Last updated on July 8th, 2026 at 04:51 am

Introduction: Protecting Assets by Separating Ownership and Control

For many individuals—especially those who own real estate, businesses, or investment assets—the question isn’t whether to plan ahead… it’s how to protect what they’ve built from risks they cannot fully control. An irrevocable trust for asset protection is one of the most effective strategies used to create separation between personal ownership and valuable assets.

Lawsuits, creditor claims, and unexpected liabilities can arise even when you’ve done everything right. And when they do, the outcome often depends on one critical factor:

👉 Do you legally own—and control—the assets in question?

An irrevocable trust is fundamentally different from other planning tools because it is designed to create real separation between you and your assets.

When structured properly, it can be used to:

- Protect real estate holdings

- Shield ownership interests in businesses and LLCs

- Reduce exposure to lawsuits and creditor claims

- Establish a long-term framework for managing and transferring wealth

But this protection comes with a trade-off:

You must give up a degree of control.

Unlike revocable trusts, which are built for flexibility and convenience, an irrevocable trust is built for structure, discipline, and legal separation. That separation is what courts and the IRS evaluate when determining whether assets are reachable.

In this guide, we’ll walk through how an irrevocable trust works, why trustee independence is critical, and how it fits into a layered asset protection strategy that can include real estate, LLC ownership, insurance, and financing.e living trust works, why real estate owners use it, and how it fits into a layered asset protection system.

Irrevocable trusts are also recognized under federal tax frameworks, and the Internal Revenue Service provides guidance on how these structures are treated from a legal and tax perspective.

- Introduction: Protecting Assets by Separating Ownership and Control

- What Is an Irrevocable Trust?

- How an Irrevocable Trust Works (Step-by-Step)

- Why Real Estate and Business Owners Use an Irrevocable Trust

- How to Transfer Assets Into an Irrevocable Trust

- Irrevocable Trust vs LLC

- Revocable vs Irrevocable Trust

- How an Irrevocable Trust Fits Into Asset Protection

- Common Mistakes to Avoid

- When an Irrevocable Trust Makes the Most Sense

- When It May Not Be Necessary

- Trustee Structure: The Critical Factor in Asset Protection

- How to Select a Trustee (Individual vs Professional)

- Option 1: Individual Trustee

- Option 2: Professional or Corporate Trustee

- Hybrid Approach (Common Strategy)

- What to Look for in a Trustee

- Questions to Ask Before Selecting a Trustee

- Final Takeaway

- Case Study: When Control Determines the Outcome

- Why the Trustee Refused — and Why the Court Agreed

- Frequently Asked Questions

- PODCAST

Unfortunately, legal action is not always based on fault. You can be the target of a claim that is frivolous or unjustified, yet still be forced to defend yourself. This happens every day.

The most important takeaway is timing. Asset protection planning must be done before there is any threat, any claim, or any hint of litigation. Once a problem exists, attempting to move or shield assets after the fact can be challenged—and in some cases, may even be considered a violation of the law.

Preparation and follow-through are what separate effective planning from reactive risk.

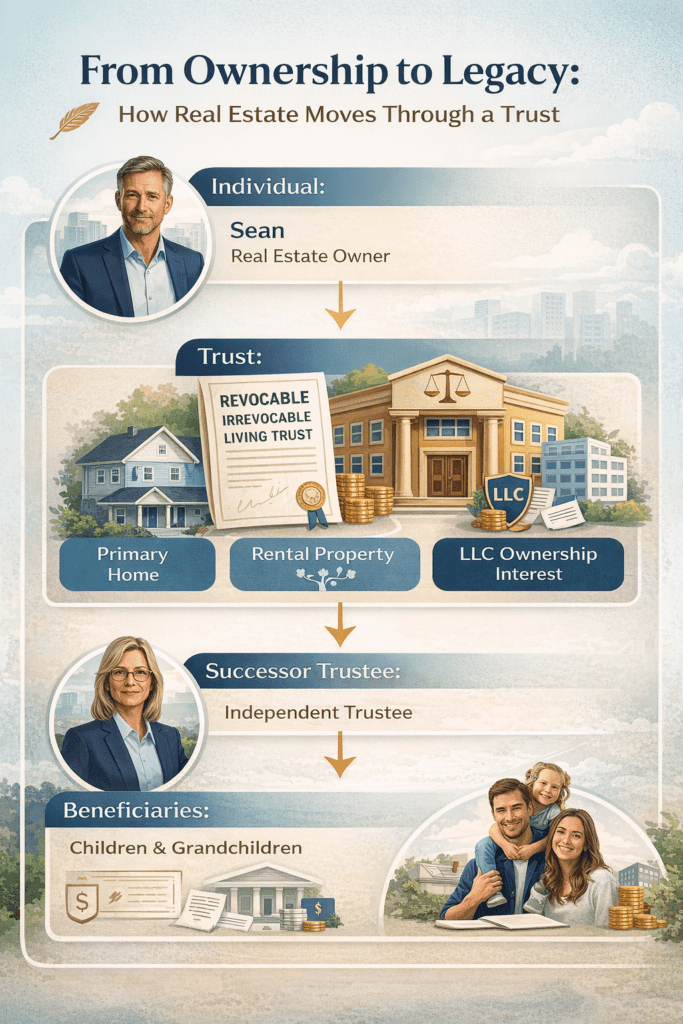

What Is an Irrevocable Trust?

An irrevocable trust is a legal structure where you transfer ownership of your assets—such as real estate, LLC interests, or business ownership—into a trust that you no longer control in the same way.

Once assets are placed into the trust:

- They are no longer legally owned by you

- They are managed by a trustee

- They must be handled according to the terms established when the trust was created

From a legal standpoint, a trust is defined as a fiduciary relationship where one party holds assets for the benefit of another, as outlined by the Legal Information Institute.

The Three Roles (And Why They Matter)

Unlike a revocable trust, an irrevocable trust requires real separation:

- Grantor – The person who creates the trust and transfers assets into it

- Trustee – An independent individual or entity responsible for managing the trust

- Beneficiaries – The individuals who benefit from the trust assets

👉 For asset protection to work, the trustee must be independent and not under your control.

⚠️ Key Concept

You cannot maintain full control and still expect asset protection.

How an Irrevocable Trust Works (Step-by-Step)

Step 1: Create the Trust Document

You establish the legal framework:

- Name of the trust

- Trustee and successor trustees

- Beneficiaries

- Distribution rules

- Special provisions (such as duress clauses)

Step 2: Transfer Assets Into the Trust

This is the most important step.

Assets may include:

- Real estate (via recorded deed transfer)

- LLC ownership interests (via assignment)

- Business ownership (depending on structure)

Example (Real Estate):

Before:

John Smith, Individual

After:

XYZ Trust Company, Trustee of the John Smith Irrevocable Trust dated January 1, 2026

Step 3: Trustee Controls the Assets

Once transferred:

- You no longer directly manage or control the assets

- The trustee makes decisions according to the trust terms

- You cannot freely sell, refinance, or dispose of assets

👉 This is the trade-off that creates protection.

Step 4: Trustee Acts Independently (Especially Under Pressure)

If:

- You face a lawsuit

- A creditor makes a claim

- A court applies pressure

The trustee is obligated to:

- Follow the trust instructions

- Use independent judgment

- Potentially deny requests made under duress

Step 5: Distributions Follow the Trust Rules

Beneficiaries (which may include you under certain structures) receive benefits:

- According to predefined rules

- Not based on immediate demands

- Not under creditor pressure

This quick decision tool helps you evaluate whether your current situation may justify a more advanced asset protection strategy. It takes into account:

- Home equity and real estate ownership

- Rental and investment property

- Business or LLC ownership

- Exposure to lawsuits or liability

- Your overall planning goals

Why Real Estate and Business Owners Use an Irrevocable Trust

1. Asset Protection

Assets are no longer legally owned by you, which may:

- Reduce exposure to lawsuits

- Limit creditor access

- Create legal separation

2. Protection of Business Ownership

Irrevocable trusts can hold:

- LLC ownership interests

- Shares in a business

- Partnership interests

This creates a layer between:

- You personally

- The value of the business

3. Structural Separation

Ownership is divided between:

- You (former owner)

- Trustee (controller)

- Beneficiaries (future recipients)

This separation is what courts evaluate.

4. Long-Term Planning

An irrevocable trust allows:

- Controlled distribution of wealth

- Protection across generations

- Structured management of assets

How to Transfer Assets Into an Irrevocable Trust

This step must be done correctly.

The Process:

- Prepare transfer documents:

- Deed for real estate

- Assignment for LLC or business interests

- Transfer ownership to the trustee

- Record documents where required

⚠️ Important Callout

If assets are not properly transferred into the trust, they remain exposed.

Irrevocable Trust vs LLC

| Feature | Irrevocable Trust | LLC |

|---|---|---|

| Asset Protection | ✅ Strong (if structured properly) | ✅ Yes |

| Probate Avoidance | ✅ Yes | ❌ No |

| Control | ❌ Limited | ✅ Yes |

| Liability Shield | ⚠️ Indirect | ✅ Yes |

| Best Use | Asset separation & long-term protection | Operational liability protection |

Key Insight:

An LLC protects against operational risk.

An irrevocable trust protects ownership itself.

Revocable vs Irrevocable Trust

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Control | ✅ Full | ❌ Limited |

| Flexibility | ✅ High | ❌ Low |

| Asset Protection | ❌ No | ✅ Yes |

| Purpose | Probate avoidance | Asset protection & separation |

Simple Explanation:

- Revocable Trust = Control + Convenience

- Irrevocable Trust = Separation + Protection

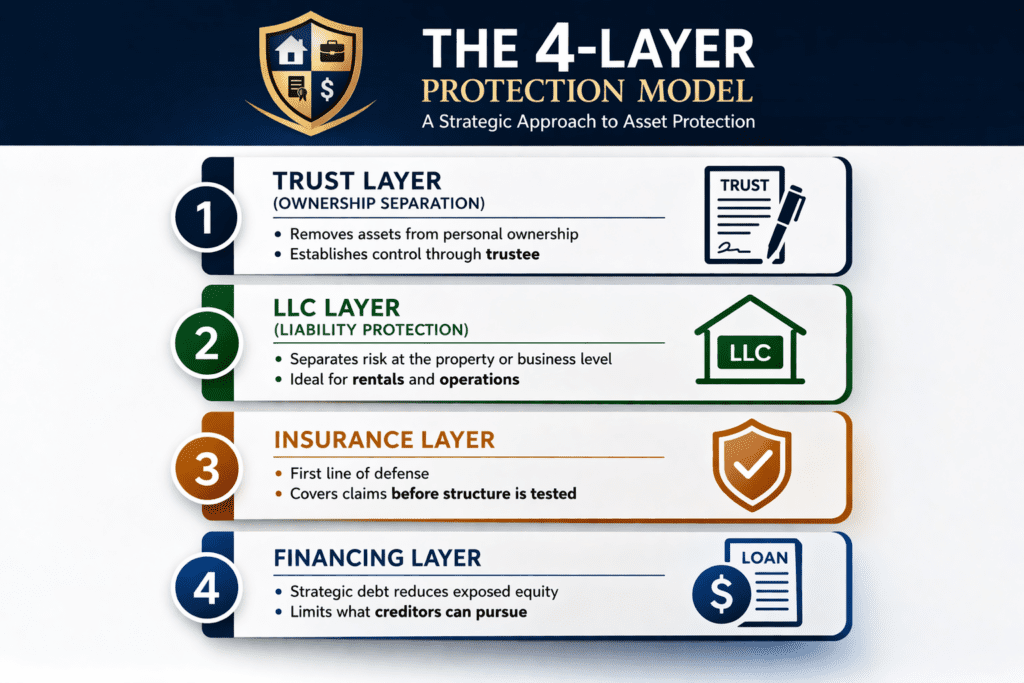

How an Irrevocable Trust Fits Into Asset Protection

An irrevocable trust is often the core layer in a broader strategy:

The 4-Layer Protection Model

1. Trust Layer (Ownership Separation)

- Removes assets from personal ownership

- Establishes control through trustee

2. LLC Layer (Liability Protection)

- Separates risk at the property or business level

- Ideal for rentals and operations

3. Insurance Layer

- First line of defense

- Covers claims before structure is tested

4. Financing Layer

- Strategic debt reduces exposed equity

- Limits what creditors can pursue

👉 Learn more in the full system:

https://retirecoast.com/asset-protection-real-estate-investors/

Common Mistakes to Avoid

1. Retaining Too Much Control

If you maintain control:

- Courts may treat assets as still yours

2. Using a Non-Independent Trustee

A controlled trustee weakens:

- Legal separation

- Asset protection strength

3. Not Following Trust Terms

Ignoring:

- Distribution rules

- Trustee authority

Can undermine the structure.

4. Improper Asset Transfers

Incorrect transfers can:

- Void protection

- Create legal complications

When an Irrevocable Trust Makes the Most Sense

An irrevocable trust is especially valuable if you:

- Own significant real estate or business assets

- Want protection from potential lawsuits

- Are building long-term wealth structures

- Are comfortable giving up some control

When It May Not Be Necessary

You may not need one if:

- You require full control of your assets

- Your asset exposure is minimal

- Your goals are limited to probate avoidance

↓

You (Trustee)

↓

Trust Assets (Real Estate)

✔ Easy to manage

✖ No asset protection

↓

Independent Trustee

↓

Trust Assets (Real Estate)

✔ Stronger protection

✖ Less flexibility

Trustee Structure: The Critical Factor in Asset Protection

One of the most important—and often misunderstood—elements of asset protection is not the trust itself… it is who controls it.

The difference between a structure that works and one that fails often comes down to a single question:

👉 Who is the trustee?

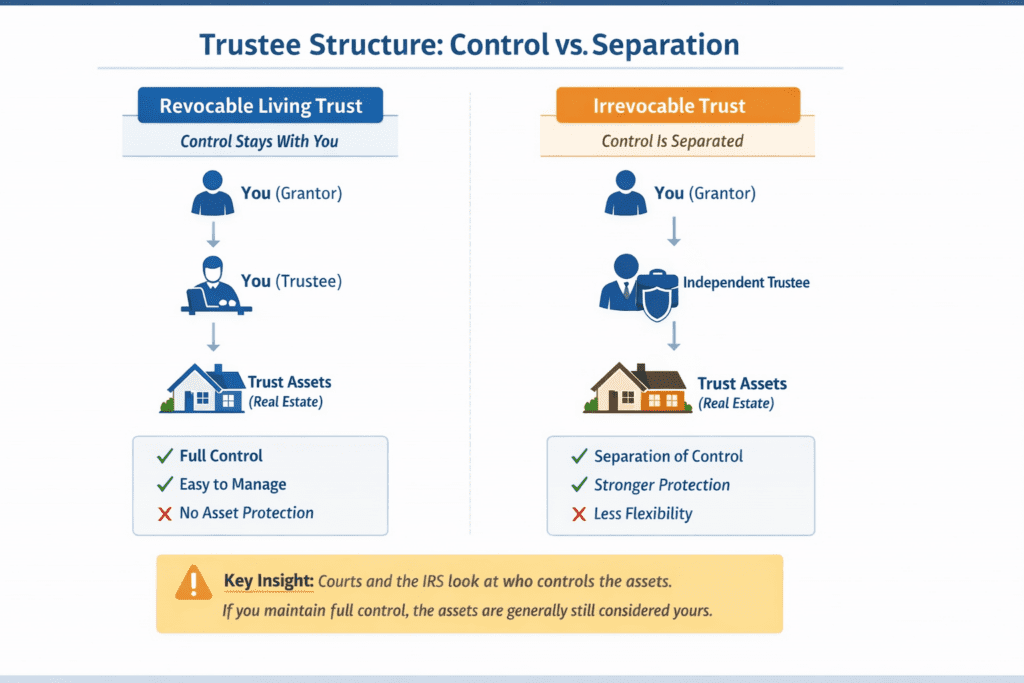

Revocable Trust: Control Stays With You

With a revocable trust, you typically:

- Serve as your own trustee

- Maintain full control over all assets

- Can buy, sell, refinance, or transfer property freely

You may also name:

- A spouse

- A family member

- A trusted individual

But in practice:

You are still in control.

👉 That control is exactly why a revocable trust does not provide asset protection.

Irrevocable Trust: Control Must Be Separated

With an irrevocable trust, the structure changes fundamentally.

While it may be possible in some cases to name a family member, effective asset protection planning typically requires:

- An independent individual, or

- A professional or corporate trustee

This creates something courts care deeply about:

Separation between you and the assets

⚠️ Key Asset Protection Insight

Asset protection does not come from the document—it comes from the loss of control.

Courts and the IRS evaluate:

- Who controls the assets

- Who benefits from them

- Whether the structure is truly independent

If you:

- Control the assets

- Direct how they are used

- Can override decisions

Then legally:

👉 Those assets may still be treated as yours

Why Trustee Independence Matters (Real-World Application)

This is exactly what you saw in Sean’s case.

- The trustee was independent

- The trustee followed the trust—not Sean

- The trustee refused to act under duress

Because of that:

- The court could not compel action

- The assets remained protected

- The structure held up under pressure

Control vs Protection

This is the trade-off every asset owner must understand:

- Revocable Trust = Control + Convenience

- Irrevocable Trust = Separation + Protection

You cannot have both at the same level.

What Real Separation Achieves

When properly structured, trustee independence:

- Strengthens legal defensibility

- Helps withstand creditor claims

- Supports IRS recognition of the structure

- Prevents forced liquidation under pressure

Practical Takeaway

For most individuals:

- Use a revocable trust for:

- Probate avoidance

- Estate organization

- Ease of transfer

- Use an irrevocable trust when:

- Asset protection is a priority

- You are willing to give up some control

- You want real legal separation between you and your assets

Final Insight

If you control it, you may still own it.

If you don’t control it, it may be protected.

👉 See how trustee structure fits into a full protection plan:

https://retirecoast.com/asset-protection-real-estate-investors/

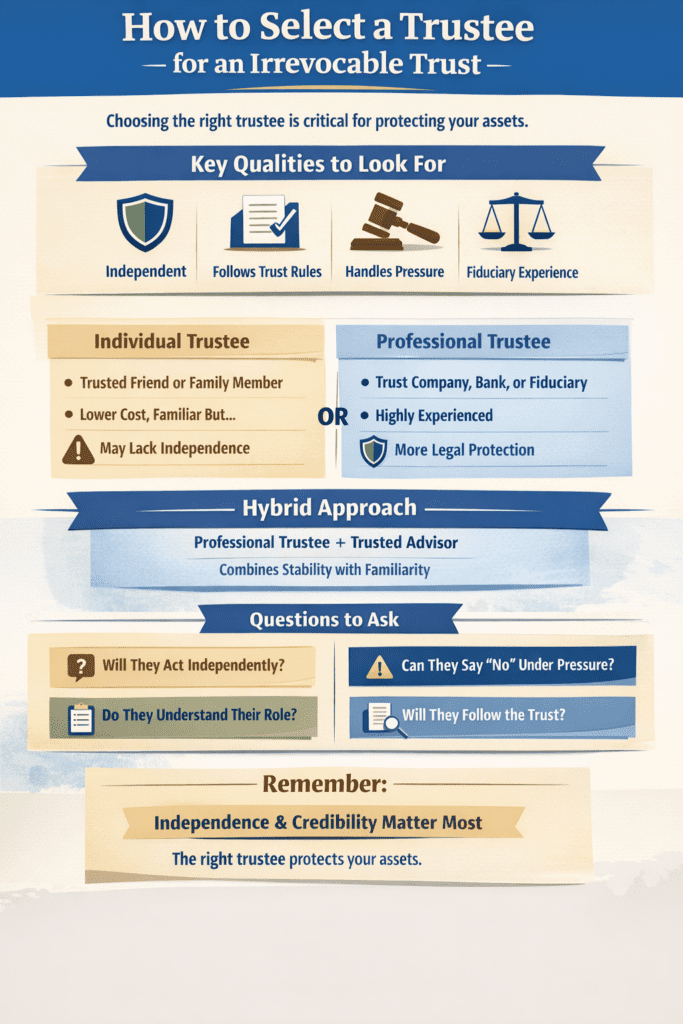

How to Select a Trustee (Individual vs Professional)

Choosing the right trustee is one of the most important decisions in your entire asset protection strategy.

You are not just selecting someone to manage assets—you are selecting the person or entity that stands between your assets and potential claims.

What a Trustee Actually Does

A trustee is responsible for:

- Managing trust assets

- Following the terms of the trust document

- Making distribution decisions

- Acting independently—even when pressured

👉 In an asset protection structure, the trustee must be willing to say no—even to you.

Option 1: Individual Trustee

This can include:

- A trusted friend

- A family member

- A business associate

Advantages

- Lower cost

- Familiarity with your situation

- Potentially more flexible communication

Risks

- May not be truly independent

- May be influenced by personal relationships

- May not withstand legal pressure

- May lack experience in handling complex situations

⚠️ Key Consideration

If the trustee is likely to follow your instructions under pressure, the structure may fail when tested.

Option 2: Professional or Corporate Trustee

This can include:

- Trust companies

- Banks

- Professional fiduciaries

- Attorneys acting in a trustee capacity

Advantages

- True independence

- Experience with fiduciary responsibilities

- Stronger legal credibility

- Less susceptible to emotional or external pressure

Trade-Offs

- Higher cost

- Less personal relationship

- More formal processes

Why This Matters

In high-stakes situations—like lawsuits or creditor claims:

👉 A professional trustee is far more likely to:

- Follow the trust document strictly

- Resist pressure from courts or creditors

- Maintain the integrity of the structure

Hybrid Approach (Common Strategy)

Many effective plans use a combination:

- Primary Trustee: Professional or corporate entity

- Secondary Role: Trusted individual (advisor, co-trustee, or successor)

This allows for:

- Independence where it matters

- Familiarity where it helps

What to Look for in a Trustee

Whether individual or professional, the trustee should have:

- Independence from your direct control

- Willingness to follow the trust—not your instructions

- Understanding of fiduciary responsibility

- Ability to handle pressure (legal, financial, emotional)

- Consistency in decision-making

The American Bar Association emphasizes the importance of proper structuring and fiduciary responsibility when creating trusts as part of an estate or asset protection plan.

⚠️ Key Asset Protection Insight

The strength of your trust is only as strong as the independence of your trustee.

Questions to Ask Before Selecting a Trustee

- Will this person or entity act independently—even if I disagree?

- Can they say “no” under pressure?

- Do they understand the legal responsibility they are taking on?

- Are they prepared to follow the trust document exactly as written?

Final Takeaway

Selecting a trustee is not about convenience—it is about credibility and protection.

- A familiar face may feel comfortable

- A professional structure may be more effective

👉 The right choice depends on your goals—but for asset protection:

Independence is not optional. It is essential.

The RetireCoast Estate Planning Membership includes an exclusive Trustee Selection Tool designed to guide you through this process and help you make a decision that strengthens your overall asset protection strategy.

Case Study: When Control Determines the Outcome

The Situation

Sean owned multiple investment properties and had taken reasonable precautions, including maintaining $2 million in liability insurance.

However, after a serious incident on one of his rental properties, a lawsuit resulted in a $5 million judgment.

This left a $3 million shortfall beyond his insurance coverage.

The Courtroom Moment

Through his attorney, Sean explained to the court:

He did not have sufficient personal assets available to satisfy the remaining judgment.

The plaintiff’s attorney challenged this claim, arguing:

Sean actually had several million dollars in real estate assets that were not encumbered and could be used to satisfy the judgment.

The Key Distinction

When questioned again by the judge, Sean clarified:

He did not personally own those assets.

They were owned by an irrevocable trust, and he had no authority to dispose of them.

The judge was skeptical.

The Judge’s Request

The judge instructed Sean:

Contact the trustee and demand that the assets be liquidated to cover the judgment.

Sean complied and sent the following message to the trustee:

“Judge Samson has ordered me to instruct you to dispose of sufficient assets to cover the $3 million shortfall from the judgment. Please follow the judge’s instructions.”

The Trustee’s Response

Within an hour, the trustee responded:

“Sean, I will not comply. You have no authority to require this, and neither does the court. Please inform your attorney of this response.”

The Legal Reality

Once the response was presented to the court, the judge acknowledged:

- The irrevocable trust was a separate legal entity

- It was not a party to the lawsuit

- Sean did not control the trust assets

👉 Therefore, the court had no authority to compel the trustee to use those assets to satisfy the judgment.

Outcome

The judgment remained enforceable only against Sean personally.

The assets held inside the irrevocable trust were not reachable.

⚠️ Key Lesson

Asset protection is not about hiding assets—it’s about not owning them in the first place.

The critical factor was:

- Sean did not control the assets

- The trustee was independent

- The structure was legally valid and respected

Why This Matters for Real Estate Owners

This case illustrates the exact principle discussed earlier:

- A revocable trust would not have protected these assets

- An irrevocable trust with an independent trustee created separation

- That separation held up—even under court pressure

U.S. courts generally evaluate control and ownership when determining whether assets can be reached, reinforcing the importance of proper structure and separation.

Why the Trustee Refused — and Why the Court Agreed

The Real Reason the Trustee Could Not Be Compelled

At first glance, it may seem surprising that the trustee could refuse both:

- Sean’s request

- And the judge’s instruction

But the answer lies in how the trust was originally structured.

When Sean created the irrevocable trust, he included specific instructions to the trustee, including a critical provision:

If Sean is ever acting under duress, the trustee is to use independent judgment and may deny any requestmade by Sean.

The Key Concept: “Under Duress”

From a legal and practical standpoint:

- A large court judgment

- Pressure to satisfy a debt

- A direct instruction from a judge

👉 All clearly qualify as duress

This triggered the trustee’s duty to:

- Act independently

- Protect the integrity of the trust

- Follow the original trust instructions—not Sean’s immediate request

Why the Judge Could Not Override This

The court ultimately recognized three critical facts:

- The trust was a separate legal entity

- The trustee had independent authority and fiduciary duty

- The trust was not a party to the lawsuit

Because of this:

The judge had no authority to force a third-party trustee to distribute assets from an entity not before the court.

Are the Assets “Locked Away Forever”?

No—and this is an important clarification.

Properly structured irrevocable trusts are not designed to punish the creator—they are designed to create separation while still allowing structured benefit.

Sean could still benefit from the trust:

- As long as distributions followed the rules established at formation

- And were not made under duress or creditor pressure

⚠️ The Critical Element: Independent Trustee

This entire outcome depended on one factor above all others:

The trustee was a disinterested third party

Not:

- Sean himself

- A controlled entity

- Someone acting under Sean’s direction

But someone with:

- Legal authority

- Independent judgment

- A duty to follow the trust—not Sean

Final Takeaway

Asset protection works when control is limited, structure is respected, and independence is real.

Without:

- Proper drafting

- A clear duress provision

- An independent trustee

👉 This outcome could have been very different.

Inside the RetireCoast Estate Planning Membership, you’ll find tools to help you:

• Build your revocable living trust

• Organize your real estate holdings

• Create a complete estate planning portfolio

👉 Start Here

Frequently Asked Questions

1. What is an irrevocable trust and how is it different from a revocable trust?

2. Can an irrevocable trust protect real estate from lawsuits?

3. Can I still benefit from assets placed in an irrevocable trust?

4. Who should I choose as trustee?

5. Can a judge force a trustee to distribute assets?

6. What does “under duress” mean in a trust?

7. Can an irrevocable trust own an LLC or business?

8. What happens if I create the trust after being sued?

9. Does an irrevocable trust eliminate the need for insurance?

10. Is an irrevocable trust right for everyone?

PODCAST

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}