If you’re a homeowner, chances are you’ve asked yourself at some point: Should I refinance my mortgage? It’s one of the most common questions in personal finance — and for good reason. Your mortgage is probably the largest debt you’ll ever carry, and even a small change in interest rates can translate into tens of thousands of dollars over the life of the loan. This article explores all facets of the question “Should I refinance my mortgage?”

UPDATED JUNE 2026

Refinancing simply means replacing your existing mortgage with a new loan — often with a lower interest rate, a different loan term, or new monthly mortgage payments that better match your budget. But deciding whether it’s the right move isn’t always easy.

That can be extremely tempting if you need funds for debt consolidation, home improvements, medical expenses, investing, or retirement planning. However, before you jump into a refinance, understand this important reality:

The amount being advertised is often subject to numerous conditions, qualifications, closing costs, fees, appraisal requirements, loan-to-value limits, and underwriting rules. In many cases, the actual amount available may be substantially lower than the marketing materials suggest.

Even more important, many homeowners are refinancing from historically low mortgage rates into loans that may carry interest rates 2% to 3% higher — or even more.

That increase can raise your monthly payment in two different ways:

- A larger loan balance because additional cash is being borrowed.

- A significantly higher interest rate than your existing mortgage.

Be extremely diligent before you leap. Carefully calculate the true payment increase, the total long-term interest cost, and whether your need for immediate cash outweighs the additional debt burden.

Use the free financial tools available in the RetireCoast Calculators Hub to estimate payments, compare scenarios, and determine whether the refinance truly fits your financial situation.

The idea of refinancing tends to gain attention whenever mortgage rates change significantly. In the early 1980s, homeowners saw rates skyrocket to nearly 17% — making refinancing nearly impossible. In contrast, during 2020–2021, mortgage rates dipped below 3% for a typical 30-year fixed-rate mortgage, leading to a historic refinancing boom.

Today, rates fluctuate between the mid-6% to 7% range, and homeowners once again wonder: Is this a good time to refinance?

🔑 Personal Story: My Refinancing Lesson

Many years ago, mortgage interest rates were in the double digits. I was fortunate to lock in a loan at 10.5%. When rates began to fall, I refinanced down to 8% — a huge improvement at the time. Unfortunately, my company transferred me just a year later, and I never recovered the cost of refinancing.

That experience taught me an important lesson: refinancing only makes sense if you can stay in the home long enough to reach the break-even point.

Years later, I refinanced again when rates dipped below 3%. This time, with no plans to move, I’ve already recouped the costs and continue to save money each month. The difference came down to timing and long-term planning.

The truth is, refinancing isn’t just about chasing the best rate. It’s about aligning your financial situation with your personal goals. Maybe you want a lower monthly payment so you can pay off credit cards faster, or you’d like to shorten your loan term to build equity before retirement. Others may be thinking about a cash-out refinance to fund home improvements or invest in a second property.

Of course, refinancing also comes with trade-offs. Closing costs can eat into your potential savings, and in some cases, you may restart the clock on a loan you’ve already been paying for years. Your credit score plays a role in whether you qualify for a better interest rate, and some loans — like FHA or VA loans — have specific waiting periods before you’re eligible to refinance.

This article is designed to cut through the confusion. We’ll break down:

- The best reasons to refinance your home loan.

- The costs and requirements you should expect.

- How to calculate your break-even point using a refinance calculator.

- Special considerations for FHA loans, VA loans, and USDA loans.

- When refinancing is a smart financial move — and when it’s not.

- Unique strategies for Gen-X homeowners preparing for retirement, Millennials building flexibility, and investors looking to leverage equity.

By the end, you’ll understand not only how refinancing works, but also whether it makes sense for you, right now.

- UPDATED JUNE 2026

- Quick Quiz: Should I Refinance?

- The 5 Best Reasons to Refinance Your Mortgage

- 2. To Change Your Loan Term

- Loan Term Trade-Off Tool

- 3. To Access Your Home Equity (Cash-Out Refinance)

- Cash-Out Refinance Impact Calculator

- 4. To Switch Mortgage Types

- Switching from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Loan

- Switching from FHA to a Conventional Loan

- Switching from Conventional to FHA or VA

- Special Case: VA IRRRL (Streamline Refinance)

- Switching to Jumbo or Non-Conforming Loans

- When Switching Loan Types Makes Sense

- When It Might Not Be the Right Move

- 5. To Eliminate Mortgage Insurance

- The Costs of Refinancing

- Refinance Break-Even Calculator

- Refinance Requirements and How Soon You Can Refinance

- The Break-Even Point: How to Know If Refinancing Really Saves You Money

- Generational Perspectives on Refinancing

- Conclusion: Is Refinancing the Right Move for You?

- FAQs: Everything You Need to Know About Refinancing

- 1. How soon can I refinance after buying a home?

- 2. Does refinancing hurt my credit?

- 3. Does refinancing reset my loan term?

- 4. What’s the difference between rate-and-term and cash-out refinancing?

- 5. Can I refinance if I have bad credit?

- 6. How do I calculate my refinance break-even point?

- 7. Is a no-closing-cost refinance really free?

- 8. Should I refinance to consolidate debt?

- 9. Can refinancing help during a divorce?

- 10. What are the alternatives to refinancing?

- Final Word

- Want more information about starting a business after retirement?

Quick Quiz: Should I Refinance?

Estimates principal & interest only. Verify program rules (PMI/MIP, VA/FHA/USDA seasoning, prepayment penalties) with your lender.

The 5 Best Reasons to Refinance Your Mortgage

1. To Lower Your Mortgage Interest Rate

The number one reason most homeowners refinance is simple: securing a lower interest rate. Your mortgage interest rate directly affects your monthly payment, the total interest you’ll pay over the life of your loan, and how quickly you build equity in your home.

Why Lowering Your Rate Matters

Think of interest as the “rent” you pay the bank for borrowing money. The higher your rate, the more you’re paying in interest each month instead of paying down your principal balance. A lower rate means more of your monthly mortgage payments go directly toward the loan balance, helping you build home equity faster.

Even small reductions in interest rates can produce big savings. For example:

- Loan amount: $300,000

- Original rate: 7.00%

- New rate: 6.00%

- Loan type: 30-year fixed-rate mortgage

At 7%, the monthly principal + interest payment is about $1,996. At 6%, it drops to about $1,799. That’s a difference of nearly $200 per month, or $72,000 over 30 years.

That $200/month savings could pay down credit cards, be invested for retirement, or go toward home improvements. Over time, the compounding effect of those savings can dramatically change your financial picture.

For a deeper look at refinance requirements and scenarios, see Freddie Mac’s refinancing basics.

The Role of Credit Score and Market Timing

Getting a better interest rate depends on two factors:

- Your credit score: Lenders reward higher scores with lower rates. A score above 740 often qualifies for the best rate, while a score in the 600s might mean you’ll pay a higher rate.

- Market conditions: Rates are influenced by broader economic forces, including inflation and policies from the Federal Reserve. Even if your credit hasn’t changed, a shift in market rates can make refinancing worthwhile.

When Lowering Your Rate Isn’t Worth It

A lower rate isn’t always a guaranteed win. Consider the following:

- Closing costs: If it costs you $6,000 to refinance, but your monthly savings is only $75, it may take over six years to break even. If you plan to move sooner, refinancing may not be a good idea.

- Loan term reset: Restarting a new 30-year loan late in your mortgage could mean paying more in total interest, even at a lower rate.

Best Practice: Run the Numbers

Use a refinance calculator to see how much you’ll save each month, and calculate your break-even point — the time it takes for savings to outweigh costs. For many homeowners, if you can reduce your current interest rate by 0.75–1.00% or more, refinancing is worth exploring.

👉 Lowering your rate is often the most straightforward reason to refinance, but as we’ll see, there are other equally important motivations depending on your financial situation and personal goals.

2. To Change Your Loan Term

One of the most strategic reasons to refinance is to change the length of your loan term. A mortgage term is simply the number of years you agree to take to repay your loan. Most homeowners start with a 30-year mortgage because it keeps monthly payments manageable, but refinancing into a different term can significantly reshape your financial future.

Loan Term Trade-Off Tool

Compare 30-, 20-, and 15-year optionsTip: Shorter terms raise the payment but slash total interest.

| Term | Monthly Payment | Total Interest | Total Paid | Years vs 30-yr |

|---|

Shortening the Loan Term

Many homeowners refinance into a 15-year mortgage (or even a 10-year or 20-year term) to pay off their homes faster.

Benefits of a Shorter Loan Term

- Less total interest: The shorter the loan, the less time interest has to accumulate.

- Example: On a $300,000 loan at 6.5%, a 30-year term costs about $383,000 in interest.

- The same loan over 15 years costs about $170,000 in interest.

- That’s a savings of $213,000 over the life of your loan.

- Build equity faster: More of each monthly mortgage payment goes toward principal instead of interest. This increases your home’s equity, giving you flexibility if you sell, refinance again, or need to borrow against it with a home equity loan or HELOC.

- Retirement planning: For Gen-X homeowners, refinancing into a shorter-term loan may align perfectly with the goal of entering retirement debt-free. Paying off a mortgage before leaving the workforce provides peace of mind and extra cash flow during the retirement years.

Challenges of a Shorter Loan Term

- Higher monthly payment: Even with a lower rate, the payment will be higher because you’re spreading the loan amount over fewer years.

- Example: $300,000 loan at 6.5%

- 30-year: $1,896/month

- 15-year: $2,613/month

- That’s a difference of $717 per month.

- Example: $300,000 loan at 6.5%

- Budget stress: A higher new payment may limit flexibility for emergencies, travel, or unexpected costs like medical bills or home repairs.

👉 Best for: Homeowners with stable income and strong savings who want to save the most on interest payments and shorten the life of their loan.

Lengthening the Loan Term

Not everyone wants to pay off their mortgage faster. Some homeowners refinance into a longer term — typically another 30-year loan — to reduce monthly mortgage payments.

Benefits of a Longer Loan Term

- Lower monthly payments: By spreading repayment over more years, your new payment drops.

- Example: $300,000 loan balance at 6.5%

- 20 years: $2,237/month

- 30 years: $1,896/month

- That’s a savings of $341 per month.

- Example: $300,000 loan balance at 6.5%

- Free up cash flow: Lower payments can provide relief if you’re juggling credit cards, personal loans, or other financial obligations. Many Millennials, for example, prefer the breathing room of a lower mortgage payment so they can invest in retirement accounts or pay down student loans.

- Avoid foreclosure risk: If you’re facing financial hardship, lengthening your loan term can make payments more manageable and prevent missed payments.

Drawbacks of a Longer Loan Term

- More total interest: Extending your loan term increases the amount of interest payments over the long run. Using the example above, the difference between a 20-year and 30-year term is about $82,000 in extra interest.

- Slower equity growth: It takes longer to build a home’s equity, delaying your ability to drop private mortgage insurance (PMI) or access cash through a refinance.

- Potential reset: If you’re already 10 years into a 30-year mortgage and refinance back into a new 30-year term, you’re essentially restarting the clock.

👉 Best for: Homeowners who need a lower monthly payment to balance their budget, free up cash flow, or weather financial uncertainty.

Which Choice Is Right for You?

Deciding between shortening or lengthening your loan term depends on your financial situation and personal goals:

- If your goal is to minimize total interest and become mortgage-free sooner, a shorter loan term makes sense.

- If your priority is monthly savings and budget flexibility, a longer loan term may be the better option.

- In some cases, refinancing into an intermediate loan term (20 years instead of 15 or 30) can provide a balance between manageable payments and reduced interest payments.

💡 Personal Story: Using Cash-Out for Investment

On more than one occasion, I used a cash-out refinance to purchase investment property. Before moving forward, I carefully evaluated the rental income, which was more than enough to cover the slightly higher house payment.

By refinancing when interest rates were dropping, I was able to lock in an even better deal. Long after I sold the original home, I still retained the investment property — a lasting financial benefit from that refinance decision.

3. To Access Your Home Equity (Cash-Out Refinance)

For many homeowners, the house isn’t just a place to live — it’s also their largest financial asset. Over time, as you make monthly mortgage payments and as your home’s value rises, you build equity. Equity is simply the difference between what your home is worth and what you still owe on your existing mortgage.

A cash-out refinance lets you tap into that equity by replacing your current loan with a new mortgage for a larger loan amount. The difference between the old balance and the new balance is paid out to you in cash at closing.

How a Cash-Out Refinance Works

Imagine your home is valued at $350,000 and you owe $200,000 on your current mortgage. If you refinance into a new loan of $280,000, the lender pays off the $200,000 balance and gives you $80,000 in cash (minus closing costs and application fees).

That cash is yours to use however you want — though how you use it makes a big difference in whether this is a smart financial move.

Cash-Out Refinance Impact Calculator

Estimate cash available, LTV, and the new paymentLTV = New loan ÷ appraised value. Lender/program LTV limits vary; verify with your lender. P&I only (excludes taxes/insurance/MI).

Max Loan Allowed (by LTV)

Requested New Loan

Post-Refi LTV

Remaining Equity

| Payment (P&I) | Total Interest (Remaining/New) | Total Paid (Remaining/New) |

|---|

Common Uses for a Cash-Out Refinance

- Home improvements

- One of the most popular uses is funding renovations that can increase your home’s value. Updating kitchens, adding bathrooms, or building energy-efficient features can provide both lifestyle upgrades and long-term return on investment.

- Debt consolidation

- Many homeowners use a cash-out refinance to pay off credit cards or other high-interest debt. For example, if you’re paying 20% on $30,000 of credit card debt, replacing it with a mortgage rate of 6% may save you thousands in interest payments.

- Example: Paying $30,000 at 20% interest costs $500/month just in interest charges. Replacing it with a mortgage loan at 6% spreads repayment over a longer term with far less interest.

- Education expenses

- Some families use cash-out funds to pay for college tuition instead of taking on personal loans or higher-interest private student loans.

- Investment opportunities

- A cash-out refinance can provide seed money for a new business, a second home, or an investment property. Used wisely, this strategy can build wealth — but it also introduces risk.

- Emergency reserves

- For homeowners without significant savings, tapping equity may be the only way to create an emergency fund for unexpected costs like medical bills.

The Federal Reserve’s consumer guide explains how refinancing impacts interest, payments, and total borrowing costs.

Benefits of a Cash-Out Refinance

- Lower interest compared to unsecured loans: Mortgage rates are almost always lower than rates on credit cards or personal loans, making this a cost-effective borrowing option.

- Single payment: Instead of juggling multiple debts, you have one monthly mortgage payment.

- Possible tax deduction: Mortgage interest may still be tax-deductible if funds are used for home improvements(consult a tax advisor).

- Stability: Unlike a HELOC, which has a variable rate, a cash-out refinance can lock in a fixed rate.

Risks of a Cash-Out Refinance

While tempting, cash-out refinances come with serious trade-offs:

- Larger loan = higher risk

- By increasing your loan amount, you reduce your home’s equity cushion. If housing values fall, you could end up owing more than your home is worth (negative equity).

- Restarting the clock

- If you refinance into a new 30-year loan, you may extend your debt decades into the future, even if your original mortgage was halfway paid off.

- Closing costs eat into cash

- Remember that application fees, title insurance, and origination fees will reduce the net cash you receive.

- Temptation to overspend

- If cash is used for vacations or nonessential purchases, you’re turning your home into an ATM and risking your long-term financial security.

Cash-Out vs. HELOC vs. Home Equity Loan

A cash-out refinance isn’t the only way to borrow against your home’s value. Here’s how it compares:

- Cash-Out Refinance

- Pros: Lower rate than unsecured loans, one payment, fixed term.

- Cons: Higher loan balance, higher closing costs, resets the mortgage term.

- Home Equity Loan

- Fixed-rate second mortgage.

- Pros: Lump sum, predictable payments, doesn’t reset your original loan.

- Cons: Usually a higher interest rate than a first mortgage, adds a second monthly payment.

- HELOC (Home Equity Line of Credit)

- Revolving line of credit with a variable rate.

- Pros: Flexibility — borrow what you need, when you need it.

- Cons: Payments can rise with interest rates, harder to budget.

👉 Rule of thumb:

- Choose a cash-out refinance if you also want a better interest rate on your full mortgage.

- Choose a home equity loan if you need a lump sum for a one-time project.

- Choose a HELOC if you need flexible access to funds over time.

When a Cash-Out Refinance Makes Sense

- You have at least 20% equity in your home.

- You plan to stay long enough to reach your break-even point.

- You’re using the cash for something that improves your financial position (paying down high-interest debt, funding home improvements, or investing in a rental property).

- You qualify for a better interest rate than your current rate.

When It’s Not a Good Idea

- You’ll spend the cash on depreciating items (cars, vacations).

- Your income is unstable, and a larger monthly payment would strain your budget.

- You’re close to retirement and don’t want to extend debt into your later years.

4. To Switch Mortgage Types

Another powerful reason to refinance is to change the type of loan you have. Different mortgages serve different purposes — some prioritize lower upfront costs, while others provide long-term stability. Refinancing gives you the opportunity to move from one loan type to another if your needs or financial situation have changed.

Switching from an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Loan

An adjustable-rate mortgage (ARM) starts with a low introductory rate, usually lasting 3, 5, 7, or 10 years. After that, the interest rate adjusts periodically based on market conditions.

- The upside: ARMs can be attractive because they often start with rates 0.5% to 1.0% lower than a comparable 30-year fixed-rate mortgage.

- The downside: Once the introductory period ends, your mortgage interest rate may rise significantly, which increases your monthly mortgage payments.

Example:

- Loan: $300,000 ARM at 5/1, initial rate 5%

- Monthly P&I during first 5 years: $1,610

- After 5 years, if rates rise to 7%, payment increases to $1,996 — a jump of nearly $400/month.

Refinancing into a fixed-rate loan locks in today’s rate for the life of the loan. This gives you predictability and stability in your budget.

👉 Best for: Homeowners who plan to stay in their house long-term and want to eliminate uncertainty around rising interest rates.

Switching from FHA to a Conventional Loan

Many first-time buyers use FHA loans because they allow for lower credit scores (580+) and smaller down payments (as low as 3.5%). The trade-off is that FHA loans come with mortgage insurance premiums (MIP).

- MIP rules:

- If your down payment was less than 10%, MIP lasts for the entire life of the loan.

- If you put down 10% or more, MIP drops off after 11 years.

That means FHA borrowers often end up paying hundreds extra each month in mortgage insurance premiums.

Example:

- $250,000 FHA loan at 3.5% down = $8,750 down payment

- Ongoing MIP = about $175/month (on top of your mortgage)

By refinancing into a conventional mortgage once you’ve built 20% equity, you can eliminate that MIP.

👉 Best for: Homeowners who’ve improved their credit score or increased their home’s value, making them eligible for conventional financing.

You can also explore CFPB’s refinance resources for plain-language answers about fees, timing, and mortgage rules.

Switching from Conventional to FHA or VA

Not all refinances are about dropping FHA insurance. Sometimes homeowners refinance into FHA or VA loans if their credit score has dropped or they need more flexible terms.

- Conventional → FHA: If you’ve experienced financial setbacks and now need more lenient qualifying rules, refinancing into an FHA loan could make sense — though you’ll take on MIP.

- Conventional → VA: Eligible veterans and service members can often refinance into a VA loan, which eliminates private mortgage insurance (PMI) entirely and may offer a lower interest rate.

Special Case: VA IRRRL (Streamline Refinance)

Veterans with existing VA loans may qualify for an Interest Rate Reduction Refinance Loan (IRRRL), also called a VA Streamline.

- Benefits: No appraisal, less paperwork, lower fees.

- Requirements: At least 210 days since closing and six on-time payments. Must demonstrate a net tangible benefit(like a lower payment or moving from an ARM to fixed).

Switching to Jumbo or Non-Conforming Loans

If your home’s value has increased and you need a larger loan beyond conforming limits (set by Freddie Mac and Fannie Mae), you might refinance into a jumbo loan.

- Pros: Access to more borrowing power, often needed in high-cost markets.

- Cons: Stricter requirements — higher credit score, lower DTI, and significant reserves required.

When Switching Loan Types Makes Sense

- You’re moving from an ARM to a fixed-rate loan for long-term stability.

- You want to refinance an FHA loan into a conventional loan to remove mortgage insurance.

- You’re a veteran moving into a VA loan for better terms and no PMI.

- You’ve built equity and can qualify for a better interest rate with a different loan type.

When It Might Not Be the Right Move

- If switching increases your closing costs without enough monthly savings.

- If you don’t plan to stay in your home long enough to reach the break-even point.

- If you’re moving into a riskier loan (e.g., refinancing into an ARM to lower payments temporarily, only to face higher rates later).

5. To Eliminate Mortgage Insurance

For many homeowners, especially first-time buyers, mortgage insurance was the price of entry into homeownership. If you didn’t put down at least 20% on a conventional loan or if you used an FHA loan, you were likely required to pay either private mortgage insurance (PMI) or mortgage insurance premiums (MIP). These costs add up quickly, and refinancing is often the only way to remove them before they expire.

💡 Did You Know? PMI Can Be Paid Up Front

With many conventional loans, you can choose to pay Private Mortgage Insurance (PMI) as a single upfront premium at closing instead of monthly. This can lower your monthly mortgage payment and may be covered by seller credits or builder incentives.

- Single Premium: Pay it all at once at closing.

- Split Premium: Pay part upfront, reduce the monthly PMI cost.

- Lender-Paid: The lender covers PMI, but your interest rate is slightly higher.

⚠️ Remember: If you sell or refinance early, you won’t get a refund on upfront PMI — in that case, monthly PMI might be the smarter move.

What Is Mortgage Insurance?

- Private Mortgage Insurance (PMI): Required for conventional loans if you put down less than 20%. PMI protects the lender, not you, in case you default. Costs typically range from 0.3% to 1.5% of the loan amount annually. On a $250,000 loan, that’s $750 to $3,750 per year.

- Mortgage Insurance Premium (MIP): Required for all FHA loans, regardless of down payment size. FHA borrowers pay both:

- An upfront MIP (usually 1.75% of the loan amount) at closing.

- An annual premium (0.45% to 1.05% of the loan balance) is added to monthly payments.

How PMI Works on Conventional Loans

With a conventional loan, PMI isn’t permanent. You can request cancellation once your loan-to-value (LTV) ratio reaches 80% — meaning you’ve built 20% equity. By law (under the Homeowners Protection Act), your lender must cancel PMI automatically once you reach 78% LTV, assuming you’re current on payments.

Example:

- $250,000 home with 10% down = $25,000. Loan amount: $225,000.

- PMI added = $150/month.

- After about 7–8 years of steady payments, your balance may fall below 80% LTV. PMI can then be dropped, reducing your monthly mortgage payments.

But here’s the key: if your home’s value has increased since you bought it, you might already have 20% equity — even sooner than expected. In that case, refinancing into a new conventional loan can eliminate PMI immediately.

How MIP Works on FHA Loans

With an FHA loan, things are trickier. For FHA loans issued after June 3, 2013:

- If your down payment was less than 10%, MIP lasts for the life of the loan.

- If you put down 10% or more, MIP drops off after 11 years.

That means many FHA borrowers are stuck paying MIP indefinitely unless they refinance into a conventional mortgage once they have 20% equity.

Example:

- $200,000 FHA loan with 3.5% down = $7,000.

- Upfront MIP = $3,500 (added to loan).

- Annual MIP = ~$140/month.

- Over 10 years, that’s more than $16,000 in premiums — just to insure the lender.

👉 Refinancing into a conventional loan when your credit score and home’s value allow it is often the best option to eliminate this cost.

Benefits of Refinancing to Remove Mortgage Insurance

- Lower monthly payment → PMI/MIP removal may cut $100–$300/month off your bill.

- Immediate savings → Unlike waiting years for automatic cancellation, refinancing lets you eliminate it now if you qualify.

- Better terms → If you’ve improved your credit score since buying, you may also qualify for a lower rate at the same time.

- More equity growth → Without insurance premiums dragging your payments, more of each monthly payment goes toward principal.

Risks and Considerations

- Closing costs: If you refinance only to remove PMI, ensure the closing costs don’t wipe out the savings.

- Loan term reset: Be careful not to restart a new 30-year mortgage late into your current one.

- Equity requirements: Most lenders require 20% equity to approve a new loan without mortgage insurance.

Case Study

- Sarah bought her home in 2020 with an FHA loan, putting down 3.5%. Her home cost $240,000, and she’s been paying $170/month in MIP.

- In 2024, her home appraised at $280,000, and her loan balance was down to $225,000. That’s 20% equity.

- By refinancing into a conventional mortgage, she eliminated MIP and lowered her rate slightly. Her new monthly payment dropped by $240/month, saving nearly $3,000 per year.

When Eliminating Mortgage Insurance Makes Sense

- Your home’s value has risen, and you’ve reached 20% equity.

- You originally used an FHA loan and want to remove MIP permanently.

- Your credit score has improved, making you eligible for conventional mortgage terms.

When It Might Not Be the Right Move

- If closing costs exceed the annual savings of dropping PMI/MIP.

- If you plan to sell in the next year or two — you may not recoup the costs.

- If refinancing would result in a higher interest rate than your current loan.

👉 For many borrowers, refinancing to remove mortgage insurance is one of the fastest ways to achieve meaningful monthly savings and move closer to long-term financial stability.

The Costs of Refinancing

While the promise of a lower interest rate or a lower monthly payment makes refinancing attractive, it’s critical to understand that refinancing is not free. Just like when you first bought your home, a refinance comes with closing costs and fees, which typically range from 2% to 5% of the loan amount. On a $300,000 mortgage, that could mean $6,000–$15,000 in costs.

These expenses can be paid in cash at closing, rolled into the new loan amount, or, in some cases, covered through a no-closing-cost refinance (which usually means accepting a slightly higher interest rate).

Here’s a breakdown of the most common refinancing costs and how they affect your decision:

Refinance Break-Even Calculator

Figure out if refinancing pays offAssumes fixed rates, principal & interest only (no PMI, taxes, or insurance).

Monthly Savings

Break-Even Point

| Payment (P&I) | Total Interest (Remaining/New) | Total Paid (Remaining/New) |

|---|

1. Origination Fee

- This is what lenders charge for processing your new loan. It’s usually 0.5% to 1% of the loan amount.

- Example: On a $250,000 refinance, a 1% origination fee = $2,500.

- Some lenders advertise “no origination fee” loans — but they may make up for it elsewhere, such as with a higher annual percentage rate (APR).

2. Application Fees

- Even before approval, some lenders charge application fees of $75–$500.

- These fees may cover initial administrative costs or pulling your credit report.

- Not all lenders require them, so it’s worth asking upfront.

3. Credit Report Fee

- Typically $30–$50, this covers the cost of checking your credit score with all three major bureaus.

- Even though this fee is small compared to others, multiple applications in a short period can result in several inquiries, potentially lowering your credit slightly.

4. Appraisal Fee

- Lenders almost always require a new appraisal to determine your home’s value.

- Expect $400–$800 depending on your location and property size.

- Some programs, like certain VA IRRRLs or streamlined FHA refinances, may waive the appraisal requirement.

5. Title Search and Title Insurance

- A title search ensures there are no liens or ownership disputes on your property.

- Title insurance protects the lender (and optionally you) against future title claims.

- Cost: $700–$1,200, though it varies by state.

6. Recording Fees and Taxes

- Local governments are responsible for recording your new loan and updating ownership records.

- These fees are generally smaller — a few hundred dollars — but unavoidable.

- Some states also impose mortgage taxes, which can add significantly to the cost.

7. Discount Points (Optional)

- A discount point is prepaid interest that lowers your rate.

- 1 point = 1% of the loan amount. On a $200,000 refinance, 1 point = $2,000.

- Paying points can make sense if you’ll keep the loan for a long time, but not if you expect to sell or refinance again within a few years.

Rolling Costs Into the Loan vs. Paying Upfront

- Pay upfront: Keeps your balance lower, saves money on interest payments over the life of the loan, but requires significant cash at closing.

- Roll into the loan: Avoids out-of-pocket costs but increases the loan amount, which means paying interest on your closing costs for years.

Example: $6,000 in closing costs rolled into a 30-year loan at 6.5% adds about $12,000 in total repayment over the life of the loan.

Tips to Manage Closing Costs

- Shop around: Closing costs vary by lender. Compare loan estimates side by side.

- Negotiate fees: Some “junk fees” (like courier charges or processing fees) can be reduced or waived.

- Consider no-closing-cost refinance: Accepting a slightly higher rate in exchange for waived fees may make sense if you don’t plan to stay long-term.

- Check for loyalty discounts: Some banks and credit unions reduce fees if you already have accounts with them.

👉 Bottom line: Always weigh the closing costs against your projected monthly savings. If you’ll stay in the home beyond the break-even point, refinancing often makes sense. If not, you may be better off waiting or considering alternatives like a HELOC.

Refinance Requirements and How Soon You Can Refinance

Refinancing isn’t just about wanting a lower interest rate — you also have to qualify. Lenders look at your credit score, income, home’s value, and other factors before approving a new loan. On top of that, certain loan types have waiting periods (called seasoning requirements) that determine how soon you can refinance after buying or refinancing.

Let’s break it down step by step.

Core Requirements Most Lenders Consider

- Credit Score

- Conventional loans usually require a 620 or higher.FHA loans allow for scores as low as 580, though better terms come with 620+.VA loans have no formal minimum, but lenders typically want 620+. Jumbo loans often require 700+.

- 740+ → Best rates, lowest fees.700–739 → Still competitive.660–699 → Higher rates, but refinance still possible.580–659 → FHA/VA options available, but conventional likely off the table.

- Debt-to-Income (DTI) Ratio

- Most lenders prefer a DTI under 43%, though some allow up to 50% with strong compensating factors. Formula: Total monthly debts ÷ gross monthly income.Example: If you earn $6,000/month and your debts total $2,400, your DTI = 40%.

- Loan-to-Value (LTV) Ratio

- LTV = Loan balance ÷ Appraised value of the home.

- Example: $200,000 loan ÷ $250,000 home = 80% LTV.

- Conventional lenders generally want ≤80% for the best terms.

- FHA and VA loans allow higher LTVs, sometimes up to 97% for rate-and-term refinances.

- Employment and Income Verification

- Expect to provide pay stubs, W-2s, or tax returns if self-employed.

- Lenders want consistent, stable income.

- Job changes aren’t disqualifying, but you may need extra documentation.

- Assets and Reserves

- Lenders like to see savings or investments that could cover several months of mortgage payments.

- Jumbo refinances often require 6–12 months of reserves.

- Property Appraisal

- Most refinances require a new appraisal to confirm your home’s value and equity.

- Some streamlined programs (VA IRRRL, FHA streamline) may waive this.

How Soon Can You Refinance? (Seasoning Rules by Loan Type)

Eligibility isn’t just about qualifications — sometimes you have to wait before you’re allowed to refinance.

| Loan Type | Waiting Period | Notes |

|---|---|---|

| Conventional Loan | No federal wait, but many lenders require 6 months | Immediate refi possible if switching lenders. |

| Conventional Cash-Out | At least 6 months ownership | Must have 20% equity post-refinance. |

| FHA Streamline Refinance | 210 days since closing + 6 on-time payments | Only for lowering the rate/term. |

| FHA Rate-and-Term | 6 months | No more than 1 late payment in past 12 months. |

| FHA Cash-Out | 12 months ownership + 6 on-time payments | Stricter requirements than streamline. |

| VA IRRRL (Streamline) | 210 days or 6 payments, whichever is later | Must show “net tangible benefit” (better rate or terms). |

| VA Cash-Out | Same as IRRRL (210 days or 6 payments) | Can go up to 100% LTV with some lenders. |

| USDA Loans | Usually 12 months | Streamlined options may allow sooner (6–12 months). |

| Jumbo Loans | Varies by lender | Often require 6–12 months seasoning. |

👉 Key takeaway: Conventional refinances are most flexible, but government-backed loans (FHA, VA, USDA) typically require at least 6 months of on-time payments before you can refinance.

Borrower Scenarios

Scenario 1: Sarah (Conventional → Conventional)

Sarah closed on her home 8 months ago with a 30-year fixed-rate mortgage at 7.25%. Rates have since dropped to 6.25%. Because she’s past the 6-month seasoning window, she can refinance immediately and save $180/month.

Scenario 2: David (FHA → Conventional)

David bought his home with an FHA loan at 3.5% down in 2022. He’s been paying $160/month in MIP. His home’s value has risen 15%, giving him 22% equity. By refinancing into a conventional mortgage, he eliminates MIP and saves over $200/month.

Scenario 3: Maria (VA IRRRL)

Maria, a veteran, bought her home with a VA loan 9 months ago. Rates dropped by 0.75%. She qualifies for a VA streamline refinance (IRRRL) since she’s made more than 6 payments and passed the 210-day mark. Her lender waives the appraisal, making the process quick and inexpensive.

Scenario 4: James (Cash-Out Refinance Too Soon)

James wants to tap into equity for home improvements, but he bought his home just 4 months ago. Because conventional cash-out refis require 6 months of ownership, he’ll have to wait 2 more months before applying.

Practical Tips

- Know your seasoning period: Ask your lender upfront if you’re eligible now or must wait.

- Improve your credit before applying: Even a small jump can improve your rate.

- Track your equity growth: Rising home values can speed up your timeline to drop PMI.

- Ask about streamlined programs: FHA and VA streamline refinances can save time and money by reducing documentation requirements.

👉 Refinancing eligibility is part math, part timing. Even if you’re motivated to refinance today, you may need to wait a few months depending on your loan type and lender. Use that time to strengthen your credit score, reduce your DTI, and prepare for the application process.

The Break-Even Point: How to Know If Refinancing Really Saves You Money

One of the most important — and overlooked — parts of deciding whether to refinance is calculating your break-even point. This is the moment when the savings from your new mortgage finally outweigh the costs of refinancing. If you sell your home or move before this point, refinancing may not make financial sense.

What Is the Break-Even Point?

The break-even point is the number of months it takes for your monthly savings from the refinance to equal the closing costs you paid.

Formula:Break-Even Point (months)=Closing CostsMonthly SavingsBreak-Even Point (months)=Monthly SavingsClosing Costs

Example:

- Closing costs = $6,000

- Monthly savings = $200

- Break-even = 30 months (2.5 years)

If you plan to stay in your home longer than 2.5 years, refinancing is likely a good idea. If you’ll move sooner, you may not recover the costs.

Scenarios to Illustrate the Break-Even Point

Scenario 1: The Quick Payoff Refi

- Current mortgage: $250,000 at 7.0%

- New mortgage: $250,000 at 6.0%

- Closing costs: $5,000

- Monthly savings: $165

5,000165≈30 months (2.5 years)1655,000≈30 months (2.5 years)

If the homeowner stays longer than 3 years, the refinance produces long-term savings.

Scenario 2: Small Savings, High Costs

- Current mortgage: $300,000 at 6.5%

- New mortgage: $300,000 at 6.25%

- Closing costs: $6,500

- Monthly savings: $95

6,50095≈68 months (5.7 years)956,500≈68 months (5.7 years)

If this homeowner plans to move in 5 years, the refinance won’t break even — even though the interest rate is lower.

Scenario 3: Cash-Out Refinance with Higher Payment

- Current loan balance: $200,000 at 5.5%

- New mortgage: $250,000 at 6.0% (includes $50,000 cash out)

- Closing costs: $7,000 (rolled into loan)

- Monthly payment increase: +$150

Here, there are no monthly savings — the break-even formula doesn’t work. Instead, you must ask: Will the $50,000 cash produce enough value (via debt consolidation, home improvements, or investments) to justify a higher payment and larger loan?

Scenario 4: Short-Term Homeowner

- Current balance: $175,000 at 7.25%

- New mortgage: $175,000 at 6.5%

- Closing costs: $4,000

- Monthly savings: $95

- Break-even = 42 months (3.5 years)

If the homeowner plans to relocate in 2 years, refinancing is not a smart financial move — they’d never hit the break-even point.

Using the Refinance Calculator Step by Step

- Enter your current loan details

- Balance, interest rate, and term.

- Example: $250,000, 7.0%, 30 years.

- Enter the new loan offer

- New interest rate, term, and whether you’re rolling costs into the loan.

- Example: $250,000, 6.0%, 30 years.

- Enter estimated closing costs

- Typically, 2–4% of the loan amount.

- Example: $5,000.

- Compare monthly payments

- Old payment vs new payment.

- Example: $1,663 → $1,498. Monthly savings = $165.

- Calculate the break-even point

- $5,000 ÷ $165 = 30 months.

- Project long-term savings

- If you stay in the home 10 years, you’ll save 120 months × $165 = $19,800 (minus $5,000 costs = $14,800 net savings).

Beyond the Numbers: Other Break-Even Factors

- How long will you stay? If you plan to move or sell soon, don’t refinance unless the savings are immediate.

- Will you restart your term? Refinancing a 20-year remaining loan into a new 30-year loan resets the clock, which can delay the break-even point even if payments are lower.

- Are you adding cash out? If yes, evaluate the use of that money. Paying off 20% credit cards may create value even if monthly payments rise.

- Tax implications: Mortgage interest may be deductible, but consult a tax advisor.

Rule of Thumb

- If you can reduce your interest rate by 0.75% to 1.00% or more and plan to stay in the home at least 3–5 years, refinancing often makes sense.

- Always run the numbers with a refinance calculator and compare scenarios — especially if you’re considering a cash-out refinance or a no-closing-cost refinance.

👉 The break-even point is the true test of whether refinancing is a smart financial move. Without this calculation, you risk saving a little each month but losing in the long run.

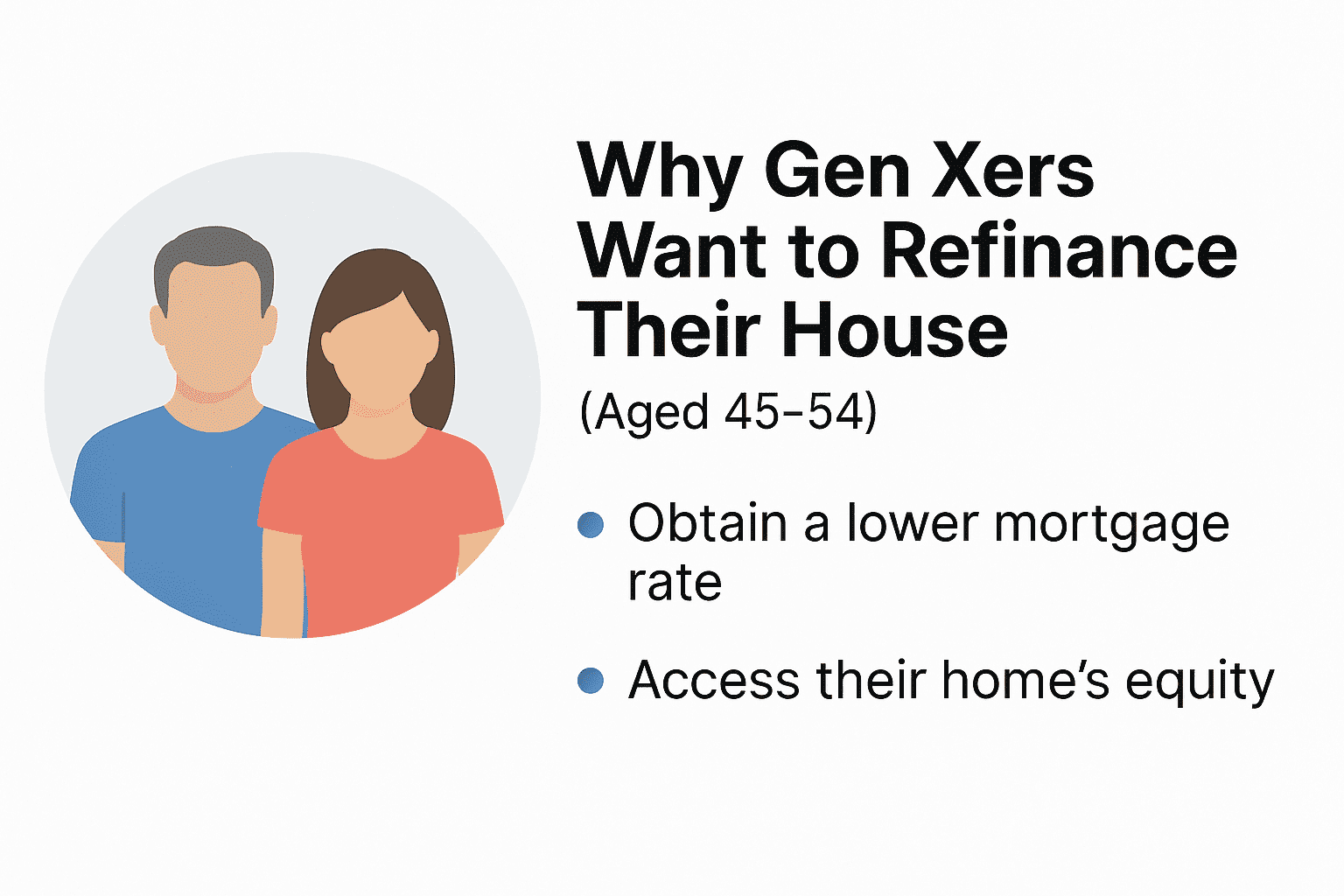

Generational Perspectives on Refinancing

Not all homeowners approach refinancing with the same goals. Age, financial stage, and life priorities shape whether a refinance is a good idea. A Gen-X homeowner nearing retirement, a Millennial juggling debt and family expenses, and a real estate investor leveraging equity all view refinancing differently. Let’s explore these perspectives.

Gen-X: Refinancing with Retirement in Mind

For Gen-Xers (born between 1965 and 1980), retirement is on the horizon — often less than 20 years away. Many are focused on entering retirement with no mortgage payment, freeing up income for travel, healthcare, or simply peace of mind. Read our article 21 Things You Must Know About Your Dream Home.

Goals

- Pay off the mortgage before retirement.

- Eliminate unnecessary expenses like PMI.

- Use equity strategically for home upgrades that improve long-term livability.

Common Refinance Strategies

- Shorten the loan term → Switching from a 30-year mortgage to a 15-year mortgage aligns payoff with retirement age.

- Lower rate, same term → Free up cash flow to boost retirement savings (401k, IRA).

- Remove PMI/MIP → Immediate monthly savings to accelerate retirement planning.

Case Study: Lisa, Age 52

- Current loan: $220,000 balance, 30-year mortgage at 6.5%, 20 years left.

- New loan: 15-year mortgage at 5.75%.

- Monthly payment increases from $1,394 to $1,835 (+$441).

- But she’ll save $89,000 in total interest and own her home free and clear by age 67 — perfect timing for retirement.

👉 For Gen-X, refinancing is often about aligning debt payoff with retirement, even if it means higher monthly payments in the short run. “Learn more in our Gen-X 20-Year Retirement Planning series

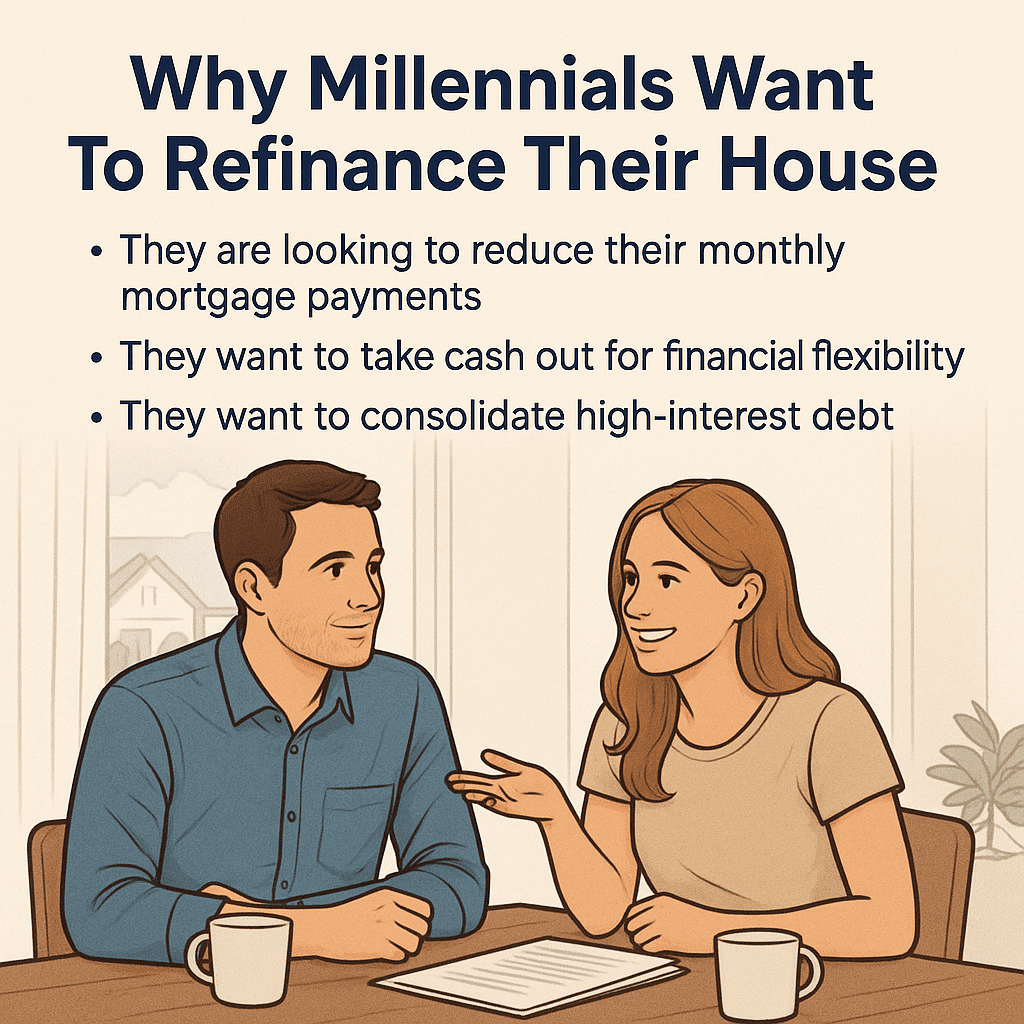

Millennials: Refinancing for Flexibility and Stability

Millennials (born between 1981 and 1996) are in the thick of life’s big expenses: raising kids, paying off student loans, or saving for future goals. For them, refinancing is less about early payoff and more about creating flexibility, stability, and lowering financial stress. See our full article on Millennial financial planning and refinancing strategies

Goals

- Lower monthly mortgage payments to free cash for other expenses.

- Refinance adjustable-rate mortgages into fixed-rate loans for stability.

- Tap into equity with a cash-out refinance to consolidate high-interest debt.

Common Refinance Strategies

- Lower monthly payment → Extending back to a 30-year fixed mortgage to reduce housing costs.

- Cash-out refinance → Pay off credit cards or student loans at a much lower interest rate.

- Switch loan type → Move from an ARM to a fixed-rate loan to lock in predictability.

Case Study: Brandon and Emily, Age 34 and 32

- Current loan: $280,000 at 6.75% ARM (adjusts in 2 years). Payment = $1,814.

- Refinance: 30-year fixed at 6.25%. Payment = $1,724.

- Savings: $90/month + stability (no rate hikes in the future).

- They also rolled $20,000 of credit card debt into a cash-out refinance. Their payment increased by $120, but they eliminated $600/month in credit card payments. Net monthly savings = $570.

👉 For Millennials, refinancing is often about balance — securing stability while creating budget flexibility for family, debt, and future planning.

Investors: Refinancing as a Wealth-Building Tool

For real estate investors, refinancing isn’t about personal monthly savings — it’s about leverage. By refinancing, they can pull out equity to buy more properties, improve cash flow, or shift into better loan terms to maximize returns.

Goals

- Access equity to buy additional properties.

- Reduce monthly expenses to improve cash-on-cash returns.

- Consolidate debt to simplify financial management.

Common Refinance Strategies

- Cash-out refinance on rentals → Pull equity to fund down payments on new acquisitions.

- Lengthen the term → Lower monthly payments to improve debt service coverage ratio (DSCR).

- Portfolio refinance → Combine multiple loans for better efficiency.

Case Study: Marcus, Real Estate Investor, Age 45

- Current loan: $150,000 balance on a rental property at 6.75%. Rent: $1,500/month, mortgage P&I = $972.

- New loan: Cash-out refinance to $200,000 at 6.5%. Payment = $1,264.

- He pockets $50,000 cash, which he uses as a down payment on another rental.

- Even though his payment rose $292, his rental still cash-flows positively ($1,500 – $1,264 = $236/month). With the new property, he doubles his income potential.

👉 For investors, refinancing is about long-term wealth building, even if it means higher debt balances. The risk? Over-leveraging during market downturns.

Key Takeaways by Generation

- Gen-X: Refinance to shorten the loan term, eliminate PMI, and align the payoff with retirement.

- Millennials: Refinance to lower payments, consolidate high-interest debt, and secure stability with a fixed rate.

- Investors: Refinance to leverage equity for new purchases, improve cash flow, and grow long-term net worth.

Refinancing isn’t one-size-fits-all. What makes sense for one generation may be a poor choice for another. The key is

Conclusion: Is Refinancing the Right Move for You?

Refinancing your mortgage can be one of the most powerful tools in personal finance — but only when used wisely. Done right, it can lower your interest rate, reduce your monthly mortgage payments, shorten the life of your loan, or unlock your home’s equity for debt consolidation, investments, or home improvements.

But refinancing isn’t a free lunch. Closing costs, application fees, and the possibility of extending your debt horizon must be factored in. The decision always comes down to three core questions:

- Will I stay in the home long enough to reach the break-even point?

- If you’ll move or sell in two years, and your break-even is four years, refinancing probably isn’t a good idea.

- Will this refinance help me achieve my financial goals?

- Gen-Xers might prioritize paying off the mortgage before retirement. Millennials might focus on lowering monthly payments to free up budget space. Investors might look at the refinance as leverage for building long-term wealth.

- Am I using refinancing as a tool, not a crutch?

- Refinancing can consolidate high-interest debt or fund home upgrades — but if the equity is being spent on vacations or depreciating assets, it may weaken your long-term financial security.

Why This Guide Is Different

Most lender-driven refinance articles end with a simple “compare rates now” pitch. But this guide digs deeper, showing you:

- The real math of refinancing with break-even examples.

- The costs and risks most lenders gloss over.

- Generational strategies for Gen-X and Millennials.

- Special rules for VA, FHA, USDA, and jumbo loans.

- The role of credit score, equity, and loan type in securing the best deal.

Refinancing can be a smart financial move — but only if it’s aligned with your unique financial situation and long-term goals. Check out our article about “What happens when you pay off your house.”

FAQs: Everything You Need to Know About Refinancing

1. How soon can I refinance after buying a home?

It depends on your loan type. Conventional loans often allow refinancing immediately, though most lenders prefer at least six months. FHA and VA loans usually require 210 days + six on-time payments. USDA loans require 12 months of history.

2. Does refinancing hurt my credit?

A refinance involves a hard credit inquiry, which may lower your credit score by a few points temporarily. Over time, though, making on-time payments on your new loan can improve your credit profile.

3. Does refinancing reset my loan term?

Yes — unless you specifically choose a shorter term. For example, if you’re 10 years into a 30-year mortgage and refinance into a new 30-year loan, you’ll start over at 30 years. To avoid this, consider refinancing into a 20- or 15-year mortgage instead.

4. What’s the difference between rate-and-term and cash-out refinancing?

- Rate-and-term refinance: Changes the loan’s rate, term, or both, without giving you extra cash.

- Cash-out refinance: Increases your loan amount so you can access equity in cash, often used for debt consolidation or home improvements.

5. Can I refinance if I have bad credit?

Yes, but options are limited. FHA loans allow scores as low as 580, and VA loans are flexible for eligible veterans. However, you may face a higher interest rate. Improving your score before refinancing usually saves thousands in the long run.

6. How do I calculate my refinance break-even point?

Divide your closing costs by your monthly savings. Example: $6,000 ÷ $200 = 30 months (2.5 years). If you’ll stay longer than 30 months, refinancing likely makes sense. Use our refinance calculator to run your own numbers.

7. Is a no-closing-cost refinance really free?

No. You won’t pay upfront, but lenders recover those costs by charging a slightly higher interest rate. This can be a good option if you plan to sell or refinance again in a few years, but it usually costs more over the life of your loan.

8. Should I refinance to consolidate debt?

It depends. Paying off credit cards at 20% interest with a mortgage at 6% is often a smart financial move. But be careful — you’re converting unsecured debt into debt secured by your home. If you fall behind, foreclosure becomes a risk.

9. Can refinancing help during a divorce?

Yes. Refinancing is often the only way to remove a spouse from the mortgage, ensuring only one person remains financially responsible. This also allows one spouse to “cash out” equity owed to the other.

10. What are the alternatives to refinancing?

- Home equity loan → Fixed-rate second mortgage, lump sum.

- HELOC → Revolving line of credit with variable rates.

- Loan modification → Sometimes offered if you’re struggling to make payments but don’t qualify to refinance.

Final Word

Refinancing is not a one-size-fits-all solution. For some, it’s the right move to save thousands and align with financial goals. For others, especially those planning to move soon or already deep into a 30-year loan, it may not make financial sense.

👉 The best next step? Use a refinance calculator, review your credit report, and talk with a trusted mortgage broker or loan officer. Armed with the information from this guide, you’ll be ready to make the best decision for your financial future. Thank you for reading our article. Hopefully, you have answered the question “Should I refinance my mortgage?

Want more information about starting a business after retirement?

Explore our Starting a Business After Retirement: Full Series Index for step-by-step guides, financing tips, tax strategies, and real-world case studies tailored for retirees.

View the Full SeriesB. The homeowner may receive a lower loan balance automatically

C. The refinance may include both a larger loan amount and a higher interest rate

D. Mortgage insurance is always eliminated

B. No, the amount depends on qualifications, appraisals, and underwriting rules

C. Yes, but only for government-backed loans

D. No, because refinance loans are illegal in some states

B. Because refinancing automatically shortens every mortgage

C. Because lenders are prohibited from charging closing costs

D. Because home insurance ends after refinancing

B. Focus only on the monthly payment

C. Use mortgage calculators to compare current and future costs

D. Refinance immediately before rates change again

B. It converts home equity into borrowed cash through a new mortgage loan

C. It lowers every homeowner’s interest rate automatically

D. It allows homeowners to skip property taxes

PODCAST

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}