Estate planning can feel complicated. Taxes can feel intimidating. When you combine the two, it’s easy to assume that a Revocable Living Trust must provide major tax advantages.

In most cases — it does not.

- 1. The Big Myth: “A Revocable Living Trust Saves Taxes.”

- 2. So Why Do People Create Revocable Living Trusts?

- 3. What About Estate Taxes?

- 4. When Does a Trust Pay Its Own Taxes?

- 5. Step-Up in Basis: A Hidden Benefit

- Case Study: When the Successor Trustee Meets Reality

- The CPA’s Explanation

- The Practical Lessons

- What This Means for Readers

- 6. Income-Producing Assets Inside a Trust

- 7. What a Revocable Living Trust Does NOT Protect You From

- 8. What Happens to Debts When the Grantor of a Revocable Living Trust Dies?

- 1️⃣ The Duty to Notify Creditors

- Example: Mississippi

- 2️⃣ The Statutory Clock Starts Running

- 3️⃣ Validating and Settling Claims

- Valid Debts

- Invalid or Questionable Claims

- 4️⃣ Encumbered Property (Mortgages & Liens)

- 5️⃣ The Danger of Distributing Assets Too Early

- Beneficiary Liability

- Trustee Personal Liability

- Practical Takeaway

- 9. State Taxes and Trusts

- 10. Business Owners and Trusts

- 11. When You Absolutely Need Professional Guidance

- 11. Business Tax Treatment: When a Revocable Living Trust Owns a Business Interest

- 1️⃣ Step-Up in Basis (Capital Gains Impact)

- 2️⃣ LLC or Partnership Considerations (Section 754 Election)

- 3️⃣ Estate Tax Consequences

- 4️⃣ Buy-Sell Agreement Considerations

- 5️⃣ Fiduciary Responsibility of the Trustee

- Practical Takeaway

- 12. Practical Takeaway for Most Families

- 12. Where RetireCoast Fits In

- Final Thought

At RetireCoast, our goal is practical clarity. Whether you’re retired on the Mississippi Gulf Coast, planning your next chapter, or part of our Millennial Financial Lab community building early, this article will explain:

- What a revocable living trust does

- What it does not do for taxes

- When taxes actually become relevant

- Where advanced planning can make a difference

This is educational content — not legal or tax advice — but it will help you walk into a conversation with a CPA or attorney prepared.

This article is part of our Estate Planning series specifically the Revocable Living Trust which can be created by members in our Millennial Financial Lab. Want more information read this article: https://retirecoast.com/revocable-living-trust-master-guide/

1. The Big Myth: “A Revocable Living Trust Saves Taxes.”

Let’s address the most common misunderstanding first.

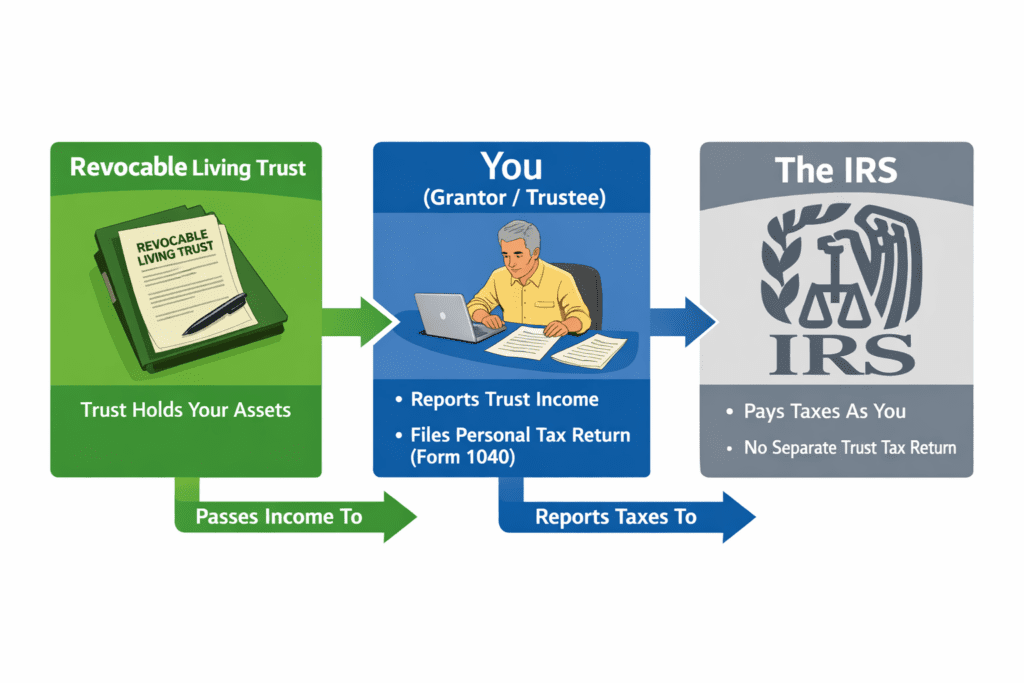

A revocable living trust does not reduce your income taxes.

It does not reduce capital gains taxes during your lifetime.

It does not eliminate estate taxes for most Americans.

Why?

Because while you are alive and serving as trustee, the IRS treats your revocable trust as you.

It is called a “grantor trust.”

You still:

- Use your Social Security number

- File your normal Form 1040

- Report income exactly as before

From a federal income tax standpoint, nothing changes.

Additional reading on asset protection: https://retirecoast.com/great-wealth-transfer-baby-boomers/

2. So Why Do People Create Revocable Living Trusts?

Because tax savings is not the primary purpose.

The real benefits are:

- Avoiding probate

- Maintaining privacy

- Planning for incapacity

- Controlling how assets pass to heirs

- Providing smoother asset management

Probate avoidance is often the biggest practical advantage, especially in states where court processes can be slow or expensive.

For example, in Mississippi, probate is not impossible — but it still requires court filings, public records, and delays. A properly funded trust can avoid that entirely.

3. What About Estate Taxes?

Here’s where reality helps calm anxiety.

The federal estate tax exemption is very high. As of current law, it is in the multi-million-dollar range per person. Most retirees and families will never owe federal estate tax.

However, very high-net-worth households may need additional planning beyond a basic revocable trust.

Advanced techniques might include:

- Irrevocable trusts

- Credit shelter (bypass) trust structures

- Charitable remainder trusts

- Generation-skipping trusts

Those are separate strategies — not the simple revocable trust most families use.

At the federal level, the estate tax exemption is very high. Most families will never owe federal estate tax.

However, several states impose their own estate or inheritance taxes, and the exemption amounts are often much lower than the federal threshold.

States That Impose Estate or Inheritance Taxes (2026)

| State | 2026 Exemption Limit | Tax Rate |

|---|---|---|

| Connecticut | $15,000,000 | 12% |

| District of Columbia | $4,988,400 | 11.2% – 16% |

| Hawaii | $5,490,000 | 10% – 20% |

| Illinois | $4,000,000 | 0.8% – 16% |

| Maine | $7,000,000 | 8% – 12% |

| Maryland | $5,000,000 | 0.8% – 16% |

| Massachusetts | $2,000,000 | 5.6% – 16% |

| Minnesota | $3,000,000 | 13% – 16% |

| New York | $7,350,000 | 3.06% – 16%* |

| Oregon | $1,000,000 | 10% – 16% |

| Rhode Island | ~$1,802,431 | 0.8% – 16% |

| Vermont | $5,000,000 | 16% |

| Washington | $2,193,000 | 10% – 20% |

*New York includes a “cliff” rule where exceeding the exemption by more than a small margin can cause the entire estate to become taxable.

Why This Matters for Trust Planning

A revocable living trust does not eliminate state estate taxes.

If you live in — or own property in — one of these states, additional planning strategies may be necessary if your estate approaches the exemption level.

Those strategies could include:

- Credit shelter (bypass) trust structures

- Lifetime gifting strategies

- Irrevocable trusts

- Charitable planning

For readers relocating to the Mississippi Gulf Coast: Mississippi currently does not impose a state estate tax, which is one reason some retirees consider lower-tax states when planning long-term wealth transfer.

The key takeaway:

A revocable living trust simplifies administration — but it is not, by itself, a state estate tax avoidance strategy. If you have a large estate, you may want to look at your state tax laws and consider relocating so your heirs can keep more of your estate.

4. When Does a Trust Pay Its Own Taxes?

A revocable trust only becomes a separate tax entity after death.

At that point:

- It receives its own EIN (federal tax Id number)

- It may need to file an IRS Form 1041

- Income retained in the trust can be taxed at trust tax rates

And here is something important:

Trust tax brackets are compressed.

Trusts reach the highest federal tax bracket at much lower income levels than individuals. That’s why trustees often distribute income to beneficiaries rather than retain it — because beneficiaries may be in lower tax brackets.

This is one area where working with a CPA is extremely valuable.

Federal Trust Tax rates 2026

| Tax Rate | Taxable Income Bracket |

| 10% | $0 to $3,300 |

| 24% | $3,301 to $11,700 |

| 35% | $11,701 to $16,000 |

| 37% | $16,001 or more |

5. Step-Up in Basis: A Hidden Benefit

One powerful tax concept many people overlook is the step-up in basis.

When assets pass through a revocable living trust at death:

- Real estate

- Stocks

- Mutual funds

They typically receive a step-up in basis to fair market value at the date of death.

This can dramatically reduce capital gains taxes if heirs sell the asset.

Example:

- You bought property for $100,000

- It is worth $400,000 when you pass

- Your heirs inherit it at $400,000 basis

If they sell immediately, there may be little or no capital gain.

This benefit applies whether assets pass via a will or a trust — but trusts help streamline the transfer.

Case Study: When the Successor Trustee Meets Reality

Pamela Steps Into the Role

Pamela recently became the successor trustee of her parents’ revocable living trust after both parents passed away.

The trust directed that:

- Pamela and her two brothers would inherit everything equally.

- The estate included:

- The parents’ primary residence

- Two income-producing rental properties

- Bank and brokerage accounts

The siblings assumed the trust would “handle everything automatically.”

It didn’t.

They had questions:

- Do we owe estate tax?

- Do we owe income tax?

- What happens if we sell the properties?

- Does the trust pay the tax — or do we?

So they scheduled a meeting with their parents’ longtime CPA.

The CPA’s Explanation

The CPA began with a simple clarification:

“The revocable living trust avoided probate. It did not eliminate taxes.”

Then he walked them through the situation step by step.

1️⃣ Federal Estate Tax

The total estate value was well below the federal estate tax exemption.

Result:

No federal estate tax owed.

The siblings were relieved.

2️⃣ State Estate Tax

Their parents lived in a state that did not impose a state estate tax.

Result:

No state-level estate tax owed.

The trust itself did not create tax savings — but it didn’t create new tax problems either.

3️⃣ Step-Up in Basis (The Big Advantage)

Here’s where things got interesting.

The CPA explained the concept of step-up in basis:

- The parents purchased the primary home decades ago for $120,000.

- It was now worth $620,000.

- The two rental properties were purchased for a combined $300,000.

- They were now worth $900,000 combined.

Because the assets passed at death:

- All three properties received a new tax basis equal to fair market value at the date of death.

That means:

If the siblings sold immediately:

- Little to no capital gains tax would be owed.

Pamela realized this was a significant tax advantage — but it had nothing to do with the trust structure itself. It was triggered by the parents’ death.

4️⃣ Rental Income After Death

The CPA then explained something they had not considered.

The trust became an irrevocable trust upon death.

- The trust now needed its own EIN.

- It must file Form 1041.

- Rental income earned after death must be reported.

And here’s the key issue:

Trust tax brackets are compressed.

If the trust retained income, it could quickly hit higher tax rates.

The CPA recommended:

- Either distributing income to the siblings annually (so they report it personally),

- Or transferring the rental properties out of the trust into three equal ownership interests.

5️⃣ Sell or Hold?

The siblings now had strategic decisions to make:

Option A: Sell everything

- Capture stepped-up basis

- Divide proceeds

- Eliminate landlord responsibilities

Option B: Keep rentals

- Continue earning income

- Coordinate management

- Track trust-level reporting

Option C: One sibling buys out the others

- Use appraised values

- Avoid outside sale

- Simplify long-term ownership

The trust document gave Pamela authority to sell, but she understood her fiduciary duty: act in the best interest of all beneficiaries.

The Practical Lessons

Pamela left the CPA’s office with clarity:

- The trust avoided probate — which saved time and preserved privacy.

- It did not eliminate taxes.

- The step-up in basis was the most powerful tax benefit.

- Income earned after death required new reporting.

- Strategic decisions mattered more than the document itself.

What This Means for Readers

If you name a successor trustee:

- That person will have real responsibilities.

- They must understand tax reporting.

- They must obtain professional guidance.

If you are creating your own trust:

- Make sure your heirs know who your CPA is.

- Keep organized records.

- Understand that tax planning is separate from probate planning.

Final Thought

Pamela initially believed the trust was a “tax shelter.”

It wasn’t.

It was an administrative tool.

The real tax implications came from:

- Federal exemption thresholds

- State rules

- Step-up in basis

- Post-death income reporting

The trust created order.

Professional advice created a strategy.

And that distinction made all the difference.

6. Income-Producing Assets Inside a Trust

If you place rental properties, dividend stocks, or businesses into your revocable trust:

- You still report income normally during your lifetime

- Depreciation continues

- Deductions remain available

The trust does not disrupt your tax structure.

For those of you building rental income portfolios — especially along the Mississippi Gulf Coast — this is reassuring. Your estate plan does not interfere with your income strategy.

7. What a Revocable Living Trust Does NOT Protect You From

Let’s be clear about limitations:

A revocable living trust does not:

- Protect assets from creditors during your lifetime

- Shield assets from lawsuits

- Eliminate Medicaid look-back rules

- Provide asset protection

Because you control the trust, creditors can reach the assets.

If asset protection is the goal, that’s a separate discussion involving irrevocable structures.

- Avoids Probate: Assets titled in the trust transfer without court supervision, saving time and maintaining privacy.

- Maintains Privacy: Unlike a will, the trust document generally does not become a public court record.

- Prevents Administrative Delays: The successor trustee can act immediately—paying bills, managing property, and preserving value.

- Protects Minor or Vulnerable Beneficiaries: You can control timing and conditions of distributions rather than issuing one lump sum.

- Reduces Family Conflict: Clear written instructions minimize disagreements between heirs.

- Preserves Real Estate Continuity: Homes and rental properties can be managed, rented, or sold without waiting on probate court approval.

- Creates Structured Distribution: Assets can be staggered over time instead of distributed all at once.

8. What Happens to Debts When the Grantor of a Revocable Living Trust Dies?

When the creator (grantor) of a revocable living trust passes away, the trust immediately becomes irrevocable.

However, one of the most common misconceptions in estate planning is this:

A living trust does not shield assets from the deceased person’s creditors.

Assets held in the trust remain legally liable for the grantor’s outstanding debts.

If you are named as successor trustee — perhaps an adult child stepping into that role — you assume a strict fiduciary duty. Before any inheritances are distributed, you must properly address creditors.

Here is how the process works.

1️⃣ The Duty to Notify Creditors

A successor trustee cannot ignore debts or “wait and see” if creditors reach out.

They are legally responsible for:

- Identifying known creditors

- Providing formal notice

- Protecting the trust from long-term liability

To limit future claims, trustees typically initiate a formal notification process.

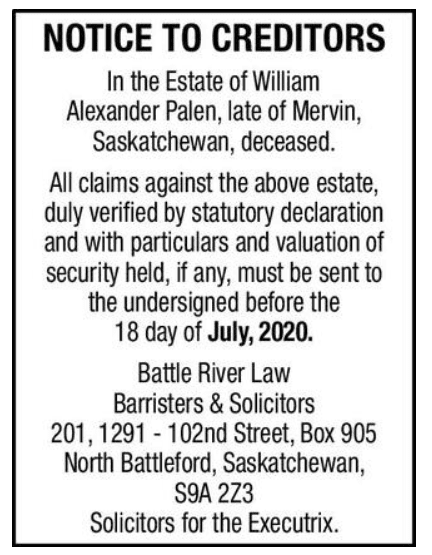

Example: Mississippi

In Mississippi, a trustee may:

- Publish a “Notice to Creditors” in a local newspaper for three consecutive weeks

- Mail a written notice to known creditors

This formal notice triggers important legal protections.

2️⃣ The Statutory Clock Starts Running

Once proper notice is published, a strict statutory clock begins.

Using Mississippi as an example:

- Creditors have 90 days from the date of first publication to submit a formal written claim.

- If they fail to do so within that window, their claim is generally barred permanently.

That means they lose the legal right to collect.

This is one of the most important risk-management tools available to a trustee.

3️⃣ Validating and Settling Claims

When creditors submit claims, the trustee must review each one carefully.

Valid Debts

If the claim is legitimate — such as:

- Medical bills

- Credit cards

- Personal loans

- Final income taxes

The trustee must pay those debts using trust assets.

If the trust has limited cash but substantial property, the trustee may need to:

- Sell investment accounts

- Liquidate vehicles

- Sell real estate

The trustee not only has the authority to do this — they have the legal obligation.

Invalid or Questionable Claims

The trustee is not required to blindly pay every demand.

They may reject:

- Undocumented claims

- Expired debts

- Incorrect billing amounts

If rejected, the creditor must file a lawsuit within a short statutory period to pursue collection.

This protects the trust from improper payouts.

4️⃣ Encumbered Property (Mortgages & Liens)

If the trust holds real estate with:

- Mortgages

- Tax liens

- Judgment liens

Those secured debts remain attached to the property.

The trustee must coordinate with the lender to:

- Pay off the loan from liquid trust assets

- Sell the property and satisfy the debt at closing

- Distribute the property to beneficiaries subject to the existing loan

A mortgage does not disappear at death simply because the property sits inside a trust.

5️⃣ The Danger of Distributing Assets Too Early

This is where trustees often make serious mistakes.

If a successor trustee distributes money or property before:

- Settling debts

- Waiting for the creditor claim period to expire

They expose themselves — and the beneficiaries — to legal risk.

Beneficiary Liability

Creditors may:

- Sue beneficiaries directly

- Recover funds up to the value of what was inherited

Trustee Personal Liability

Even more serious:

A creditor can sue the trustee personally for breach of fiduciary duty if the trustee failed to properly settle valid debts before distributing assets.

Serving as a trustee is not ceremonial. It is a legal responsibility.

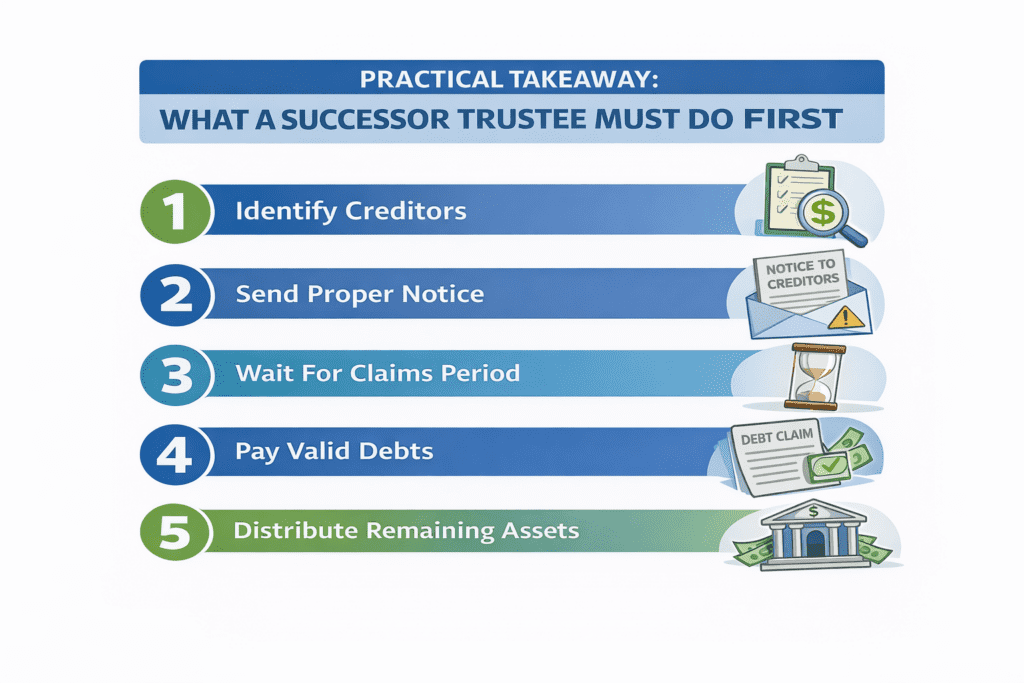

Practical Takeaway

A revocable living trust:

- Avoids probate

- Maintains privacy

- Streamlines administration

But it does not eliminate the grantor’s debts.

After death, the trustee must:

- Identify creditors

- Initiate formal notice

- Wait for the statutory claim period

- Pay valid debts

- Only then distribute remaining assets

For families and successor trustees, working with an experienced CPA and estate attorney during this phase is often essential.

The trust creates structure.

Proper administration creates protection.

And timing creates safety.

9. State Taxes and Trusts

Some states impose estate or inheritance taxes. Others do not.

Mississippi does not currently have a state estate tax.

However, if you own property in multiple states, additional considerations may apply.

For families relocating from high-tax states to more tax-friendly regions, trust planning can simplify multi-state asset transfers — but again, the trust itself is not a tax shelter.

10. Business Owners and Trusts

If you own:

- An LLC

- A small business

- Investment partnerships

Your membership interests can typically be assigned to your revocable trust.

This does not change how the business is taxed.

However, it can:

- Avoid probate on ownership interests

- Provide continuity if you become incapacitated

- Support business succession planning

For retirees starting businesses in their second act — something we discuss often at RetireCoast — coordinating your operating agreement with your trust is critical.

11. When You Absolutely Need Professional Guidance

You should consult a CPA or attorney if:

- Your estate approaches federal exemption thresholds

- You own property in multiple states

- You have blended family issues

- You have special needs beneficiaries

- You want Medicaid planning strategies

- You operate complex businesses

Walking into that meeting informed will save you time and money.

Arriving prepared — with draft documents and clarity — reduces billable hours dramatically. Members can use our tools to organize and plan before any meetings with professional advisors. Consider your meeting more of a review of what you have created. Saves time and money.

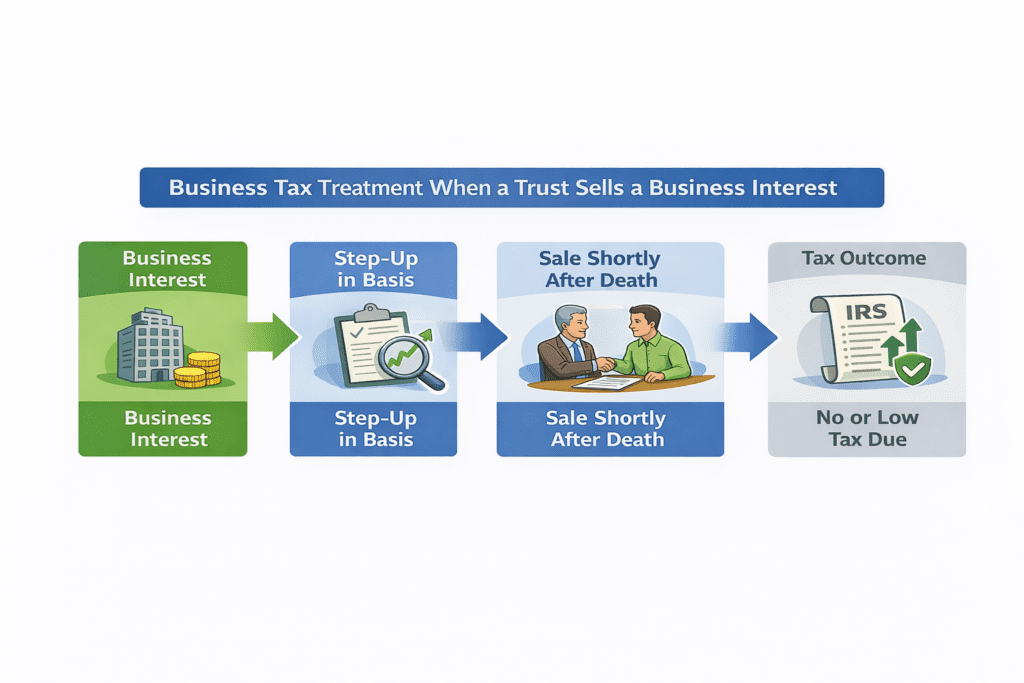

11. Business Tax Treatment: When a Revocable Living Trust Owns a Business Interest

Case Example: Joe’s 1/3 Ownership Interest

Joe owned one-third of a company. During his lifetime, he assigned that ownership interest to his revocable living trust.

Important point:

Because the trust was revocable, the IRS treated Joe as the owner during his lifetime. Nothing changed for income tax purposes while he was alive.

When Joe passed away:

- The trust became irrevocable.

- His 1/3 business interest became part of his gross estate.

- The successor trustee stepped in.

Shortly afterward, the other two owners offered to buy out Joe’s ownership interest from the trustee for cash.

Here are the tax consequences that follow.

1️⃣ Step-Up in Basis (Capital Gains Impact)

This is the single most important tax factor.

Under federal law, assets included in a decedent’s estate receive a step-up in basis to fair market value (FMV) on the date of death.

What That Means

If Joe originally invested $50,000 decades ago and the 1/3 interest was worth $900,000 at death:

- The old $50,000 basis disappears.

- The trust’s new tax basis becomes $900,000 (date-of-death value).

If the trustee sells the interest for $900,000 shortly after death:

- There is no capital gain.

- No income tax is due on decades of appreciation.

If it sells later for $950,000:

- Only the $50,000 increase after death is taxable.

The appreciation during Joe’s lifetime is erased for income tax purposes.

2️⃣ LLC or Partnership Considerations (Section 754 Election)

If the business is structured as:

- An LLC taxed as a partnership

- A partnership

There may be additional complexity.

Even though the trust receives a stepped-up “outside basis,” the company’s internal asset basis may not automatically adjust.

This can create unexpected ordinary income exposure if the company holds:

- Depreciated equipment

- Unrealized receivables

- “Hot assets”

The Protection Mechanism

The company may elect under Internal Revenue Code Section 754 to adjust its internal basis to align with Joe’s stepped-up ownership interest.

If properly handled:

- The trust avoids unexpected ordinary income taxation.

- The buyout becomes tax-neutral at FMV.

This is a technical area where a CPA familiar with partnership taxation is essential.

3️⃣ Estate Tax Consequences

While income tax may be minimized, estate tax is a separate issue.

The full appraised value of Joe’s 1/3 interest is included in his gross estate.

The trustee must:

- Add the business value

- Add all other trust and non-trust assets

- Compare the total to federal and state exemption thresholds

If the estate exceeds the exemption:

- Federal estate tax (currently up to 40%) may apply.

- Some states impose separate estate or inheritance taxes.

Often, the cash from the buyout is used to satisfy any estate tax obligation.

4️⃣ Buy-Sell Agreement Considerations

If the company had a buy-sell agreement:

- The agreement may dictate valuation methodology.

- It may restrict transfer.

- It may fix the price or require an appraisal.

If properly structured, a buy-sell agreement can:

- Provide liquidity at death

- Prevent disputes

- Support defensible valuation for estate tax purposes

If no agreement exists, the trustee must negotiate carefully while honoring fiduciary duties to beneficiaries.

5️⃣ Fiduciary Responsibility of the Trustee

The successor trustee must:

- Obtain a formal valuation of the business interest

- Confirm compliance with any operating or shareholder agreement

- Evaluate tax consequences before signing the sale documents

- Ensure sale terms are fair to all beneficiaries

The trustee cannot simply accept the first offer if it undervalues the interest.

They have a duty to maximize value for the estate.

Practical Takeaway

When a business interest is owned by a revocable living trust:

- During life: no tax change.

- At death: step-up in basis applies.

- On sale shortly after death: little or no capital gains tax.

- Estate tax may still apply depending on the total estate size.

- Partnership structures require special attention to Section 754 elections.

The trust itself does not create the tax benefit.

The step-up in basis does.

And careful coordination between the trustee, CPA, and business partners ensures that the buyout proceeds smoothly and tax-efficiently.

12. Practical Takeaway for Most Families

For the majority of readers:

A revocable living trust is about:

- Control

- Simplicity

- Privacy

- Probate avoidance

- Smoother transfer to heirs

It is not primarily about tax savings.

And that’s perfectly fine.

Good planning is not about clever tricks. It’s about reducing friction for your family during difficult moments.

12. Where RetireCoast Fits In

We do not provide legal advice.

What we provide is education and structured tools that help you:

- Think clearly

- Organize your information

- Understand terminology

- Draft preliminary documents

- Prepare for professional review

When you walk into an attorney’s office already organized, the conversation becomes review — not discovery.

That alone can significantly reduce costs.

Final Thought

Taxes and trusts intersect — but not in the way many people assume.

A revocable living trust is not a magic tax solution.

It is a planning framework.

Used correctly, it simplifies administration, preserves privacy, and positions your family for smoother transitions.

IRS references to Step-up

And that is often far more valuable than a tax deduction.IRS Publication 551 (Basis of Assets)

This is the primary, comprehensive IRS publication that covers how to calculate the tax basis for all types of assets, including those that are inherited through an estate or trust.

Link: https://www.irs.gov/publications/p551

Where to look: Scroll down to the “Basis Other Than Cost” section, and then look for the subsection specifically titled “Inherited Property.” ### 2. IRS FAQ: Gifts & Inheritances If you want a quicker, more direct summary of how the basis resets to the Fair Market Value (FMV) on the date of death, the IRS has a dedicated FAQ page that answers whether money received from the sale of inherited property is taxable.

Link: https://www.irs.gov/faqs/interest-dividends-other-types-of-income/gifts-inheritances/gifts-inheritances

Note on Recent IRS Updates: The IRS recently finalized new rules regarding “consistent basis reporting” under Section 1014(f). This means the step-up basis the trust or the heirs claim when selling the business interest must exactly match the final valuation reported on the decedent’s official estate tax return. Publication 551 includes these new regulatory updates.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}