Real estate investors and small business owners spend years building wealth through real estate investments, rental properties, and business assets. Over time, this often becomes a significant portion of their net worth.

But what many do not realize is how exposed that wealth can be to legal threats. A single lawsuit, tenant injury, or unexpected legal action can place everything at risk—including your personal assets and primary residence.

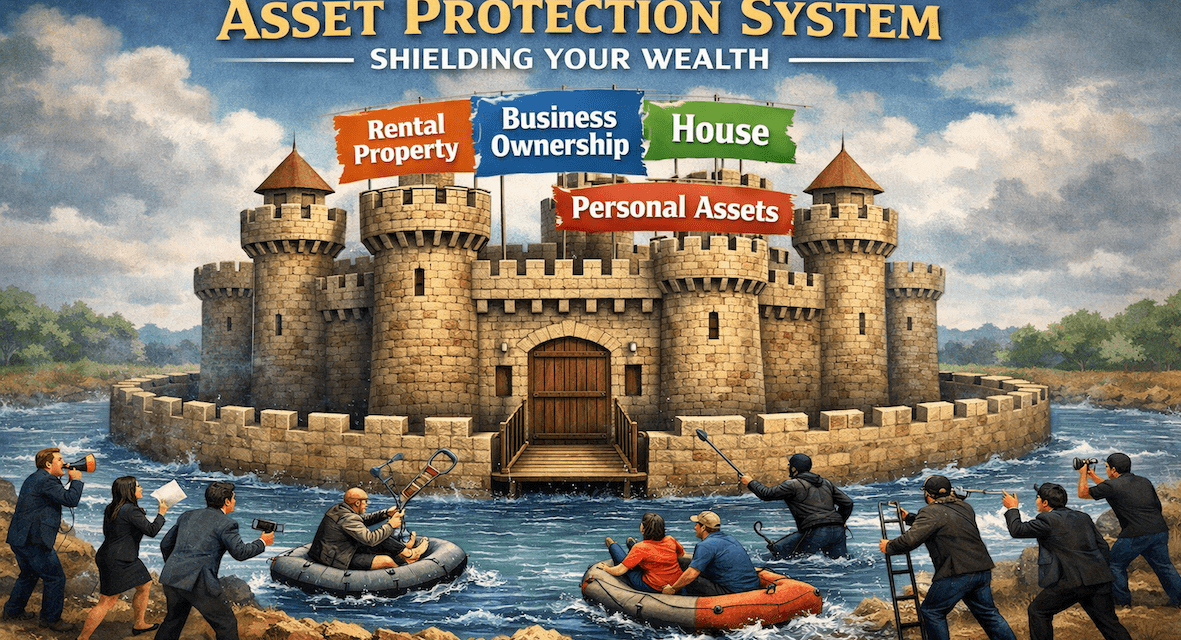

This article outlines a complete asset protection system designed to create multiple layers of protection around your real estate holdings, business entities, and fixed assets.

Our complete asset protection system is like building a wall around your wealth and installing a moat outside of the wall. Some who want what you have may penetrate the moat—but few, if any, can penetrate the wall.

The idea of implementing this system may seem overwhelming at first, but it is not. It requires careful planning, following the proper steps, and maintaining documentation over time.

You will not lose control or access to your assets. You can still benefit from them, generate cash flow, and sell them when appropriate—provided the system is properly maintained.

RetireCoast did not create these strategies. What we have done is organize proven asset protection strategies into a practical system that individuals can understand and implement.

This article focuses on the “why” and “what.” The “how” is available through our Estate Planning Membership and Business Builder Membership, where tools and step-by-step guidance are provided.

The cost of these memberships is minimal compared to the financial security they can help protect.

The system described here does not apply only to rental properties or business assets. If your primary residence is fully paid for, it may be one of your most exposed assets.

Something as simple as a child falling on your driveway or an accident involving your property can trigger legal action that puts your home at risk.

This article focuses on fixed assets—real estate, vehicles, boats, and other tangible property—that cannot be easily hidden or transferred.

Always remember: If you have something of value, there is someone out there who wants it.

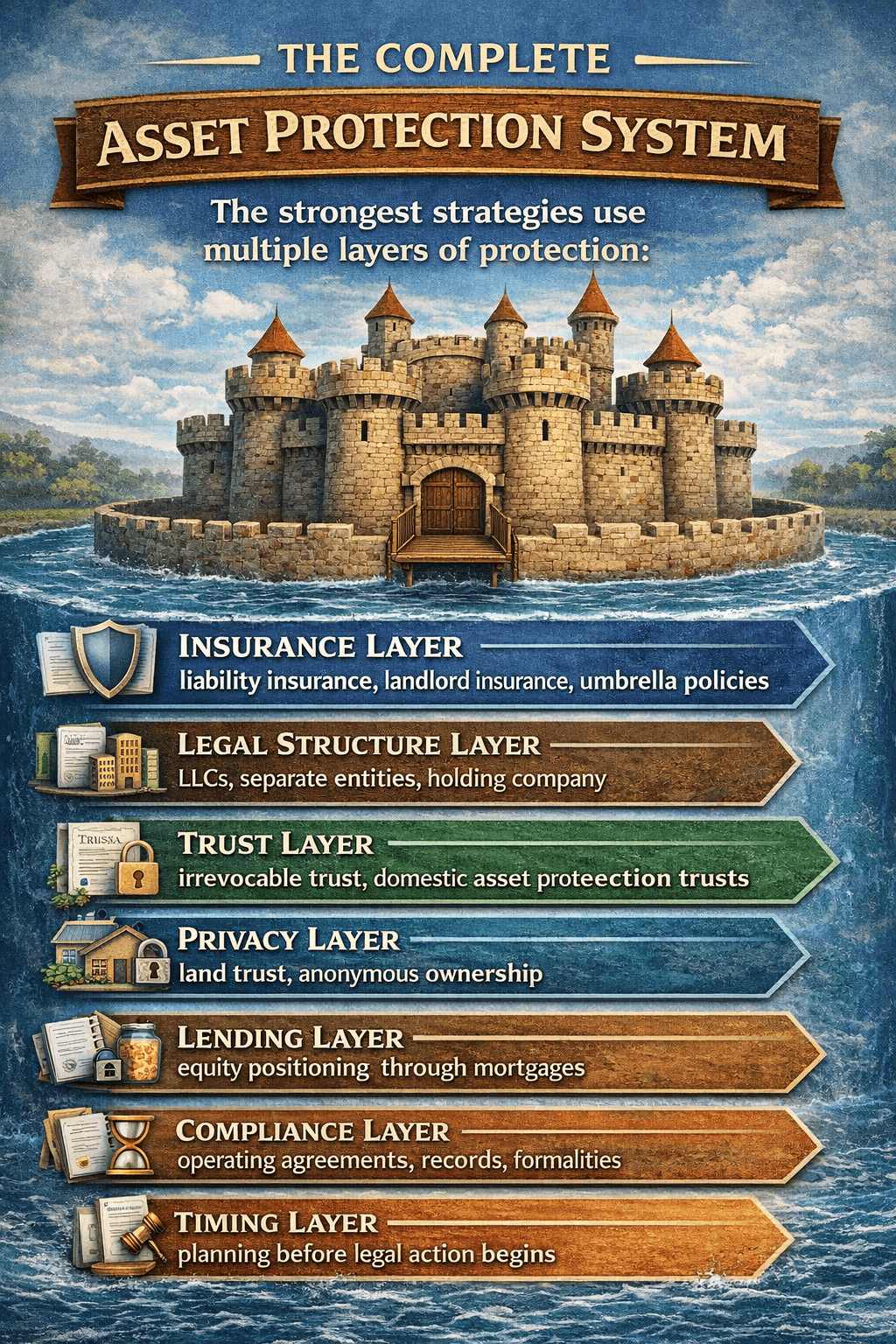

The Complete Asset Protection System

The strongest asset protection strategies rely on multiple coordinated layers—not a single tool.

- Insurance Layer – liability insurance, landlord insurance, umbrella policies

- Legal Structure Layer – LLCs, separate entities, holding companies

- Trust Layer – irrevocable trust, domestic asset protection trusts

- Privacy Layer – land trust, anonymous ownership

- Lending Layer – equity positioning through mortgages

- Compliance Layer – operating agreements, records, annual reports

- Timing Layer – planning before legal action begins

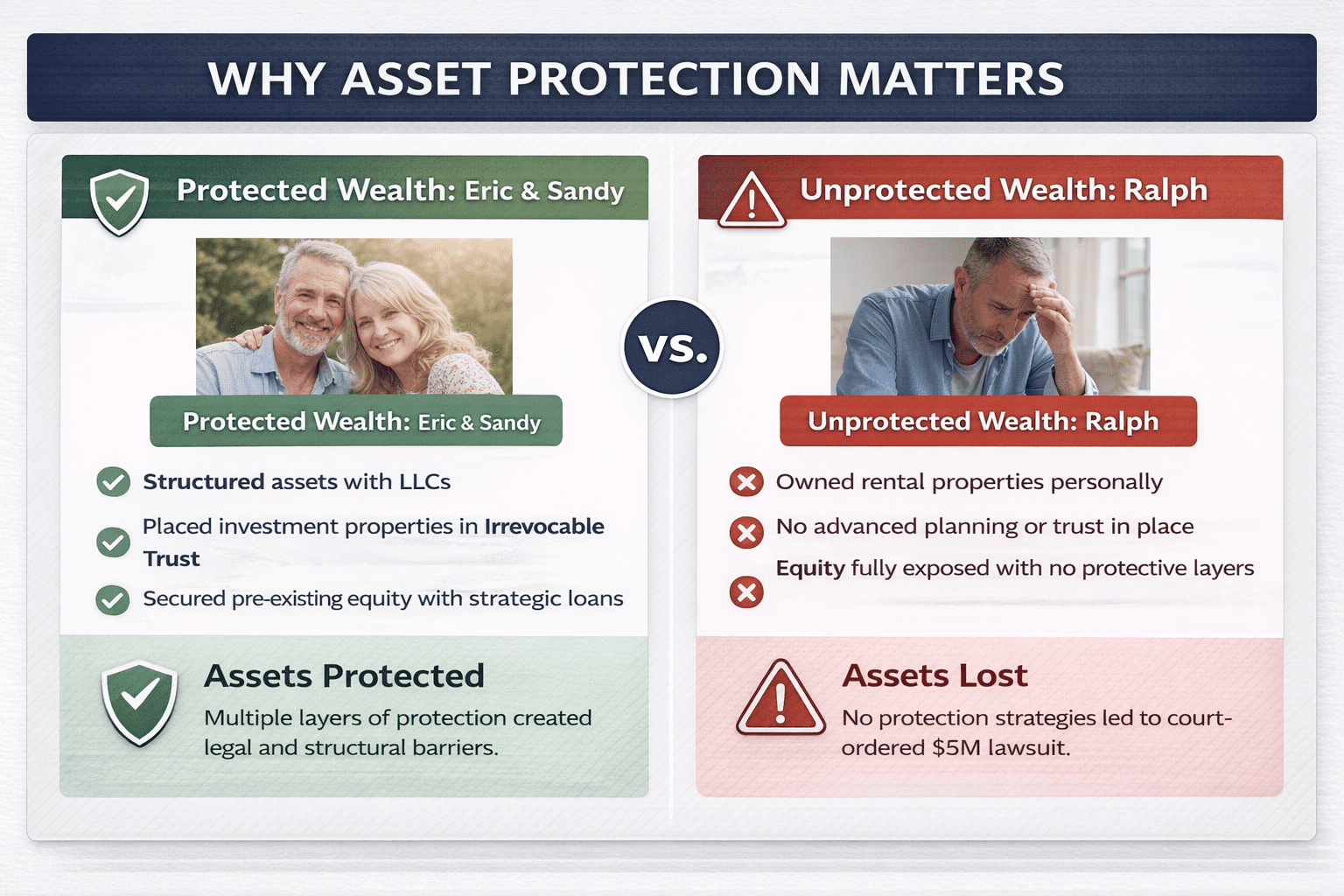

Case Study: Planning Ahead (Eric & Sandy)

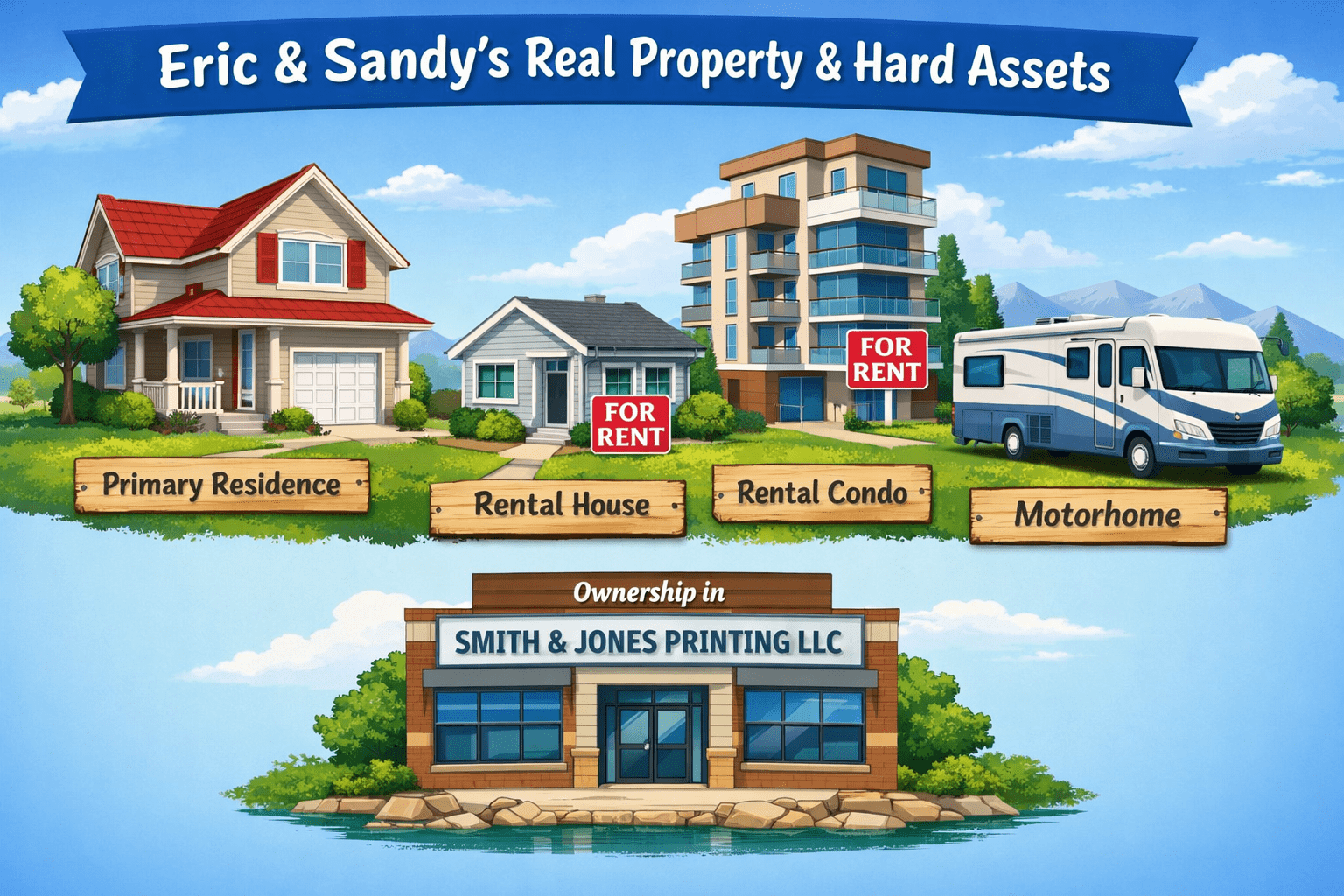

Eric and Sandy spent years building wealth. They owned a primary residence with approximately $400,000 in equity and two rental properties worth a combined $850,000—both paid off.

They also owned vehicles and a motor home, all fully paid for. Their net worth was substantial.

After seeing a friend face a lawsuit, they took action. They created separate LLCs for each property, established mortgages to reduce exposed equity, and implemented an irrevocable trust.

They acted before any legal issues existed, which is critical under asset protection planning rules.

Now, anyone attempting to reach their assets faces multiple legal barriers, significantly reducing the likelihood of a successful claim.

Case Study: No Protection (Ralph)

Ralph owned three rental properties, all fully paid for. He believed this was the best way to invest and had no asset protection strategies in place.

A tenant filed a lawsuit after a fall. Ralph believed the claim was invalid—but he lost in court.

The judgment exceeded his insurance coverage, and he was forced to give up his properties to satisfy the claim.

Only his primary residence remained protected due to existing debt on the home.

Ralph later learned that simple planning steps could have made his assets significantly more difficult to reach.

Protecting an ownership interest—such as 25% of a business—requires careful structuring using legal entities, agreements, and tax-aware planning.

Attempting to do this without proper guidance can create conflicts with IRS rules and may fail under legal scrutiny.

Our Business Builder Membership provides step-by-step guidance and tools to properly structure business ownership protection.

Key Components Explained

Limited Liability Companies (LLCs)

Using separate LLCs for each rental property creates separation between business assets and personal assets.

Irrevocable Trusts

An irrevocable trust can remove assets from personal ownership, reducing exposure to creditor claims.

Insurance Coverage

Liability insurance and landlord insurance act as the first line of defense against claims.

Equity Positioning

Mortgages and lending structures can reduce exposed equity, making assets less attractive targets.

IRS Revenue Ruling 77-137 may require a creditor holding a charging order to pay income taxes on income they have not received.

This creates financial pressure on creditors and often leads to settlement discussions rather than prolonged legal action.

Charging orders may also expire if not enforced or renewed.

Read more about IRS treatment of LLC distributional interests →

“The fat purse attracts thieves.” If you have something of value, someone wants it. This system helps you protect what you have spent years building.

Frequently Asked Questions

Is an LLC enough to protect my assets?

No. A complete system requires multiple layers including insurance, trusts, and compliance.

When should I implement asset protection?

Before any legal action exists. Late transfers may be considered fraudulent.

Can I still control my assets?

Yes. Proper structuring allows continued control and income.

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}