Relocating for wealth preservation is not just about finding a lower tax state—it is about reducing your total financial burden, including housing costs, property taxes, sales taxes, and everyday living expenses. For many individuals and families, taxes represent one of the largest long-term expenses. But focusing only on income tax can lead to the wrong decision. A state with no income tax may still cost more overall due to higher housing prices, property taxes, insurance, or cost of living.👉 The real question is:

Will relocating reduce the total amount of money leaving your pocket each year?

- This Is About Dollars—Nothing Else

- 💡 The Shift: From “Lower Taxes” to “Lower Total Cost.”

- 🧠 Why This Matters More Than Ever

- 🔻 States Moving to Eliminate Income Taxes

- 🏠 States Considering Property Tax Reduction or Elimination

- 🛒 Sales Tax Shifts (Especially on Essentials)

- ⚠️ Important Reality: Tax Reductions Often Shift the Burden

- 🔄 Real-World Example

- 🧠 The Key Insight

- 👥 Who Benefits Depends on Your Profile

- 💼 The Emerging Risk: Wealth Taxes & High-Income Surtaxes

- ⚠️ Strategic Warning

- 📊 Final Takeaway

- 📊 What You Should Actually Measure

- ⚖️ The RetireCoast Principle

- 🧮 Next Step

- Run the Numbers Before You Move

- 💡 Why a Simple Calculation Can Change Your Decision

- 🎯 The Goal

- FINANCIAL SNAPSHOT TOOL

- ⚠️ Before You Interpret the Results

- 📣 What Comes Next

- How to Interpret Your Results (What Really Matters)

- 🧠 Look Beyond the Final Number

- 🔍 Identify Your Biggest Cost Drivers

- ⚠️ The Hidden Risk: Future Tax Changes

- 🧠 The Real Question You Should Be Asking

- 📣 Where the Free Tool Stops

- 🔓 The Smarter Approach

- 💡 Upgrade Your Analysis

- 🧱 Final Insight Before You Decide

- A Simple Framework for Making the Right Move

- 🧠 The RetireCoast Relocation Framework

- ⚖️ The Final Decision Filter

- 🔓 Go Beyond the Snapshot

- 🧠 Final Thought

- Premium Relocation Wealth Preservation Tool

- Core Purpose

- Step 1: Define the Household Profile

- Step 2: Model Current State Financial Pressure

- Step 3: Model Target State Financial Pressure

- Step 4: Identify the True Financial Drivers

- Step 5: Model Transition Costs and Break-Even

- Step 6: Scenario and What-If Modeling

- Step 7: Future Tax-Shift Risk Modeling

- Step 8: Estate and Inheritance Consideration

- Step 9: Decision Output

- Step 10: Interpretation and Guidance

- Key Benefit

- Final Principle

- QUIZ

- FAQ

This Is About Dollars—Nothing Else

This article is not about quality of life, parks, schools, or things to do.

It does not address cultural considerations such as conservative vs. liberal environments, lifestyle preferences, or community values—although all of these are valid and important reasons people choose to relocate.

👉 This article focuses on one thing:

Money.

More specifically:

Preserving your wealth and reducing the amount of money leaving your control each year.

That said, you may find that in the process of identifying financially efficient locations, you also discover:

- Strong school systems

- Appealing communities

- Lifestyle environments that align with your personal views

But those outcomes are secondary in this analysis.

The primary objective is clear:

Identify where your dollars go—and how to keep more of them.

🧠 Why This Conversation Is Happening Now

There is a growing trend across several states toward expanding tax structures beyond traditional income and property taxes.

For example:

- Washington has implemented wealth-based taxation measures

- California has explored wealth tax proposals

- New York has considered similar approaches

These policies are often positioned as targeting only the ultra-wealthy.

However, history suggests something important:

Tax thresholds can change over time.

What begins as a tax on billionaires or high-net-worth individuals may evolve into a broader application as states seek additional revenue.

👉 The concern is not just the tax itself—it’s the direction of policy.

I decided to create this article and the accompanying tools because of recent developments in state-level tax policy. States such as Washington, California, and New York either have implemented or are actively exploring wealth taxes.

Do not assume these taxes will remain limited to billionaires—or even millionaires, as currently framed in some proposals. These policies can establish a framework that allows thresholds to be adjusted over time.

The goal here is not fear—it is awareness. Ignoring early signals in tax policy shifts can have long-term financial consequences.

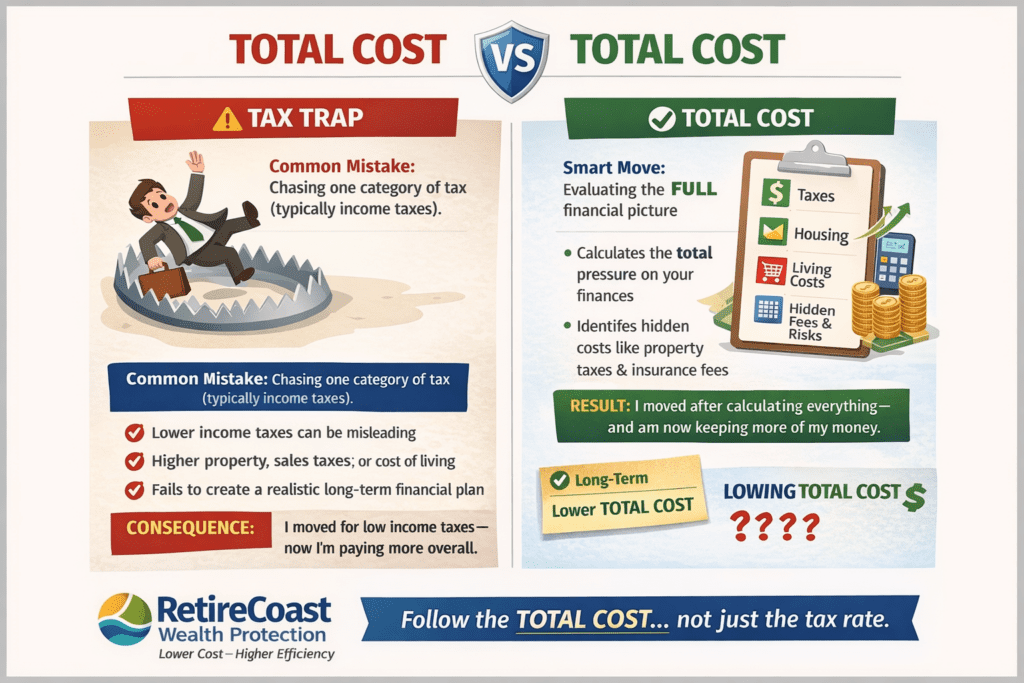

💡 The Shift: From “Lower Taxes” to “Lower Total Cost.”

Most relocation advice focuses on one factor: income tax.

That approach is incomplete—and often misleading.

A smarter strategy looks at the full picture:

- Income taxes

- Property taxes (driven by home values)

- Sales taxes (including local additions)

- Cost of living (food, utilities, insurance)

- Housing affordability

👉 When combined, these determine your true financial position.

🧠 Why This Matters More Than Ever

The national tax landscape is undergoing significant structural change.

States are actively restructuring how they generate revenue—not just to balance budgets, but to:

- Attract new residents

- Encourage investment

- Lower the perceived cost of living

- Compete with higher-tax states

👉 This is no longer theoretical—it is happening right now.

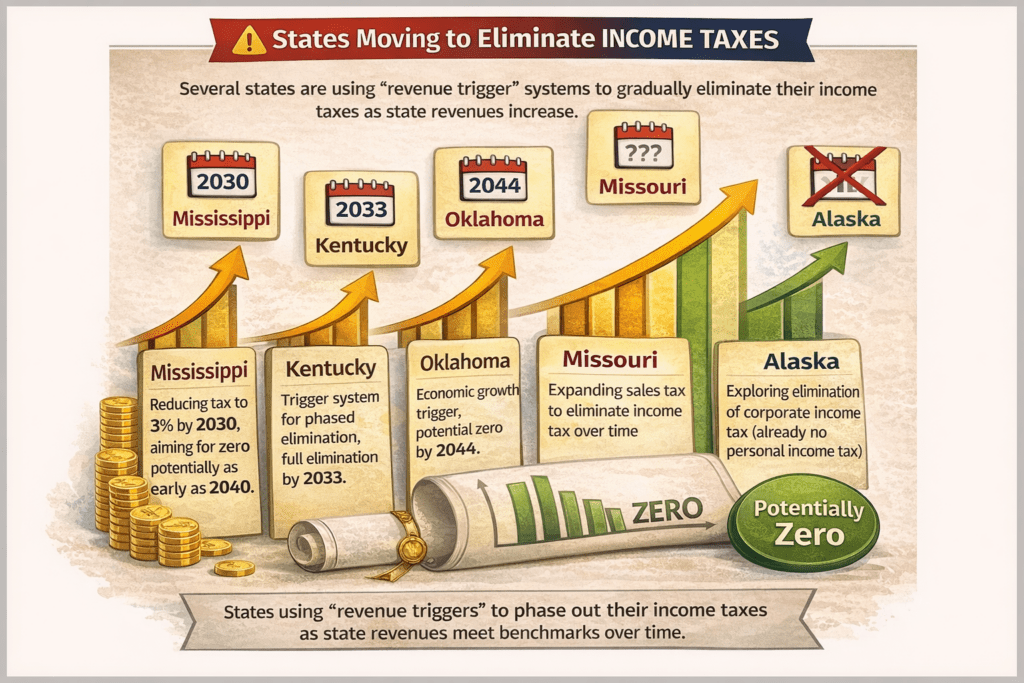

🔻 States Moving to Eliminate Income Taxes

While states like Texas and Florida have long attracted residents with no personal income tax, several other states are now following a structured path to eliminate theirs.

These states are using “revenue trigger” systems, meaning taxes are reduced automatically as state revenues meet certain benchmarks.

Notable Examples:

- Mississippi

Currently reducing its income tax to 3% by 2030, with a framework in place to continue lowering it to zero—potentially as early as 2040. - Kentucky

Using a reserve-based trigger model, with a legal path toward full elimination by 2033. - Oklahoma

Passed legislation tying income tax reductions to economic growth, potentially reaching zero by 2044. - Missouri

Exploring the expansion of sales tax to offset and eliminate income tax over time. - Alaska

Already has no personal income tax and is now exploring eliminating corporate income tax.

👉 Additional states like West Virginia and Georgia have publicly stated long-term goals of reaching zero income tax.

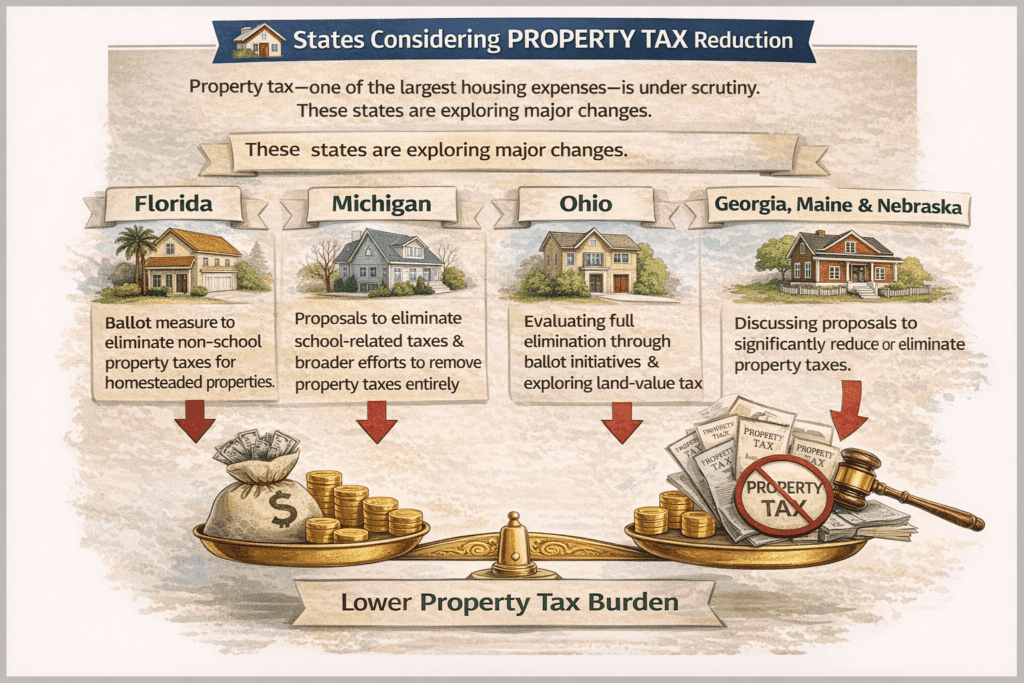

🏠 States Considering Property Tax Reduction or Elimination

Property tax—one of the largest expenses tied directly to housing—is also under pressure.

While full elimination is difficult due to its role in funding local governments and schools, several states are exploring major changes.

Key Developments:

- Florida

Considering ballot measures to eliminate non-school property taxes for homesteaded properties. - Michigan

Proposals include eliminating school-related property taxes for certain households and broader efforts to eliminate property taxes entirely. - Ohio

Evaluating full elimination through ballot initiatives, along with potential shifts to land-value taxation. - Georgia, Maine, and Nebraska

Have introduced or discussed proposals to significantly reduce or eliminate property taxes.

🛒 Sales Tax Shifts (Especially on Essentials)

While no state is eliminating sales tax entirely, many are reducing or eliminating taxes on groceries, which directly impacts the cost of living.

Recent Changes:

- Arkansas & Illinois

Eliminated statewide grocery taxes in 2026 (local taxes may still apply). - Kansas

Eliminated the grocery tax in 2025. - Oklahoma

Eliminated its 4.5% grocery tax in 2024. - Mississippi

Reduced the grocery tax and is under pressure to eliminate it entirely.

👉 This is a major shift:

States reducing income taxes often increase reliance on consumption taxes.

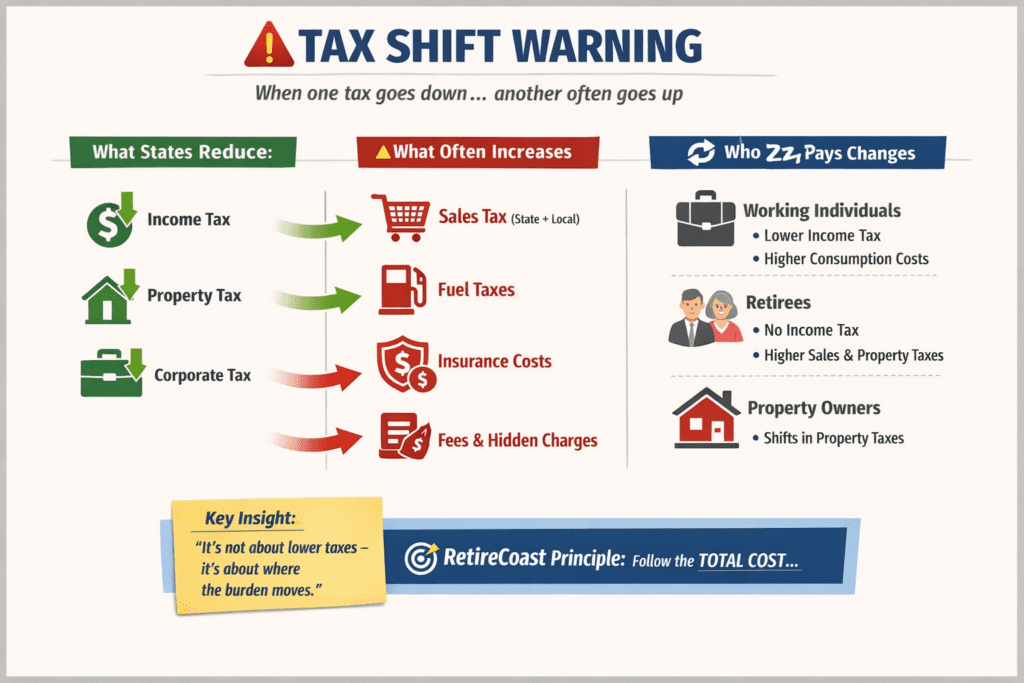

⚠️ Important Reality: Tax Reductions Often Shift the Burden

Here is the most important concept in this entire discussion:

When a state reduces one tax, it usually replaces that revenue somewhere else.

This is called a tax shift.

🔄 Real-World Example

Mississippi reduced its grocery tax and shifted revenue toward fuel taxes.

👉 Impact:

- Retirees benefit (lower food costs, less driving)

- Frequent drivers and businesses may pay more

🧠 The Key Insight

It’s not about how much tax is eliminated—it’s about who ends up paying it.

Examples of shifting burden:

- Income tax ↓ → Sales tax ↑

- Property tax ↓ → Consumption or fuel taxes ↑

- Business tax ↓ → Residential burden ↑

👥 Who Benefits Depends on Your Profile

These changes create very different outcomes depending on who you are:

- Working professionals → Benefit most from income tax reductions

- Retirees → Benefit from lower cost of living and consumption taxes

- Investors → Sensitive to capital gains and wealth tax policy

- Property owners → Directly impacted by property tax changes

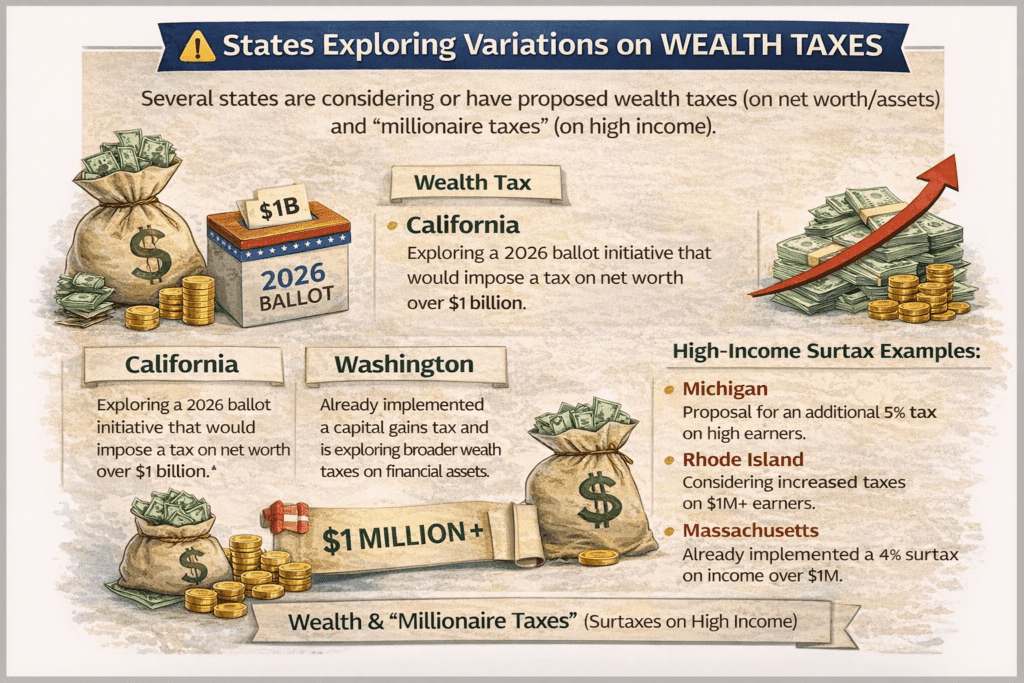

💼 The Emerging Risk: Wealth Taxes & High-Income Surtaxes

In contrast to tax reductions in some states, others are exploring entirely new tax categories.

🧾 Two Types to Watch:

1. True Wealth Taxes

Taxes on accumulated net worth (assets), even if not sold

2. “Millionaire Taxes”

Higher tax rates on high income or capital gains

Key Developments:

- California

Exploring a 2026 ballot initiative that would impose a tax on net worth over $1 billion. This article outlines the issues: https://calmatters.org/politics/2026/04/billionaire-tax-labor-divided/ - Washington

Already implemented a capital gains tax and is exploring broader wealth taxes on financial assets. - Coordinated legislative efforts in states like:

New York,

Illinois,

Maryland,

Connecticut

High-Income Surtax Examples:

- Michigan

Proposal for an additional 5% tax on high earners. Click here to learn more about this. - Rhode Island

Considering increased taxes on $1M+ earners. - Massachusetts

Already implemented a 4% surtax on income over $1M.

⚠️ Strategic Warning

Do not assume these taxes will remain limited to the ultra-wealthy.

Historically:

- Tax thresholds shift

- Definitions expand

- Revenue needs grow

👉 What begins as a tax on billionaires or millionaires can evolve over time.

📊 Final Takeaway

States that successfully restructure their tax systems often see:

- Increased inbound migration

- Rising housing demand

- Shifting cost structures

👉 Which makes one thing clear:

Understanding these trends is not optional—it’s essential for long-term wealth preservation.

📊 What You Should Actually Measure

To make a smart decision, you must evaluate the total cost structure, not just one category.

At a minimum, this includes:

💰 Income Taxes

- Earned income

- Retirement income (some states do not tax this)

🏠 Housing & Property Taxes

- Home values directly impact tax burden

- Lower-cost housing often leads to lower long-term expenses

🛒 Sales Taxes

- State rate plus local additions

- Direct impact on everyday spending

🧾 Cost of Living

- Utilities

- Food

- Insurance

- Services

⚖️ The RetireCoast Principle

This is the foundation of the strategy:

We don’t chase low taxes.

We reduce total financial pressure.

🧮 Next Step

Now that you understand the concept, the next step is simple:

👉 Use the free calculator below to determine whether relocating could improve your financial position based on your numbers.

Run the Numbers Before You Move

Understanding tax shifts and cost-of-living differences is important—but at some point, you need to apply those concepts to your actual numbers.

That’s where most people fall short.

They rely on general advice like:

- “This is a low-tax state.”

- “That area is more affordable.”

But without running the numbers, those statements can be misleading.

👉 What matters is how those factors affect your income, your spending, and your property.

💡 Why a Simple Calculation Can Change Your Decision

A move that looks financially beneficial on the surface may not be once you account for:

- Higher property taxes tied to home values

- Increased sales taxes from local jurisdictions

- Changes in the cost of living

- Differences in how income is taxed

On the other hand, a state that doesn’t look dramatically different at first glance may produce meaningful long-term savings.

🎯 The Goal

This tool is designed to answer one simple question:

Will relocating improve your financial position based on your current situation?

It does this by comparing:

- Income taxes

- Property taxes

- Sales taxes (including local impact)

- Cost of living adjustments

FINANCIAL SNAPSHOT TOOL

This free tool gives you a quick financial snapshot so you can see whether a move looks favorable, neutral, or potentially disadvantageous before going deeper.

⚠️ Before You Interpret the Results

Keep in mind:

- This is a financial snapshot, not a full analysis

- It uses state-level averages, not local precision

- It does not account for future tax changes

👉 But it will give you something extremely valuable:

A clear starting point based on your numbers—not assumptions.

📣 What Comes Next

Once you see your result, the next step is to understand:

- Why the result looks the way it does

- Which factors are driving the outcome

- How future tax changes could impact your decision

👉 That’s exactly what we’ll cover next.

How to Interpret Your Results (What Really Matters)

Now that you’ve run your numbers, you have something most people never get:

👉 A data-driven starting point

But the result itself is only part of the story.

What really matters is understanding why the result looks the way it does.

🧠 Look Beyond the Final Number

Your result likely showed one of three outcomes:

🟢 Strong Financial Benefit

This means the move appears to reduce your overall financial burden.

👉 But don’t stop there—identify what’s driving the savings:

- Lower income taxes?

- Lower housing costs?

- Reduced cost of living?

🟡 Limited Impact

This means the financial difference is relatively small.

👉 In these cases:

- Lifestyle factors may carry more weight

- Small changes in assumptions could shift the result

- Local costs (not included in this tool) may matter more

🔴 Potential Financial Disadvantage

This means the move could increase your total cost.

👉 Common reasons include:

- Higher property taxes

- Higher housing costs

- Increased cost of living

- Higher consumption taxes

🔍 Identify Your Biggest Cost Drivers

This is one of the most important steps.

Your result is not just about totals—it’s about what’s causing the difference.

👉 Ask yourself:

- Is housing driving the change?

- Are property taxes higher in the target state?

- Is the cost of living offsetting tax savings?

- Are sales taxes (including local additions) higher?

⚠️ The Hidden Risk: Future Tax Changes

Remember what we discussed earlier:

Tax structures change—and often shift the burden over time.

States like:

- Florida

- Texas

- Mississippi

…are actively exploring ways to restructure taxes.

👉 That means:

- Today’s advantage may look different tomorrow

- Property taxes, sales taxes, or fees could increase

- The burden may shift between income earners and retirees

🧠 The Real Question You Should Be Asking

Not:

“Is this a lower tax state?”

But:

“How stable is this financial advantage over time?”

📣 Where the Free Tool Stops

The tool you just used is designed to give you a quick financial snapshot.

It does not:

- Model future tax changes

- Account for detailed retirement income rules

- Include estate or inheritance taxes

- Evaluate multiple scenarios

👉 And that’s where many relocation decisions go wrong.

🔓 The Smarter Approach

Before making a move, you should be able to answer:

- What happens if this state changes its tax structure?

- What if property taxes increase?

- What if my income mix changes (working → retired)?

💡 Upgrade Your Analysis

The RetireCoast Estate Planning Membership includes a more advanced relocation tool that allows you to:

- Run “what-if” scenarios

- Model future tax shifts

- Compare multiple states side-by-side

- Evaluate both working and retirement income strategies

👉 This turns a simple estimate into a long-term financial decision tool

🧱 Final Insight Before You Decide

Relocation is not just about saving money this year.

It’s about positioning yourself in a system where you can preserve more of your wealth over time.

A Simple Framework for Making the Right Move

At this point, you understand something most people don’t:

- Lower taxes do not always mean lower costs

- Cost of living can outweigh tax savings

- Tax structures change—and often shift the burden

👉 Now it’s time to turn that knowledge into a decision.

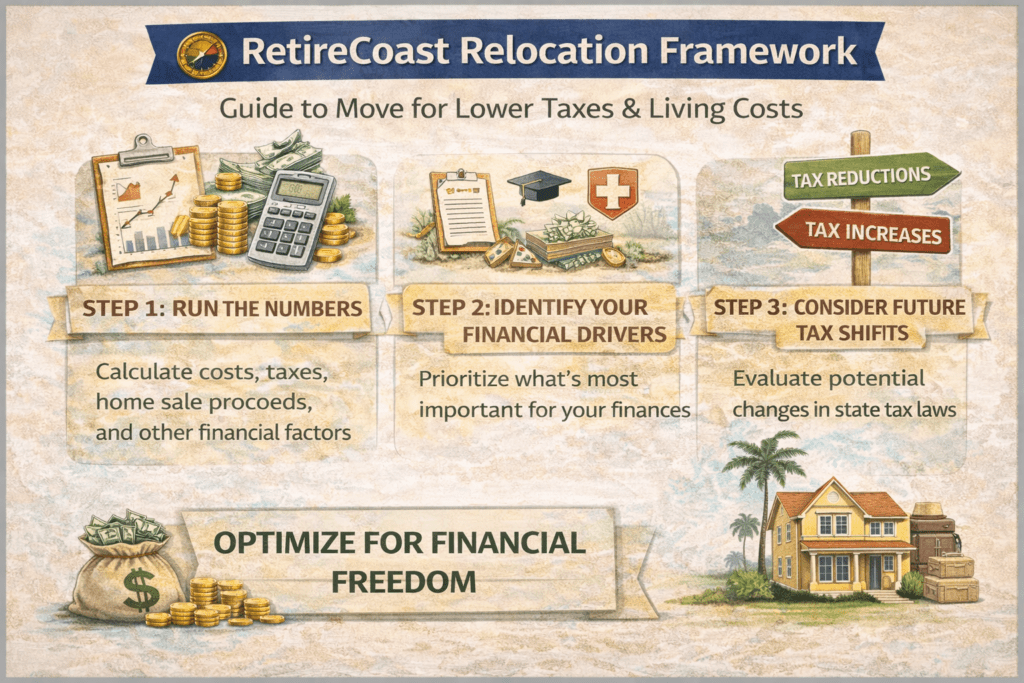

🧠 The RetireCoast Relocation Framework

Use this simple 4-step approach before making any move:

✅ Step 1: Run the Numbers

Start with the basics:

- Compare income taxes

- Evaluate property taxes tied to housing

- Factor in sales tax (including local additions)

- Adjust for cost of living

👉 This is exactly what the free tool helps you do.

✅ Step 2: Identify Your Financial Drivers

Every result has a cause.

Ask:

- What is saving me money?

- What is costing me more?

👉 This step often reveals something unexpected:

Housing and cost of living frequently matter more than income tax alone.

✅ Step 3: Consider Future Tax Shifts

This is where most decisions fail.

States like:

- Florida

- Texas

- Mississippi

…are actively evaluating tax changes.

👉 Remember:

Today’s tax advantage is not guaranteed tomorrow.

✅ Step 4: Match the Move to Your Profile

Different people benefit from different structures:

Working Individuals

- Benefit most from lower income taxes

Retirees

- Benefit from low cost of living and reduced consumption taxes

Property Owners

- Highly sensitive to property tax structures

👉 There is no “best state”—only the best fit for your situation.

⚖️ The Final Decision Filter

Before you commit to relocating, ask yourself:

Will this move reduce my total financial burden—not just one category of tax?

If the answer is yes—and the advantage appears stable—you likely have a strong financial case.

🔓 Go Beyond the Snapshot

The free tool you used gives you a strong starting point.

But major financial decisions deserve deeper analysis.

The RetireCoast Estate Planning Membership includes a more advanced relocation tool that allows you to test different scenarios, model future tax changes, and make decisions with greater confidence.

🧠 Final Thought

Relocating is one of the few decisions that can immediately improve your financial position—but only if you evaluate it correctly.

Don’t chase lower taxes.

Follow the total cost—and where it’s going.

Premium Relocation Wealth Preservation Tool

The Premium Relocation Wealth Preservation Tool available as part of our Estate Planning Membership, is designed to solve a problem that cannot be handled manually. Relocating to another state involves multiple interdependent financial variables, including income taxes, property taxes, housing costs, insurance, cost of living, retirement income treatment, and estate exposure. These variables interact over time and change as a household transitions from working years into retirement.

A simple comparison using averages is not sufficient. The premium tool replaces broad estimation with structured modeling based on the user’s specific financial profile.

Core Purpose

The purpose of the premium tool is not to identify the lowest-tax state.

The purpose is to determine whether relocating reduces total financial pressure over time.

This includes evaluating:

- Tax burden across multiple income types

- Housing and property cost structure

- Consumption-driven costs such as sales tax

- Insurance and cost-of-living pressures

- Transition costs associated with moving

- Long-term risk of tax shifts

- Estate and inheritance exposure

The output is a clear, structured decision, not just a set of numbers.

Step 1: Define the Household Profile

The tool begins by identifying the user’s financial identity.

It categorizes the household as:

- Working household

- Retired household

- Mixed-income household

This matters because tax exposure changes significantly depending on whether income is earned, drawn from retirement accounts, or received through Social Security or investments.

The tool also considers age and expected retirement timing to model how the financial profile will evolve.

Step 2: Model Current State Financial Pressure

The tool calculates the total annual financial pressure in the current state.

This includes:

- Earned income tax

- Retirement income tax

- Investment income exposure

- Property tax burden

- Sales tax impact on spending

- Housing costs adjusted for local conditions

- Insurance costs

- Utilities, food, and healthcare

This creates a baseline that reflects how much financial pressure the current location is placing on the household each year.

Step 3: Model Target State Financial Pressure

The same structure is applied to the target state.

However, the tool does not assume that lower income tax automatically leads to savings.

It recalculates:

- Housing costs in the new state

- Property tax exposure

- Sales tax impact on consumption

- Insurance differences

- Cost-of-living adjustments

- Differences in retirement income taxation

This produces a realistic estimate of the financial environment after the move.

Step 4: Identify the True Financial Drivers

The tool does not stop at totals.

It isolates the strongest and weakest drivers of the result.

Examples include:

- Income tax savings

- Increased housing costs

- Higher property taxes

- Insurance increases

- Sales tax differences

This step explains why the move works or does not work.

Step 5: Model Transition Costs and Break-Even

Relocation is not free.

The tool calculates total transition costs, including:

- Moving expenses

- Real estate transaction costs

- Travel and setup costs

- Temporary housing or storage

It then calculates a break-even timeline.

This answers a critical question:

How long does it take for the financial benefits of the move to recover the cost of relocating?

Step 6: Scenario and What-If Modeling

The premium tool allows for multiple future scenarios.

Examples include:

- Continuing to work for several years after moving

- Transitioning from earned income to retirement income

- Downsizing housing later in retirement

- Changes in spending patterns

This allows the user to see how different life paths affect the financial outcome.

Step 7: Future Tax-Shift Risk Modeling

One of the most important elements of the tool is future tax-shift modeling.

States do not maintain the same tax structure forever.

The tool introduces structured stress testing by adjusting:

- Income tax assumptions

- Property tax levels

- Sales tax impact

- Insurance costs

- Housing cost pressure

It also assigns a future risk score based on structural factors such as growth pressure and fiscal demand.

This is not a prediction of future laws.

It is a method of testing whether the financial outcome is durable under changing conditions.

Step 8: Estate and Inheritance Consideration

The tool incorporates estate-level considerations.

This is critical because a move that reduces taxes during life may still expose the household to estate or inheritance taxes at death.

The tool flags:

- States with estate tax exposure

- States with inheritance tax exposure

This ensures that wealth preservation is evaluated across generations, not just during the user’s lifetime.

Step 9: Decision Output

The tool produces a structured result, not just raw data.

The result is categorized as:

- Strong Move

- Moderate Move

- Weak Move

- Not Recommended

This classification is based on:

- Annual financial impact

- Break-even timeline

- Strength of financial drivers

- Performance under stress testing

- Future risk exposure

Step 10: Interpretation and Guidance

The tool provides interpretation to explain the result.

It highlights:

- Why the move works or fails

- Which cost categories matter most

- Where assumptions are sensitive

- Where additional analysis is needed

This transforms the output from a calculation into a decision-making framework.

Key Benefit

The primary benefit of the premium tool is clarity.

It replaces guesswork and assumptions with structured financial modeling.

Instead of relying on general statements such as “no income tax” or “lower cost of living,” the user can evaluate the full financial system surrounding the move.

Final Principle

The tool is built around one principle:

Do not chase low taxes.

Reduce total financial pressure.

Relocation is one of the largest financial decisions a household can make.

This tool helps ensure that decision is based on a complete financial view, not a partial one.

QUIZ

Answer these 10 questions to see whether you are approaching a move from a strong financial perspective.

FAQ

Is moving to a no-income-tax state always better?

No. Many states replace income taxes with higher property or sales taxes.

Do retirees benefit more from relocating?

Often yes, especially in states that do not tax retirement income.

Are property taxes higher in no-income-tax states?

In many cases, yes. Texas is a common example.

Do sales taxes vary by location?

Yes. Local jurisdictions often add to the base state rate.

Can tax laws change after I move?

Yes. States frequently adjust tax structures, which can impact long-term planning.

Is cost of living more important than taxes?

Both matter. The goal is total financial efficiency.

Should I consider estate taxes?

Yes, but this tool does not include them. The membership tool does.

What is the biggest mistake people make?

Focusing only on income tax instead of total cost.

Do I need to change residency officially?

Yes. Proper domicile changes are critical.

Is this tool enough to make a decision?

No. It’s a starting point. Use the full tool for deeper planning.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}