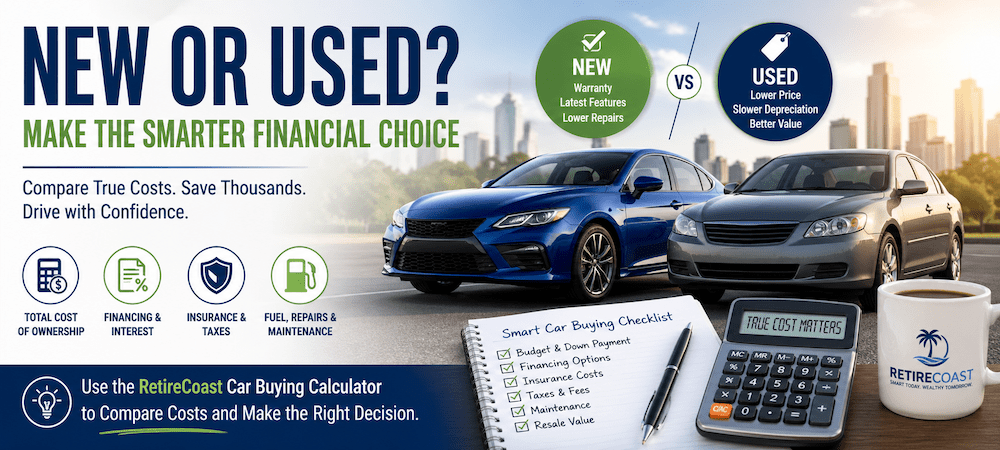

Buying a car isn’t just a purchase—it’s a financial system that can impact your monthly cash flow, your long-term savings, and even your stress level for years.

Most people walk into a dealership thinking about one number:

👉 “What will my monthly payment be?”

That’s where things go wrong.

Because the real question isn’t the payment—it’s:

👉 What will this car actually cost me over time?

This guide walks through the full decision process—from choosing the right vehicle to negotiating the deal—so you can make a decision that fits your life and your finances.ht vehicle to negotiating the deal—so you can make a decision that aligns with your financial goals.

- Start With This Question: Why Do You Need a Car?

- Choosing the Right Type of Vehicle

- Shopping for a Car: The Step Most Buyers Underestimate

- A Real-World Example

- New vs Used: What Are You Really Paying For?

- Lease vs Purchase: A Different Kind of Decision

- Cash vs Financing: It’s Not Always One Answer

- The 0% Financing Question

- Insurance: The Cost That Shows Up Later

- Sales Tax and Registration: The Hidden Layer

- Vehicle Buying Programs and Timing

- Negotiation: Where Preparation Wins

- Total Cost of Ownership: The Only Number That Matters

- Use the Free Tool Before You Decide

- Who Is Buying Cars Today? (And What It Means for Your Decision)

- New Vehicle Buyers by Generation

- Used Vehicle Buyers by Generation

- Key Buying Trends by Generation

- What This Means for You

- The Bigger Insight

- Tie-In to Your Decision

- Final Thoughts

- FAQ

Start With This Question: Why Do You Need a Car?

It sounds simple, but this is where many people take a wrong turn.

A car isn’t just a product—it’s a tool. And the right tool depends on what you’re trying to do.

If you’re commuting 40 miles a day, fuel efficiency matters.

If you’re hauling a fifth wheel, capability matters.

If you’re driving occasionally, reliability matters more than anything else.

But here’s what often happens:

Someone walks onto a lot, sees a truck they like, and starts imagining everything they could do with it—whether they actually will or not.

That gap between need and want is where thousands of dollars disappear.

Choosing the Right Type of Vehicle

Once you’re clear on your purpose, the vehicle type becomes much easier.

A long commuter will benefit from a fuel-efficient sedan or hybrid. A growing family may need an SUV or minivan. A business owner might need a truck or van.

What’s often overlooked is that the wrong type of vehicle doesn’t just cost more upfront—it costs more every month:

- Higher insurance

- Higher fuel costs

- More expensive repairs

Choosing correctly at the beginning reduces friction—and cost—for years.

Car buying cost breakdown infographic highlighting upfront and ongoing expenses like taxes, insurance, and maintenance.

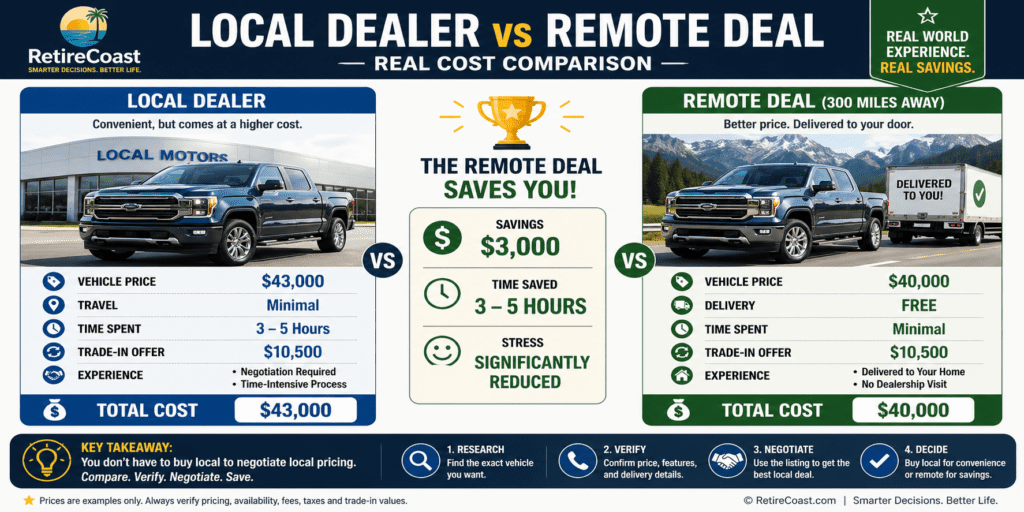

Shopping for a Car: The Step Most Buyers Underestimate

Years ago, buying a car meant visiting local dealerships and picking from what was available.

That’s no longer the case.

Today, you’re not limited to what’s within 10 miles—you have access to inventory across the country. And that changes the strategy completely.

Many smart buyers now use a simple but powerful approach:

They go to a local dealer first—not to buy—but to look.

They sit in the vehicle, test drive it, and confirm it’s exactly what they want.

Then they go home and start searching.

Platforms like Autotrader and Facebook Marketplace allow you to compare the same vehicle across dozens or even hundreds of listings.

And this is where things get interesting.

You may find the exact same truck:

- $43,000 locally

- $40,000 a few hundred miles away

At that point, you have leverage.

Before doing anything, you call the distant dealer. You confirm:

- The price is real

- The features match

- There are no surprises

Then you make a decision.

Sometimes the savings are worth the trip. Other times, they’re worth something even better—you take that listing back to your local dealer.

Now the conversation changes.

Instead of negotiating blindly, you’re negotiating with facts.

The dealer knows you have options. And in many cases, they’ll move closer than you expect—because losing a deal over a few thousand dollars isn’t something they want to do.

I searched online and found the same truck about 300 miles away in another state at a significantly lower price. When I called, I expected complications—but instead, they offered to deliver it directly to my home at no additional cost.

I also had a newer, smaller truck to trade in, which I thought might complicate things. Instead, they gave me exactly what I was hoping for.

The delivery driver arrived, I signed a few documents (financed through my credit union), and he drove my trade-in back.

No dealership visit. No hours of negotiation. Just a clean, efficient transaction.

This experience reinforced an important point: today’s car buying process is far more flexible than most people realize—especially if you’re willing to expand your search beyond your local market.

A Real-World Example

A few years ago, I was looking for a 3/4-ton pickup to pull a fifth wheel.

My local dealer didn’t have what I wanted—at least not one available for purchase. They had one that was already sold, which helped me confirm the configuration.

So I went online.

I found the exact truck about 300 miles away at a significantly lower price. When I called, I expected complications.

Instead, they told me they would deliver it to my home—for free.

I also had a newer truck to trade in, which I assumed would complicate things. It didn’t. They offered exactly what I was hoping for.

A driver showed up, I signed a few documents (I had already arranged financing through my credit union), and he drove my trade-in back.

No dealership visit. No hours of negotiation.

That experience changed how I think about car buying.

The flexibility is there—you just have to use it.

New vs Used: What Are You Really Paying For?

This is one of the most debated questions, but the answer is less about preference and more about trade-offs.

A new car gives you certainty:

- Full warranty

- No wear and tear

- Latest technology

But it comes at a cost—primarily depreciation.

A significant portion of a new car’s value disappears in the first few years.

A used car, on the other hand, has already gone through that phase. You’re buying it closer to its “real” value.

The trade-off is uncertainty:

- Maintenance risk

- Unknown history

For many buyers, the best balance is somewhere in the middle—a vehicle that’s two to four years old.

Someone else absorbed the steepest depreciation, but the vehicle is still modern and reliable.

Monthly Payment: $500

Term: 36 months

Total Paid:

$500 × 36 = $18,000

End Result:

❌ You own nothing

❌ Must lease again or buy

Monthly Payment: $650

Term: 60 months

Total Paid:

$650 × 60 = $39,000

End Result:

✅ You own the vehicle

✅ Asset value remains (example: $15,000+)

Lease twice (6 years): ~$36,000 and still no ownership

Buy once (5 years): ~$39,000 with a vehicle worth ~$15,000

Leasing feels cheaper monthly—but buying often builds real long-term value, especially if you keep the vehicle beyond the loan period.

Lease for flexibility and lower short-term cost.

Buy for long-term financial advantage.

Lease vs Purchase: A Different Kind of Decision

Leasing and buying aren’t just two ways to pay—they’re two different philosophies.

Leasing prioritizes:

- Lower monthly payments

- Driving newer vehicles

- Short-term flexibility

Buying priorities:

- Ownership

- Long-term value

- Eliminating payments over time

This becomes clearer when you look at a simple scenario.

A lease might cost $500 per month. A loan might cost $650.

At first glance, the lease looks like the better deal.

But over time, the picture changes.

After three years, you’ve spent $18,000 on the lease—and you own nothing.

After five years of payments, you own the vehicle—and it still has value.

Leasing feels cheaper in the moment. Buying often costs less in the long run—especially if you keep the vehicle for 6–10 years.

Cash vs Financing: It’s Not Always One Answer

There’s a common belief that paying cash is always best.

That’s not entirely true.

Paying cash eliminates interest, which is a real benefit. But it also ties up money that could be used elsewhere.

Financing, on the other hand, keeps your cash available—but adds cost.

The decision often comes down to interest rates.

If rates are high, paying cash becomes more attractive.

If rates are low—or even 0%—financing can be a strategic choice.

The 0% Financing Question

Manufacturers often advertise 0% financing. It sounds like a clear win—but it’s not always that simple.

In many cases, taking 0% financing means giving up a rebate or discount.

So the real question becomes:

👉 Is the interest you save greater than the discount you lose?

Sometimes it is. Sometimes it isn’t.

The only way to know is to run the numbers.

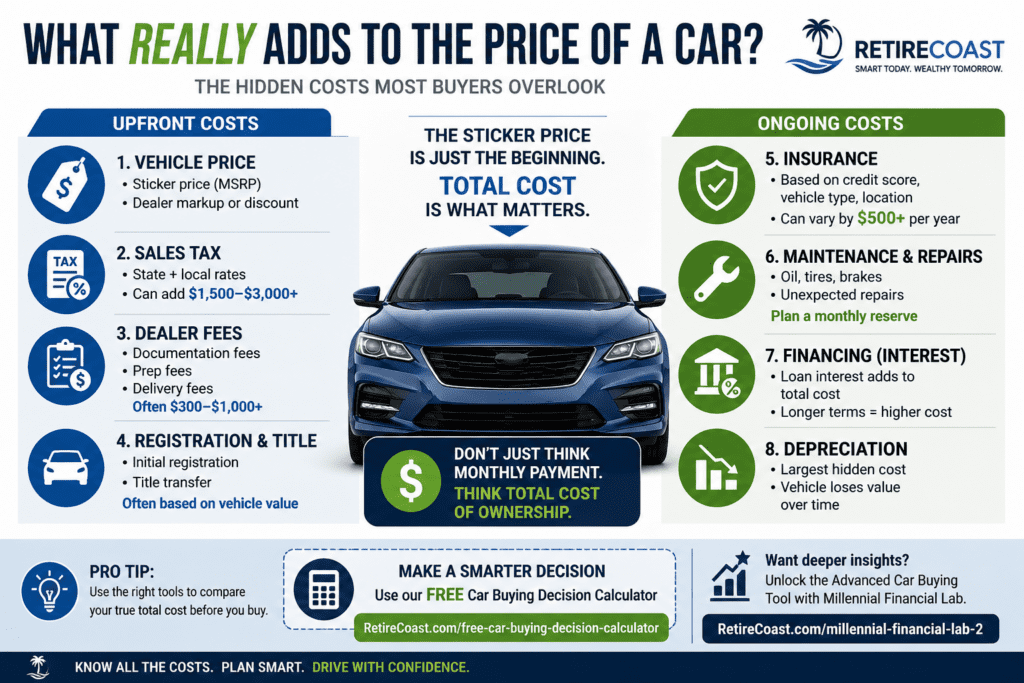

Insurance: The Cost That Shows Up Later

Insurance is rarely part of the buying conversation—but it should be.

Two vehicles with similar prices can have very different insurance costs.

Before buying, it’s worth calling your insurer and asking:

👉 “What would this cost me to insure?”

That one step can prevent surprises.

Sales Tax and Registration: The Hidden Layer

The price you see is not the price you pay.

Taxes and registration fees can add thousands.

In Mississippi, for example, the tax rate is relatively low—but there’s an important advantage:

The value of your trade-in is deducted before calculating tax.

So a $30,000 purchase with a $10,000 trade is taxed on $20,000.

That reduces both:

- Immediate tax

- Future registration costs

It also highlights an important point:

Sometimes taking a trade-in—rather than selling privately—can actually make financial sense once taxes are considered.

Vehicle Buying Programs and Timing

There are ways to reduce prices that many buyers overlook.

Programs like the Costco Auto Program offer pre-negotiated pricing.

Manufacturers offer discounts for:

- Military

- First responders

- Loyalty customers

Some buyers can even purchase through programs like the Army & Air Force Exchange Service.

Timing also matters.

Dealers are more motivated:

- At the end of the month

- At the end of the year

- When new models arrive

Buying last year’s model—when the new one is on the lot—is one of the simplest ways to save money.

The authors’ discussion about dealer add-ons.

Negotiation: Where Preparation Wins

Negotiation doesn’t start at the dealership—it starts before you go.

The strongest position you can have is this:

👉 You don’t need the dealer.

That comes from preparation.

You know:

- What the vehicle costs elsewhere

- What your financing options are

- What your trade-in is worth

When you sit down, you focus on one thing: the price of the vehicle.

Not the payment. Not the trade-in. Just the price.

As the conversation progresses, the dealer may offer better terms if you finance with them.

At that point, you already have your rate. Now they have to beat it.

The key is staying focused—and not getting pulled into side conversations that blur the numbers.

-

:contentReference[oaicite:0]{index=0}

nhtsa.gov

👉 Check VIN recalls and official 5-Star Safety Ratings before buying a used vehicle. -

:contentReference[oaicite:1]{index=1} – Car Buying Guide

consumer.ftc.gov/articles/buying-and-owning-a-car

👉 Learn your rights, spot dealer tactics, and understand warranties and financing. -

:contentReference[oaicite:2]{index=2} – Auto Loans

consumerfinance.gov/consumer-tools/auto-loans

👉 Understand loan terms, compare rates, and avoid costly financing mistakes. -

:contentReference[oaicite:3]{index=3} – Fuel Economy

fueleconomy.gov

👉 Compare MPG, estimate fuel costs, and review EV and hybrid tax credits.

-

:contentReference[oaicite:4]{index=4}

iihs.org

👉 Known for rigorous crash testing. Look for “Top Safety Pick” ratings. -

:contentReference[oaicite:5]{index=5} (Cars)

consumerreports.org/cars

👉 Excellent for long-term reliability and real owner data. -

:contentReference[oaicite:6]{index=6} & :contentReference[oaicite:7]{index=7}

kbb.com | edmunds.com

👉 Check fair market value before negotiating price or trade-in.

Total Cost of Ownership: The Only Number That Matters

Everything comes back to this.

The true cost of a car includes:

- Purchase price

- Interest

- Insurance

- Maintenance

- Depreciation

A lower monthly payment doesn’t always mean a lower cost.

Looking at the full picture is what separates a good decision from an expensive one.

Use the Free Tool Before You Decide

Before making a final decision, it helps to see the numbers clearly.

👉 https://retirecoast.com/free-car-buying-decision-calculator-compare-costs/

This tool allows you to:

- Compare local vs remote deals

- Evaluate financing options

- Estimate your total cost

It’s a simple step—but one that can prevent costly mistakes.

Compare local vs remote deals, cash vs financing, trade-in impact, taxes, insurance, and total cost—all in one place.

This tool helps you see the real cost before you buy.

multi-vehicle comparisons, lease vs buy analysis, 6–10 year ownership costs, depreciation, tax impact, and more.

Rising vehicle prices, higher interest rates, and increased insurance costs have pushed many buyers to rethink how they approach the decision.

That’s why many buyers today are:

- Comparing used vs new more carefully

- Shopping beyond local dealerships

- Focusing on total cost—not just monthly payment

- Using tools to evaluate long-term financial impact

The buyers who take the time to run the numbers and compare scenarios are the ones who avoid overpaying.

This approach is exactly what the Millennial Financial Lab was built around—helping you make decisions based on real numbers, not pressure or assumptions.

Who Is Buying Cars Today? (And What It Means for Your Decision)

When you’re buying a car, it’s easy to feel like it’s just a personal decision. But step back for a moment, and you’ll see something bigger:

👉 You’re part of a much larger trend.

Different generations approach car buying in very different ways—based on income, lifestyle, and financial priorities. Understanding where you fit can help you make a smarter decision and avoid following the wrong strategy for your situation.

New Vehicle Buyers by Generation

New car purchases are still dominated by older generations—primarily because they’re in their peak earning years and have accumulated more wealth.

Current Breakdown of New Vehicle Buyers:

| Generation | Birth Years | Share of New Buyers |

|---|---|---|

| Generation X | 1965–1980 | 32% – 36% |

| Millennials | 1981–1996 | 27% – 29% |

| Baby Boomers | 1946–1964 | 26% – 28% |

| Generation Z | 1997–2012 | 8% – 9% |

| Silent Generation | 1928–1945 | 2% – 3% |

What This Means

For years, Baby Boomers dominated new vehicle purchases. But that’s changing.

Their share has declined from over 32% in 2019 to roughly 27% today as they move out of their primary buying years.

At the same time:

👉 Millennials are steadily gaining ground

They are now one of the largest groups of new car buyers—and that trend is expected to continue.

Used Vehicle Buyers by Generation

The used car market tells a different story.

Here, the demographics shift younger—driven by affordability and first-time purchases.

Current Breakdown of Used Vehicle Buyers:

| Generation | Share of Used Buyers |

|---|---|

| Millennials | 31% – 32% |

| Generation X | 30% – 31% |

| Baby Boomers | 20% – 25% |

| Generation Z | 10% – 15% |

| Silent Generation | < 3% |

What This Means

👉 Millennials dominate the used car market.

👉 Generation Z is entering fast—but primarily through used vehicles.

This reflects two realities:

- Rising vehicle prices

- Higher interest rates

Younger buyers are adapting by focusing on value and affordability rather than brand-new purchases.

Key Buying Trends by Generation

Understanding these patterns helps you see what’s driving decisions—not just what people are buying.

Generation X (The Market Leaders)

Gen X leads in overall new vehicle purchases.

They tend to:

- Buy higher-priced vehicles

- Take on larger loans

- Favor trucks, SUVs, and luxury vehicles

👉 This group is often balancing peak income with family needs and lifestyle purchases.

Millennials (The Strategic Buyers)

Millennials are shaping the market in two major ways:

- They dominate used vehicle purchases

- They are the fastest-growing EV buyers

Over 12% of their new vehicle purchases are electric vehicles.

👉 This reflects a shift toward:

- Cost awareness

- Long-term savings

- Technology adoption

Baby Boomers (The Established Buyers)

Boomers still hold a large share of purchases, but their preferences are clear:

- Traditional gas vehicles

- Hybrid options

- Reliable, comfortable SUVs

👉 Their focus is less on trend and more on reliability and familiarity.

Generation Z (The Emerging Buyers)

Gen Z is still a smaller portion of the market—but growing quickly.

They tend to:

- Buy used vehicles

- Focus on affordability

- Choose smaller, fuel-efficient cars

Common choices include:

- Honda Civic

- Toyota Camry

👉 This group is highly sensitive to:

- Price

- Interest rates

- Monthly affordability

What This Means for You

This data isn’t just interesting—it’s useful.

It shows that:

- Buying new is often tied to income level and financial stability

- Buying used is often tied to strategy and affordability

- Younger buyers are adapting faster to rising costs

The Bigger Insight

👉 The “right” car decision depends less on age—and more on financial position.

You don’t need to follow what your generation is doing.

But understanding the trends helps you ask a better question:

👉 “Am I making this decision based on my situation—or just following the market?”

Tie-In to Your Decision

Before you decide:

- Compare new vs used

- Evaluate financing

- Consider total cost

👉 Then run your numbers here:

https://retirecoast.com/free-car-buying-decision-calculator-compare-costs/

Final Thoughts

Buying a car doesn’t have to be complicated—but it does require intention.

When you:

- Define your need

- Compare your options

- Run the numbers

- Stay disciplined

You shift the outcome in your favor.

A car should support your life—not quietly work against it.

The right tools and strategy can completely change that outcome.

FAQ

1. Is it better to buy a new or used car?

2. Should I pay cash or finance a car?

3. Is 0% financing always the best deal?

4. How much should I consider insurance before buying?

5. Does trading in a car reduce sales tax?

6. Can I avoid sales tax by buying a car in another state?

7. Is leasing better than buying?

8. What is total cost of ownership?

9. When is the best time to buy a car?

10. How can I compare car buying options before going to the dealer?

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}