Introduction: Why Proper Classification Is Critical for Business Owners

Hiring workers is one of the most important business decisions you will make—but it is also one of the easiest places to make costly mistakes. Do you hiring employees vs contractors?

Many business owners assume that labeling someone as an independent contractor is enough to avoid employee benefits, payroll taxes, and compliance requirements. Under rules enforced by the Internal Revenue Service and the U.S. Department of Labor, that assumption can lead to severe penalties.

- Introduction: Why Proper Classification Is Critical for Business Owners

- What Is an Employee vs Independent Contractor? (Federal Law Explained)

- When a Contractor Refuses to Provide a TIN (Form 1099-NEC Compliance Rules)

- Backup Withholding: The Most Critical Step

- How to Avoid Penalties: Document Everything

- Why Employee Misclassification Leads to Severe Penalties

- State Regulations: Where Classification Gets More Complex

- Hiring “Persons in the United States Illegally”

- Case Study: When Things Go Wrong

- 1099 Compliance: The Law Applies to Everyone

- Use the Free Classification Tool

- How to Protect Yourself (Best Practices System)

- Case Study: Doing It Right

- Key Takeaways

- Next Step: Build Your Compliance System

- FAQ

The issue comes down to proper classification.

If a worker is misclassified:

- You may owe back taxes, including Social Security and Medicare taxes

- You may face financial penalties, legal fees, and audits

- You may be liable for back wages, minimum wage, and overtime under the Fair Labor Standards Act

This applies whether you are:

- A company with full-time employees

- A small business owner

- A real estate investor hiring contractors

- An individual paying someone for work

➡️ The key takeaway: Worker classification is based on the relationship—not what you call it

📞 Need Help Right Now?

- IRS Business Help: 800-829-4933

- DOL Wage & Hour: 866-4US-WAGE

- E-Verify Assistance: Available through USCIS website

If you are unsure about classification, it is far better to ask questions now than to deal with penalties later.

⚠️ When in doubt, verify before you hire.

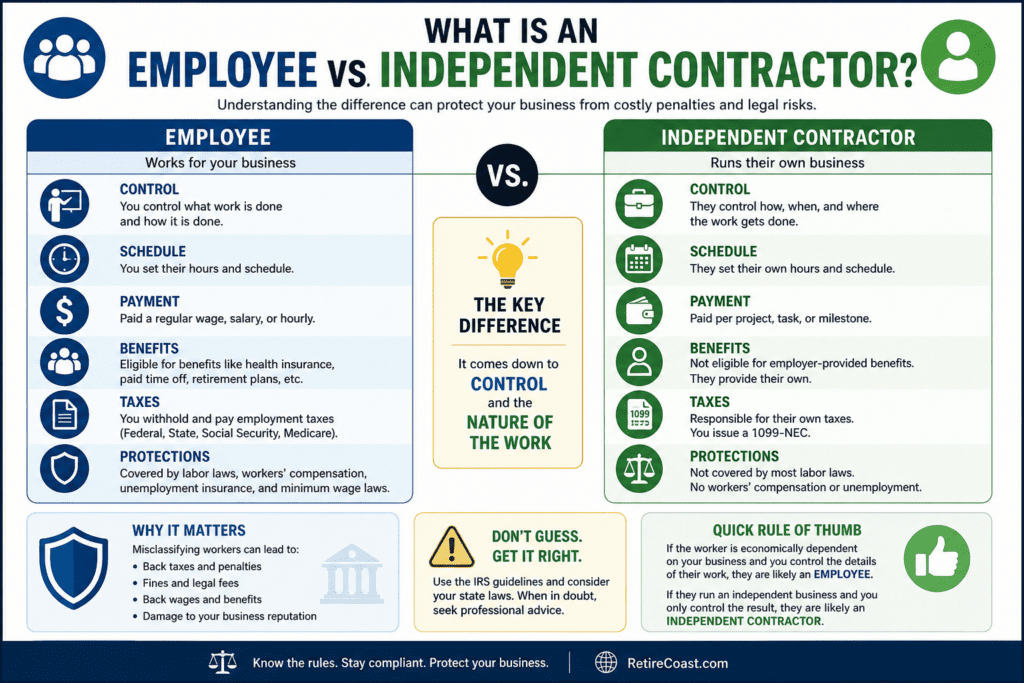

What Is an Employee vs Independent Contractor? (Federal Law Explained)

Under federal law, determining a worker’s status depends on the level of control and the economic realities of the relationship.

IRS Guidelines: The Control Test

The Internal Revenue Service https://www.irs.gov/businesses applies a version of the common law test, focusing on three main categories:

1. Behavioral Control

- Who controls the work schedule?

- Who determines how the job is performed?

- Is training provided?

➡️ More control = Employee

2. Financial Control Factors

- Who makes a significant investment in tools?

- Does the worker have an independent business?

- Can the worker earn a profit or loss?

➡️ More independence = Contractor

3. Type of Relationship

- Is there a written contract?

- Are employee benefits like health insurance provided?

- Is the relationship ongoing?

➡️ Long-term employment relationship = Employee

⚠️ Important Rule

There is no single factor that determines worker classification.

Instead, agencies look at:

- The degree of control

- The entire employment relationship

- The specific circumstances

🧠 Not Sure If Your Worker Is an Employee or Contractor?

Don’t guess—and don’t risk costly mistakes. Use our free tool to evaluate behavioral control, financial control factors, and the type of relationship based on IRS guidelines.

- ✔ Identify employee misclassification risk

- ✔ Understand IRS and state law factors

- ✔ Get a clear classification recommendation

- ✔ Avoid back taxes, penalties, and audits

Make informed business decisions and protect yourself before you hire.

📄 1099 Compliance: Key Takeaways

- $2,000+ Paid: You are generally required to issue a 1099 and report to the IRS.

- Under $2,000: Classification laws still apply — this is NOT a safe harbor.

- 1099 ≠ Contractor: Filing a 1099 does not legally make someone an independent contractor.

- Individuals Included: Homeowners and individuals hiring workers are not exempt.

- State Rules Apply: Some states have different thresholds and additional reporting requirements.

⚠️ If you misclassify a worker, issuing a 1099 will not protect you from penalties.

Department of Labor: Economic Reality Test

The U.S. Department of Labor uses the economic reality test:

- Is the worker economically dependent on you?

- Or are they truly self-employed individuals operating their own business?

This test often expands beyond IRS rules and focuses on:

- Worker rights

- Wage and hour laws

- Fair compensation

⚠️ Missing TIN? You Still Have Legal Obligations

- $600+ Paid: You must still file Form 1099-NEC.

- No TIN Provided: Leave the field blank—do NOT use fake numbers.

- Backup Withholding: You must withhold 24% from future payments.

- Your Risk: Failure to withhold can make YOU liable for unpaid taxes.

- Documentation: Keep all W-9 requests to prove compliance.

📌 If a contractor refuses to provide a TIN, that is a major red flag—proceed with caution.

When a Contractor Refuses to Provide a TIN (Form 1099-NEC Compliance Rules)

One of the most overlooked compliance risks for business owners occurs when a contractor fails—or refuses—to provide a Taxpayer Identification Number (TIN).

A TIN is typically:

- A Social Security Number (SSN), or

- An Employer Identification Number (EIN)

Even without this information, the Internal Revenue Service still requires you to follow strict reporting rules.

You Must Still File Form 1099-NEC

If you paid a contractor $600 or more during the tax year, you are required to file Form 1099-NEC—even if you do not have their TIN.

✔ Filing Requirements:

- File by the deadline (typically January 31)

- Leave the TIN field blank (do NOT enter dummy numbers)

- Complete all other fields:

- Name

- Address (if known)

- Total amount paid (Box 1)

➡️ Filing late or incorrectly increases your exposure to penalties.

🎧 Author Insight: Employee vs Contractor Decisions That Matter

In this short audio, we focus on one of the most important business decisions you will make—determining whether someone is truly an employee or an independent contractor. We also cover a critical compliance issue many overlook: obtaining a contractor’s Social Security Number (SSN) or Employer Identification Number (EIN) to avoid IRS penalties and backup withholding risk.

Key topics: worker classification, IRS compliance, SSN/EIN requirements, and avoiding costly mistakes.

Backup Withholding: The Most Critical Step

If a contractor does not provide a TIN, you are required to begin backup withholding immediately.

How Backup Withholding Works:

- Rate: 24% of all future payments

- Your Role: You act as a tax withholding agent

- Where It Goes: Paid directly to the IRS

- Reporting: Filed annually using Form 945

⚠️ Major Risk to Business Owners

If you continue paying a contractor without withholding the required 24%, the IRS can:

- Hold your business liable

- Require you to pay the uncollected tax out of your own pocket

- Assess additional penalties and interest

➡️ This is one of the fastest ways to turn a small compliance mistake into a serious financial liability

Below is an example of an actual IRS CP2100A Notice issued after a payer submitted 1099-MISC forms for tax year 2024. The IRS identified inconsistencies between the contractor information submitted on the 1099 forms and the information contained in IRS records.

In this case, the inconsistencies were caused by the spelling of the entity names. The names submitted on the 1099 filings did not exactly match the spelling originally associated with the Taxpayer Identification Numbers (TINs) in IRS records.

- The IRS is actively reviewing and matching 1099 filings.

- Accuracy is critical. Even when a contractor properly completes a W-9 form, mistakes can still occur during data entry, bookkeeping, or tax filing preparation.

This is one reason why businesses should maintain a structured worker compliance process that includes reviewing names, verifying TIN information, tracking payments carefully, and retaining documentation.

How to Avoid Penalties: Document Everything

When a 1099 is filed without a TIN, the IRS will eventually send notices such as:

- CP2100 / CP2100A (“B Notice”)

- Notice 972CG (penalty notice)

Penalties can reach $310 per form.

To avoid or reduce these penalties, you must prove “reasonable cause.”

What Counts as Reasonable Cause?

You must show that you made proper efforts to obtain the contractor’s TIN.

Required Steps:

1. Initial Request (W-9)

- Request a completed Form W-9 before payment is made

2. First Annual Solicitation

- If not received, request again by:

- December 31, or

- January 31 (if hired in December)

3. Second Annual Solicitation

- Request again the following year if still not provided

Best Practice: Protect Yourself With Documentation

Keep:

- Copies of all W-9 requests

- Emails or written communications

- Certified mail receipts (if used)

➡️ This documentation becomes your best defense if the IRS issues penalties.

Why Employee Misclassification Leads to Severe Penalties

Misclassifying workers affects:

- Tax obligations

- Worker rights

- Compliance with federal and state labor laws

Potential consequences include:

- Back wages and unpaid overtime

- Employment taxes and unemployment insurance

- Workers’ compensation liability

- Legal consequences including lawsuits

- IRS penalties up to 100% of unpaid taxes

- Audit exposure from multiple government agencies

➡️ One mistake can trigger federal and state investigations at the same time

State Regulations: Where Classification Gets More Complex

Different jurisdictions apply different standards.

California: The ABC Test

In California, the ABC test is used:

A worker is presumed an employee unless:

- They are free from control

- Perform work outside your business

- Operate an independent business

➡️ One of the strictest classification systems in the country

Texas: More Flexible but Still Enforced

In Texas:

- Uses IRS-style analysis

- Focuses on control and independence

- Still enforces unemployment insurance and labor laws

Mississippi (2026): Increasing Enforcement

In Mississippi:

- Follows federal classification frameworks

- Increasing enforcement through state agencies

- Added focus on employment compliance and hiring practices

📊 State-by-State Comparison: Worker Classification Enforcement

| State | Classification Standard | Enforcement Level | Key Penalties | Immigration Enforcement |

|---|---|---|---|---|

| California | Strict ABC Test | Very High |

• Per-worker fines • Back wages & overtime • Civil penalties up to thousands per violation • Possible lawsuits |

Strict labor enforcement; immigration tied to labor violations in some cases |

| Texas | Common law / IRS-based | Moderate |

• Unemployment tax penalties • Wage claims • Audit exposure |

Active enforcement; some E-Verify requirements for public employers |

| Mississippi (2026) | Federal-aligned | Increasing |

• Payroll tax exposure • Workers’ comp penalties • Potential civil fines |

State-level criminal penalties possible for hiring persons in the United States illegally |

| Florida | Common law / IRS-based | High (recent increases) |

• Fines for misclassification • Workers’ comp enforcement • Stop-work orders |

Mandatory E-Verify for many employers |

| New York | Strict (industry-specific ABC) | Very High |

• Significant fines • Criminal penalties in severe cases • Back wages & benefits |

Strong coordination between labor and immigration enforcement |

| General Trend | Moving toward stricter definitions | Increasing nationwide |

• Higher fines • Multi-agency audits • Expanded worker rights |

More states adopting E-Verify and immigration enforcement measures |

⚠️ Important: One misclassification issue can trigger both federal and state investigations at the same time.

Hiring “Persons in the United States Illegally”

A critical compliance issue involves hiring persons in the United States illegally.

Even when using contractors:

- You may still have legal obligations

- You cannot ignore red flags

- You may face legal consequences if you “should have known”

What Is E-Verify?

E-Verify is a system administered by the federal government to confirm work eligibility.

- Required for certain employers

- Required in some states

- Used to confirm legal work status

Even when not required, using it demonstrates:

- Due diligence

- Good faith compliance

- Reduced legal risk

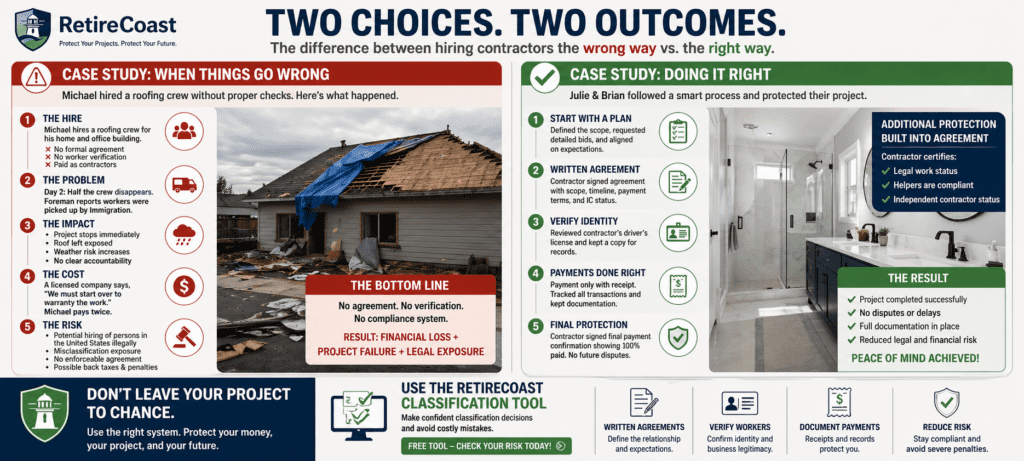

Case Study: When Things Go Wrong

Michael hired a crew to replace the roofs on his home and office building.

On the second day:

- Half the workers did not show up

- The foreman reported they were picked up by Immigration

The result:

- Work stopped

- Project delayed

- Additional cost

A licensed roofing company later refused to warranty the work unless they started from scratch.

➡️ Michael paid twice

Lesson

Failure to verify:

- Worker status

- Compliance

- Legitimacy

…can lead to financial loss and operational failure

📊 1099 vs W-2 Decision Flow (Quick Check)

1. Do you control how the work is done?

➡️ Yes → Employee (W-2)

➡️ No → Continue

2. Does the worker operate independently?

➡️ No → Employee (W-2)

➡️ Yes → Continue

3. Is the relationship ongoing?

➡️ Yes → Employee (W-2)

➡️ No → Continue

4. Is the worker a legitimate business?

➡️ No → High Risk Employee

➡️ Yes → Contractor (1099)

⚠️ Filing a 1099 does NOT determine classification.

1099 Compliance: The Law Applies to Everyone

Many believe that issuing a 1099 determines contractor status.

It does not.

Even:

- Under $2,000

- Without issuing a form

➡️ Worker classification laws still apply

You may still owe:

- Employment taxes

- Back wages

- Penalties

Use the Free Classification Tool

Before making classification decisions, use a structured system.

👉 [Use the Free Employee vs Contractor Classification Tool]

This tool helps you:

- Evaluate control test factors

- Identify classification risks

- Make informed business decisions

How to Protect Yourself (Best Practices System)

Your best defense is structure and documentation.

1. Use Written Contracts

A proper contract should include:

- Scope of work

- Payment terms

- Independent contractor status

- Compliance certification

2. Require Documentation

- W-9

- Identification

- Proof of business (if applicable)

3. Control Payment Structure

- Pay per project (not hourly when possible)

- Require invoices

- Maintain records

4. Avoid Behavioral Control

- Do not dictate how work is performed

- Focus on results

5. Perform Due Diligence

- Verify legitimacy

- Watch for red flags

- Document everything

Case Study: Doing It Right

Julie and Brian hired a contractor to remodel their bathroom.

They:

- Required a written bid

- Used a signed agreement

- Verified identification

- Required receipts for payments

- Documented final payment

The contractor certified:

- Legal work status

- Compliance of helpers

➡️ The result:

- Completed project

- No disputes

- Full documentation

Key Takeaways

- Worker classification affects taxes, compliance, and legal obligations

- There is no single factor—classification depends on the full relationship

- Federal and state regulations both apply

- Misclassification leads to severe penalties

- Documentation is your best defense

🚀 Stop Guessing. Build a Real Compliance System.

Reading about worker classification is a great start—but real protection comes from having the right tools, documents, and systems in place.

The RetireCoast Business Membership gives you everything you need to make confident, compliant business decisions—whether you’re hiring contractors, managing properties, or running a small business.

- ✔ Contractor Agreement Generator

- ✔ Worker Classification System

- ✔ Compliance & Documentation Tools

- ✔ Business Formation Resources

- ✔ Short-Term Rental Financial Tools

- ✔ Ownership & Structure Planner

- ✔ Audit-Ready Documentation Systems

- ✔ Ongoing Compliance Guidance

🛡️ One mistake can cost thousands in back taxes, penalties, or legal fees. A system helps you avoid it entirely.

Designed for business owners, real estate investors, and anyone hiring workers.

Next Step: Build Your Compliance System

Don’t rely on guesswork.

Use:

- The classification tool

- Written agreements

- Structured hiring processes

👉 Upgrade to access the full RetireCoast Business Membership tools:

- Contractor agreement generator

- Compliance tracking system

- Audit protection tools

FAQ

❓ Frequently Asked Questions: Employees vs Contractors

People Also Ask:

🔎 People Also Ask: Employees vs Contractors

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}