Introduction

In this comprehensive guide on how to create a will, we will explain in plain English what all of the legal terms mean. This guide is provided as a public service by RetireCoast for our readers. It’s considered definitive meaning that it literally covers every element of a Last Will and Testament.

Have you ever been exposed to a situation where a family member or friend passed away and failed to let their heirs know their wishes through a will?

If you have, you already know how quickly things can become chaotic. Family members who are already dealing with grief suddenly find themselves trying to determine what their loved one wanted, who should receive certain assets, who should manage the estate, and in some cases, who should care for minor children.

What should be a time for healing can quickly turn into a stressful and emotionally draining process.

Prefer listening instead of reading? Every major RetireCoast pillar guide includes a complete audio edition so you can learn while commuting, exercising, traveling, or relaxing at home. The narration follows this article closely, allowing you to switch seamlessly between reading and listening whenever it’s most convenient.

- Introduction

- What Is a Will?

- A Will Is More Than a List of Assets

- Why Every Adult Should Consider Having a Will

- What Happens If You Die Without a Will?

- State Law Takes Control

- Your Family May Face Unnecessary Delays

- Minor Children Face Additional Uncertainty

- Family Disagreements Become More Likely

- Intestate Does Not Mean Simple

- The Good News

- Continue Building Your Estate and Financial Planning Knowledge

- Famous People Who Died Without a Will

- A Will Provides Clarity During Difficult Times

- A Will Is Often the First Step in Estate Planning

- What a Will Can and Cannot Do

- What a Will Can Do

- What a Will Cannot Do

- Why Many Estate Plans Include Both a Trust and a Will

- The Bottom Line

- The 15 Decisions You Must Make Before Creating a Will

- Decision #1: Your Personal Information

- Decision #2: Choosing Your Executor

- Decision #3: Naming an Alternate Executor

- Decision #4: Identifying Your Beneficiaries

- Decision #5: Choosing Per Stirpes or Per Capita Distribution

- Decision #6: Specific Gifts

- Decision #7: Minor Children

- Decision #8: Children With Special Needs

- Decision #9: Digital Assets

- Decision #10: Funeral and Final Wishes

- Decision #11: Bond Waiver

- Decision #12: No-Contest Clause

- Decision #13: Self-Proving Affidavit

- Decision #14: Alternate Beneficiaries

- Decision #15: Communicating Your Decisions

- The Good News

- How to Choose the Right Executor for Your Will

- What Does an Executor Do?

- The Biggest Mistake People Make

- Characteristics of a Good Executor

- Should Your Spouse Be Your Executor?

- Should You Name Co-Executors?

- Professional Executors

- Questions to Ask Before Naming an Executor

- Executor vs. Trustee

- The Bottom Line

- Understanding Per Stirpes vs. Per Capita: One of the Most Important Decisions in Your Will

- Why This Decision Matters

- What Does Per Stirpes Mean?

- What Does Per Capita Mean?

- Why Most Families Choose Per Stirpes

- A Real-World Example

- There Is No Right or Wrong Answer

- The Bottom Line

- Specific Gifts, Family Heirlooms, and Avoiding Family Disputes

- What Is a Specific Gift?

- Why Families Fight Over Small Things

- The Story of the Family Watch

- Make a List Before You Create Your Will

- Consider Talking With Your Family

- Fair Is Not Always Equal

- Consider a Separate Personal Property Memorandum

- The Goal Is Family Harmony

- A Valuable Lesson

- Guardianship for Minor Children and Planning for Special Needs Beneficiaries

- Why Guardianship Matters

- Choosing a Guardian

- Always Name an Alternate Guardian

- Should Guardians and Executors Be the Same Person?

- Planning for the Financial Needs of Minor Children

- Special Needs Beneficiaries Require Additional Planning

- Case Study: The Parents Who Planned Ahead

- The Real Purpose of Guardianship Planning

- Key Takeaway

- Digital Assets, Passwords, Cryptocurrency, and Online Accounts

- What Are Digital Assets?

- Why Digital Assets Matter

- The Family Photo Problem

- The Hidden Wealth Problem

- Cryptocurrency Requires Special Attention

- Your Executor Cannot Read Your Mind

- Creating a Digital Asset Inventory

- Social Media Accounts

- Online Businesses and Digital Income

- A Modern Estate Planning Necessity

- The Bottom Line

- Funeral Wishes, Final Arrangements, and Reducing Stress for Your Family

- Why Funeral Planning Matters

- The Financial Reality of Funeral Expenses

- Burial or Cremation?

- Military Honors

- Religious and Personal Preferences

- Prepaid Funeral Plans

- Don’t Leave the Family Guessing

- A Practical Suggestion

- Case Study: The Family That Didn’t Have to Guess

- The Bottom Line

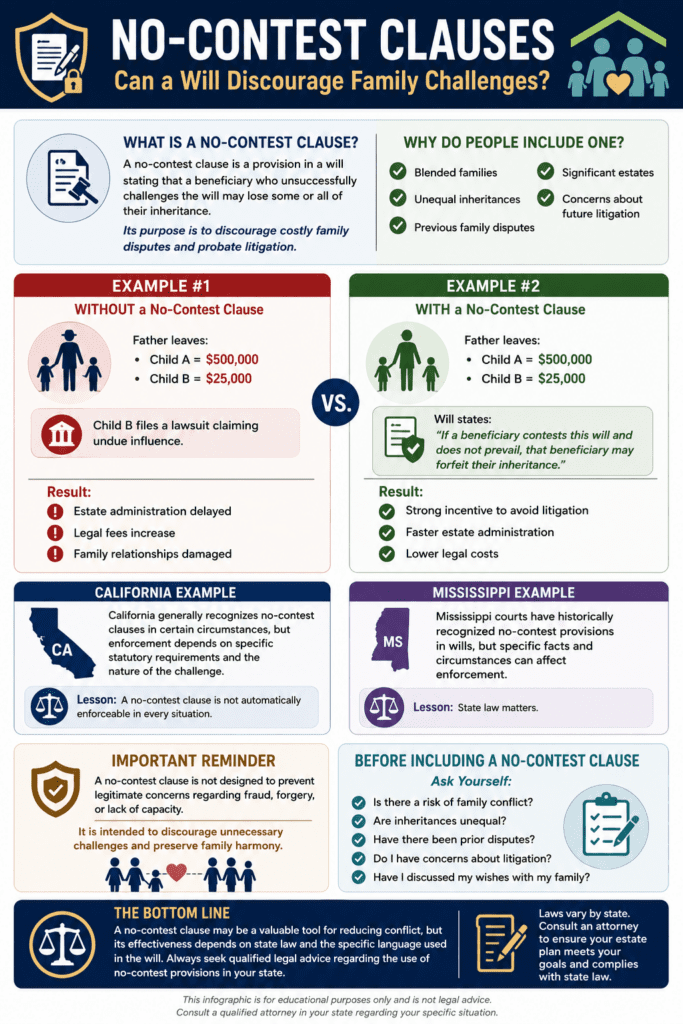

- No-Contest Clauses, Bond Waivers, and Self-Proving Affidavits: Small Clauses That Can Make a Big Difference

- What Is a No-Contest Clause?

- What Is a Bond Waiver?

- What Is a Self-Proving Affidavit?

- Why These Clauses Matter

- A Real-World Example

- The Bottom Line

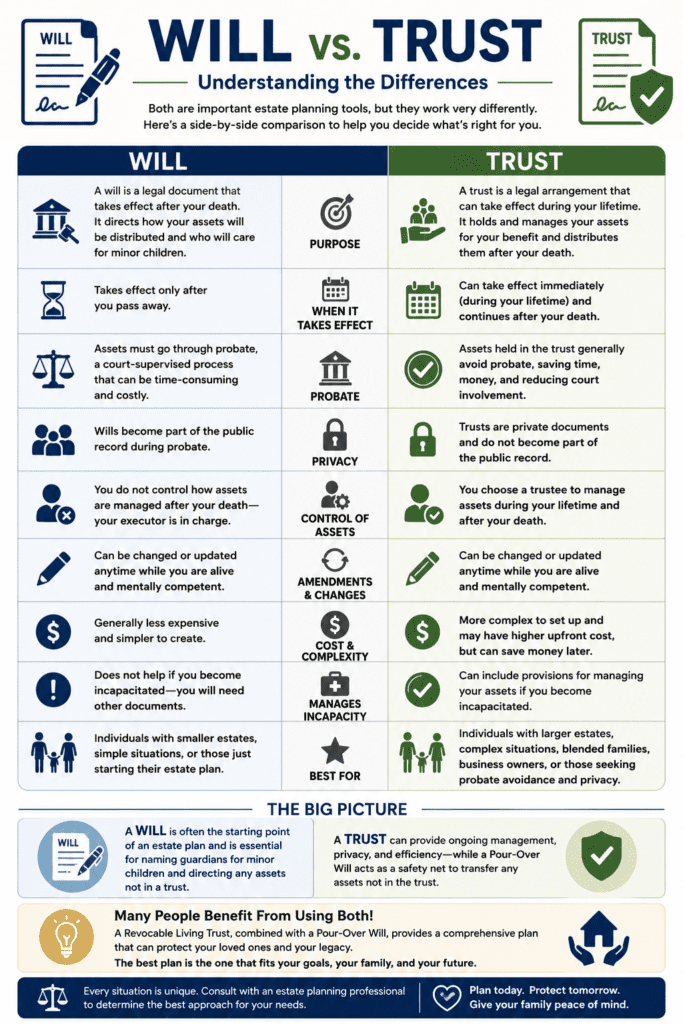

- Do You Need a Will, a Trust, or Both?

- What Is a Will?

- What Is a Revocable Living Trust?

- The Biggest Difference: Probate

- A Trust Does Not Replace a Will

- What Is a Pour-Over Will?

- Who Might Benefit From a Trust?

- Who Might Start With a Will?

- Case Study: The Couple Who Started Small

- Case Study: The Family Who Needed More Than a Will

- The Bottom Line

- “I Put My Adult Child on My Bank Account and My House Has a Mortgage. Why Do I Need a Will?”

- Case Study #2: Dad Put One Child on the Bank Account

- When Should You Update Your Will?

- Why Wills Become Outdated

- Major Life Events That Should Trigger a Review

- Retirement Is an Excellent Time for a Review

- How Often Should You Review Your Will?

- The Forgotten Documents Problem

- Case Study #3: The Will That Was Never Updated

- The Bottom Line

- Case Study #4: “Dad Took Care of Everything”

- Conclusion: The Greatest Gift You Leave Behind Is Peace of Mind

- Ready to Create Your Estate Planning Portfolio?

- References and Additional Resources

- FAQ

- PODCAST

Creating a will now can eliminate many of these problems and create a clear structure to ensure your wishes are fulfilled. It provides direction for your loved ones, reduces confusion, and often helps prevent disagreements that can permanently damage family relationships.

There is tremendous peace of mind that comes from knowing you have taken the time to organize your affairs and provide guidance to the people you care about most.

I understood this many years ago, which is why I created my own estate planning portfolio long before I ever thought I would need it. As a business owner, husband, father, and someone who has witnessed both successful and unsuccessful estate settlements, I realized that estate planning is not really about the person creating the documents.

It is about helping those left behind navigate a difficult period in their lives.

Part of my mission through RetireCoast is helping people improve their financial lives and make informed decisions about retirement, wealth preservation, and legacy planning.

Creating an estate planning portfolio often begins with a simple but critically important document—a Last Will and Testament or, in many cases, a Pour-Over Will that works alongside a Revocable Living Trust.

Our Estate Planning Membership was created specifically to help individuals and families work through this process. Inside the membership, you will find tools, worksheets, educational resources, and document builders designed to help you organize your information and create a comprehensive estate planning portfolio.

Whether your goal is to create a basic will, establish a living trust, appoint powers of attorney, prepare healthcare directives, or organize important financial information, the membership provides a structured path to help you accomplish those goals.

Understand what estate planning is

Before you begin creating your will, it is important to understand that estate planning is much more than deciding who gets your property. You will need to think about executors, beneficiaries, guardians for minor children, specific gifts, digital assets, healthcare decisions, funeral wishes, charitable gifts, and many other topics that people often overlook.

The more thoughtful your planning process, the easier it will be for your loved ones to carry out your wishes.

This article is intentionally comprehensive. It will take some time to read, but I encourage you to invest that time. The knowledge you gain here will help you better understand the estate planning process and prepare you to make informed decisions when creating your own will.

More importantly, it will help you avoid many of the common mistakes that families make when they postpone planning or fail to communicate their intentions.

You will learn what you can and cannot do!

As we move through this guide, you will learn what a will can and cannot do, how to select an executor, how to protect minor children, how to distribute assets fairly, how to avoid common estate planning mistakes, and when it may be appropriate to consider additional planning tools such as a Revocable Living Trust.

By the time you finish reading, you will have a much clearer understanding of the decisions that need to be made and the steps required to create an estate plan that reflects your values, protects your family, and preserves your legacy.

Let’s begin with a simple question: What exactly is a will, and why is it one of the most important documents you will ever create?

A Revocable Living Trust only controls assets that were actually transferred into the trust. If an account, vehicle, personal item, or piece of property was left outside the trust, the trust may not control it after death.

That is why many trust-based estate plans also include a Pour-Over Will. It acts like a safety net, directing assets left outside the trust to be transferred into the trust after death.

A will can also name guardians for minor children, appoint an executor, and provide backup instructions for property that was not properly titled in the trust.

What Is a Will?

A will, sometimes called a Last Will and Testament, is one of the foundational documents of a comprehensive estate plan. It is a legal document that allows you to specify how your assets should be distributed after your death, who will manage your estate, and who will care for your minor children if both parents pass away.

While most people understand that a will distributes property, many do not realize how many important decisions are contained within this single document. A properly drafted will can help reduce confusion, prevent family disputes, and provide clear instructions to the people responsible for carrying out your wishes.

Simply put, a will allows you—not the state government or a probate court—to make decisions regarding your estate.

A Will Is More Than a List of Assets

One of the biggest misconceptions about wills is that they are simply documents used to divide money and property.

In reality, a will can address many important issues, including:

- Who receives your assets

- Who serves as executor of your estate

- Who serves as an alternate executor

- Who cares for your minor children

- How specific family heirlooms are distributed

- Whether distributions should be made per stirpes

- Funeral and burial preferences

- Charitable gifts

- Instructions regarding digital assets

Many families discover that the emotional value of certain items greatly exceeds their financial value. A family Bible, grandfather’s watch, military medals, photo albums, jewelry, firearms, or collectibles can become sources of disagreement if your wishes are not clearly documented.

A well-prepared will helps eliminate uncertainty.

The legal term is called “dying intestate.” While that may sound like legal jargon, what it really means is that you failed to provide instructions for what should happen to your family, your assets, and in some cases, your minor children.

In simple terms, Judge Bubba will decide for you.

A judge you have never met and who knows nothing about your family, values, relationships, or personal wishes will be required to follow state law when determining who receives your assets and, in some situations, who may become the legal guardian of your children.

The court will not know:

- Which child should receive a family heirloom

- Who you trust most to manage your estate

- Your wishes regarding minor children

- Your charitable intentions

- Your concerns about specific beneficiaries

- Why you wanted certain assets distributed a particular way

Do you really want a stranger to interpret your final wishes without a roadmap?

A properly prepared will provides that roadmap. It tells your family, your executor, and the court exactly what you want to happen. Creating a will is one of the simplest and most important steps you can take to protect your loved ones and preserve family harmony after you are gone.

Why Every Adult Should Consider Having a Will

Many people delay estate planning because they believe they are too young, do not have enough assets, or assume everything will automatically pass to their spouse.

Unfortunately, life rarely follows a predictable schedule.

Consider the following situations:

- A married couple with young children.

- An unmarried couple living together.

- A business owner.

- A divorced parent.

- A retiree with investment accounts.

- A homeowner with significant equity.

Each of these individuals has reasons to create a will.

The reality is that estate planning is not reserved for the wealthy. In many cases, middle-income families have the most to gain because they often lack the financial resources to absorb lengthy probate proceedings, family disputes, and legal expenses.

What Happens If You Die Without a Will?

One of the most common misconceptions in estate planning is that if you do nothing, everything will simply “work itself out.”

Unfortunately, that is rarely the case.

When someone dies without a valid Last Will and Testament, the legal system considers them to have died intestate.

While the word sounds complicated, its meaning is simple:

You did not leave legally recognized instructions explaining what should happen to your estate.

Because no instructions exist, your state’s intestate succession laws determine who inherits your assets.

In other words, the government has already written a will for you.

The problem is that it almost certainly does not reflect your personal wishes.

State Law Takes Control

When there is no will, the probate court must follow state law.

The judge does not know:

- Who you trusted most.

- Which child cared for you during your final years.

- Which grandchild you wanted to receive your military medals.

- Which charity you hoped to support.

- Who should inherit sentimental family heirlooms.

- Your personal family relationships.

The court simply applies the law as written.

That may produce results you never intended.

Your Family May Face Unnecessary Delays

Without a will, someone must still settle your estate.

The probate court may need to:

- Appoint an estate administrator.

- Identify legal heirs.

- Determine who receives your assets.

- Resolve disagreements among family members.

- Supervise the administration of your estate.

This often creates additional paperwork, court hearings, legal expenses, and delays.

During an already emotional time, your family may spend months—or even years—resolving issues that could have been avoided with proper planning.

Minor Children Face Additional Uncertainty

If you have minor children, the consequences can be even more significant.

Without a will, you lose the opportunity to nominate the person you want to serve as their guardian.

Instead, the court must determine who will raise your children.

The judge will certainly try to make the best decision possible.

But no judge knows your family as well as you do.

Naming a guardian in your will provides valuable guidance and greatly increases the likelihood that your wishes will be followed.

Family Disagreements Become More Likely

Most families do not begin arguing because they are greedy.

They argue because they genuinely believe they know what their loved one would have wanted.

Imagine three adult children standing in their parents’ home after the funeral.

One believes Mom promised her the family piano.

Another remembers Dad saying the antique grandfather clock would someday belong to him.

The third insists everything should simply be divided equally.

Without written instructions, everyone believes they are honoring their parents’ wishes.

Unfortunately, nobody truly knows.

A properly prepared will removes the guesswork.

Intestate Does Not Mean Simple

Some people assume that if they do not have a will, the probate process becomes easier.

The opposite is often true.

Without clear instructions, the court must answer questions that you could have answered yourself while you were alive.

Creating a will allows you—not the court—to make those decisions.

The Good News

Fortunately, avoiding intestate succession is remarkably simple.

Creating a valid Last Will and Testament gives you the opportunity to:

- Choose your beneficiaries.

- Name an executor.

- Nominate guardians for minor children.

- Leave specific gifts.

- Provide guidance for your family.

- Reduce confusion and potential conflict.

The peace of mind that comes from having a will extends far beyond the legal document itself.

It comes from knowing your loved ones will not be left wondering what you wanted.

In the next section, we’ll look at several well-known individuals whose families experienced the very real consequences of dying without a will. Their stories demonstrate that estate planning is not about how much money you have—it’s about making life easier for the people you leave behind.ransfers those decisions to others.

Famous People Who Died Without a Will

Many people assume that wills are only necessary for the wealthy or those with large estates. History tells a very different story.

In fact, some of the most famous estate battles in modern history occurred because successful individuals failed to leave behind a valid will. The legal term for dying without a will is intestate. When this happens, state law—not personal wishes—determines who receives assets and who controls the estate.

When an ordinary family dies intestate, the results can be difficult. When a celebrity dies intestate, the consequences often become public, expensive, and incredibly chaotic.

The following examples demonstrate why having a will is one of the most important steps in protecting your family and preserving your legacy.

Prince (2016)

When music icon Prince passed away unexpectedly in 2016, he left behind an estate estimated at approximately $156 million, a vast music catalog, and hundreds of unreleased recordings.

What he did not leave behind was a will.

Because Prince had no spouse or living parents, numerous individuals came forward claiming to be heirs. Some claimed to be children, while others asserted family relationships that required extensive investigation and court review.

The result was years of legal battles and administrative proceedings before the courts ultimately determined the rightful heirs.

Lesson: Even extraordinary wealth cannot compensate for the absence of clear instructions.

Jimi Hendrix (1970)

Legendary guitarist Jimi Hendrix died at only 27 years old without a will.

While his estate was not considered enormous at the time of his death, the value of his music catalog and intellectual property rights grew dramatically over the following decades.

Because there was no will, ownership passed according to state law. After additional family deaths and changing circumstances, disputes arose regarding who should control the rights to Hendrix’s music and legacy.

The legal battles surrounding the estate continued for decades.

Lesson: Estate planning is not just about current assets. Future appreciation can create substantial value that your heirs may later fight over.

Aretha Franklin (2018)

When the Queen of Soul, Aretha Franklin, died in 2018, it was initially believed she had left no will for her estimated $18 million estate.

Under those circumstances, Michigan’s intestate succession laws would have determined how her estate was distributed among her heirs.

Months later, family members discovered multiple handwritten documents hidden in her home. Some were found in a locked cabinet while another was reportedly discovered in a notebook under a couch cushion.

The discovery sparked years of litigation as family members argued over which document reflected her true intentions and whether the handwritten documents qualified as valid wills.

Lesson: Even when instructions exist, failing to organize and properly document them can create confusion, delays, and significant legal expenses.

The Real Cost of Dying Intestate

The biggest misconception about wills is that they are primarily designed to save taxes.

While taxes may be a consideration for some estates, the most immediate benefit of a will is usually much simpler:

Clarity.

A properly prepared will tells your family exactly what you want to happen. It provides a roadmap for your executor, guidance for your beneficiaries, and instructions for the court.

Without that roadmap, surviving family members are often left to guess your intentions, and those guesses can lead to disagreements, lawsuits, and permanently damaged relationships.

The lesson from these famous cases is the same lesson that applies to every family: estate planning is not about how much money you have. It is about making life easier for the people you leave behind.

A Will Provides Clarity During Difficult Times

One of the greatest benefits of a will is not legal—it is emotional.

Family members are often dealing with grief, uncertainty, and financial concerns following the loss of a loved one. The last thing they need is confusion about your wishes.

A clear will provides direction.

Instead of arguing about what Mom or Dad “would have wanted,” family members can focus on supporting one another and carrying out the instructions already provided.

Many estate disputes begin not because family members are greedy, but because they genuinely believe they know what the deceased intended. A written will removes much of that uncertainty.

A Will Is Often the First Step in Estate Planning

For many individuals and families, creating a will is the first step toward building a complete estate planning portfolio.

As your financial situation grows more complex, additional documents may become appropriate, including:

- Revocable Living Trusts

- Pour-Over Wills

- Financial Powers of Attorney

- Healthcare Directives

- HIPAA Authorizations

- Trustee Selection Documents

- Asset Inventories

The good news is that creating a will forces you to begin thinking about these important issues. It helps organize your thoughts and establish the framework for a more comprehensive estate plan in the future.

Before you can create an effective will, however, it is important to understand exactly what a will can—and cannot—do.

The legal term is called “dying intestate.” While that may sound like legal jargon, what it really means is that you failed to provide instructions for what should happen to your family, your assets, and in some cases, your minor children.

In simple terms, Judge Bubba will decide for you.

A judge you have never met and who knows nothing about your family, values, relationships, or personal wishes will be required to follow state law when determining who receives your assets and, in some situations, who may become the legal guardian of your children.

The court will not know:

- Which child should receive a family heirloom

- Who you trust most to manage your estate

- Your wishes regarding minor children

- Your charitable intentions

- Your concerns about specific beneficiaries

- Why you wanted certain assets distributed a particular way

Do you really want a stranger to interpret your final wishes without a roadmap?

A properly prepared will provides that roadmap. It tells your family, your executor, and the court exactly what you want to happen. Creating a will is one of the simplest and most important steps you can take to protect your loved ones and preserve family harmony after you are gone.

What a Will Can and Cannot Do

One of the biggest misconceptions in estate planning is that a will controls everything you own and automatically solves all estate administration problems.

Unfortunately, that is not true.

A will is an incredibly important legal document, but it has limitations. Understanding what a will can and cannot do will help you determine whether a simple will is sufficient for your situation or whether additional planning tools such as a Revocable Living Trust should be considered.

Many people spend considerable time creating a will only to discover later that some of their largest assets pass outside of the will entirely.

Let’s look at the differences.

What a Will Can Do

A properly drafted will gives you significant control over your estate and allows you to make important decisions that otherwise would be left to state law.

A will can:

Name Your Beneficiaries

Perhaps the most obvious purpose of a will is deciding who receives your assets.

You may leave assets to:

- Your spouse

- Children

- Grandchildren

- Other family members

- Friends

- Charities

- Religious organizations

Without a will, state law generally determines who inherits your property.

Appoint an Executor

An executor is responsible for carrying out your wishes.

The executor may be responsible for:

- Filing probate documents

- Gathering assets

- Paying debts

- Filing tax returns

- Distributing property

- Closing financial accounts

Selecting the right executor is one of the most important decisions you will make.

Name Guardians for Minor Children

For parents, this may be the most important function of a will.

If both parents pass away while children are still minors, a will allows you to nominate the person you want to serve as guardian.

Without this guidance, the court may be forced to decide.

Distribute Specific Gifts

A will allows you to specifically identify who receives certain items.

Examples include:

- Jewelry

- Firearms

- Vehicles

- Family heirlooms

- Artwork

- Collectibles

- Family photographs

Specific gifts often prevent family disputes.

Explain Your Wishes

Some people include personal explanations regarding certain distributions.

These explanations may help family members better understand why decisions were made.

What a Will Cannot Do

Just as important as understanding what a will can do is understanding what it cannot do.

A Will Does Not Avoid Probate

This surprises many people.

A will actually serves as the instruction manual used during probate.

The existence of a will does not automatically avoid the probate process.

In many states, the will must still be submitted to the court for administration.

A Will Cannot Override Beneficiary Designations

Many financial accounts pass directly to named beneficiaries.

Examples include:

- Life insurance policies

- IRAs

- 401(k) plans

- Annuities

- Transfer-on-death accounts

- Payable-on-death accounts

If your beneficiary designation conflicts with your will, the beneficiary designation generally controls.

This is one reason why beneficiary reviews should be part of every estate planning review.

A Will Cannot Control Jointly Owned Property

Jointly owned assets often transfer automatically to the surviving owner.

Examples may include:

- Joint bank accounts

- Joint brokerage accounts

- Jointly owned real estate

These assets may pass outside of the will.

A Will Cannot Manage Assets During Incapacity

A will becomes effective after death.

If you become incapacitated due to illness or injury, your will generally provides no authority for someone to manage your finances or make healthcare decisions.

This is why many estate plans also include:

- Financial Power of Attorney

- Healthcare Directive

- HIPAA Authorization

A Will Cannot Control Assets Already Owned by a Trust

If assets have been transferred into a Revocable Living Trust, the trust—not the will—controls those assets.

This is where many people become confused.

The trust and the will often work together as part of a larger estate planning strategy.

Why Many Estate Plans Include Both a Trust and a Will

People often ask:

“If I have a trust, why do I need a will?”

The answer is simple.

A trust only controls assets that have actually been transferred into the trust.

A will serves as a backup plan for assets that were accidentally left outside the trust.

This is why many attorneys recommend a Pour-Over Will when creating a Revocable Living Trust.

The will acts as a safety net, directing remaining assets into the trust after death.

The Bottom Line

A will is one of the most important documents in your estate planning portfolio, but it is only one piece of the puzzle.

Think of your will as the foundation.

As your family grows, your assets increase, or your circumstances become more complex, you may need additional planning tools to fully protect your family and your legacy.

The next step is understanding the specific decisions you must make before sitting down to create your will. Most people are surprised to learn there are far more decisions involved than simply deciding who gets their property.

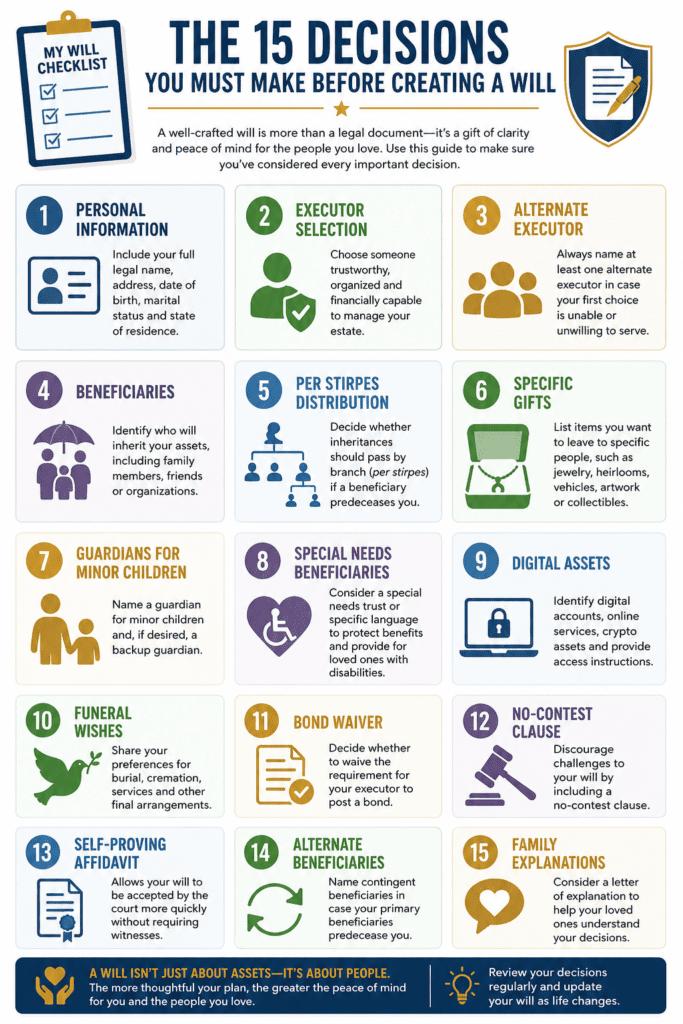

The 15 Decisions You Must Make Before Creating a Will

Many people assume that creating a will is simply a matter of deciding who gets the house, bank account, or family heirlooms.

In reality, creating a will requires a series of important decisions that affect your family, your beneficiaries, your executor, and potentially future generations.

This is one reason why so many people procrastinate. They sit down intending to create a simple will and quickly realize there are far more decisions involved than they expected.

The good news is that once you understand these decisions and work through them one at a time, the process becomes much easier.

In fact, the RetireCoast Will Builder was specifically designed to guide you through each of these decisions step-by-step so that you can create a comprehensive estate plan rather than simply filling in blanks on a legal form.

Let’s examine each decision in detail.

Decision #1: Your Personal Information

The first step seems obvious, but accuracy matters.

Your will should clearly identify:

- Your full legal name

- Current address

- State of residence

- Marital status

This information helps eliminate confusion and ensures there is no doubt regarding the identity of the person creating the will.

If you have recently moved, remarried, or changed your name, your estate planning documents should be updated accordingly.

Decision #2: Choosing Your Executor

Your executor is the person responsible for carrying out your instructions after your death.

Think of your executor as the project manager of your estate.

Responsibilities may include:

- Filing probate paperwork

- Gathering assets

- Paying debts

- Managing property

- Filing tax returns

- Distributing inheritances

The executor does not need to be your oldest child, closest relative, or spouse.

The best executor is usually the person who is:

- Organized

- Trustworthy

- Financially responsible

- Able to communicate effectively

Many people choose a spouse first and then designate an adult child or trusted family member as an alternate executor.

Decision #3: Naming an Alternate Executor

Life happens.

The person you originally select may:

- Pass away before you

- Become incapacitated

- Move away

- Decline to serve

Always name at least one alternate executor.

This simple step can save your family significant time and expense later.

Decision #4: Identifying Your Beneficiaries

A beneficiary is anyone who receives assets under your will.

Beneficiaries may include:

- Spouse

- Children

- Grandchildren

- Friends

- Charities

- Religious organizations

This is often where people begin thinking about fairness versus equality.

Those are not always the same thing.

One child may have already received substantial financial assistance during your lifetime. Another may have special needs. A third may have helped care for you during retirement.

These are personal decisions that only you can make.

Decision #5: Choosing Per Stirpes or Per Capita Distribution

This is one of the most important decisions in modern estate planning.

Most people have never heard the term “per stirpes” until they begin creating a will.

A simple example explains it best.

Suppose you have three children.

Each child receives one-third of your estate.

However, one child dies before you and leaves two children of their own.

Under a Per Stirpes distribution, that deceased child’s share passes to their children.

Many families prefer this approach because it preserves inheritance rights across generations.

Without a per stirpes provision, the outcome may be very different.

This is why the Per Stirpes option is pre-selected in our Will Builder. It reflects the choice most families make after understanding how the distribution works.

Decision #6: Specific Gifts

Specific gifts are individual items or assets you want distributed to particular people.

Examples include:

- Jewelry

- Watches

- Firearms

- Vehicles

- Family photographs

- Coin collections

- Military memorabilia

- Artwork

Many estate disputes involve items with little monetary value but tremendous sentimental value.

A five-dollar pocket watch may become the most contested item in an estate if everyone believes it should belong to them.

Being specific can eliminate confusion and prevent future arguments.

Decision #7: Minor Children

If you have minor children, this may be the most important decision in your entire will.

Who would raise your children if both parents pass away?

Many parents assume family members already know the answer.

Often they do not.

You should:

- Select a guardian

- Select an alternate guardian

- Discuss the decision with those individuals

Naming a guardian provides guidance to the court and significantly increases the likelihood that your wishes will be honored.

Decision #8: Children With Special Needs

Estate planning becomes more complex when a beneficiary has special needs.

A direct inheritance could potentially impact eligibility for certain government assistance programs.

In these situations, professional legal advice is often appropriate.

The goal is to provide financial support while protecting long-term benefits and care.

Decision #9: Digital Assets

A generation ago this decision did not exist.

Today many people have significant digital assets including:

- Email accounts

- Social media accounts

- Online photographs

- Cloud storage

- Cryptocurrency

- Online businesses

- Digital subscriptions

If nobody knows these assets exist, they may never be located.

A comprehensive estate plan should address digital assets and provide guidance regarding access and management.

Decision #10: Funeral and Final Wishes

Your family will appreciate having guidance during one of the most difficult periods of their lives.

Consider documenting:

- Burial or cremation preferences

- Religious services

- Memorial preferences

- Military honors

- Donation requests

The clearer your instructions, the easier it becomes for your family to honor your wishes.

Decision #11: Bond Waiver

Some wills waive the requirement that an executor obtain a bond.

A bond acts as a type of insurance policy protecting beneficiaries.

Waiving the bond requirement may reduce administrative costs and simplify the probate process.

Decision #12: No-Contest Clause

A no-contest clause discourages beneficiaries from challenging the will.

While state laws vary, these clauses can sometimes reduce the likelihood of litigation among family members.

They are particularly common in situations involving:

- Blended families

- Unequal inheritances

- Significant estates

- Prior family conflicts

Decision #13: Self-Proving Affidavit

A self-proving affidavit may help streamline probate administration.

This document is signed alongside the will and helps verify the authenticity of the document.

In many jurisdictions, this can reduce delays after death.

Decision #14: Alternate Beneficiaries

Never assume your primary beneficiary will outlive you.

Life is unpredictable.

Always identify backup beneficiaries who will inherit if the primary beneficiary is unable to receive their inheritance.

Decision #15: Communicating Your Decisions

This final decision may be more important than all the others.

A will is a legal document.

Communication is a family tool.

Many disputes arise because family members are surprised by what they discover after death.

You do not need to disclose exact dollar amounts.

However, discussing your overall intentions with your family can dramatically reduce misunderstandings and conflict later.

The Good News

At first glance, fifteen decisions may seem overwhelming.

Fortunately, most of these decisions only need to be made once and reviewed periodically as your life changes.

The reward for taking the time to work through them is substantial: peace of mind for you and clarity for the people you care about most.

Now that you understand the decisions involved, let’s look at one of the most important choices in the entire process—selecting the right executor to carry out your wishes.

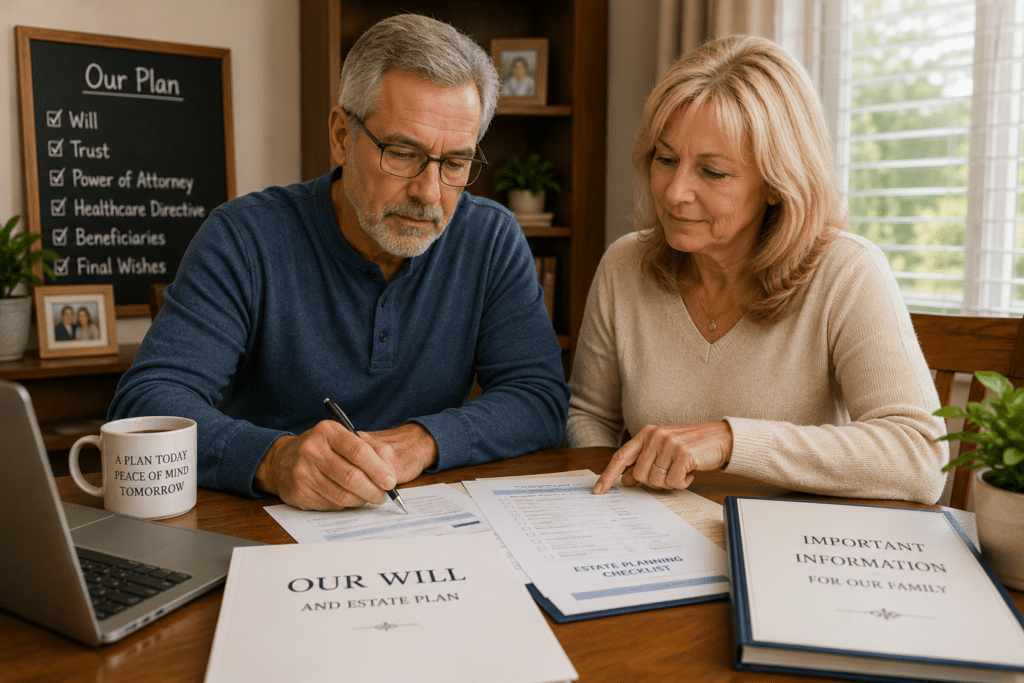

Harry and Jennifer spent several years preparing for retirement and understood that estate planning was not just about money. It was about reducing stress for their adult children and making sure their wishes were clear.

They created a Last Will and Testament, updated their beneficiary designations, organized their financial accounts, prepared healthcare directives, and later added a Revocable Living Trust with a Pour-Over Will.

More importantly, they talked with their three adult children. They explained who would serve as executor, how specific family items would be handled, and why certain decisions were made. No one had to guess. No one was surprised.

When Harry passed away unexpectedly, the family still grieved, but they were not forced to fight over missing instructions. Jennifer and the children had a roadmap.

The Result:

The estate transition was orderly, the family relationships remained intact, and the documents Harry and Jennifer created years earlier did exactly what they were intended to do: protect the people they loved.

How to Choose the Right Executor for Your Will

If your will is the roadmap for your estate, your executor is the person responsible for following that roadmap.

Many people spend considerable time deciding who should inherit their assets but give very little thought to who will actually carry out those instructions. In reality, choosing the right executor may be one of the most important decisions in your entire estate plan.

A great executor can make the administration of an estate efficient and relatively stress-free. A poor choice can lead to delays, confusion, family disputes, and unnecessary expenses.

Before naming an executor, it is important to understand exactly what the job involves.

What Does an Executor Do?

An executor is the individual responsible for administering your estate after your death.

Their responsibilities often include:

- Locating your will

- Filing probate documents

- Notifying beneficiaries

- Collecting and safeguarding assets

- Paying debts and taxes

- Closing financial accounts

- Managing real estate

- Distributing inheritances

- Maintaining records of estate transactions

In larger estates, the executor may work closely with attorneys, accountants, financial advisors, real estate professionals, and financial institutions.

The role can last several months and sometimes several years depending on the complexity of the estate.

The Biggest Mistake People Make

One of the most common mistakes is automatically naming the oldest child.

There is no law that says the oldest child should serve as executor.

Likewise, there is no rule requiring you to select:

- The oldest child

- The child who lives closest

- The wealthiest child

- The child who expects the role

The best executor is usually the person most capable of performing the job.

Sometimes that person is the oldest child.

Sometimes it is not.

Characteristics of a Good Executor

A strong executor is generally:

Organized

Estate administration involves paperwork, deadlines, financial records, and communication with multiple parties.

An organized person can dramatically simplify the process.

Honest

The executor owes a fiduciary duty to the beneficiaries.

They must act in the best interests of the estate rather than their own interests.

Financially Responsible

An executor does not need to be a financial expert, but they should be comfortable dealing with financial matters and keeping accurate records.

Able to Communicate

Family members often have questions.

A good executor communicates clearly and professionally.

Emotionally Stable

The executor is often dealing with their own grief while managing estate responsibilities.

Someone who can remain calm under pressure is often a better choice.

Should Your Spouse Be Your Executor?

For married couples, the surviving spouse is often the first choice.

This is perfectly reasonable in many situations.

However, you should always name at least one alternate executor in case:

- Both spouses die together

- The surviving spouse becomes incapacitated

- The spouse declines to serve

Never assume your primary executor will always be available.

Should You Name Co-Executors?

Some people name multiple children as co-executors in an effort to be fair.

While the idea sounds reasonable, it often creates complications.

If every decision requires agreement among multiple people, simple tasks can become difficult.

Examples include:

- Selling a home

- Closing accounts

- Hiring professionals

- Distributing assets

In many situations, naming one executor and one alternate executor is more practical.

Professional Executors

Some individuals choose:

- Attorneys

- Trust companies

- Banks

- Professional fiduciaries

This approach may be appropriate when:

- Family relationships are strained

- The estate is particularly large

- There is no suitable family member

- Significant business interests are involved

Professional executors generally charge fees but can provide neutrality and expertise.

Questions to Ask Before Naming an Executor

Before making your decision, ask yourself:

✓ Does this person handle their own finances responsibly?

✓ Can they work with family members who may disagree?

✓ Do they have the time to serve?

✓ Are they organized?

✓ Would I trust them with every asset I own?

✓ Have I discussed the role with them?

The last question is especially important.

Never assume someone is willing to serve.

Ask them.

Executor vs. Trustee

Many people become confused about the difference between an executor and a trustee.

An executor administers your estate after death.

A trustee manages assets held in a trust.

In some cases, the same person serves both roles.

In other situations, different individuals are selected.

As you continue building your estate planning portfolio, understanding these distinctions becomes increasingly important.

The Bottom Line

Choosing an executor is not a popularity contest.

It is a business decision made on behalf of your family.

Select the person most capable of carrying out your wishes, managing the estate responsibly, and communicating effectively with beneficiaries.

Your executor may ultimately determine whether your estate administration is smooth and efficient—or stressful and expensive.

Now that you understand the importance of selecting the right executor, let’s examine one of the most misunderstood estate planning concepts: Per Stirpes vs. Per Capita distributions and how those choices can affect future generations of your family.

One of the most important words in estate planning is fiduciary.

A fiduciary is a person who has a legal and ethical duty to act in someone else’s best interests rather than their own. In other words, a fiduciary must put your interests—or the interests of your beneficiaries—ahead of personal gain.

Think of it this way:

When you choose an executor, trustee, guardian, or agent under a Financial Power of Attorney, you are selecting someone who has a fiduciary responsibility. That person is legally expected to make decisions honestly, prudently, and solely for the benefit of you or your beneficiaries.

- Executor — Carries out the instructions contained in your will.

- Trustee — Manages property held in a trust for the benefit of beneficiaries.

- Agent under a Financial Power of Attorney — Makes financial decisions if you become unable to do so.

- Guardian — Cares for the personal well-being of a minor child or incapacitated adult.

RetireCoast Tip: When selecting any fiduciary, choose someone who is honest, organized, financially responsible, and willing to serve. The best choice isn’t always your oldest child or closest relative—it’s the person who will faithfully carry out your wishes and put the interests of your beneficiaries first.

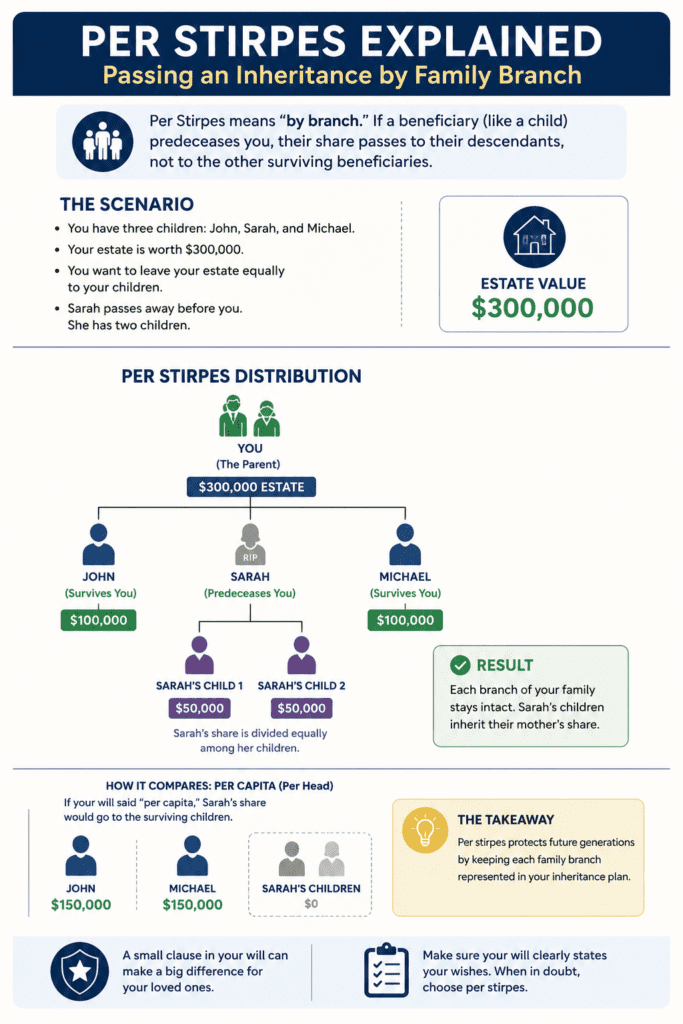

Understanding Per Stirpes vs. Per Capita: One of the Most Important Decisions in Your Will

If you remember only one legal term from this article, make it Per Stirpes.

This is one of the most important decisions you will make when creating a will, yet many people have never heard the term until they begin the estate planning process.

The good news is that the concept is much simpler than the Latin words make it sound.

In fact, understanding Per Stirpes can help ensure that your grandchildren and future generations are protected if something unexpected happens.

Why This Decision Matters

Most people assume that when they leave assets to their children, the assets will eventually stay within that child’s family line.

Unfortunately, that is not always what happens.

Consider a simple example.

You have three children:

- John

- Sarah

- Michael

Your will leaves your estate equally among your three children.

Everything seems straightforward.

However, what happens if Sarah dies before you?

Should Sarah’s share go to her children?

Or should Sarah’s share be divided between John and Michael?

The answer depends entirely on how your will is written.

This is where Per Stirpes and Per Capita become important.

What Does Per Stirpes Mean?

Per Stirpes is a Latin term that essentially means:

“By family branch.”

Under a Per Stirpes distribution, if one of your beneficiaries dies before you, that person’s share passes down to their descendants.

Let’s look at an example.

Example: Per Stirpes Distribution

You have a $300,000 estate.

You have three children:

- John

- Sarah

- Michael

Each child would receive:

- John = $100,000

- Sarah = $100,000

- Michael = $100,000

Now assume Sarah passes away before you and leaves two children of her own.

Under a Per Stirpes distribution:

- John receives $100,000

- Michael receives $100,000

- Sarah’s two children split her $100,000 share

Each grandchild receives $50,000.

Sarah’s family line remains protected.

This is why many families prefer Per Stirpes distributions.

What Does Per Capita Mean?

Per Capita means:

“By the head” or “equally among surviving beneficiaries.”

Using the same example:

You have:

- John

- Sarah

- Michael

Sarah passes away before you.

Under a Per Capita distribution:

- John receives $150,000

- Michael receives $150,000

- Sarah’s children receive nothing

Sarah’s share is redistributed among the surviving beneficiaries.

Some people prefer this method because it treats all living beneficiaries equally at the time of death.

Why Most Families Choose Per Stirpes

Most parents and grandparents want their descendants to remain represented even if one of their children dies before they do.

When people understand the difference, they often choose Per Stirpes because:

- It protects grandchildren.

- It preserves family branches.

- It reflects how many families naturally think about inheritance.

- It prevents one branch of the family from being unintentionally disinherited.

This is one reason the Per Stirpes option is commonly selected in our Will Builder.

A Real-World Example

Imagine a family farm that has been owned for generations.

The parents have three children.

One child dies unexpectedly but leaves behind two children who grew up working on the farm.

If the will uses Per Stirpes language, those grandchildren can inherit their parent’s share.

Without it, their inheritance may disappear entirely depending on how the will is written.

This single clause can have a significant impact on future generations.

There Is No Right or Wrong Answer

Per Stirpes is not automatically better.

Per Capita is not automatically worse.

The correct choice depends on your goals.

Ask yourself:

- Do I want my grandchildren to inherit their parent’s share if my child dies before me?

- Do I want assets distributed only among living beneficiaries?

- How important is preserving inheritance within each family branch?

Your answers will help determine which approach best reflects your wishes.

The Bottom Line

Many people spend more time deciding who receives a piece of jewelry or a vehicle than they spend thinking about how their estate will be distributed if a beneficiary dies before they do.

Yet this single decision can affect multiple generations of your family.

Fortunately, once you understand the difference between Per Stirpes and Per Capita, the choice often becomes much easier.

The next major decision involves another area that can dramatically affect family harmony after your death: how to handle specific gifts, family heirlooms, collectibles, and sentimental property.

Specific Gifts, Family Heirlooms, and Avoiding Family Disputes

One of the biggest mistakes people make when creating a will is focusing only on major assets such as homes, bank accounts, retirement accounts, and investment portfolios.

In reality, some of the most heated family disputes involve items with very little financial value.

Why?

Because emotional value and financial value are rarely the same thing.

A watch worth $50 may trigger more disagreement among family members than a bank account worth $50,000.

That watch may have belonged to a grandfather, been worn during military service, or have become a symbol of a cherished relationship. To the beneficiaries, it may be priceless.

This is why specific gifts are such an important part of estate planning.

What Is a Specific Gift?

A specific gift is an item or asset that you intentionally leave to a particular person.

Examples include:

- Jewelry

- Watches

- Firearms

- Vehicles

- Boats

- Family photographs

- Military medals

- Artwork

- Antiques

- Coin collections

- Musical instruments

- Family Bibles

- Collectibles

Rather than allowing beneficiaries to decide who receives these items after your death, you make the decision in advance.

This removes uncertainty and significantly reduces the likelihood of disagreements.

Why Families Fight Over Small Things

After many years in business and real estate, I have observed numerous estate situations involving families.

One lesson appears repeatedly.

Family disputes are rarely about money.

They are usually about emotions.

One child may believe they deserve a family heirloom because they spent the most time with a parent.

Another may feel entitled because they cared for a parent during illness.

A third may simply want the item because it reminds them of childhood memories.

None of these feelings are necessarily wrong.

The problem is that everyone may feel equally justified.

Without written instructions, disagreements can quickly develop.

The Story of the Family Watch

Imagine a father who owns a simple pocket watch.

The watch is not particularly valuable.

An appraiser might estimate its value at less than $100.

However, after the father passes away, all three children want the watch.

Why?

Because each remembers seeing their father wear it throughout their childhood.

Suddenly an item worth less than a restaurant dinner becomes the center of a family dispute.

The disagreement is not about the watch.

It is about memories.

A simple sentence in a will could have completely eliminated the conflict.

Make a List Before You Create Your Will

One of the best exercises you can perform before creating a will is to walk through your home with a notebook.

Make a list of items that may have either:

Financial Value

Examples include:

- Vehicles

- Jewelry

- Firearms

- Precious metals

- Artwork

- Collections

Sentimental Value

Examples include:

- Family photographs

- Military memorabilia

- Scrapbooks

- Heirloom furniture

- Wedding items

- Family keepsakes

You may be surprised how many items deserve consideration.

Consider Talking With Your Family

This may be one of the most valuable steps in the entire estate planning process.

Ask family members whether there are specific items that are particularly meaningful to them.

The answers may surprise you.

Sometimes two people want the same item.

Other times, an item you assumed everyone wanted is of interest to nobody.

Having these conversations while you are alive often prevents misunderstandings later.

Fair Is Not Always Equal

Parents often struggle with the difference between fairness and equality.

Suppose you have three children.

One child has always loved fishing and spent years fishing with you.

The other two have no interest in boats or fishing equipment.

Would it really be unfair to leave the boat and fishing gear to that child?

Not necessarily.

Many successful estate plans focus on honoring relationships and personal interests rather than creating perfectly equal distributions of every asset.

Consider a Separate Personal Property Memorandum

Some states allow a separate written list that identifies who should receive personal property.

This can be helpful because the list may be updated without rewriting the entire will.

Examples include:

- Father’s watch → John

- Military medals → Sarah

- Coin collection → Michael

- Family photo albums → Jennifer

Consult legal counsel regarding whether this approach is recognized in your state.

The Goal Is Family Harmony

When people think about estate planning, they often focus on legal documents.

The real objective is much broader.

The goal is family harmony.

Every instruction you provide removes uncertainty.

Every item you identify eliminates guesswork.

Every conversation you have with your beneficiaries reduces the potential for conflict.

A well-crafted will is not merely a document that distributes property.

It is a tool that protects relationships.

And in many cases, preserving family relationships becomes one of the most valuable gifts you leave behind.

A Valuable Lesson

Many people spend years accumulating assets but only a few hours thinking about how those assets will be distributed.

Take the time to identify the items that matter.

Document your wishes clearly.

Discuss them when appropriate.

The effort you invest today may prevent years of confusion and disagreement for your loved ones tomorrow.

Now let’s turn our attention to another critically important topic for parents and grandparents: selecting guardians for minor children and planning for loved ones who may require special care after you are gone.

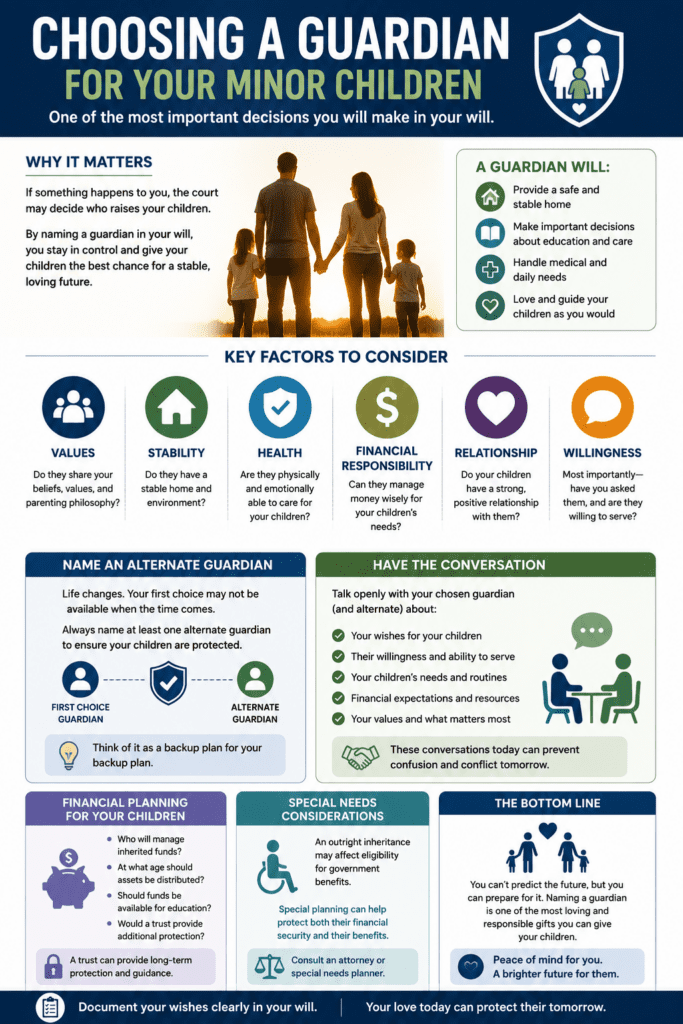

Guardianship for Minor Children and Planning for Special Needs Beneficiaries

If you ask most parents what their greatest concern is, few will mention bank accounts, investment portfolios, or real estate.

Most will answer the same way:

“My children.”

For parents of minor children, the guardianship section of a will may be the single most important provision in the entire document.

While many people think of a will as a tool for distributing assets, parents often use a will primarily to answer a much more important question:

Who will care for my children if I cannot?

Why Guardianship Matters

Imagine the unthinkable.

Both parents pass away unexpectedly while their children are still minors.

Someone must immediately make decisions regarding:

- Housing

- Schooling

- Medical care

- Daily supervision

- Financial support

- Religious upbringing

- General welfare

Without guidance from the parents, the court may be required to determine who will serve as guardian.

The judge will attempt to make the best decision possible, but the court cannot know your wishes as well as you do.

A will provides a roadmap.

Choosing a Guardian

Many parents assume the choice is obvious.

Unfortunately, it is often more complicated than expected.

Potential guardians may include:

- Grandparents

- Adult siblings

- Close friends

- Aunts and uncles

- Other relatives

When evaluating potential guardians, consider:

Values

Do they share your beliefs and parenting philosophy?

Stability

Do they have a stable home environment?

Health

Are they physically capable of raising children?

Financial Responsibility

Can they responsibly manage funds intended for the children’s benefit?

Willingness

Perhaps the most overlooked question:

Have you asked them?

Never assume someone is willing or able to serve as a guardian.

Have the conversation.

Always Name an Alternate Guardian

Life changes.

The person you select today may:

- Relocate

- Develop health problems

- Experience financial difficulties

- Become unable to serve

For this reason, every will should include an alternate guardian.

Think of it as a backup plan for your backup plan.

Should Guardians and Executors Be the Same Person?

Not necessarily.

Some families choose the same person.

Others separate the responsibilities.

For example:

- A sibling may be an excellent parent figure.

- Another sibling may be more financially organized.

In this situation, one person might serve as guardian while another serves as executor or trustee.

There is no single correct answer.

The goal is selecting the best person for each responsibility.

Planning for the Financial Needs of Minor Children

Naming a guardian solves only part of the problem.

Children also require financial support.

Questions to consider include:

- Who will manage inherited funds?

- At what age should children receive assets?

- Should distributions occur gradually?

- Should funds be available for education?

Many parents eventually determine that a trust structure provides additional protection and flexibility for minor children.

This is one reason Revocable Living Trusts are frequently used by families with young children.

Special Needs Beneficiaries Require Additional Planning

Estate planning becomes even more important when a child or beneficiary has special needs.

Parents naturally want to provide financial support and security.

However, an outright inheritance can sometimes create unintended consequences.

In certain situations, receiving assets directly may affect eligibility for government assistance programs.

This is why families with special needs beneficiaries should carefully evaluate their options and seek professional guidance when appropriate.

Case Study: The Parents Who Planned Ahead

David and Michelle had two children ages 8 and 11.

When creating their estate plan, they initially focused on who would receive their assets.

A financial advisor asked a simple question:

“Who would raise your children if both of you were gone?”

The question stopped them cold.

They realized they had never discussed it.

After several conversations, they selected Michelle’s sister as guardian and named a trusted family friend as alternate guardian.

They also purchased additional life insurance and created instructions regarding education and healthcare decisions.

Years later, both parents were still healthy and active.

The documents had never been needed.

But they both slept better knowing that if the unexpected occurred, their children would be protected.

The Real Purpose of Guardianship Planning

Many parents delay creating a will because discussing these topics feels uncomfortable.

That reaction is completely normal.

No parent enjoys thinking about scenarios where they are no longer present.

However, estate planning is not about predicting tragedy.

It is about preparing for uncertainty.

Creating a guardianship plan is one of the most loving acts a parent can perform.

It removes doubt.

It provides guidance.

And most importantly, it helps ensure that the people you trust most will be in a position to care for the people you love most.

Key Takeaway

If you have minor children, your will is about far more than money.

It is about protection.

Take the time to carefully consider who would step into your role if necessary.

Then document those wishes clearly.

Your children deserve nothing less.

In the next section, we will examine one of the fastest-growing areas of estate planning: digital assets, online accounts, passwords, social media profiles, and the hidden wealth that many families never discover after a loved one passes away.

You are obviously reading this article to learn more about creating a will. Most readers naturally think about themselves first. That is understandable.

As you work through this guide, also consider your adult children and how a will could benefit them.

A will is not only for older people, retirees, or individuals with significant assets. A will is a basic planning tool that every adult should consider.

Your adult children may have vehicles, bank accounts, pets, digital assets, personal belongings, minor children, or specific wishes that should be documented. Encouraging them to create a will now can help them protect their own families and avoid unnecessary confusion later.

Digital Assets, Passwords, Cryptocurrency, and Online Accounts

Twenty years ago, most estate planning discussions focused on homes, bank accounts, vehicles, retirement plans, and personal property.

Today, a significant portion of many people’s lives exists online.

In fact, some families spend months trying to locate digital assets after a loved one passes away. Others never find them at all.

This is one of the fastest-growing areas of estate planning and one of the most overlooked.

What Are Digital Assets?

Digital assets include far more than social media accounts.

Examples include:

- Email accounts

- Online banking

- Investment accounts

- Cryptocurrency wallets

- PayPal and payment accounts

- Cloud storage

- Family photographs

- Online businesses

- Websites and blogs

- Domain names

- Subscription services

- Reward programs and airline miles

- Digital music and media libraries

Many people are surprised to discover how much of their financial and personal lives exist online.

Why Digital Assets Matter

Imagine that you are the executor of an estate.

You know the deceased owned:

- Several bank accounts

- An investment account

- A website

- Cryptocurrency

- Thousands of family photographs

The problem?

You have no idea where any of it is located.

No passwords.

No account list.

No instructions.

You can quickly see why digital assets have become a major estate planning issue.

The Family Photo Problem

Let’s start with something simple.

Many families no longer store photographs in albums.

Instead, photos may exist in:

- Google Photos

- Apple Photos

- Dropbox

- OneDrive

- External hard drives

- Social media accounts

Without instructions, decades of family memories could become inaccessible.

Many people focus on financial assets while overlooking the emotional value of family photographs and videos.

The Hidden Wealth Problem

Now consider financial assets.

Every year, billions of dollars are transferred to state unclaimed property programs because heirs never locate accounts.

Common examples include:

- Forgotten bank accounts

- Brokerage accounts

- Savings bonds

- Online payment accounts

- Cryptocurrency holdings

If your family doesn’t know an account exists, they cannot claim it.

Cryptocurrency Requires Special Attention

Cryptocurrency creates unique estate planning challenges.

Unlike traditional bank accounts, cryptocurrency often depends entirely on access credentials.

If the wallet information, passwords, or recovery phrases are lost, the assets may become inaccessible forever.

There are stories of individuals whose families were unable to recover substantial cryptocurrency holdings because nobody knew how to access them.

Whether you own $500 or $500,000 in cryptocurrency, it should be documented as part of your estate plan.

Your Executor Cannot Read Your Mind

Many people assume family members will “figure it out.”

Unfortunately, that assumption is often wrong.

Your executor may not know:

- Which institutions you use

- What accounts exist

- Which subscriptions are active

- How to access important information

Creating a simple inventory can save hundreds of hours of work later.

Creating a Digital Asset Inventory

One of the best estate planning exercises you can perform is creating a digital asset inventory.

The inventory should identify:

Financial Accounts

- Banks

- Brokerage firms

- Retirement accounts

- Cryptocurrency platforms

Online Accounts

- Email providers

- Cloud storage

- Social media accounts

Important Websites

- Business websites

- Domain registrations

- Revenue-generating platforms

Password Management

Rather than listing passwords directly in your will, consider maintaining a secure password manager or separate confidential document that your executor can access when needed.

Social Media Accounts

Many people want instructions regarding:

- Facebook accounts

- Instagram accounts

- LinkedIn profiles

- X (formerly Twitter) accounts

- YouTube channels

Questions to consider include:

- Should the account be deleted?

- Should it be memorialized?

- Should family members have access?

Providing instructions can simplify these decisions.

Online Businesses and Digital Income

For some individuals, digital assets generate income.

Examples include:

- Websites

- Blogs

- Affiliate marketing businesses

- YouTube channels

- E-commerce stores

If these assets produce income, your executor should understand:

- How they operate

- Where revenue originates

- How expenses are paid

- How ownership can be transferred

Without documentation, a valuable online business can quickly lose value.

A Modern Estate Planning Necessity

A generation ago, estate planning focused primarily on physical property.

Today, comprehensive estate planning requires addressing both physical and digital assets.

Ignoring digital assets can create confusion, delays, and even permanent financial losses for your beneficiaries.

The good news is that organizing these assets is often easier than people expect.

A simple inventory, updated periodically, can provide tremendous value to your executor and family.

The Bottom Line

Your digital life is part of your estate.

The accounts, photographs, financial records, subscriptions, websites, and online assets you manage today may become important to your family tomorrow.

Taking the time to document them now is one of the most practical gifts you can leave behind.

Next, we’ll discuss another topic that many families avoid but every estate plan should address: funeral wishes, final arrangements, and how clear instructions can reduce stress during one of life’s most difficult moments.

One of the biggest challenges faced by executors and family members today is locating and accessing online accounts. A password manager can help solve this problem while improving your cybersecurity.

A password manager stores your usernames, passwords, and account information in an encrypted vault. Only individuals with the proper login credentials can access the information.

Unlike handwritten notebooks, sticky notes, or spreadsheets, a password manager reduces the risk of passwords being lost, forgotten, or falling into the wrong hands. It also makes it much easier for your executor or trusted family members to locate important accounts when the time comes.

Popular Options Include:

- Apple Passwords – Built into Apple devices and integrated across the Apple ecosystem.

- Bitwarden – A highly regarded password manager with a robust free version suitable for most users.

- Proton Pass – Designed with privacy and security in mind and popular among users seeking enhanced protection.

Some password managers require a subscription, while others offer free versions. For estate planning purposes, many people prefer a solution with a free tier so there is no concern about maintaining another monthly payment throughout retirement.

Estate Planning Action Item

If you use a password manager, be sure your spouse, executor, trustee, or another trusted individual knows how to access it in an emergency. A password manager is only valuable if someone can locate and access it when needed.

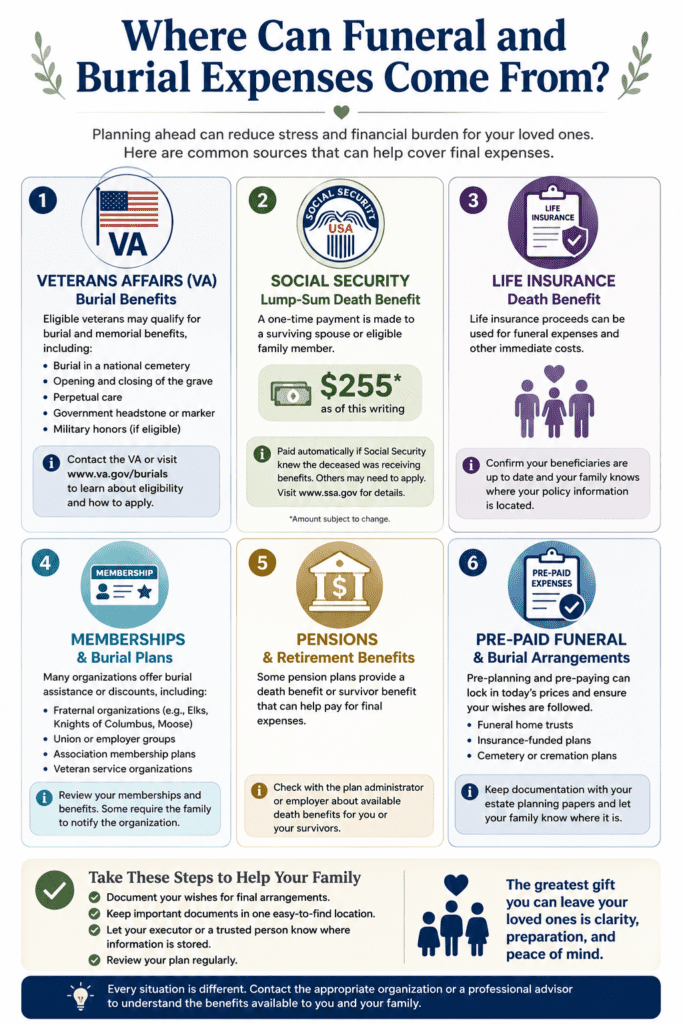

Funeral Wishes, Final Arrangements, and Reducing Stress for Your Family

Few estate planning topics are more uncomfortable to discuss than funeral arrangements.

Most people avoid the conversation entirely.

Unfortunately, that decision often transfers the burden to family members who are already dealing with grief, uncertainty, and emotional stress.

One of the greatest gifts you can leave your loved ones is clear guidance regarding your final wishes.

Why Funeral Planning Matters

When a death occurs, decisions often must be made quickly.

Family members may need to determine:

- Burial or cremation

- Religious services

- Funeral home selection

- Cemetery preferences

- Military honors

- Memorial services

- Obituary details

- Distribution of personal effects

Without guidance, family members may struggle to determine what you would have wanted.

Even well-intentioned relatives may disagree.

One child may believe you wanted burial.

Another may insist you preferred cremation.

A surviving spouse may have one opinion while adult children have another.

Clear instructions eliminate much of this uncertainty.

The Financial Reality of Funeral Expenses

Many people are surprised by the cost of final arrangements.

Expenses may include:

- Funeral home services

- Burial plots

- Cremation services

- Caskets or urns

- Headstones

- Flowers

- Transportation

- Clergy services

- Obituaries

- Reception expenses

The total cost can range from a few thousand dollars to well over ten thousand dollars depending on the services selected.

Planning ahead helps reduce financial stress for surviving family members.

Burial or Cremation?

One of the most important decisions involves burial versus cremation.

Neither choice is right or wrong.

The decision is highly personal and may be influenced by:

- Religious beliefs

- Family traditions

- Cost considerations

- Environmental concerns

- Personal preferences

The important thing is documenting your wishes.

Military Honors

Veterans may qualify for military funeral honors and burial benefits.

These may include:

- Honor guard services

- Presentation of the United States flag

- Taps ceremony

- Burial in a national cemetery (if eligible)

Many families are unaware of these benefits until after a loved one passes away.

Veterans should ensure discharge documents and military records are readily accessible.

Religious and Personal Preferences

Some individuals want detailed instructions.

Others prefer broad guidance.

Examples may include:

- Preferred clergy member

- Religious readings

- Favorite songs or hymns

- Charitable donations in lieu of flowers

- Celebration of life events

- Private family gatherings

Providing direction can make planning easier for your loved ones.

One of the most thoughtful gifts you can leave your family is a plan for your final expenses. Consider pre-paying for funeral services, cremation, burial arrangements, or other final wishes while you are alive.

By paying today, you may be able to lock in current pricing and remove both the financial burden and difficult decision-making process from your loved ones during an emotional time.

If you are a veteran, take time now to investigate the benefits available through the Department of Veterans Affairs. Eligible veterans may qualify for valuable burial and interment benefits, including burial in a national cemetery and military funeral honors.

Do not assume your family knows what benefits may be available. Gather your military records and discuss these benefits with your spouse, executor, or adult children so they know exactly what to do when the time comes.

Don’t Forget Social Security

As of this writing, Social Security provides a one-time lump-sum death benefit of $255 to certain eligible surviving family members. While this amount will not cover funeral expenses, it is a benefit that many families overlook during the estate settlement process.

Prepaid Funeral Plans

Some individuals choose to prearrange and prepay funeral expenses.

Potential benefits include: