Section I: Financial Literacy Is Not Optional Anymore

Listen to the author’s comments on this article:

Author’s audio comments

Financial literacy is no longer a “nice-to-have” skill. It is a survival skill—and the foundation of sound financial strategies that guide everyday decisions about spending, saving, borrowing, and planning for the future.

The modern financial landscape is more complex than at any point in recent history. Families are navigating higher costs of living, volatile markets, changing retirement rules, evolving tax policies, and increasingly expensive education choices—all while being expected to apply effective financial strategies that will shape decades of financial outcomes.

Yet despite these rising demands, financial literacy in the United States remains stubbornly low, leaving many households without the basic tools needed to apply even simple financial strategies consistently.

Multiple national studies paint a consistent and concerning picture.

On the Personal Finance Index (P-Fin Index), U.S. adults correctly answer only about half of basic financial knowledge questions, a figure that has barely improved since 2017. In separate surveys, fewer than one-third of adults can correctly answer a majority of foundational questions about saving, borrowing, investing, and risk—core concepts required to build reliable financial strategies. Nearly half of Americans grade their own financial knowledge a “C” or worse—an honest reflection of both low confidence and low mastery.

The weakest area across all age groups is understanding risk and diversification, the very skills required to make sound long-term decisions and implement sustainable financial strategies. This gap shows up in real-world behavior: fewer people pay credit cards in full, emergency savings are thin, and many households carry significant debt without fully understanding its long-term impact.

These are not abstract statistics. They translate directly into stress, limited flexibility, missed opportunities, and financial strategies that fail when they are needed most.

Financial literacy grows strongest when knowledge is shared across generations.

Financial Literacy Is About Daily Decisions

Financial literacy is often misunderstood as something reserved for investing or retirement planning. In reality, it affects daily decisions:

How income is allocated between spending, saving, and future goals

Whether emergency savings are protected or slowly consumed

How debt is used—or misused

How large, one-time decisions ripple through the household budget

Small gaps in understanding can compound into major consequences over time.

One of the clearest examples is emergency readiness. While many Americans believe they are financially stable, a significant portion still cannot comfortably absorb a modest unexpected expense. When savings are thin, every major decision becomes riskier—and mistakes become harder to recover from.

Why Gen X Faces a Unique Financial Literacy Test

Generation X sits at the center of competing financial pressures.

They are close enough to retirement that mistakes matter, yet still far enough away that they are often supporting others. Many Gen X households are balancing:

Mortgages and housing costs

Saving for retirement on a shortened timeline

Supporting children through college or early adulthood

Assisting aging parents

Rising healthcare and insurance expenses

This makes financial literacy especially critical. There is less margin for error and fewer years to recover from poor decisions.

And yet, Gen X did not grow up with widespread financial education requirements. Most learned money management through experience—often during periods of economic upheaval. That experience builds resilience, but it does not automatically fill knowledge gaps around modern financial tradeoffs.

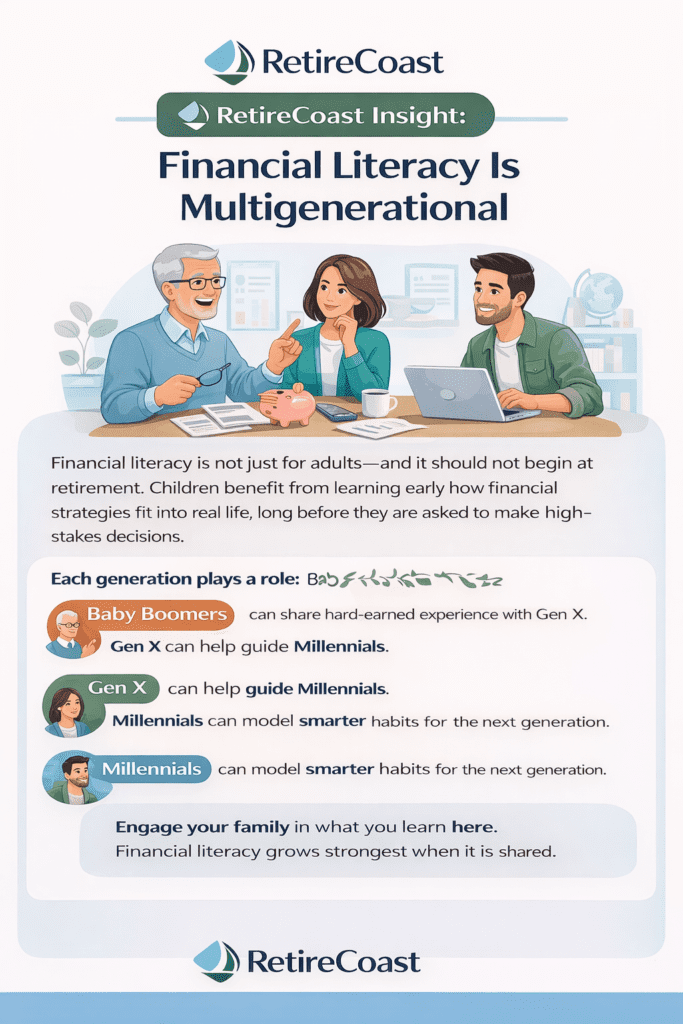

RetireCoast Insight: Financial Literacy Is Multigenerational

Financial literacy is not just for adults—and it should not begin at retirement.

Children benefit from learning early how financial strategies fit into real life,

long before they are asked to make high-stakes decisions.

Each generation plays a role:

Baby Boomers can share hard-earned experience with Gen X,

Gen X can help guide Millennials,

and Millennials can model smarter habits for the next generation.

Engage your family in what you learn here. Financial literacy grows strongest when it is shared.

Emotion Is the Enemy of Financial Literacy

The most damaging financial decisions are rarely made out of ignorance alone. They are often made under emotional pressure.

Fear, pride, guilt, optimism, and social comparison can quietly override rational analysis. This is especially true for high-stakes decisions that involve family, identity, or future opportunity.

When emotion leads and numbers follow, households tend to:

Underestimate total costs

Overestimate future income

Minimize risk

Assume “it will work out somehow”

Financial literacy is the discipline of reversing that order.

It does not remove values, goals, or compassion from decisions. It simply insists that reality be acknowledged before commitment is made.

Financial Literacy in Action

This article is not about memorizing definitions or mastering complex formulas. It is about applying financial literacy where it matters most—at decision points that shape long-term outcomes.

That includes:

How income is divided between current needs, savings, and future goals

How family support is provided without undermining stability

How large investments—like education—are evaluated for return and risk

Few decisions test financial literacy more than paying for a child’s education. It is expensive, emotional, and often framed as non-negotiable. But when handled without structure, it can quietly derail even well-prepared households.

That is why the next section focuses on Financing Education for Children—not as a moral question or a cultural expectation, but as a real-world financial decision that demands clarity, boundaries, and honest analysis.

Financial literacy is not about saying “no.” It is about making sure that when you say “yes,” you can afford the consequences.

RetireCoast TestFinancial Literacy Basics

Financial Literacy Quick Test (10 Questions)

These questions cover the basics every competent adult should understand—compounding, inflation, diversification,

borrowing, credit, and retirement accounts. Surveys consistently show many adults score around 50%

or lower on these fundamentals, which helps explain costly mistakes with debt and investing.

How it works: Answer each question, then click Score My Test.

You’ll see your score, a skill breakdown, and quick explanations.

Progress

0 of 10 answered

Tip: “Do not know” is better than guessing when learning.

Your Results

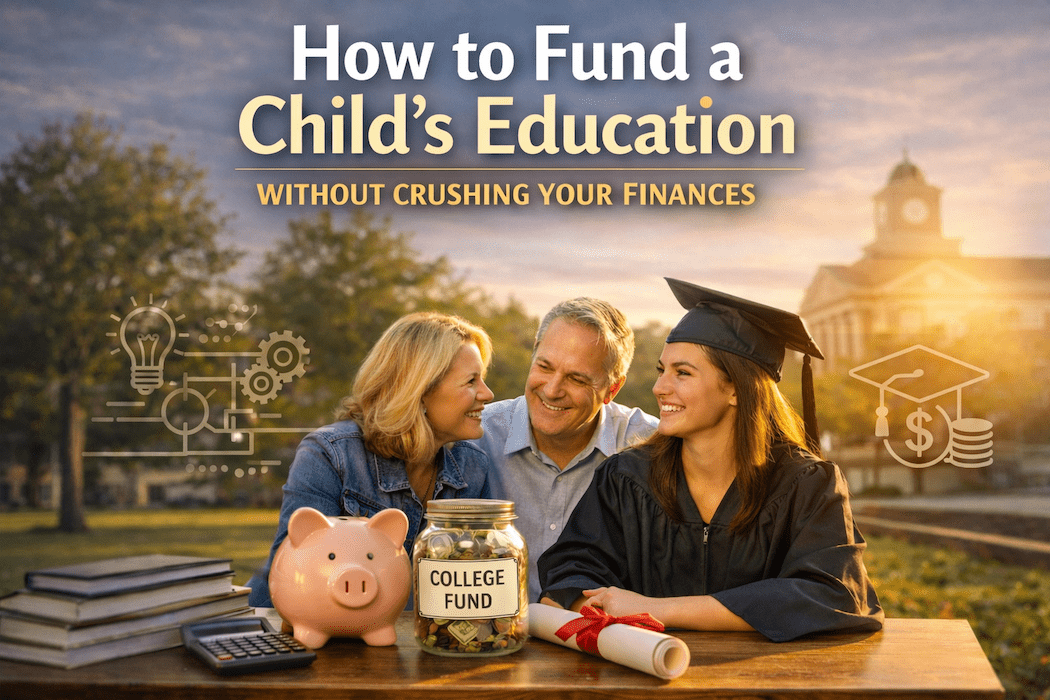

Section II: Financing Education for Children — Financial Strategies in Action

Section II Financing Education for Children

Paying for a child’s education is one of the most consequential financial decisions a family can make. Unlike routine budget choices, education funding often involves large sums, long time horizons, and emotional pressures that can easily override good judgment.

Too often, parents focus on school name, peer choices, or short-term affordability without clearly evaluating the long-term financial impact. This is why a household’s approHow to Fund a Child’s Education Without Crushing Your Financesach to how to pay for college must be anchored in solid financial literacy and a disciplined decision framework.

At its core, education funding is a capital allocation decision—not a moral obligation. When a family commits to cover tuition, room, board, fees, and borrowing, they are choosing how to distribute scarce resources across competing goals like retirement, homeownership, or emergency savings.

Without structure, emotion too often drives this decision, leading families to borrow more than they can comfortably manage or to exhaust savings that would otherwise protect the household during unexpected life events.

The full companion article, “How to Fund a ChildHow to Fund a Child’s Education Without Crushing Your Finances’s Education Without Crushing Your Finances,” provides a step-by-step guide that families can follow to evaluate education choices more intelligently. It introduces a simple decision equation that compares education cost to expected lifetime earnings and explains how to apply that equation in practical scenarios.

The article also walks through student loan risks, including the differences between federal and private borrowing, repayment structures, and the long-term consequences of default or deferment. This deeper treatment helps families understand not just the cost of college but the true cost when accounting for interest, lost investment opportunity, and stress on household finances.

Real families make this abstract. In the companion article, you’ll find the rSean & Janet case study, which illustrates how a well-intentioned decision to pay for an expensive private college can deplete savings, eliminate safety nets, and create stress when life unexpectedly changes.

Their experience underscores why a carefully structured, math-first approach is vital—not just for avoiding regret, but for preserving stability.

To support rigorous analysis, the companion article also includes the EducationEducation ROI & Career Decision Calculator ROI & Career Decision Calculator, a tool that takes inputs like total cost, available funds, borrowing needs, expected earnings, and risk factors (like job loss or elder care) to produce a clear comparison of alternatives.

Running scenarios side-by-side—such as in-state public school, community college transfers, trade/technical programs, or military academies—often changes the conversation and prevents emotionally driven commitments.

Additionally, the article offers practical tools like a Family Meeting Summary PDF, designed to guide calm, value-based conversations rather than reactive debates. Together with the calculator, this PDF helps align expectations, surface assumptions, and keep the focus on financial sustainability.

Finally, the full guide explores alternatives families might overlook: savings strategies, scholarships/grants that do not require repayment, trade school paths that can lead to strong earnings with less debt, and disciplined borrowing strategies when loans are unavoidable. It also highlights the importance of protecting emergency savings and retirement accounts while still supporting a child’s goals.

In short, this section of the pillar article sets up the problem and introduces the concepts of disciplined education funding. For the complete roadmap—with tools, examples, and detailed steps—visit How to Fund a Child’s Education Without Crushing Your Finances at RetireCoast.

Need a Step-by-Step Plan to Pay for College?

Paying for education is one of the biggest financial decisions a family can face — and emotion often outweighs analysis.

The companion guide **“How to Fund a Child’s Education Without Crushing Your Finances”** walks you through:

How to compare total cost vs expected earnings (ROI)

Student loan risks — federal vs private

Structured tools like the Education ROI & Career Decision Calculator

Case studies and printable family discussion tools

Alternative paths such as community college, trades, and grants

Section III: Understanding Your Income — More Than a Paycheck

Most people believe they understand their income. They know their salary, their hourly wage, or what shows up in their bank account on payday. But financial literacy requires a deeper understanding than that.

Income is not just a paycheck. It is a system of cash flow, timing, taxes, obligations, and tradeoffs that determines how resilient—or fragile—your financial life truly is.

Two households earning the same amount can experience completely different financial outcomes depending on how their income is structured, how predictable it is, and how much of it is already committed before spending decisions are ever made.

Understanding your income at this level is the foundation for every financial strategy that follows.

Gross Income vs. Usable Income

At the most basic level, there is a critical difference between what you earn and what you can actually use.

Gross income is the headline number—your salary, wages, or total earnings. Usable income is what remains after taxes, payroll deductions, insurance, retirement contributions, and other mandatory withholdings are removed.

Many financial mistakes begin when people build budgets or make commitments based on gross income instead of usable income. When that happens, plans fail not because of a lack of discipline, but because the underlying assumptions were unrealistic.

Financial literacy starts with realism.

Understanding Payroll Deductions: What You Actually Control

One of the most misunderstood aspects of income is what happens to it before it ever reaches your bank account.

You are legally required to pay income taxes on your earnings, adjusted for allowable deductions. For most employees, those taxes are collected throughout the year through payroll withholding, based on information provided on the W-4 form.

This is where many people unintentionally create problems.

Some employees reduce withholding in an attempt to increase take-home pay. Others over-withhold because they like receiving a large refund. Both approaches misunderstand how payroll withholding should be used.

Under-withholding often leads to an unpleasant surprise at tax time—owing the IRS money, sometimes with penalties for failing to pay enough throughout the year. Over-withholding creates a different problem: it turns your paycheck into an interest-free loan to the government.

Payroll withholding is not a savings strategy. It is a cash-flow management tool.

[INSERT RETIRECOAST CALLOUT: “The Big Refund Is Not a Win”]

Mandatory Payroll Taxes: The Hidden Cost of Income

Another reason income feels smaller than expected is that employers and employees are both required to pay mandatory payroll taxes.

These include Social Security, Medicare, and unemployment taxes—costs that are largely invisible to employees but materially affect total compensation and take-home pay.

[INSERT TABLE: Mandatory Payroll Taxes Paid by Employers]

Seeing these deductions laid out helps explain why gross income and usable income diverge so sharply.

Special Consideration: Self-Employed Income Is Different

Self-employed individuals, contractors, and small business owners experience income very differently.

Instead of sharing payroll tax responsibility with an employer, self-employed individuals pay both sides of Social Security and Medicare. Income is also irregular, taxes are paid quarterly, and no withholding occurs automatically.

Treating self-employed income like a traditional paycheck is one of the most common and costly mistakes.

⚠️

Self-Employed Income Is Taxed Very Differently

If you are self-employed, a contractor, or earn income outside of a traditional paycheck,

your income is not taxed the same way as a W-2 employee’s income.

There is no automatic withholding, no employer sharing payroll taxes,

and no safety net if you fail to plan ahead.

Self-employed individuals are responsible for both sides of Social Security and Medicare taxes,

must make quarterly estimated tax payments, and often experience irregular cash flow.

Treating this income like a normal paycheck is one of the most common—and expensive—mistakes.

Financial literacy for self-employed households requires larger cash buffers,

disciplined tax planning, and a clear separation between business revenue and personal spending.

Without structure, strong income can still lead to financial stress.

W-2 Employee vs. Self-Employed Income: What’s Different

Category

W-2 Employee

Self-Employed / 1099

Payroll taxes (Social Security & Medicare)

Pays 7.65%. Employer pays the other half.

Pays 15.3% (both employee and employer portions).

Tax withholding

Automatically withheld from each paycheck.

No automatic withholding — must plan and set aside taxes manually.

Quarterly estimated taxes

Typically not required.

Often required to avoid IRS penalties.

Income predictability

Regular and predictable pay schedule.

Often irregular, seasonal, or project-based.

Benefits

May include employer-sponsored insurance and retirement plans.

Must self-fund health insurance and benefits.

Retirement options

Typically 401(k) with possible employer match.

SEP IRA, Solo 401(k), Roth IRA (self-managed).

Biggest common mistake

Budgeting based on gross income instead of take-home pay.

Spending tax money as if it were profit.

RetireCoast Insight: Self-employed income can create flexibility and upside,

but it requires stronger systems — disciplined tax planning, larger cash reserves,

and a clear separation between business revenue and personal spending.

Income Timing Matters as Much as Income Amount

When income arrives unevenly—through commissions, bonuses, seasonal work, or business revenue—expenses do not adjust automatically.

Mortgage payments, utilities, insurance, and food costs operate on fixed schedules. Financially literate households recognize this mismatch and compensate with larger cash buffers and more conservative commitments.

Ignoring income timing creates stress even in households with strong earnings.

Where Your Paycheck Actually Goes

To understand usable income, it helps to visualize the path money takes from gross pay to take-home pay.

Where Your Paycheck Goes — From Gross Pay to Take-Home

Hover over highlighted terms to understand how each step affects your

usable income.

Gross pay is your total earnings before any deductions.

This is not the amount you can spend.

Gross Pay Headline income shown on your offer letter or salary agreement.

↓

Pre-tax deductions reduce taxable income but also reduce cash flow.

They are often your best opportunity to automate smart financial behavior.

Pre-Tax Deductions

401(k) contributions

Health insurance premiums

↓

These taxes are mandatory. Underpaying can result in penalties,

while overpaying creates interest-free loans to the government.

Taxes Withheld

Federal income tax

Social Security (FICA)

Medicare (FICA)

State & local taxes

↓

Post-tax deductions reduce flexibility because taxes are already paid.

Loans here limit future cash flow.

Post-Tax Deductions

401(k) loan repayments

Garnishments (if applicable)

↓

This is the only money available for living expenses.

All budgets must be built from this number.

Net Pay (Take-Home Pay)

Used for housing, food, transportation, utilities, and discretionary spending.

RetireCoast Insight: Hovering over each section reveals why

income planning must start before money ever hits your checking account.

This visual reinforces a critical lesson: a significant portion of income never reaches checking, yet still affects your financial flexibility.

Why Small Changes Matter: The 401(k) Example

Many people hesitate to increase retirement contributions because they fear losing too much take-home pay. In reality, the impact is often far smaller than expected due to tax treatment.

The 401(k) Contribution Impact Calculator allows you to adjust contribution percentages and immediately see how changes affect both take-home pay and long-term savings.

RetireCoast Tool: See How 401(k) Contributions Affect Your Paycheck

Many people underestimate how little increasing a 401(k) contribution actually reduces take-home pay.

This calculator lets you compare two contribution rates side-by-side and see the estimated impact on

your paycheck and annual retirement savings.

This tool consistently demonstrates that financially literate households use payroll deductions to automate good behavior instead of relying on willpower.

Income Has a Job, Not Just a Destination

Every dollar of income has one of three purposes:

Cover today’s needs

Protect against risk

Build the future

When income is not assigned intentionally, it defaults to consumption. When it is assigned deliberately, it becomes a tool.

This mindset—not income level—is what separates households that feel constantly behind from those that feel in control.

Category

❌ Bad Strategy

✅ Smart Strategy

W-4 Withholding

Under-withheld to “get more now”

Accurate withholding to avoid tax shock

Tax Outcome

Owes IRS at filing + possible penalties

Break-even or small refund

Retirement Savings

Minimal or skipped to “free up cash”

Automatic 401(k) or Roth IRA funding

Use of Extra Cash

Spent unintentionally

Directed to long-term growth

Psychological Effect

Short-term relief, long-term stress

Predictability and confidence

Long-Term Result

No growth, recurring tax problems

Compounding assets, fewer surprises

Why This Comes Before Budgeting

Many people jump straight to budgeting apps or expense tracking without first understanding their income. That approach almost always fails.

Budgeting is about allocation. Allocation only works when income is clearly understood in terms of:

Amount

Timing

Stability

Obligations

In the next section, we’ll build on this foundation by showing how financially literate households divide income into practical categories that support daily living, future goals, and flexibility—without relying on unrealistic assumptions.

System Checkpoint:

Are needs funded automatically?

Does protection absorb surprises without panic?

Is the future growing even when life gets busy?

If any answer is “no,” the solution is not more effort—it’s system adjustment.

Section IV: Dividing Income Into Needs, Protection, and the Future

From Understanding Income to Directing It With Intention

In Section III, we focused on something many people never truly examine: how income actually flows. We looked at payroll deductions, W-2 versus self-employed income, and why take-home pay is often very different from gross pay. That understanding matters—but it is only the starting point.

Once income hits your checking account, clarity without direction doesn’t create progress.

This section is about what happens next.

Rather than treating money as something to track after it’s spent, this framework treats income as something that must be assigned on purpose. Not rigidly. Not obsessively. But intentionally.

Why Income Must Be Assigned—Not Just Budgeted

Traditional budgeting often focuses on categories and limits. In practice, that approach breaks down under real life—unexpected expenses, fluctuating income, family obligations, and rising costs.

What consistently works better is assignment before spending.

You already accept this idea without realizing it:

Taxes are withheld before you can spend them

Health insurance premiums are deducted automatically

Retirement contributions happen before money reaches your account

Those dollars behave differently because they were decided on in advance.

The same principle applies to the rest of your income.

💡

RetireCoast Insight

Money that is assigned behaves differently than money that is leftover.

Assigned dollars get a job before spending begins—needs, protection, or the future. Leftover dollars tend to disappear

into whatever happens next.

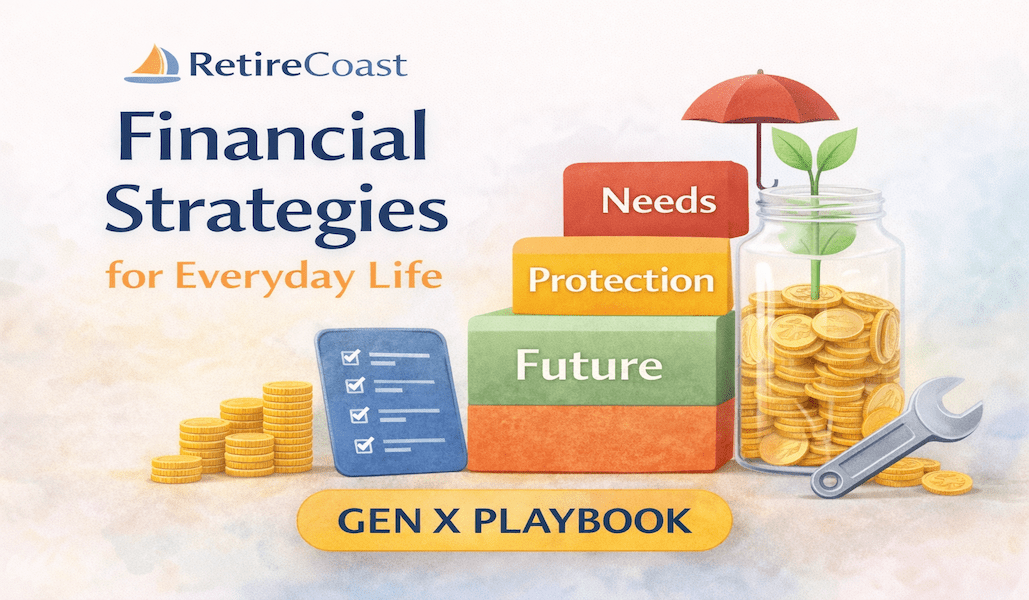

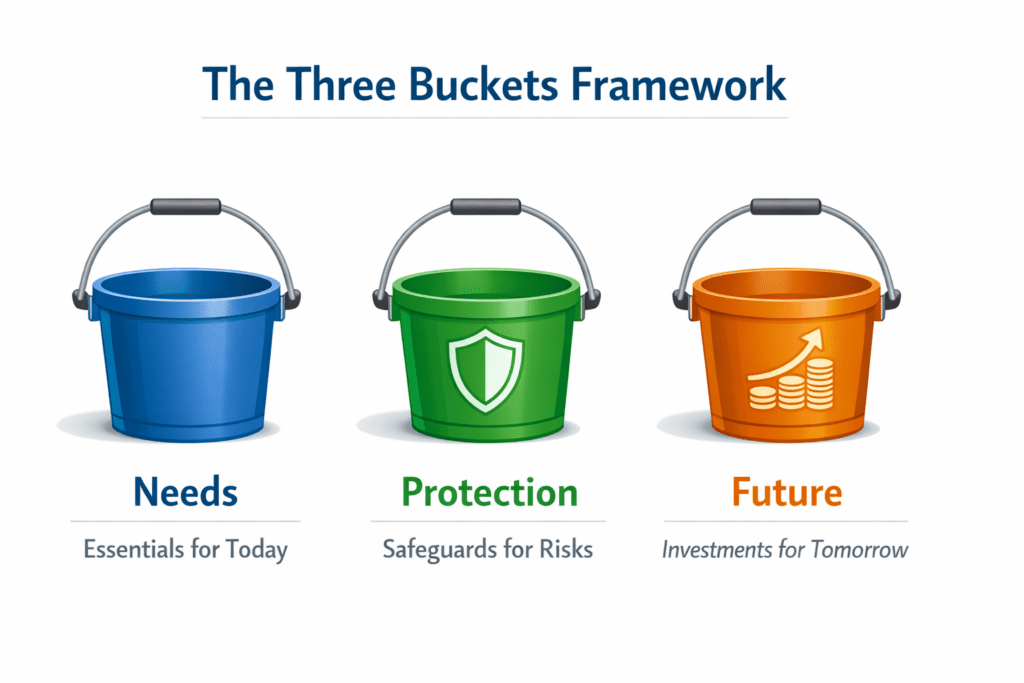

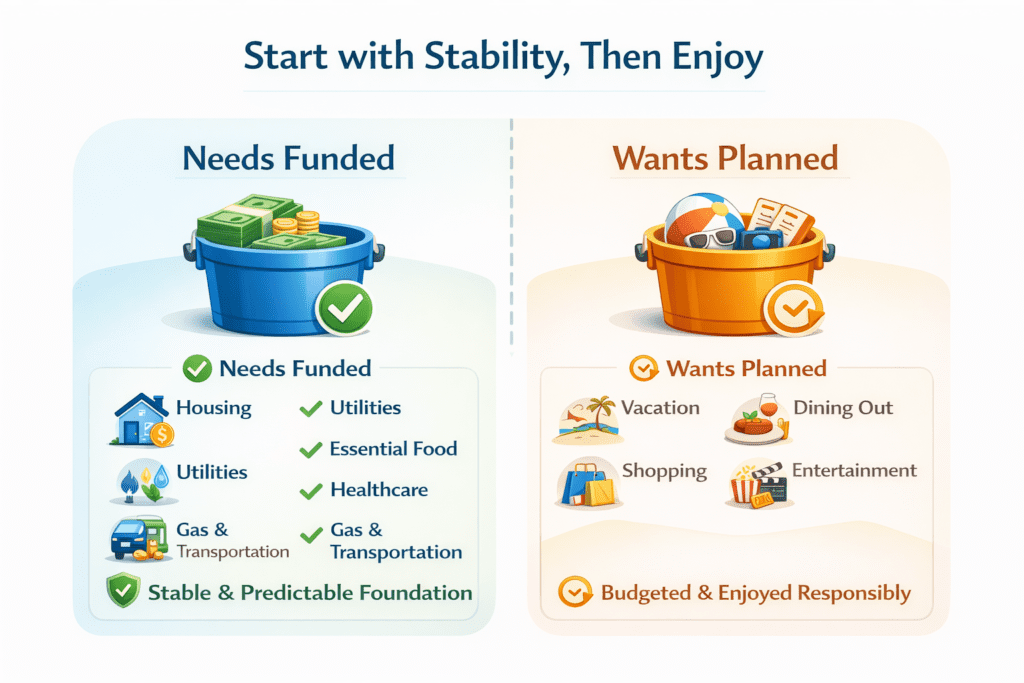

This section introduces a simple framework that replaces vague budgeting with structured decisions.The Three Buckets Framework

Every dollar you earn ultimately serves one of three purposes:

Needs – What keeps your household functioning

Protection – What prevents disruption from becoming damage

The Future – What builds long-term security and flexibility

This is not a rigid percentage system. It is a decision framework that helps you prioritize intelligently as income changes over time.

The Three Buckets Framework helps direct income with intention—covering today’s needs, protecting against disruptions, and building long-term financial security.

Each bucket has a distinct job. Confusing them—or ignoring one—creates stress later, even when income looks “good” on paper.

Bucket One: Needs — Stabilizing the Present

Needs are the expenses required to keep life running:

Housing

Utilities

Food

Transportation

Basic healthcare

Minimum debt obligations

These expenses form the foundation of financial stability. If this bucket is unstable, nothing else works smoothly.

Two important distinctions matter here:

Fixed needs (mortgage, insurance premiums)

Variable needs (groceries, fuel, utilities)

Many financial problems don’t come from income shortages—they come from unnoticed expansion of variable needs.

✔

Common Household Needs

These are core expenses required to keep a household stable and functioning.

They should be funded before discretionary spending or future upgrades.

Housing (rent or mortgage, property taxes, HOA fees)

Minimum debt obligations (student loans, credit cards, personal loans)

Child or dependent-related essentials

RetireCoast Insight: Needs are not about lifestyle level—they are about

predictability. When this bucket is stable, every other financial decision becomes easier.

Monthly household requirements represent the “Needs” bucket—core expenses that must be covered before discretionary spending or future goals.

The goal is not austerity. The goal is predictability.

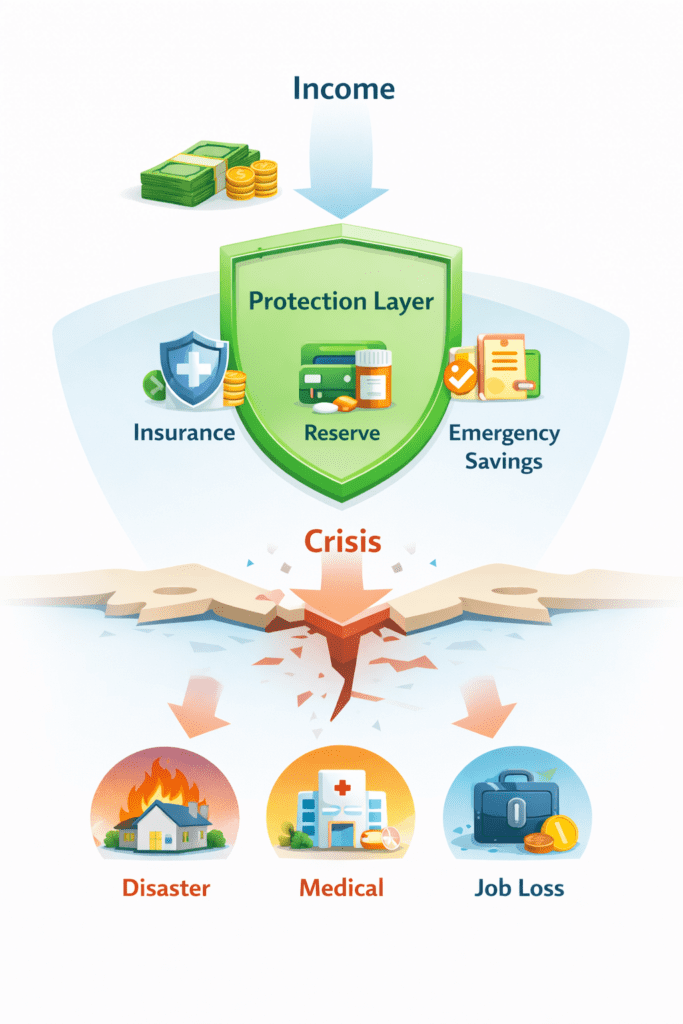

Bucket Two: Protection — Containing Risk

Protection is the most commonly neglected category—and the most emotionally expensive to ignore.

This bucket exists to prevent a setback from becoming a financial emergency.

Protection typically includes:

Emergency savings

Health insurance

Disability and life insurance where appropriate

Short-term cash reserves

Coverage for property and liability risk

For Gen X households in particular, this bucket is critical. Many are simultaneously supporting children, aging parents, mortgages, and careers that may not be as secure as they once were.

🛡️

RetireCoast Perspective

Protection isn’t pessimism—it’s planning.

Insurance, emergency reserves, and income safeguards are not about expecting

the worst. They exist to keep a temporary disruption from becoming a permanent

setback—especially during peak earning years.

Protection doesn’t generate excitement or visible progress. What it provides instead is time and options—two things that disappear quickly during a crisis.

Protection acts as a buffer between income and crisis, preventing unexpected events from becoming long-term financial damage.

Bucket Three: The Future — Creating Forward Momentum

The future bucket is where financial growth happens.

This includes:

Retirement contributions

Long-term investments

Education planning

Property upgrades

Travel and lifestyle goals

Legacy or estate planning

This bucket often gets treated as optional—something to fund “later.” The problem is that later usually arrives faster than expected.

Funding the future is not about predicting everything perfectly. It’s about giving compound growth time to work and ensuring that today’s comfort doesn’t undermine tomorrow’s security.

How This Builds Directly From Section III

Section III showed you how money moves before it reaches your hands. Section IV shows how to control what happens after.

The same logic applies:

Assign dollars automatically where possible

Separate purpose before spending begins

Reduce reliance on willpower and memory

When needs are stabilized, protection is in place, and the future is consistently funded, income stops feeling reactive—and starts feeling deliberate.

In the next section, we’ll turn this framework into something practical and repeatable: a system that adjusts as income rises, falls, or changes form.

Author’s Note: Needs vs. Wants

The dictionary defines a need as something essential or required,

while a want is something desired but not necessary.

On paper, the distinction is clear. In real life, the two are often confused.

Wants are not bad. Vacations, entertainment, and lifestyle upgrades are part of a

balanced life—but they must be planned. They should never replace managing

needs first.

In my years managing younger employees, I once saw someone run out of gas at a bar.

The reason wasn’t income—it was prioritization. The money went to drinks (a want)

instead of fuel for the car (a need). That single decision turned an inconvenience

into a crisis.

Financial stability comes from funding needs first—then planning wants so they can be enjoyed without creating risk.

Section V: Turning Allocation Into a Living System

Understanding income is important. Dividing income into needs, protection, and the future is essential. But financial strategies only become powerful when they move beyond concepts and turn into a living system—one that adapts as life changes.

RetireCoast Insight:

Financial strategies that rely on memory eventually fail. Systems that automate decisions

adjust automatically as income, expenses, and priorities change.

This section focuses on how to convert your allocation framework into something practical, repeatable, and resilient. Not a one-time setup. Not a rigid budget. A system that works whether income rises, falls, or shifts form entirely.

Why Static Plans Fail—and Systems Succeed

Many people approach money with static plans:

Fixed budgets that don’t adjust

Percentages copied from someone else’s situation

Rules that worked at 30 but fail at 45 or 55

The problem isn’t discipline—it’s rigidity.

Effective financial strategies behave more like operating systems than spreadsheets. They adjust automatically when:

Income changes

Expenses rise unexpectedly

Family responsibilities shift

Priorities evolve over time

A living system keeps decisions aligned without requiring constant attention.

📈

Future Bucket Growth Calculator

Model how monthly contributions and time can grow your Future bucket.

This supports financial strategies built on automation and consistency.

This is an estimate. Use conservative assumptions for planning.

Results

Year

Contributions

Growth

End Balance

Disclaimer: This tool assumes a steady monthly contribution and constant return rate for educational modeling.

Automation Is the Backbone of Sustainable Financial Strategies

If something depends on monthly willpower, it will eventually fail.

The most reliable financial strategies rely on automation:

Payroll deductions

Scheduled transfers

Account separation

Default decision-making

You’ve already seen this work in Section III. Taxes, insurance, and retirement contributions behave differently because they are automated before spending decisions begin.

That same logic should extend to:

Needs funding

Protection reserves

Future-oriented accounts

When money is assigned automatically, behavior improves without effort.

Author’s Note: Automation Reduces Stress and Cost

As an investor who owns—and has owned—many rental properties, I’ve spent years trying

to convince tenants to use their bank’s bill pay system to pay rent on time.

I’ve explained it in person and in writing.

They receive a paycheck on the 25th and could simply pre-schedule rent to be paid

automatically by the 1st. Done once, it runs every month. No late payments.

No late fees. No stress.

And yet, many couldn’t grasp how much easier life would be. Instead, they paid late

fees and created anxiety for everyone involved.

The same logic applies to a mortgage. If you have the money, why risk missing a payment

because you forgot—taking a credit hit in the process?

RetireCoast takeaway: Use automation to make life easier, reduce stress,

protect your credit, and spend less on unnecessary penalties.

Aligning the “Future” Bucket With Long-Term Strategy

The future bucket is where financial strategies either compound quietly—or fall apart slowly.

This is where tax efficiency, time horizon, and purpose matter most.

Rather than treating all savings the same, strong systems deliberately use:

Automation – Decisions happen without constant effort

Flexibility – Adjustments don’t require starting over

Alignment – Daily actions match long-term goals

These traits separate short-term tactics from durable financial strategies.

When income changes, the system adapts. When expenses rise, protection absorbs the shock. When priorities shift, the future bucket redirects—without chaos.

System Checkpoint:

Are needs funded automatically?

Does protection absorb surprises without panic?

Is the future growing even when life gets busy?

If any answer is “no,” the solution is not more effort—it’s system adjustment.

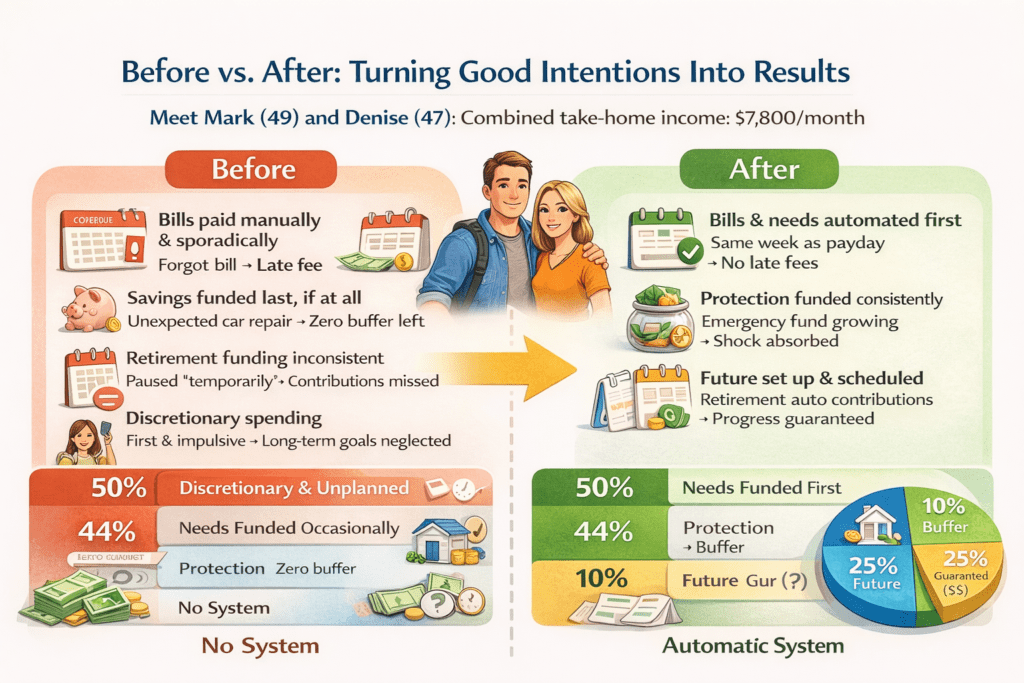

Case Study: Turning Financial Strategies Into a System That Actually Works

Meet Mark and Denise (A Gen X Household)

Mark (49) and Denise (47) both work full-time. Their combined take-home income averages $7,800 per month. On paper, they earn “good money.” In practice, they often felt behind.

They weren’t reckless spenders. They paid their bills. They contributed to retirement—when they remembered. And yet, surprises kept throwing them off balance.

Late fees appeared occasionally. Credit card balances lingered longer than planned. Retirement contributions were inconsistent.

Their problem wasn’t income. It was structure.

Before: Good Intentions, No System

Here’s how their money flowed before applying structured financial strategies:

Bills paid manually throughout the month

Retirement contributions adjusted “when things felt comfortable”

Emergency savings funded only if something was left over

Discretionary spending came first because it was visible and immediate

What went wrong:

A car repair wiped out most of their checking balance

A forgotten credit card payment triggered interest and a fee

Retirement contributions paused “temporarily” and stayed paused

They were reacting instead of directing.

Turning Good Intentions into Resuts

The Shift: Applying the Three-Bucket Framework

Instead of creating a stricter budget, Mark and Denise adopted a system-based approach:

Needs (Automated First)

Mortgage, utilities, insurance, groceries

Paid automatically within days of each paycheck

Protection (Made Invisible)

Emergency fund auto-transfer every payday

Insurance premiums consolidated and scheduled

Future (Committed, Not Optional)

Retirement contributions automated

Separate account for planned upgrades and travel

Discretionary spending still existed—but it was planned, not impulsive.

After: Same Income, Completely Different Outcome

Within six months:

No late fees

Emergency fund growing quietly

Retirement contributions happening every month

Fewer money-related arguments

Less anxiety around “what if” scenarios

Nothing dramatic changed. Their income didn’t increase. Their lifestyle didn’t shrink.

What changed was that their financial strategies became a system—one that worked even when they were busy, tired, or distracted.

Why This Case Study Matters

This example highlights a core truth:

Financial strategies don’t fail because people lack discipline. They fail because systems weren’t designed to survive real life.

Mark and Denise didn’t need better math. They needed automation, priority, and structure.

That’s what turns theory into results.

How to Apply This to Your Situation

You don’t need to copy their numbers. You need to copy the sequence:

Assign income before spending begins

Automate needs, protection, and future funding

Treat discretionary spending as planned—not leftover

This is how financial strategies become resilient instead of fragile.

How This Sets Up the Next Section

So far, you’ve learned:

How income actually flows

How to divide it intentionally

How to turn allocation into a system

The next step is learning how to stress-test that system—before life does it for you.

In the next section, we’ll examine:

Trade-offs

Decision points

Common failure patterns

How small adjustments prevent large setbacks

🧰

RetireCoast Insight: What Are “Sinking Funds”?

A sinking fund is money you set aside gradually for a known future expense.

It’s not an emergency fund. It’s a planned replacement or predictable cost fund.

Sinking funds turn “big, stressful bills” into smaller, manageable monthly transfers.

This is one of the simplest ways to make your financial strategy feel calm and controlled.

Common Sinking Funds

Auto insurance renewal (often increases year to year)

Vehicle maintenance & tires

Home repairs (plumbing, appliances, pest control)

Water heater / HVAC replacement

Property taxes or escrow shortages

Medical deductibles and out-of-pocket costs

Annual subscriptions and memberships

Travel or holiday spending (planned “wants”)

How to use them: Pick 3–5 predictable categories, estimate the annual cost,

divide by 12, and automate a monthly transfer into a separate savings bucket.

RetireCoast takeaway: Emergency funds cover the unexpected. Sinking funds cover

the expected—before it becomes urgent.

Section VI: Stress-Testing Your Financial Strategies Before Life Does

By this point, you’ve done something many people never do: You’ve moved beyond income awareness and budgeting concepts and built financial strategies that operate as a system.

But systems are only useful if they hold up under pressure.

This section is about stress-testing—not pessimism, not fear, and not worst-case obsession. It’s about confirming that your financial strategies can absorb disruption without forcing panic decisions.

Why Stress-Testing Matters More Than Perfect Planning

Most financial breakdowns don’t come from catastrophic events. They come from ordinary disruptions:

A temporary income dip

A surprise expense

A timing mismatch between bills and paychecks

Inflation quietly raising costs year after year

Without stress-testing, these moments feel personal and emotional. With it, they feel mechanical and solvable.

⚠️

RetireCoast Insight

Stress-testing removes emotion from financial decisions.

When people are under financial stress, they often react instinctively by reaching

for the largest visible pool of money—frequently a 401(k) or retirement account—

without fully understanding the penalties, taxes, and long-term damage involved.

This happened to me when I was younger. What felt like a quick solution to a

short-term problem turned into a long-term setback once taxes, penalties,

and lost compounding were accounted for.

Stress-testing helps prevent this reaction. By knowing in advance which bucket

absorbs a shock—and how long it can do so—you avoid turning a temporary disruption

into a permanent financial issue.

RetireCoast takeaway: The goal of stress-testing isn’t to predict

emergencies. It’s to stop panic decisions before they start.

Three Scenarios Every Household Should Test

You don’t need dozens of models. Most households only need to test three core scenarios.

Scenario 1: Income Disruption

Temporary job loss

Reduced hours

Commission or bonus volatility

Self-employment fluctuation

Key question: How long can your system function without changing behavior?

Scenario 2: Expense Shock

Medical costs

Car repair

Home system failure

Insurance deductibles

Key question: Does protection absorb the hit—or does it leak into credit cards and panic decisions?

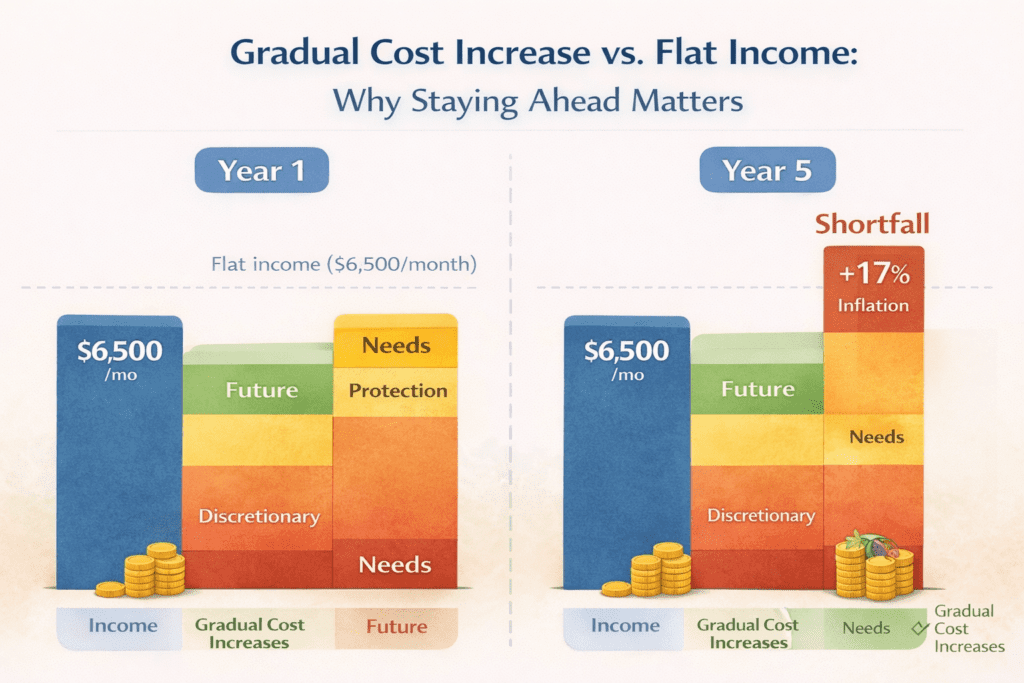

Scenario 3: Cost Creep (The Silent One)

Insurance renewals

Property taxes

Utilities

Food and fuel

Key question: Are you staying ahead of inflation—or reacting to it?

When income stays flat but costs rise gradually, financial stress builds quietly—making proactive planning and system adjustments essential.

This is where sinking funds quietly do their best work.

What Stress-Testing Reveals (And Why That’s Good News)

Stress-testing almost always reveals something:

A thin protection layer

Overcommitted discretionary spending

An underfunded replacement timeline

Too much reliance on memory instead of automation

This is not failure. It’s early warning—the most valuable kind.

Well-designed financial strategies don’t eliminate problems. They surface them while solutions are still inexpensive.

📉

RetireCoast Insight: Inflation Is Part of the Calculation

Inflation isn’t a one-time event—it’s cumulative. Each year’s increase

stacks on top of the last. During a recent four-year period, inflation rose into the

mid-20% range precisely because of this compounding effect.

Here’s how that works in simple terms. Assume inflation averages just

3% per year:

Year 1: $100 becomes $97.00

Year 2: $97.00 becomes $94.09

Year 3: $94.09 becomes $91.27

Year 4: $91.27 becomes $88.53

Year 5: $88.53 becomes $85.87

After five years, what once bought $100 worth of goods now buys less than $86.

Nothing dramatic happened in any single year—but the erosion is real.

RetireCoast takeaway: Financial strategies that ignore inflation quietly fail.

Systems that account for it—through sinking funds, future-bucket growth, and regular adjustments—

stay ahead instead of falling behind.

Adjusting Without Starting Over

One of the most important lessons for Gen X households is this:

You do not need to rebuild your financial life when something breaks.

You adjust in sequence:

Stabilize Needs

Protect the Protection layer

Temporarily adjust the Future bucket

Reduce or pause discretionary spending

Re-automate once stability returns

This hierarchy prevents short-term disruption from becoming long-term damage.

🔧

RetireCoast Insight

Adjust the system—don’t abandon it.

When life changes, the answer is rarely to start over. Most financial stress comes

from abandoning systems at the first sign of disruption instead of tuning them.

Strong financial strategies are designed to bend without breaking. Contributions

can be reduced temporarily. Timelines can shift. Priorities can be reordered.

The key is to preserve structure—especially automation—so progress resumes as soon

as stability returns.

RetireCoast takeaway: Systems survive disruption. Abandonment turns

short-term problems into long-term setbacks.

Stress-Testing Turns Financial Strategies Into Confidence

Confidence doesn’t come from knowing nothing will go wrong. It comes from knowing what happens when something does.

Households that stress-test:

Make fewer emotional decisions

Use less high-interest debt

Recover faster from setbacks

Stay invested in long-term goals

This is the quiet advantage of system-based financial strategies.

How Often Should You Stress-Test?

You don’t need to do this monthly.

A good rule:

Once per year

After major life changes

When income structure changes

When large expenses approach (college, retirement, relocation)

Think of it like a financial check-up—not an emergency room visit.

🧭

RetireCoast Checklist

When to Re-Run Your Financial Stress Test

You don’t need to stress-test constantly. Use this checklist to know when it’s

time to review and adjust your system.

Once per year as part of a regular financial checkup

After a job change, promotion, layoff, or income structure change

When moving from W-2 income to self-employment (or vice versa)

Following major life events (marriage, divorce, birth, caregiving responsibilities)

Before large, predictable expenses (college costs, relocation, major home repairs)

When inflation or insurance renewals materially increase monthly costs

If emergency or sinking fund balances are used significantly

When retirement contributions are paused or changed

RetireCoast takeaway: Stress-testing isn’t about expecting trouble.

It’s about confirming that your system still works as life evolves.

Where This Leaves You

At this point in the pillar, you’ve covered:

How income actually flows

How to assign income intentionally

How to build automation and structure

How to plan for predictable costs

How to test your system against reality

That’s not theory. That’s practical financial literacy.

In the next and final section, we’ll pull everything together into a simple, repeatable financial playbook—something you can revisit year after year without starting from scratch.

Final Capstone: Your Financial Strategies Playbook

By now, you’ve moved well beyond tips, rules of thumb, and abstract advice.

You’ve learned how income actually flows, how to divide it intentionally, how to build systems instead of relying on memory, how to plan for predictable costs, and how to stress-test your financial strategies before life forces the test on you.

That combination is what turns information into a playbook.

Not something you read once—but something you return to.

What This Playbook Does for You

A strong financial playbook doesn’t promise that nothing will ever go wrong. It does something far more valuable:

It reduces panic decisions

It keeps short-term disruptions from becoming long-term damage

It replaces reaction with structure

It gives you clear next steps when conditions change

Most importantly, it respects reality. Life evolves. Income changes. Costs rise. Priorities shift.

The goal isn’t perfection. The goal is continuity.

To help you apply what you’ve learned, RetireCoast provides a growing library of calculators designed to support real-world decision-making—not just theory.

👉 Explore the RetireCoast Calculators Hub Use calculators for retirement planning, income analysis, tax considerations, stress-testing scenarios, and more—all in one place.

A Practical Starting Point: Budget Planning

If you want a simple way to put structure around your needs, protection, and future buckets, start here. This planning tool is especially helpful for Gen X households juggling competing priorities.

Mr. Anderson is an expert in business management, real estate, finance, and wealth building.

Mr. Anderson has created several businesses including a multi-million dollar national business he sold to a Fortune 200 company. More than 1,500,000 visitors to Quora.com have read Mr. Anderson's answers to questions about real estate, investment, retirement, and other areas of his expertise.

Be sure to visit the About Us page to read Mr. Anderson's complete story.

Air Force veteran, real estate broker, investor, and founder of RetireCoast. I write about retirement planning, relocation, real estate, and launching second-act businesses.

Planning a trip to the Mississippi Gulf Coast?

Enjoy clean, comfortable homes just steps from the sand with

Christie’s Gulf Beach Rentals.

Ideal for families, couples, and long-term visitors.

RetireCoast is independently operated for readers who love retirement, coastal living, and real estate.

Explore our growing collection of articles about life in 1776,

the people of the Revolution, weapons, camp followers, women of the war,

and how America changed over 250 years. Many of our 250th Anniversary

articles are among the most-read and highly rated history features on RetireCoast.

{kind=link}

Listen to the author’s comments on this article: