️⃣ Coordination With Other Legal Documents

- 8️⃣ Common Execution Errors

- 9️⃣ Emotional Leadership

- Final Reflection on Section X

- SECTION XI

- Advanced Planning Considerations: Legal, Tax, and Structural Realities of a Revocable Living Trust

- 1️⃣ Asset Protection During Your Lifetime

- 2️⃣ Estate Taxes and Federal Thresholds

- 3️⃣ Income Tax Reporting

- 4️⃣ Retirement Accounts and Beneficiary Designations

- 5️⃣ Life Insurance Policies

- 6️⃣ Business Interests and Operating Agreements

- 7️⃣ Blended Families and Second Marriages

- 8️⃣ Special Needs Beneficiaries

- 9️⃣ Multi-State Real Estate Ownership

- 🔟 Limitations and Legal Reality

- General Information Disclaimer

- Section XII

- State Laws Regulate Trusts — Why Probate Costs Vary Across the Country

- Illustrative Comparison: Probate vs. Revocable Living Trust

- Real-World Contrast: When Does a Revocable Living Trust Add Value?

- Section XIII

- The Cost of Delay: A Real-World Illustration

- Case Study: Brenda and Saul

- What Happened Next

- Financial Impact Illustration

- Emotional Cost

- A Balanced Contrast: The Johnson Family

- Structural Lesson

- Subtle Planning Reality

- SECTION XIV

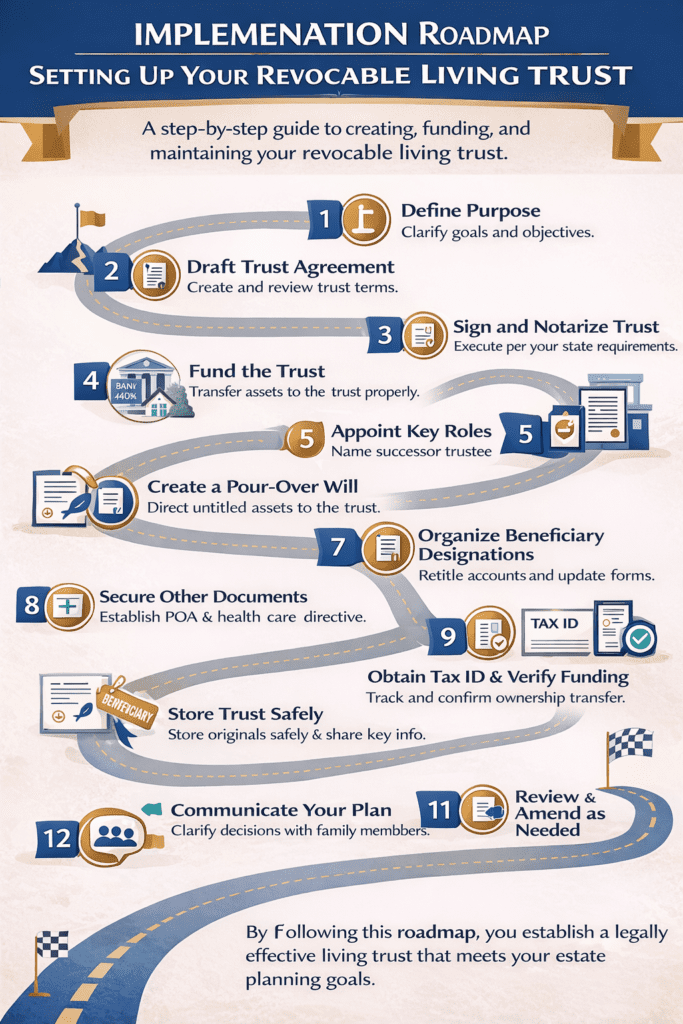

- Implementation Roadmap: Turning Structure Into Action

- Step 1: Gather Your Information

- Step 2: Define Roles Before Drafting

- Step 3: Clarify Distribution Philosophy

- Step 4: Use a Structured Drafting Process

- Step 5: Execute Properly

- Step 6: Fund the Trust

- Step 7: Review Every 2–3 Years

- Why This Matters

- A Thoughtful Closing Reflection

- Ready to Build?

- Short Quiz

- FAQ’s

- Frequently Asked Questions About Revocable Living Trusts

Video Revocable Living Trust overview

A revocable living trust is one of the most consequential documents you may ever create. It determines how your assets are managed during your lifetime, how they are handled if you become incapacitated, and how they are ultimately distributed to the people you care about most.

This master guide was created to move beyond surface-level explanations. It is designed to walk through the structure of a revocable living trust clause by clause, explaining not only what each provision does, but why it matters and how thoughtful decisions at each stage can strengthen the entire document.

The accompanying Revocable Living Trust Builder, part of our subscription Financial Lab series, was not assembled casually or generated in a single sitting. Creating it was a long and deliberate process. I have been at the helm of this project from the beginning.

It took more than a month of drafting, refining, restructuring, and testing to ensure that the tool produces a clear, coherent, and adaptable trust document — not just an automated form.

As part of an estate planning portfolio, I wanted our members to have an excellent tool, not simply an AI creation. The goal was to build something that mirrors the careful thought process that goes into strong estate planning.

Many years ago, I went through this same decision-making process personally. I learned what was necessary to protect my family financially through careful planning, asset management, and disciplined documentation. The questions you will encounter in this guide are not theoretical. They are the same structural considerations I worked through when putting my own planning framework in place.

As with virtually everything I have written and created at RetireCoast, this material comes from experience. I have been there and done that.

You will notice throughout this guide that I have inserted what are labeled as “callouts.” These highlighted sections are written in plain English to emphasize some of the most important structural elements of this article. While we have made every effort to keep the process clear and manageable, legal terminology can sometimes feel dense.

When in doubt, pause and read the callouts. They are designed to restate key points simply and prevent confusion before it begins.

If you take the time to understand the clauses explained in this guide — and apply them thoughtfully using the builder — you will not simply complete a document. You will build a structured, living plan designed to evolve with your circumstances over time.

I am pleased that you are moving forward with one of the most important planning efforts you will ever undertake.

Hint: Use the table of contents to navigate this article. Click on any section, and it will take you directly there.

Let’s begin.

SECTION I

The Foundation of Control: What It Means to Create a Revocable Living Trust

When you decide to create a revocable living trust, you are not merely drafting paperwork. You are establishing a legal structure that determines how assets are held, controlled, and ultimately transferred.

At its core, a revocable living trust is a framework of authority.

Before examining specific clauses, it is essential to understand what actually happens when you create a revocable living trust and how control is structured within it.

Legal terminology can feel unfamiliar — after all, how often do we use words like “Grantor” in everyday life?

In this document, you are the Grantor because you are creating this revocable living trust. Even if an attorney or third party drafts the document, they are doing so on your behalf. You remain the Grantor because the trust originates from you.

1. The Legal Architecture

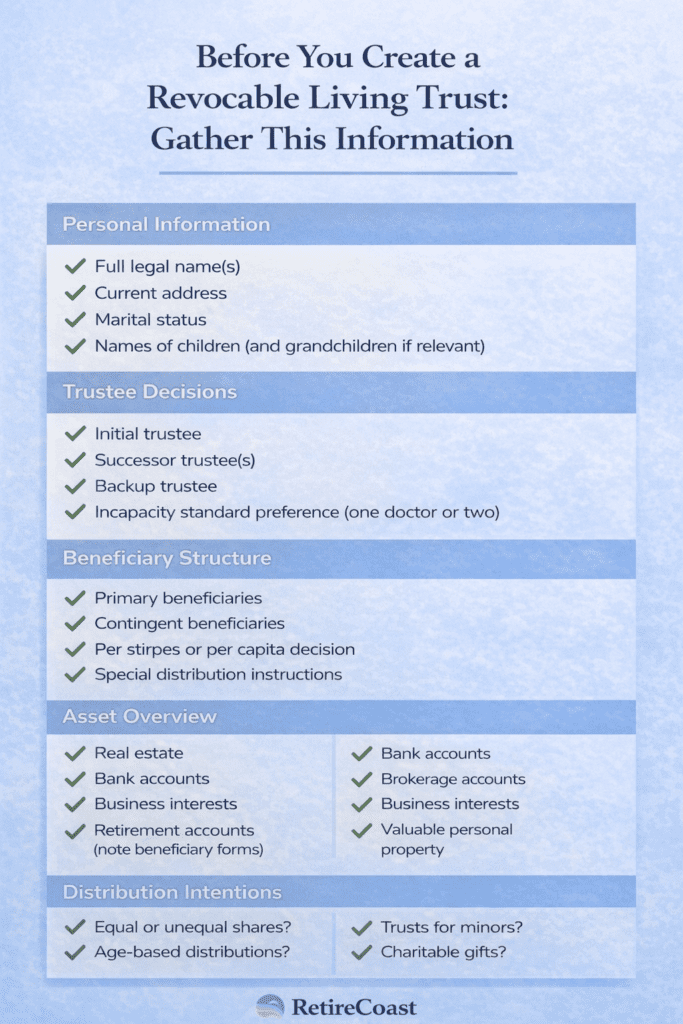

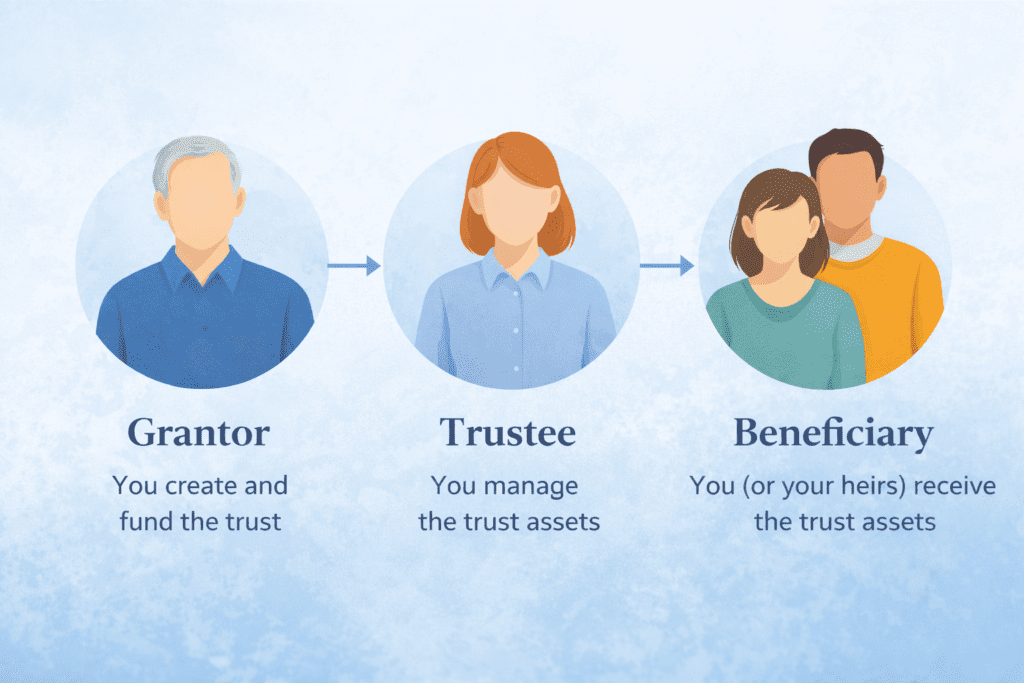

To create a revocable living trust, three foundational roles must exist:

- The Grantor (also called Settlor or Trustor)

- The Trustee

- The Beneficiaries

The Trustee is the person responsible for managing the trust assets according to the instructions written in the document.

In most revocable living trusts, you serve as your own Trustee during your lifetime. This means you continue managing your property exactly as you do now — buying, selling, investing, and making financial decisions.

A successor Trustee only steps in if you become incapacitated or after your death.

In most modern revocable living trusts, especially during the grantor’s lifetime, these roles initially overlap.

You are typically:

- The Grantor (the person creating the trust)

- The Trustee (the person managing the trust)

- The primary beneficiary during your lifetime

This overlap is not a flaw. It is intentional.

When you create a revocable living trust, you are not surrendering control of your assets. You are repositioning legal title while retaining authority.

A Primary Beneficiary is the person (or people) you name to receive assets from the trust under the first level of distribution instructions.

In simple terms, these are the individuals you intend to benefit from the trust when its instructions are carried out.

Later in this guide, we will explain how contingent beneficiaries and generational distribution rules may affect this structure.

2. What “Revocable” Truly Means

The word “revocable” is often misunderstood.

Creating a revocable living trust means:

- You can amend it.

- You can revoke it entirely.

- You can change beneficiaries.

- You can change trustees.

- You can modify distribution instructions.

At any time during your lifetime — provided you are legally competent — you maintain complete authority.

This distinguishes a revocable trust from an irrevocable trust, which typically involves surrendering control.

The revocability feature ensures that when you create a revocable living trust, the document remains adaptable to:

- Marriage or divorce

- Birth of children or grandchildren

- Acquisition of property

- Sale of businesses

- Changes in financial condition

- Shifts in family relationships

A strong trust is not static. It evolves.

3. Retaining Control While Changing Title

One of the most misunderstood aspects of estate planning is this:

When you create a revocable living trust, ownership of certain assets is transferred into the trust — but control is not surrendered.

Here’s what actually changes:

| Before | After |

|---|---|

| You own assets individually | The trust owns the assets |

| You control assets personally | You control assets as Trustee |

Functionally, very little changes during your lifetime.

You still:

- Buy and sell property

- Manage investments

- Open and close accounts

- Collect income

- Pay expenses

The difference is structural. Legal title is repositioned so that management continuity exists if you become incapacitated or pass away.

4. The Grantor’s Central Role

When you create a revocable living trust, the grantor is the architect.

The grantor:

- Determines beneficiaries

- Defines distribution rules

- Appoints successor trustees

- Establishes incapacity standards

- Sets protective provisions (such as spendthrift clauses)

The trust document does not think for itself. It reflects the grantor’s decisions.

This is why understanding each clause matters.

You are not filling blanks.

You are the defining authority.

5. Trust Funding: The Step Many People Miss

It is possible to create a revocable living trust and still fail to achieve its purpose.

The most common mistake is failing to properly fund the trust.

Funding means transferring ownership of assets into the name of the trust.

Examples:

- Deeding real estate to the trust

- Retitling brokerage accounts

- Assigning business interests

- Changing account ownership to the trust

If you create a revocable living trust but do not fund it, the document becomes largely symbolic.

Case Study Example:

David creates a revocable living trust but forgets to transfer his rental property into the trust’s name. Upon his death, the rental property must still go through probate because it was never titled in the trust.

The lesson:

Creating a revocable living trust is only step one.

Funding completes the structure.

We will explore funding in much greater depth in a later section.

To become effective, your revocable living trust must be funded. This means transferring ownership of assets into the name of the trust.

For example, a checking account currently titled in your personal name would be retitled so that the trust becomes the legal owner. The same principle applies to real estate and other titled assets.

Do not worry — you still maintain control. When you serve as Trustee, you continue managing those assets just as you do now. The trust changes legal title, not your authority.

6. The Living Document Concept

One of the most powerful features of a revocable trust is flexibility.

When you create a revocable living trust, you are building a document designed to change over time.

You should review it when:

- A child is born

- A beneficiary dies

- A trustee relocates

- You acquire significant assets

- Tax laws shift

- Family dynamics change

Strong estate planning is not a one-time event.

It is a disciplined, periodic review process.

Creating a revocable living trust does not, by itself, avoid probate.

Only assets that are properly transferred into the trust — meaning legally retitled in the name of the trust — are governed by its instructions outside of probate.

If assets remain in your individual name at death, those assets may still require probate, even if you have taken the time to create a revocable living trust.

7. Why This Foundation Matters

Before evaluating:

- Spendthrift clauses

- Per stirpes distributions

- Incapacity certifications

- Residue instructions

- Pour-over coordination

You must first understand the architecture of control.

When you create a revocable living trust, you are not surrendering authority.

You are organizing it.

And organization is what prevents confusion, delay, and unnecessary conflict later.

Transition to Section II

Now that we have established how control is structured when you create a revocable living trust, the next step is to examine how trustees function — both during your lifetime and after incapacity or death.

Section II will explore:

- The role of the initial trustee

- Successor trustees

- Incapacity standards (one doctor vs two)

- Practical activation scenarios

A revocable living trust is only one of many types of trusts recognized under the law.

When referring to your document, it is best to call it what it is — a Revocable Living Trust — to avoid confusion with other structures such as irrevocable trusts, special needs trusts, charitable trusts, or asset protection trusts.

Precision in terminology prevents misunderstanding, especially when communicating with financial institutions, attorneys, or family members.

SECTION II

Trustee Structure and Incapacity Standards

When you create a revocable living trust, control does not disappear — it transitions according to rules you establish.

This section explains how that transition works.

Understanding trustee structure is essential because the trustee is the individual legally responsible for carrying out your instructions. The trustee is not symbolic. The trustee is the operating authority.

Selecting a successor trustee can be one of the most emotionally complex decisions in creating a revocable living trust.

To help remove emotion from the process, RetireCoast has created a structured Successor Trustee Evaluation Tool available exclusively to Financial Lab members. The tool guides you through objective criteria — including financial literacy, organization, availability, and stability — so you can make a reasoned decision.

This tool is located inside the Membership Lab → Revocable Living Trust Section and is not part of the free public content.

1. Initial Trustee — You Remain in Control

In most revocable living trusts, the person who creates the trust also serves as the initial trustee.

This means:

- You continue managing your assets.

- You make investment decisions.

- You buy and sell property.

- You control bank accounts.

- You retain full authority.

When you create a revocable living trust and serve as trustee, daily life does not change.

The structure changes.

Control does not.

This is one of the reasons many people choose to create a revocable living trust — it allows continuity without surrendering autonomy.

2. Successor Trustee — Who Steps In and When?

A successor trustee is the person (or institution) you name to manage the trust if:

- You become incapacitated, or

- You pass away.

This is one of the most important decisions in the document.

The successor trustee does not inherit your assets.

They administer them according to your written instructions.

Case Study Example:

Maria names her adult daughter as successor trustee. Maria continues managing everything herself while healthy. Years later, after a serious stroke, Maria is declared incapacitated under the standards defined in her trust. Her daughter immediately steps in as trustee and manages the trust assets without court involvement.

This is the structural continuity a revocable living trust is designed to create.

Naming a successor trustee is not always as simple as entering a name into a document.

If you have children, it can be wise to speak with all of them about your decision — especially if you are naming one child over the others. Explain your reasoning clearly and calmly. This is your decision, but transparency can prevent misunderstandings later.

Express your desire that everyone work together and respect the structure you have created. A thoughtful family conversation today may prevent unnecessary conflict in the future.

3. Incapacity Standards — One Doctor or Two?

When you create a revocable living trust, you must define how incapacity is determined.

Most trusts use one of two standards:

Option A — Certification by One Licensed Physician

Simpler. Faster.

Less administrative burden.

Option B — Certification by Two Licensed Physicians

More conservative.

Adds protection against premature activation.

There is no universally correct answer.

Considerations:

- Family dynamics

- Potential for disputes

- Complexity of assets

- Personal comfort level

The decision affects how easily your successor trustee can act.

This is not a theoretical clause.

It determines how quickly financial management continues if you cannot act for yourself.

4. Co-Trustees and Institutional Trustees

Some individuals choose:

- Co-trustees (two people acting together)

- A corporate trustee (bank or trust company)

Each has implications.

Co-Trustees:

- May provide checks and balances

- May slow decision-making

- Require cooperation

Corporate Trustees:

- Professional administration

- Fee-based structure

- Useful for complex estates

Most revocable living trusts begin with an individual successor trustee and name a backup.

Selecting a successor trustee is a practical decision, not simply a symbolic one.

If you choose a family member, select the person with the strongest ability to manage not only financial matters, but also family dynamics and unexpected issues that may arise.

The role requires organization, patience, objectivity, and sound judgment. It is often less about affection and more about capability.

5. Trustee Responsibilities After Death

When the grantor passes away, the successor trustee must:

- Locate trust documents

- Gather trust assets

- Notify beneficiaries

- Pay valid debts

- Distribute assets according to instructions

- Maintain accounting records

This is an administrative role, not a ceremonial one.

When you create a revocable living trust thoughtfully, you reduce confusion for the person who must perform these duties.

🔹 Transition to Data Gathering Section

Now we bridge into practical implementation.

Before you create a revocable living trust — and before naming trustees — you should gather structured information.

This prevents rushed decisions and incomplete drafting.

SECTION III

Beneficiary Structure: Who Receives What and How

When you create a revocable living trust, one of the most significant decisions you make involves who will ultimately benefit from the assets you have organized.

This section explains how beneficiary design works, how distribution layers are structured, and how generational planning decisions affect long-term outcomes.

The goal is clarity — not complexity.

1. Primary Beneficiaries — The First Level of Distribution

Primary beneficiaries are the individuals (or entities) you name to receive assets under your first layer of instructions.

In many revocable living trusts, primary beneficiaries are:

- A surviving spouse

- Children

- Or a combination of both

If you are married, your trust may state that upon your death, all assets remain available for the benefit of your surviving spouse.

If you are single, your primary beneficiaries may be your children.

When you create a revocable living trust, you are defining the first line of succession.

This is not merely a naming exercise — it establishes the structural order of inheritance.

2. Contingent Beneficiaries — The Backup Plan

Contingent beneficiaries step in if a primary beneficiary is unable to receive their share.

For example:

You name your three children as primary beneficiaries.

If one child predeceases you, what happens to that child’s share?

Without clear instructions, uncertainty can arise.

When you create a revocable living trust thoughtfully, you anticipate that life may not unfold in perfect sequence.

Contingent beneficiary design prevents gaps.

We will now examine the two most common generational distribution methods used in modern trusts.

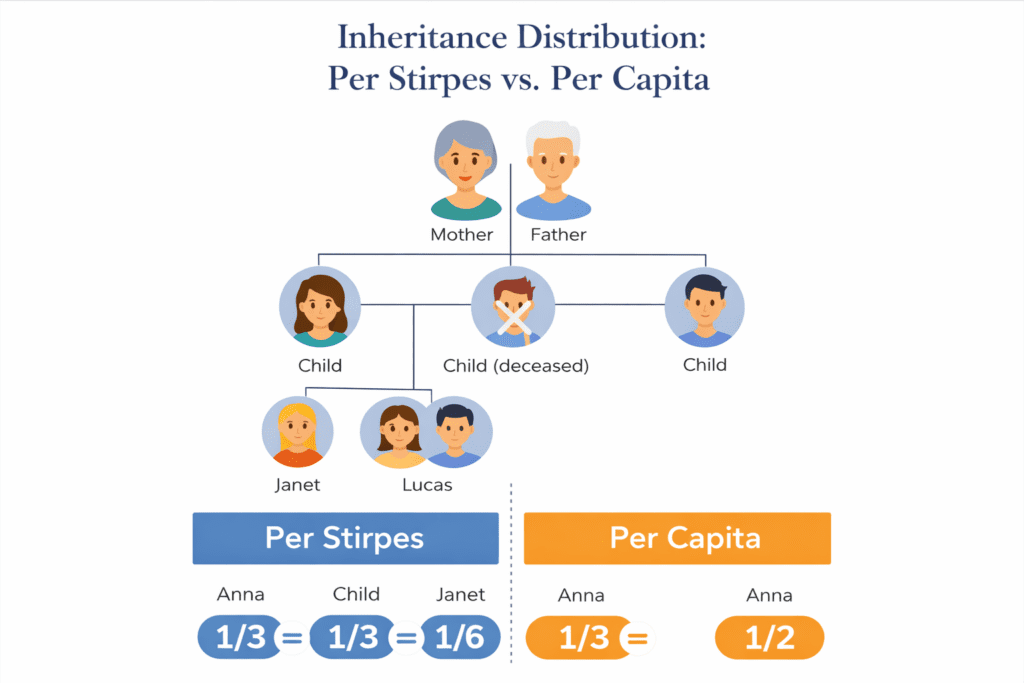

3. Per Stirpes vs. Per Capita — Why It Matters

These Latin phrases may sound intimidating, but they describe a simple structural difference.

They answer one question:

If one beneficiary dies before you, who receives that person’s share?

When creating your revocable living trust, you must decide between per stirpes and per capita — unless you are leaving everything to one person and it will never be divided.

Most married couples leave everything to the surviving spouse first. When the spouse later passes away, the children typically divide the estate equally.

If one child passes before you and leaves children of their own, many families prefer that the grandchildren divide their parent’s share equally. This is the per stirpes approach.

For many families, this structure feels straightforward and fair — which is why Per Stirpes commonly chosen.

Per Stirpes

“Per stirpes” means by branch of the family.

If a beneficiary dies before you, that beneficiary’s children step into their place and divide that share equally.

Example:

You have three children:

- Anna

- Brian

- Claire

Each is entitled to 1/3.

Brian dies before you, but has two children.

Under per stirpes:

Anna receives 1/3

Claire receives 1/3

Brian’s two children split his 1/3 (each receives 1/6)

The family branch continues.

Per Capita

“Per capita” means by headcount among surviving members.

Using the same example:

If Brian dies before you, under per capita:

Anna and Claire would split the estate equally.

Brian’s children would not automatically receive his share unless separately named.

The branch does not continue.

Why Most Revocable Living Trusts Use Per Stirpes

When individuals create a revocable living trust, they often want their grandchildren to inherit their parents’ share if that parent has passed away.

Per stirpes preserves generational continuity.

Per capita may be appropriate in some circumstances — especially where beneficiaries are not related by branch structure.

The choice is intentional.

It shapes generational distribution.

Quick Knowledge Check

Before moving forward, take a moment to confirm your understanding of the core structure. If you can comfortably answer these questions, you are well prepared to create a revocable living trust using the guided builder.

1. Who is the Grantor when you create a revocable living trust?

You are the Grantor. The person creating the trust is the Grantor, even if an attorney drafts the document on your behalf.

2. Who controls the assets during your lifetime?

You control the assets as Trustee. Creating a revocable living trust changes legal title, not your authority.

3. What does “per stirpes” mean?

It means “by branch.” If a child passes away before you, that child’s share passes to their children rather than being redistributed among surviving siblings.

4. What does a spendthrift clause protect?

It protects beneficiaries by preventing creditors from accessing trust assets before distributions and limiting assignment of future inheritance.

5. Does simply creating a trust automatically avoid probate?

No. Only assets properly transferred (funded) into the trust avoid probate. Unfunded assets may still require probate.

If these answers feel clear to you, you are prepared to move from understanding to implementation.

SECTION IV

Distribution Control and Protective Clauses

When you create a revocable living trust, naming beneficiaries is only part of the structure. A strong trust also contains protective provisions designed to reduce disputes, preserve assets, and clarify how instructions are to be enforced.

These clauses are not dramatic additions. They are structural safeguards.

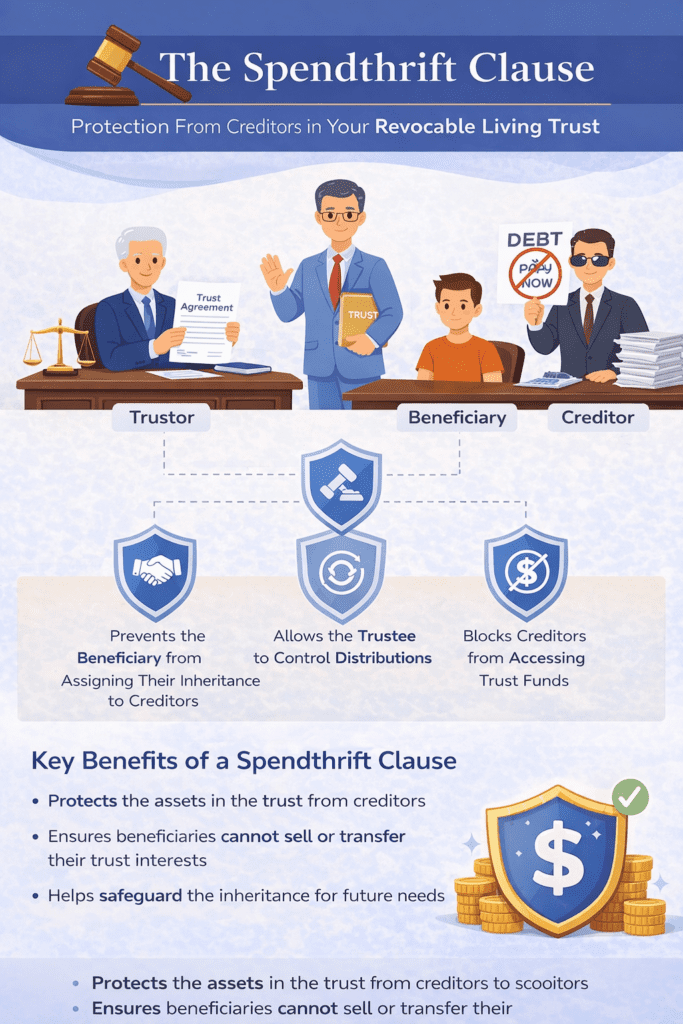

1. The Spendthrift Clause

A spendthrift clause is one of the most common protective provisions in a revocable living trust.

What It Does

A spendthrift clause generally prevents:

- Beneficiaries from assigning their future inheritance to creditors

- Creditors from seizing trust assets before distribution

- Beneficiaries from pledging trust interests as collateral

In simple terms, it protects inherited assets before they are distributed.

The spendthrift clause appears in nearly all modern revocable family trusts — and for good reason.

Not every beneficiary will have the same level of financial experience or discipline. In addition, outside pressures or unscrupulous individuals may attempt to influence beneficiaries to redirect or pledge future inheritance.

A properly drafted spendthrift clause limits that risk by preventing assignment of future trust interests and restricting creditor access before distributions are made.

It protects your instructions from being undermined after you are no longer present to enforce them.

Important Clarification

When you create a revocable living trust, a spendthrift clause does not:

- Protect you (the grantor) from your own creditors

- Shield assets during your lifetime

- Provide asset protection against personal liability

Its purpose is to protect beneficiaries once the trust begins making distributions.

Practical Example

Suppose you leave assets to a child who later experiences financial difficulty. Without a spendthrift clause, creditors may attempt to intercept distributions.

With a properly drafted spendthrift clause, the trustee retains discretion and control over distributions. This creates an additional layer of protection.

2. The No-Contest Clause

A no-contest clause (sometimes called an “in terrorem” clause) is designed to discourage litigation.

It generally states:

If a beneficiary challenges the trust and loses, that beneficiary forfeits their inheritance.

This provision can reduce:

- Frivolous lawsuits

- Emotionally driven disputes

- Opportunistic claims

However, enforceability varies by state law.

When you create a revocable living trust, clarity in drafting is essential because ambiguous provisions often fuel contests.

Litigation is often the result of trusts that are not clearly drafted — where there is uncertainty about who receives what, when, and under what conditions.

Leaving out even one essential structural element can lead to disputes that consume years and significant legal fees, reducing the very assets the trust was designed to preserve.

A properly written no-contest clause discourages unnecessary challenges and reinforces the clarity of a well-crafted revocable living trust.

Practical Example

If one beneficiary believes they were treated unfairly and files suit to challenge the trust, the no-contest clause may require them to risk their inheritance in order to proceed.

This often discourages weak or emotionally driven challenges.

3. The Residue Clause

The residue clause governs:

“All the rest, residue, and remainder” of the trust estate.

No matter how carefully you draft a trust, something may be unintentionally omitted:

- A small bank account

- A refund

- Personal property

- A late-discovered asset

The residue clause ensures that these assets are still distributed according to your overall plan.

Without a residue clause, even minor omissions can create major confusion.

When you create a revocable living trust properly, nothing is left structurally unaccounted for.

Just when you think everything has been properly transferred into your trust, you discover an asset you overlooked.

If you were to pass away without recognizing and transferring that asset, the residue clause and a properly drafted pour-over will can act as a safety net.

The Scenario

An investor establishes a revocable living trust for estate planning purposes. They properly transfer their primary residence and two LLCs holding short-term rental properties into the trust.

Two years later, they acquire a new multi-family property using the BRRRR method. After stabilizing the property, they place it into a newly formed LLC. However, they forget to formally assign the membership interest of this new LLC to the trust.

Unexpectedly, the investor passes away.

The Potential Crisis

Because the new LLC remains titled in the investor’s individual name, it falls outside the instructions of the trust.

Without a protective structure in place, that asset could be subject to probate. Depending on the circumstances and state law, distribution may not align perfectly with the trust’s intended structure. Legal fees and delays could follow.

The Safety Net

Fortunately, a properly drafted pour-over will was created alongside the trust. The will contains a residuary clause stating:

“I give, devise, and bequeath all the rest, residue, and remainder of my estate to the Trustee of my Trust, to be administered according to its terms.”

This clause directs any assets unintentionally left outside the trust to be transferred into the trust and distributed under its instructions.

While probate may still be required for that asset, the pour-over provision ensures it ultimately follows the structured plan you created.

The lesson is simple: funding your trust is critical — but strong drafting anticipates human oversight.

4. Intentional Exclusion and Disinheritance

In some situations, you may choose to exclude an individual from receiving assets.

This is a separate drafting issue from protective clauses and deserves careful treatment.

We will address intentional disinheritance and related considerations — including pretermitted heir concerns — in the next section.

Clear drafting prevents ambiguity.

Ambiguity invites conflict.

Transition

Protective clauses strengthen the structure of your trust.

But when it comes to intentionally excluding someone — or clearly identifying who is and is not included — additional clarity is required.

Next, we will address:

SECTION V

Intentional Disinheritance, Pretermitted Heirs, and Drafting Clarity

When you create a revocable living trust, precision is not optional. It is protective.

Many estate disputes do not arise because someone was treated unfairly. They arise because the document was unclear, silent, or incomplete.

The law in most states protects certain family relationships by default. If you intend to depart from those defaults, clarity is required.

This section explains how intentional disinheritance works, how courts interpret omissions, and why professional drafting strategies focus heavily on eliminating ambiguity.

1️⃣ The Concept of a Pretermitted Heir

A pretermitted heir is generally a child who is unintentionally omitted from a will or trust.

In many states, courts presume that a child who is completely left out — particularly one born or adopted after the document was executed — was omitted accidentally.

If that presumption applies, the court may intervene and award the omitted child a statutory share of the estate, even if the trust does not name them.

The goal of these laws is fairness.

The consequence, however, can be disruption of your carefully structured plan.

When you create a revocable living trust, silence can be interpreted as mistake.

2️⃣ A State Law Example: Mississippi’s Framework

To illustrate how state-level law operates, consider Mississippi as an example.

You will not find a single statute in the Mississippi Uniform Trust Code (Title 91, Chapter 8) labeled “Intentional Disinheritance.”

Instead, Mississippi addresses these issues through its broader Wills and Estates statutes under Title 91, Chapter 5.

Disinheriting Children

Under Mississippi Code § 91-5-3 and § 91-5-5

(See: https://law.justia.com/codes/mississippi/title-91/chapter-5/)

The state protects pretermitted heirs. If a child is entirely omitted, the court may presume the omission was accidental and award that child a statutory share.

To overcome this presumption, the trust or will must contain explicit language demonstrating that the omission was intentional.

For example:

“I have intentionally made no provision in this Trust for my son, John Doe, and he shall take nothing.”

The law does not prohibit disinheritance.

It requires clarity.

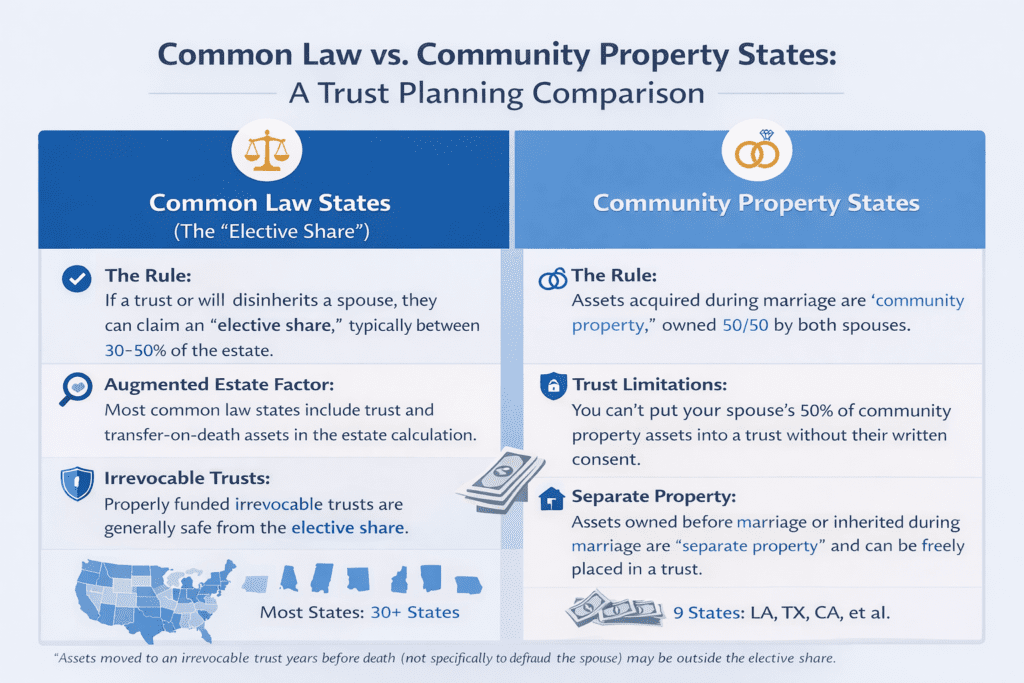

Disinheriting a Spouse

Spouses are treated differently in most states, including Mississippi.

Under Mississippi Code § 91-5-25, a surviving spouse generally has the right to “renounce” a will or related estate plan if they are left less than their statutory entitlement.

By filing a renunciation, the spouse may claim what is commonly referred to as a “child’s share,” regardless of the trust’s instructions.

In practical terms:

You generally cannot fully disinherit a surviving spouse without formal legal consent, such as a valid prenuptial or postnuptial agreement.

This distinction between children and spouses exists in many states, though the details vary.

3️⃣ Omission vs. Intentional Disinheritance

There is a critical legal difference between:

Accidental omission

and

Intentional exclusion

If you intend to exclude someone from your trust:

• Name them clearly

• State that the omission is intentional

• Avoid emotional or inflammatory language

• Keep the language factual

Ambiguity invites interpretation.

Interpretation invites litigation.

When you create a revocable living trust, clarity prevents courts from guessing at your intent.

4️⃣ Why Every Family Member Should Be Considered

Even if you do not intend to leave assets to certain individuals, every close family member should be considered in the drafting process.

This includes:

• Biological children

• Adopted children

• Children from prior marriages

• Future-born children

• In some cases, stepchildren

You are not required to distribute assets equally.

You are not required to distribute assets at all.

But you should make deliberate decisions.

Consideration strengthens the structure of the document.

Section VI

Professional Drafting Strategies to Prevent Disputes

When advising clients who intend to leave family members or business partners out of a trust, estate planning attorneys focus on two objectives:

Eliminate ambiguity.

Preempt litigation.

The strategy changes depending on whether the person involved is a family member or a professional colleague.

Advice Regarding Family Members

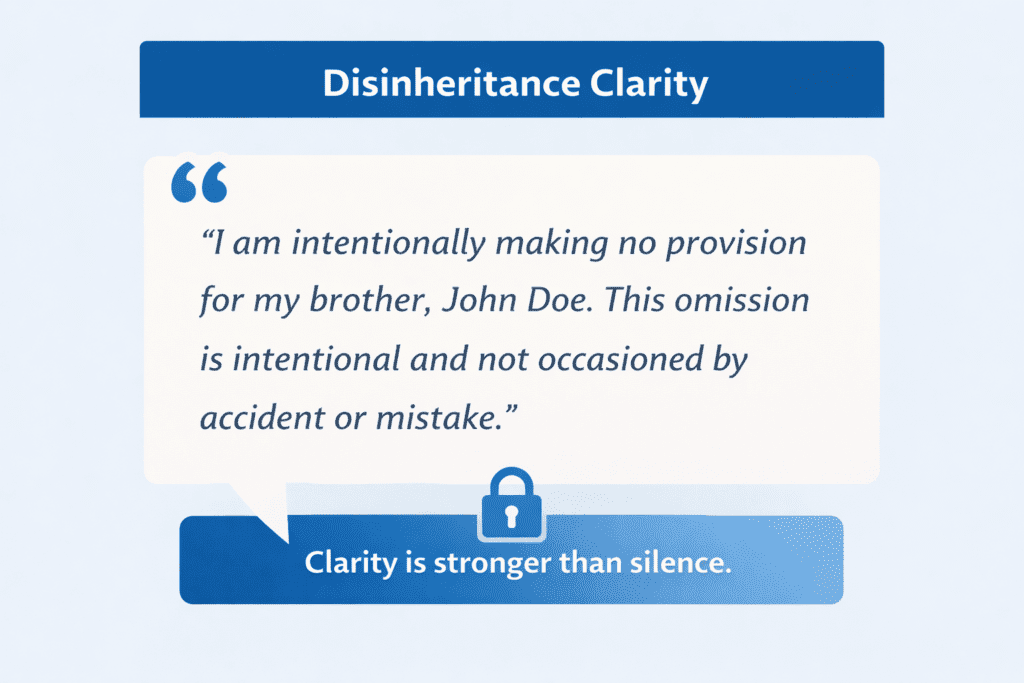

1️⃣ Name Names Clearly

Attorneys advise against simply ignoring someone in a trust.

Clear language reduces the risk of pretermitted heir claims.

Example:

“I am intentionally making no provision for my brother, John Doe. This omission is intentional and not occasioned by accident or mistake.”

Clarity is stronger than silence.

2️⃣ The “Token Gift” Strategy

In some circumstances, attorneys may recommend leaving a small, specific bequest to a potentially litigious relative rather than leaving nothing.

This is often paired with a strict No-Contest (In Terrorem) Clause.

The reasoning is practical:

The individual must choose between accepting the guaranteed amount or challenging the trust and risking forfeiture.

This does not eliminate litigation risk.

But it can discourage weak challenges.

Enforceability varies by state.

3️⃣ Address Spousal Rights Properly

In many states, a spouse’s statutory rights cannot simply be drafted away.

If the objective is to separate certain assets — such as business holdings or a real estate portfolio — attorneys typically require:

• A prenuptial or postnuptial agreement

• A written waiver of elective share rights

• Explicit reference to that agreement within the trust

Without proper documentation, statutory spousal protections may override your plan.

4️⃣ Communicate the “Why” Outside the Trust

Trusts should remain neutral and legal in tone.

However, attorneys often advise preparing a separate “Letter of Wishes.”

This private document may:

• Explain unequal distributions

• Reference prior lifetime financial assistance

• Address concerns about financial responsibility

• Provide context for the trustee

The trust remains legally precise.

The explanation remains private.

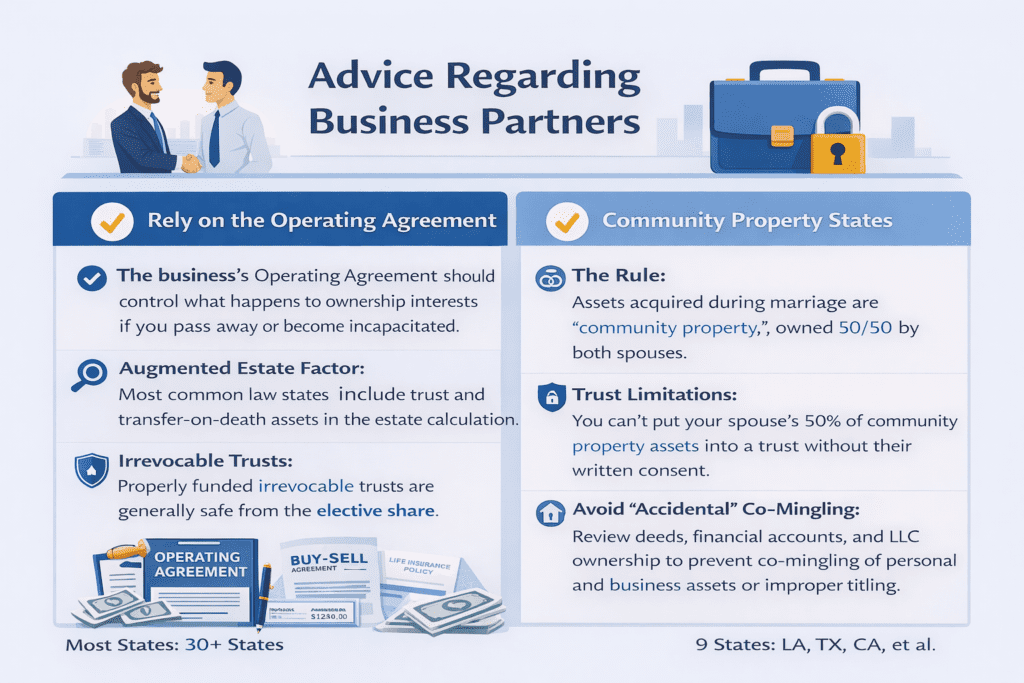

Advice Regarding Business Partners

Estate planning becomes more complex when business interests are involved.

The guiding principle is separation.

Build a firewall between your personal estate plan and your professional entities.

1️⃣ Rely on the Operating Agreement — Not the Trust

The best way to prevent unintended co-ownership problems is through the governing documents of the business.

An LLC Operating Agreement or Shareholder Agreement should dictate what happens to your ownership interest upon death or incapacity.

The trust should not be the primary mechanism controlling business succession.

2️⃣ Implement a Buy-Sell Agreement

Attorneys widely recommend Buy-Sell provisions that:

• Require the estate to sell ownership interests back to the company or partner

• Establish a valuation method

• Use life insurance to fund the purchase

This prevents your surviving spouse or children from unexpectedly becoming co-owners of an operating enterprise.

3️⃣ Avoid Accidental Co-Mingling

Titling controls outcome.

If property is held as:

“Joint Tenants with Right of Survivorship”

It may automatically transfer to the surviving joint owner — regardless of what your trust states.

Review:

• Deeds

• LLC membership certificates

• Brokerage registrations

• Bank account titling

Your trust does not override improper titling.

When you use our Revocable Living Trust Builder, you will be prompted to consider anyone and everyone you may want to leave something to. The final trust document you print is designed to reflect that careful consideration—using the same structural thinking outlined in this guide.

Before you sit down to enter your information, take a few minutes to review the sections above. No trust is bulletproof, but thoughtful planning and clear decisions can greatly increase the likelihood that your document does what you intend.

The Structural Lesson

When you create a revocable living trust, you are building within a legal framework.

Intentional exclusion requires:

• Clear drafting

• Awareness of state law

• Coordination with business agreements

• Accurate asset titling

• Thoughtful communication

Estate planning is not simply document preparation.

It is structural coordination.

Our Revocable Living Trust Builder is designed to work in coordination with other essential estate planning documents — including our Pour-Over Will creator.

A revocable living trust does not replace a will, and a will does not replace a revocable living trust. Most well-structured estate plans include both. Each document serves a different legal function and contains provisions the other does not.

To better understand how these documents interact, review our article: Estate Planning Documents Overview .

SECTION VII

Funding the Trust: Turning Structure Into Reality

Creating a revocable living trust establishes the legal structure.

Funding the trust makes it operational.

A signed trust that is never funded is structurally incomplete. Assets not transferred into the trust may still be subject to probate and distributed according to default rules rather than your written plan.

Funding means transferring ownership of assets from your individual name to the name of your trust.

Below is how that process works across major asset categories.

1️⃣ Real Estate (Primary Residence, Rental Property, Land)

Real property must be formally retitled.

This typically involves:

• Preparing a new deed

• Transferring ownership from your individual name to the trust

• Recording the deed with the appropriate county office

If you own property in multiple states, each property must be transferred separately.

Mini-Checklist — Real Estate

- ☐ Confirm how the property is currently titled

- ☐ Prepare appropriate deed (often warranty or quitclaim, depending on situation)

- ☐ Reference the full legal name of the trust

- ☐ Record deed with county clerk

- ☐ Retain recorded copy with trust documents

Important: If the property is jointly owned with a spouse, both spouses may need to execute the transfer.

We have created a detailed article — Funding a Revocable Living Trust — specifically to help you understand how to properly transfer assets into your trust, including how to transfer real estate.

You should read that article before beginning the funding process. As we have emphasized throughout this guide, your funding process should be complete and deliberate, leaving nothing out of consideration.

Whether you ultimately decide to include a particular asset in your trust is less important than thoughtfully determining whether it belongs there or not.

2️⃣ LLC Interests and Business Ownership

Business ownership is not transferred through a deed. It is transferred through the assignment of membership interest.

If you own:

• An LLC holding rental property

• A brokerage

• A consulting company

• An investment entity

You typically execute an Assignment of Membership Interest, transferring your ownership interest into the trust.

The LLC Operating Agreement should also be reviewed to ensure trust ownership is permitted.

Mini-Checklist — LLC Interests

- ☐ Review the Operating Agreement for transfer restrictions

- ☐ Prepare Assignment of Membership Interest

- ☐ Update company records to reflect trust ownership

- ☐ Coordinate with Buy-Sell provisions (if applicable)

Remember: The trust governs your ownership interest. The Operating Agreement governs company operations.

3️⃣ Bank Accounts

Bank accounts are typically retitled by visiting the institution and completing trust account documentation.

You will usually need:

• A Certificate of Trust

• Trust identification details

• Personal identification

The account name changes to:

“John Doe, Trustee of the John Doe Revocable Living Trust dated [date]”

Mini-Checklist — Bank Accounts

- ☐ Obtain Certificate of Trust

- ☐ Visit the bank branch

- ☐ Retitle account in trust name

- ☐ Confirm online access remains active

You retain control as Trustee.

4️⃣ Brokerage and Investment Accounts

Brokerage accounts follow a similar process to bank accounts.

However, pay attention to:

• Margin agreements

• Options permissions

• Beneficiary designations

Mini-Checklist — Brokerage Accounts

- ☐ Contact brokerage firm

- ☐ Complete trust retitling forms

- ☐ Confirm cost basis tracking remains intact

- ☐ Review beneficiary designations if applicable

5️⃣ Retirement Accounts (IRAs, 401(k)s)

Retirement accounts are usually not retitled into a revocable living trust during your lifetime.

Instead, the trust may be named as a beneficiary — depending on planning objectives.

Improper beneficiary designation can override your trust entirely.

Mini-Checklist — Retirement Accounts

- ☐ Review current beneficiary forms

- ☐ Confirm primary and contingent designations

- ☐ Coordinate with the trust distribution structure

- ☐ Avoid conflicting instructions

Beneficiary forms often control the trust language.

6️⃣ Transfer-on-Death (TOD) and Payable-on-Death (POD) Accounts

These accounts pass outside probate automatically.

However, if improperly structured, they may bypass your trust.

You must decide whether to:

• Leave them as direct transfers

• Align them with the trust

• Use them strategically for liquidity

7️⃣ Tangible Personal Property

Furniture, jewelry, artwork, firearms, collectibles, and household contents may be transferred via:

• General assignment document

• Personal property memorandum

• Specific schedule attached to trust

For most households, a general assignment of tangible personal property into the trust is sufficient.

8️⃣ Why Funding Matters

Your trust controls only what it owns.

If an asset remains in your individual name:

• It may require probate

• It may be distributed under state intestacy law

• It may trigger disputes

Funding is the bridge between planning and execution.

🔹 Funding Flow Summary

- Create and sign the trust

- Identify all assets

- Retitle real property

- Assign business interests

- Retitle financial accounts

- Coordinate beneficiary forms

- Execute the general assignment of personal property

Structure → Transfer → Confirm → Document

📥 Downloadable Funding Checklist (Single PDF)

To simplify implementation, we have created a consolidated Funding Checklist that includes:

• Real estate transfer steps

• LLC assignment documentation list

• Bank and brokerage retitling checklist

• Retirement beneficiary alignment review

• Personal property assignment guide

Download the complete Funding Checklist in the Membership Lab

SECTION VIII

Advanced Planning Considerations: Legal, Tax, and Structural Realities

A revocable living trust is a powerful estate planning tool. However, it does not operate in isolation. It must coordinate with your overall estate plan, financial accounts, beneficiary designations, and other legal documents.

The following considerations strengthen your trust structure and reduce the likelihood of probate court involvement, court supervision, unnecessary legal fees, or unintended asset distribution.

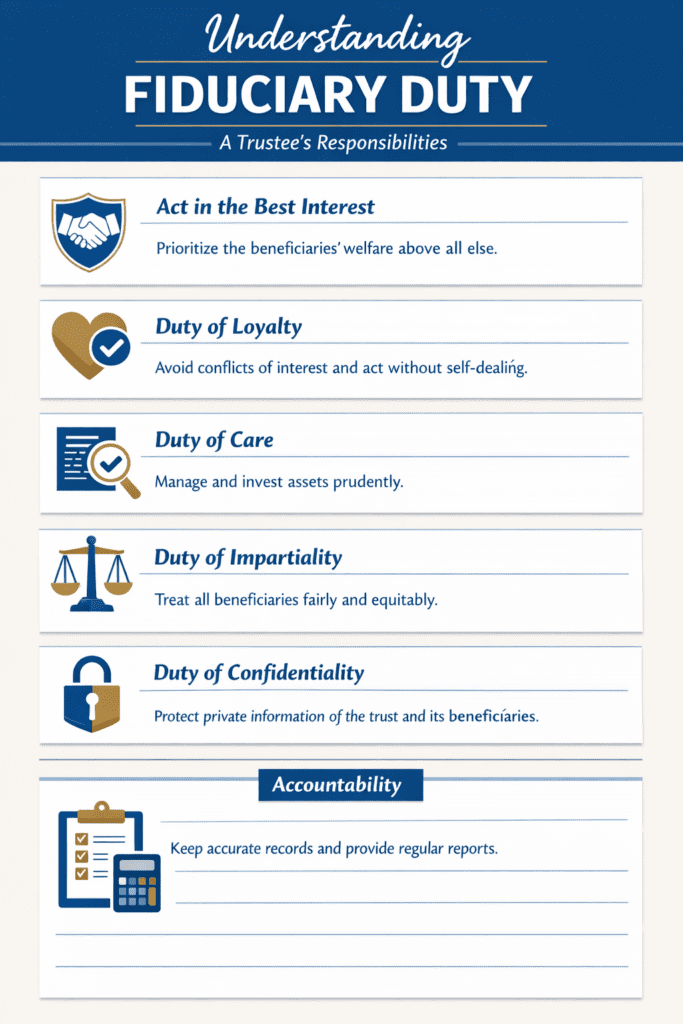

1. Fiduciary Duties of the Trustee

Every trustee — whether you are acting as your own trustee or you appoint a successor trustee — has fiduciary obligations.

A trustee must:

- Act solely for the benefit of the beneficiaries

- Preserve trust property

- Keep accurate records

- Avoid commingling assets

- Avoid self-dealing

- Follow the terms of the trust exactly as written

These duties apply whether the trustee is:

- A family member

- A professional trustee

- A trust company

- A professional fiduciary

Choosing the right trustee is an important step. The right trustee combines reliability, financial judgment, and the ability to manage sensitive family matters during difficult times.

2. Tax Reality of a Revocable Living Trust

A revocable living trust does not automatically reduce estate taxes.

Because you retain complete control during your lifetime:

- Trust assets remain part of your taxable estate

- Income from trust property is reported on your personal tax return

- Transfers into the trust are generally not taxable gifts

If tax efficiency or asset protection is a primary goal, irrevocable trusts may be considered in coordination with professional guidance.

A revocable trust is primarily about probate avoidance, continuity of management, and structured asset distribution — not tax advantages by itself.

3. When to Review and Update Your Trust

A revocable living trust should evolve with your life.

Review your trust document after:

- Marriage or divorce

- Birth or adoption of minor children

- Death of a beneficiary of the trust

- Acquisition of real estate or business interests

- Significant changes in your financial situation

- Changes in estate tax law

- Relocation to another state

Even modest estates benefit from periodic review. A trust agreement that is never updated may create additional costs, attorney fees, and probate proceedings later.

4. Minor Children and Structured Distributions

If you have minor children, the trust structure allows you to control how and when assets are distributed.

Rather than transferring assets outright at age 18, you may:

- Stage distributions at specific ages

- Authorize the successor trustee to distribute funds for education, housing, or health

- Maintain oversight of asset management during early adulthood

This provides peace of mind and protects family members from premature financial decisions.

5. Special Needs Planning

If a beneficiary has special needs, direct inheritance may affect eligibility for public benefits.

In these cases, trust agreements may incorporate subtrust provisions that preserve eligibility while providing financial support.

Proper drafting is critical in these situations and may require the professional services of attorneys.

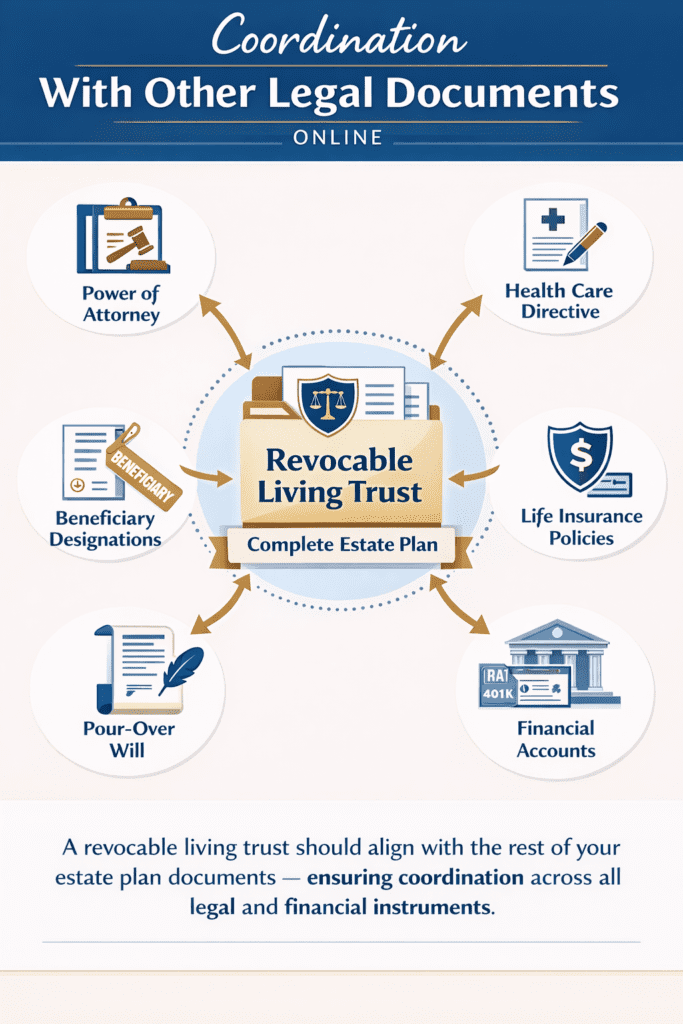

A revocable living trust works best when coordinated with your other legal and financial documents — including powers of attorney, health care directives, beneficiary designations, insurance policies, and financial accounts — forming a complete and aligned estate plan.

6. Coordination With Other Legal Documents

A revocable living trust should align with:

- Power of attorney documents

- Health care directives

- A pour-over will

- Beneficiary designations on retirement accounts

- Life insurance policies

- Financial accounts at each financial institution

Remember:

Beneficiary designations often override the terms of the trust if not properly aligned.

7. Business Interests and Asset Management

If you own business interests, those interests must be coordinated carefully.

Operating agreements should define:

- Transfer of assets upon death

- Buy-sell provisions

- Valuation methods

- Authority of trust administrators

The trust structure should complement — not conflict with — business agreements.

8. Privacy and Public Record

One significant advantage of a revocable living trust is privacy.

Unlike probate proceedings, which become part of the public record through court filings, a properly funded trust agreement remains private.

This protects sensitive information regarding:

- Trust assets

- Real property

- Personal property

- Financial accounts

- Family dynamics

9. The Limits of a Revocable Living Trust

It is important to understand what this type of trust does not do.

A revocable living trust:

- Does not eliminate legal process entirely

- Does not automatically reduce estate taxes

- Does not override improperly titled assets

- Does not replace professional guidance in complex cases

- Does not remove the need for proper funding

It is a more efficient way to manage asset distribution and probate avoidance, but it must be executed carefully.

A revocable living trust accomplishes many important objectives. It can help organize your estate, avoid probate, provide continuity in the event of incapacity, and ensure that your wishes are clearly documented and carried out.

However, it is not the same as a limited liability company (LLC), and it does not function as a legal shield against personal liability. During your lifetime, assets inside a revocable trust remain subject to your creditors because you retain complete control over them.

While a trust is certainly a legal document, its primary purpose is estate organization and structured asset distribution — allowing the law to help ensure your instructions are followed.

10. General Information Disclaimer

This guide is provided for general information purposes only and does not constitute legal advice.

Every financial situation is unique. Professional guidance from estate lawyers or estate planners may be appropriate depending on your specific needs.

SECTION IX

Common Mistakes When Creating a Revocable Living Trust

A revocable living trust is a powerful tool.

But like any legal document, its effectiveness depends on execution.

Most trust failures do not occur because the trust was invalid.

They occur because critical steps were overlooked.

Understanding common mistakes helps prevent unnecessary probate proceedings, court intervention, and additional legal fees.

1️⃣ Failing to Fund the Trust

This is the most common mistake.

Creating a trust document without transferring trust assets into it defeats the purpose of probate avoidance.

If real property, bank accounts, business interests, or financial accounts remain in your individual name, they may still be subject to probate court supervision.

A trust that is never funded is an incomplete estate planning tool.

2️⃣ Inconsistent Beneficiary Designations

Retirement accounts and life insurance policies pass according to beneficiary designations — not according to the trust agreement, unless the trust is properly named.

Common errors include:

• Naming the spouse individually but restructuring the trust differently

• Forgetting to update beneficiaries after divorce

• Naming minor children outright

• Leaving outdated designations in place

Beneficiary forms often override the terms of the trust.

3️⃣ Choosing the Wrong Successor Trustee

Many people choose the oldest child by default.

However, the right trustee is not determined by birth order.

The successor trustee must:

• Manage financial affairs

• Communicate clearly with family members

• Maintain records

• Follow detailed instructions

• Act impartially

A poor trustee choice can create more conflict than the probate process itself.

4️⃣ Ignoring State Law Differences

While trust structures are consistent nationwide, state laws vary regarding:

• Spousal elective share

• Community property vs common law

• Execution formalities

• Creditor rights

• Notice requirements

Relocating to another state without reviewing your trust may create unintended consequences.

5️⃣ Overlooking Business Interests

If you own:

• An LLC

• A closely held corporation

• Investment property partnerships

Failure to coordinate your trust with operating agreements and buy-sell provisions can create operational disputes.

Your trust should complement corporate documents — not override them.

6️⃣ Not Updating the Trust After Major Life Events

A revocable living trust is not a one-time document.

Common triggers for review include:

• Marriage or divorce

• Birth of minor children

• Death of a beneficiary

• Significant asset acquisition

• Sale of real estate

• Major changes in estate taxes

Outdated provisions can result in asset distribution that no longer reflects the grantor’s wishes.

7️⃣ Assuming a Revocable Trust Provides Asset Protection

A revocable trust does not generally protect assets from creditors during your lifetime because you retain complete control.

Individuals seeking asset protection must consider different legal structures, often including irrevocable trusts.

Confusing estate planning with asset protection is a frequent misunderstanding.

8️⃣ Failing to Communicate With Family Members

While the trust document itself should remain legally neutral, failing to explain major decisions can lead to:

• Suspicion

• Litigation

• No-contest challenges

• Emotional disputes

Clear communication — separate from the legal document — often preserves family harmony.

9️⃣ Treating the Trust as a Substitute for All Other Documents

A revocable living trust does not replace:

• A pour-over will

• Power of attorney

• Health care directive

• Business succession agreements

A trust is part of your estate plan — not the entire estate plan.

10️⃣ Improper Execution

Even the best trust structure can be undermined by failure to properly execute the document.

Execution requirements vary by state and may include:

• Notarization

• Witness signatures

• Proper dating

• Initialing certain pages

We will cover execution formalities in the next section.

Transition to Next Section

Now that you understand the structural mechanics and common mistakes, the next critical step is execution.

A trust becomes legally effective only after proper signing and formal validation.

SECTION X

Execution and Administration: Making Your Revocable Living Trust Legally Effective

Drafting a revocable living trust is an intellectual exercise.

Executing and administering it is a leadership decision.

A trust document does not become operational simply because it is written. It becomes legally effective only after proper execution, and it becomes functionally effective only after proper funding.

This section explains what transforms a written trust into a working legal structure.

1️⃣ Proper Execution Requirements

A revocable living trust becomes legally effective when:

• The trust agreement is signed by the grantor

• The signature is notarized (as required by state law)

• All required formalities are satisfied

While requirements vary by state, notarization is strongly recommended in virtually all jurisdictions because it:

• Confirms identity

• Reduces later challenges

• Strengthens evidentiary reliability

• Enhances institutional acceptance

Some states require witnesses. Others do not. Always confirm execution requirements for your state of residence.

2️⃣ The Difference Between “Valid” and “Functional”

A trust can be legally valid but practically ineffective.

A signed trust that has not been funded:

• Will not avoid probate

• Will not control untitled assets

• Will not function as intended

Funding is what activates probate avoidance.

Execution creates authority.

Funding creates effectiveness.

3️⃣ Trustee Authority During Life

If you serve as your own trustee:

• You retain complete control

• You may buy and sell real estate

• You may manage financial accounts

• You may write checks

• You may invest or liquidate trust property

Titling assets in the name of the trust does not limit your authority. It reorganizes it.

4️⃣ Successor Trustee Activation

Upon incapacity or death:

• The successor trustee derives authority from the trust document

• Court appointment is generally not required

• Probate court supervision may be avoided

However, that successor trustee must:

• Secure trust property

• Notify beneficiaries

• Obtain tax identification numbers

• Inventory trust assets

• Coordinate with financial institutions

• File tax returns

• Maintain fiduciary records

Administration is real work.

Which leads to one of the most important decisions in the entire planning process.

During the process of writing this guide, it became increasingly clear that choosing a successor trustee — the person who steps in after you and your spouse pass — can be one of the most stressful decisions in the entire estate planning process.

To remove emotion from the final decision, I created a structured evaluation tool that helps you compare candidates using objective criteria. The goal is to make the final selection based on facts, not pressure or tradition.

The last thing you want is to select the wrong person and unintentionally place unnecessary stress on them during an already difficult time.

This Successor Trustee Evaluation Tool is available exclusively to members inside the Membership Lab → Revocable Living Trust Section.

Case Study: Choosing the Right Successor Trustee

Mike and Christie were in the process of creating their first revocable living trust when they reached the decision point about selecting a successor trustee.

They had three adult children — Susan, Brian, and Josh — each with families of their own.

Susan was the oldest. She held a busy executive position and had strong business experience. Naturally, Mike and Christie leaned toward choosing her.

Just before finalizing the trust agreement, they had dinner with friends who had completed their own planning years earlier.

Their friends offered one simple suggestion:

“Don’t choose based on birth order. Choose based on defined factors.”

That advice changed everything.

Instead of relying on tradition or emotion, Mike and Christie evaluated each child objectively using structured criteria.

The Five Factors They Considered

1. Financial Literacy and Business Acumen

Administering a trust is not as simple as writing checks.

If the trust holds:

• Real estate investment properties

• Rental homes

• LLC interests

• Business assets

• Brokerage accounts

The successor trustee must understand:

• Tax implications

• Capital gains

• When to hire professionals

• How to value or liquidate assets

Competence matters.

2. Administrative Organization

A trustee is a fiduciary.

That means:

• Strict record-keeping

• Documented expenditures

• Formal accountings

• Timely tax filings

• Clear beneficiary communication

Disorganization can create liability.

3. Time and Availability

Trust administration can resemble a part-time job during the first year.

The trustee must:

• Secure property

• Sort tangible personal property

• Meet with advisors

• Handle paperwork

Bandwidth matters.

4. Geographic Proximity

Although digital management is possible, physical proximity helps when:

• Preparing real property for sale

• Managing maintenance

• Accessing safe deposit boxes

• Coordinating appraisals

A local trustee often operates more efficiently.

5. Personal Financial Stability

A successor trustee should be financially stable.

While trust assets are separate, financial distress may impair judgment.

Stability reduces risk.

The Outcome

After evaluating each child objectively:

• Susan remained capable but lacked availability

• Brian lived nearby and had schedule flexibility

• Josh was personable but historically disorganized

Mike and Christie selected Brian as successor trustee and named Susan as alternate.

More importantly, they explained their reasoning to all three children.

That transparency preserved family harmony.

The Structural Lesson

Selecting a successor trustee is not about hierarchy.

It is about:

• Competence

• Discipline

• Availability

• Stability

• Judgment

When you execute your trust, you are appointing someone to carry out your legal authority.

Choose carefully.

5️⃣ Certificate of Trust

After execution, financial institutions often request a Certificate of Trust.

This summary document confirms:

• Name of the trust

• Date of execution

• Identity of trustee

• Trustee authority

It does not reveal distribution terms.

This allows trustees to act without exposing sensitive provisions.

6️⃣ Safe Storage and Communication

Once executed:

• Store the original in a safe place

• Inform your successor trustee

• Provide location instructions

• Keep digital copies

A trust that cannot be located can cause unnecessary delay.

7️⃣ Coordination With Other Legal Documents

Execution should align with:

• A pour-over will

• Durable power of attorney

• Advance health care directive

• Beneficiary designations

• Life insurance policies

• Financial institution account titling

A revocable living trust works best as part of a complete estate plan — not as a standalone legal document.

8️⃣ Common Execution Errors

Avoid:

• Inconsistent trust names

• Missing notarization

• Unfunded real estate

• Unchanged beneficiary forms

• Failure to sign amendments properly

Formalities matter.

9️⃣ Emotional Leadership

Execution is more than a legal process.

It is an act of responsibility.

You are:

• Reducing probate proceedings

• Minimizing court intervention

• Protecting sensitive information

• Avoiding unnecessary legal fees

• Preserving peace of mind

No trust is perfect.

But a properly executed and funded trust significantly reduces friction during difficult times.

Final Reflection on Section X

A revocable living trust becomes powerful only when:

• Properly drafted

• Properly executed

• Properly funded

• Properly coordinated

• Properly communicated

Execution is not the end of planning.

It is the beginning of structure.

SECTION XI

Advanced Planning Considerations: Legal, Tax, and Structural Realities of a Revocable Living Trust

A revocable living trust is a powerful estate planning tool — but it is not a cure-all.

Understanding its legal boundaries, tax realities, and structural limitations is essential for creating a trust document that truly reflects your goals.

This section addresses the advanced considerations that thoughtful planners evaluate before finalizing their trust agreement.

1️⃣ Asset Protection During Your Lifetime

A revocable living trust does not protect trust assets from your personal creditors during your lifetime.

Because you retain complete control, the law treats trust property as though you still own it individually.

If you are sued, declare bankruptcy, or face creditor claims:

• Trust assets remain reachable

• Financial accounts inside the trust are not shielded

• Real property titled in the name of the trust remains exposed

Asset protection requires a different type of trust — typically an irrevocable trust — and must be structured carefully.

A revocable living trust is primarily a probate avoidance and management tool, not a creditor shield.

2️⃣ Estate Taxes and Federal Thresholds

Because the trust is revocable:

• Trust assets remain part of your taxable estate

• They are included in federal estate tax calculations

• They are subject to applicable state estate taxes where relevant

At the federal level, estate tax thresholds change over time. Most individuals fall below the federal exemption, but high-net-worth households should consider:

• Portability elections

• Marital deduction planning

• Bypass or credit shelter trusts

• Generation-skipping transfer tax implications

A revocable trust does not automatically reduce estate taxes.

Tax efficiency requires strategic planning beyond basic trust structure.

3️⃣ Income Tax Reporting

During your lifetime:

• A revocable trust typically uses your Social Security number

• Income is reported on your personal tax return

• There is no separate income tax filing requirement

After death:

• The trust becomes irrevocable

• It may require its own tax identification number

• Income distributed to beneficiaries may carry tax consequences

This transition from revocable to irrevocable status is an important structural shift.

4️⃣ Retirement Accounts and Beneficiary Designations

Retirement accounts — such as IRAs and 401(k)s — pass according to beneficiary designations, not according to your trust document unless the trust is named as beneficiary.

Important considerations:

• Naming your spouse directly often preserves favorable tax treatment

• Naming the trust as beneficiary may alter distribution timing

• The SECURE Act changed distribution rules for many beneficiaries

• Required minimum distribution rules apply differently depending on structure

Your trust should coordinate with beneficiary designations — not contradict them.

5️⃣ Life Insurance Policies

Life insurance policies also pass by beneficiary designation.

Options include:

• Naming an individual directly

• Naming the trust as beneficiary

• Creating an Irrevocable Life Insurance Trust (ILIT) for estate tax planning

If estate taxes are a concern, irrevocable trust structures may be more appropriate.

6️⃣ Business Interests and Operating Agreements

If you own:

• LLC interests

• Partnerships

• Closely held corporations

• Professional practices

Your trust must coordinate with:

• Operating agreements

• Buy-sell agreements

• Shareholder restrictions

• Transfer limitations

In some cases, the governing business agreement overrides the trust structure.

A well-drafted operating agreement is often more important than the trust when it comes to business succession.

7️⃣ Blended Families and Second Marriages

Revocable living trusts are particularly useful in blended families.

They allow you to:

• Provide income to a surviving spouse

• Preserve principal for children from a prior marriage

• Create staged distributions

• Avoid unintended disinheritance

Without careful drafting, however, ambiguity can create conflict.

Clarity in the terms of the trust prevents disputes.

8️⃣ Special Needs Beneficiaries

If a beneficiary receives government benefits:

• Direct inheritance may jeopardize eligibility

• Supplemental needs trusts may be required

• Distribution language must be carefully structured

A simple distribution clause may not be sufficient.

9️⃣ Multi-State Real Estate Ownership

If you own real property in multiple states:

• A revocable living trust may prevent multiple probate proceedings

• Each property must be properly retitled

• State-specific execution requirements must be satisfied

This is one of the most practical uses of a trust structure.

🔟 Limitations and Legal Reality

A revocable living trust:

✔ Avoids probate (when funded)

✔ Maintains privacy

✔ Provides incapacity planning

✔ Offers structured asset distribution

It does not:

✘ Eliminate taxes automatically

✘ Shield assets from personal creditors

✘ Replace all other estate planning documents

✘ Prevent family disputes without clear drafting

Understanding these boundaries strengthens your overall estate plan.

General Information Disclaimer

This section is provided for general information purposes only and does not constitute legal advice.

Trusts are governed by state and federal law. While many structural principles are consistent nationwide, specific execution requirements and statutory rules vary.

Consult professional services of attorneys or estate planners for guidance tailored to your financial situation and jurisdiction.

Section XII

State Laws Regulate Trusts — Why Probate Costs Vary Across the Country

A revocable living trust is governed primarily by state law. While the core structure of a trust is similar nationwide, probate procedures, court oversight, timelines, and fee structures vary significantly from state to state.

It is not practical to explain how every state differs. However, we can illustrate why many individuals consider a revocable living trust by looking at typical probate costs and timelines in selected states.

Example: Probate Costs and Timelines (Without a Trust)

| State | Typical Probate Fees | Average Timeline | Key Notes on RLT Benefits |

|---|---|---|---|

| California | $15,000–$40,000 (3–8%) | 12–18 months | High mandatory court and statutory attorney fees; significant savings from probate avoidance. |

| Florida | $10,000–$30,000 (2–6%) | 6–12 months | Circuit court delays common; revocable living trusts improve privacy and speed, especially for snowbirds. |

| New York | $20,000–$40,000 (4–8%) | 9–15 months | Surrogate’s Court oversight; strong benefits for multi-state asset owners. |

| Alabama | $500–$5,000 (<2%) | 6–12 months | Streamlined process for simple estates; trusts often used for incapacity planning rather than cost avoidance. |