Where to Invest First — Priority Planner

A “next dollar” decision flow built for Millennials. Enter your basics and get a prioritized checklist with monthly next steps.

Disclosure: RetireCoast does not provide investment, tax, or legal advice. This tool is educational and uses general rules-of-thumb.

For personalized advice, consider speaking with a qualified financial professional.

Inputs

Keep it simple. You can refine later—this is meant to give you a clean order-of-operations.

FAQ

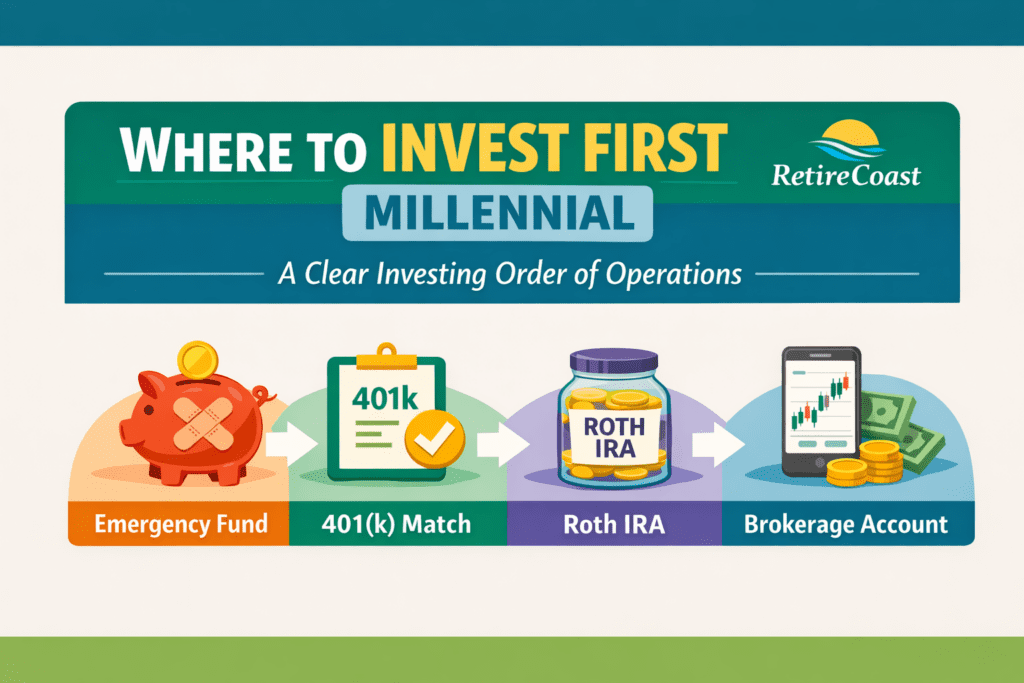

Why does emergency savings come first?

Because a small cash buffer prevents new debt when life happens. It protects your investing plan from being interrupted.

Is a 401(k) match really “free money”?

Generally, yes—if you contribute enough to receive the match, you’re getting additional compensation from your employer.

When does a Roth IRA beat a brokerage account?

Often when your goal is retirement and you want tax-free qualified withdrawals later. A brokerage can be better for near-term goals like a down payment.

How much emergency fund should I target?

A common rule is 3–6 months of essentials. If your income is variable (commission, tips, freelance), lean higher.

How often should I rebalance?

Many people use every 6–12 months, or when allocations drift by ~5 percentage points.

The Millennial Hub: A Practical Financial Literacy Master Class

The Millennial Hub isn’t a single article—it’s a growing collection of companion guides that work together.

When read as a series, these articles are equivalent to a real-world master class in financial literacy,

covering cash flow, taxes, debt, saving, long-term planning, and decision-making most people were never taught.

Each article stands on its own, but the real value comes from combining them.

Concepts introduced in one guide are reinforced and expanded in others—helping you connect the dots

between daily money decisions and long-term outcomes.

Example of a Core Companion Article

Taxes & Long-Term Impact

— This article shows how tax policy, deductions, and long-term planning decisions quietly shape

your financial future, reinforcing why cash flow awareness and informed choices matter over decades.

Tip: Start with cash flow and budgeting articles, then layer in taxes, credit, and long-term planning.

Financial literacy builds best when concepts are learned in context—not isolation.