When building a serious asset protection strategy, most people focus on structure—trusts, LLCs, and financing.

But there is one layer that often determines whether the entire plan holds together… or collapses under scrutiny:

👉 Insurance.

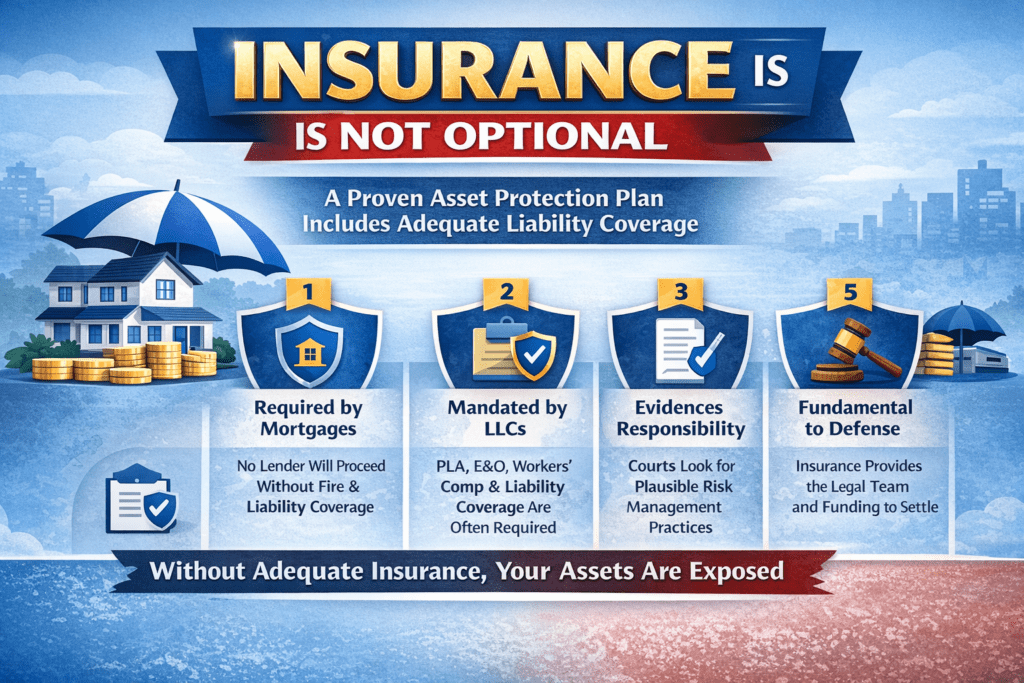

In the RetireCoast 4-Layer Asset Protection Model, insurance is not optional—it is foundational.

- The 4-Layer Protection Model (Quick Reminder)

- Why Insurance Is a Critical Component (Especially With a Mortgage)

- Fire Insurance Is Required — But Liability Is What Really Matters

- Why $2 Million in Coverage May Not Be Enough

- The Smart Upgrade: Umbrella Coverage

- Estimated Cost to Increase Coverage

- What Impacts the Cost?

- Why Higher Coverage Can Actually Prevent Lawsuits from Escalating

- The Insurance Company’s Role: The “Duty to Defend”

- Important Limitations to Understand

- Where to Learn More About Business Insurance

- The Bottom Line: Insurance Validates Your Entire Plan

- Final Takeaway

- Want to see how insurance integrates with the full asset protection system?

- FAQ

The 4-Layer Protection Model (Quick Reminder)

Before diving deeper, here’s where insurance fits:

- Trust Layer → Separates ownership

- LLC Layer → Separates liability

- Insurance Layer → Absorbs financial impact

- Financing Layer (Mortgage Strategy) → Reduces exposed equity

👉 Learn more about the full system:

https://retirecoast.com/asset-protection-real-estate-investors

👉 Irrevocable trust strategy explained:

https://retirecoast.com/irrevocable-trust-asset-protection

Why Insurance Is a Critical Component (Especially With a Mortgage)

If your strategy includes a mortgage—whether held personally, through an LLC, or even by an irrevocable trust—insurance becomes mandatory, not optional.

Lenders Require It

Any entity holding a mortgage will require:

- Fire and hazard insurance

- Coverage sufficient to protect the collateral

- Proper naming of insured parties (including trusts or entities)

Even if the mortgage is part of your asset protection structure, the lender will not close the deal without proof of insurance.

A Missing Policy Can Destroy Your Entire Strategy

This is where things become serious.

If a lawsuit occurs and there is no insurance in place, an opposing attorney could argue:

“This was never a legitimate asset protection plan—this was an attempt to shield assets without taking basic risk precautions.”

That argument can be powerful in court.

⚠️ No insurance = credibility problem

It signals:

- Lack of real risk management

- Intent to avoid responsibility

- Weak overall planning

Fire Insurance Is Required — But Liability Is What Really Matters

Most people think:

“I have insurance, I’m covered.”

But they’re usually referring to property coverage (fire, storm, hazard).

That’s only part of the picture.

The Real Risk: Liability

Liability is where lawsuits originate:

- Slip-and-fall claims

- Tenant disputes

- Contractor injuries

- Property-related negligence

- Business operations exposure

This is where the phrase applies:

👉 “This is where the rubber meets the road.”

Why $2 Million in Coverage May Not Be Enough

Many standard policies offer:

- $1M per occurrence

- $2M aggregate

That sounds like a lot—until you consider:

- Legal fees

- Medical claims

- Pain and suffering awards

- Multiple plaintiffs

For real estate investors, property owners, and business operators, this limit can be insufficient.

The Smart Upgrade: Umbrella Coverage

The solution is straightforward:

👉 Add a Commercial Umbrella Policy

This policy sits on top of your existing coverage and increases your protection.

Example:

- Base policy: $2M

- Umbrella: +$3M

- Total protection: $5M

Estimated Cost to Increase Coverage

Increasing from $2M to $5M typically costs:

👉 $1,200 to $2,700 per year

👉 Roughly $100 to $225 per month

Industry Breakdown:

- Average: $400–$900 per $1M of coverage

- Cost per million often decreases at higher levels

This is one of the highest value upgrades in your entire protection plan.

Hunter and Jennifer built a strong landscaping business with clients across town, including higher-value residential properties. Early in the planning stages of their company, they learned about the RetireCoast Asset Protection Layer Program and quickly put all four layers in place to protect their business, home, and other assets.

As part of their planning, they reviewed their liability insurance with their broker. Their base policy already provided $2 million in coverage, but they chose to add an umbrella policy for additional protection. For a relatively small increase in premium, they added $5 million more in coverage, bringing their total available liability protection to $7 million.

Then the unexpected happened. While trimming a large tree at a client’s property, the tree fell in the wrong direction and crashed into a $2 million home. The impact caused major structural damage, destroyed valuable contents inside the residence, and injured one of the homeowners, who suffered a broken arm.

The client’s attorney presented a claim for $10 million, including repairs to the home, replacement of valuable contents, medical costs, and pain and suffering. Hunter and Jennifer immediately contacted both their insurance broker and their attorney.

After reviewing the situation, their attorney explained that they were in a far stronger position than most business owners because their protection plan had already been built. Their business and assets were structured, their equity was not easily exposed, and their $7 million liability insurance program was available to respond to the claim.

With the help of the insurance company’s attorney, the matter was negotiated and ultimately settled for $4 million. That settlement resolved the claim quickly and saved them from a potentially larger loss while avoiding a long and uncertain court battle.

- Insurance matters. A strong asset protection strategy is incomplete without proper liability coverage.

- Umbrella coverage can change the outcome. The extra coverage created room to settle a major claim without exposing personal assets.

- Attorneys often pursue the easiest source of recovery. When assets are properly structured and tied up, the insurance company may become the most practical source of settlement funds.

- Immediate money often wins. Faced with the option of a prompt settlement or a costly fight in court, the claimant accepted less in exchange for certainty.

- The four layers work together. Insurance did not replace structure—it reinforced it and helped make the entire plan effective.

This example shows why the insurance layer is not just a side issue. It can be the difference between a manageable claim and a financial disaster.

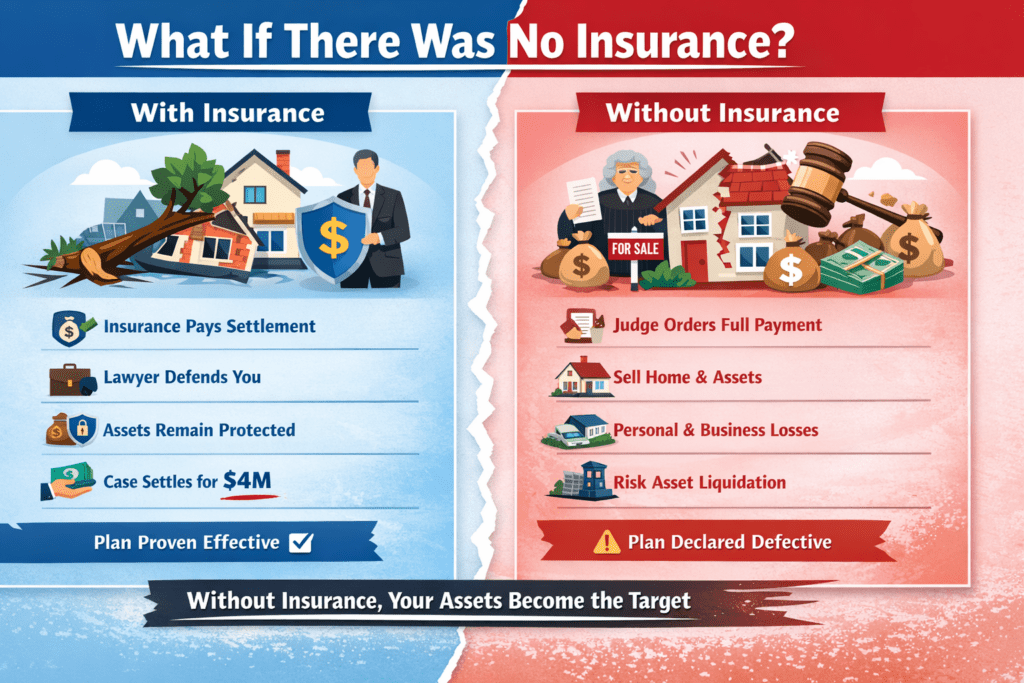

Now consider the same situation—but without proper liability insurance in place.

The tree still falls. The home is still damaged. The homeowner is still injured. The lawsuit still arrives—this time demanding $10 million.

But now there is no insurance company to step in. No legal team provided under a policy. No coverage available to absorb the financial impact.

During the case, the opposing attorney raises a critical argument:

“This was not a legitimate asset protection plan. The defendants failed to carry even basic liability insurance. This structure was designed to avoid responsibility, not manage risk.”

The court reviews the situation and finds that the plan lacks a critical component—real-world risk protection.

As a result, the judge determines that the asset protection structure is defective in practice and allows the claim to proceed aggressively against available assets.

The court orders that the judgment must be satisfied—even if it requires the forced sale of property, liquidation of assets, or seizure of business interests.

Without insurance:

- There is no buffer between the claim and your assets

- Legal defense costs come directly out of pocket

- Settlement leverage is dramatically reduced

- Personal and business assets become primary targets

- Forced liquidation becomes a real possibility

The takeaway: An asset protection plan without insurance is not a complete plan—it is an exposed strategy.

What Impacts the Cost?

Several factors influence pricing:

1. Industry Risk

Higher exposure = higher cost

Examples:

- Property management

- Vacation rentals

- Real estate brokerage

2. Revenue & Scale

More transactions = higher probability of claims

3. Property Type & Location

- Coastal properties

- High-turnover rentals

- Amenities (pools, docks, etc.)

4. Claims History

- Clean record = lower cost

- Prior claims = higher premiums

5. Contractual Requirements

Lenders, leases, or vendors may require minimum coverage levels

Why Higher Coverage Can Actually Prevent Lawsuits from Escalating

This is one of the most misunderstood concepts in asset protection.

Attorneys Follow the Money

Many plaintiff attorneys work on a contingency basis (a percentage of recovery).

That means they prefer:

👉 Fast, certain payouts

Over:

👉 Long, complex legal battles

What Happens in Practice

When a claim is filed:

- Insurance company steps in

- Legal defense is provided

- Settlement negotiations begin

If your coverage is:

- Low → The plaintiff may pursue your personal assets

- High → The insurer becomes the primary target

The Strategic Advantage

A strong policy (e.g., $5M):

✔ Encourages settlement

✔ Keeps disputes within insurance limits

✔ Reduces incentive to pursue personal assets

✔ Makes litigation less attractive beyond policy limits

Add in a Mortgage… and the Strategy Gets Stronger

If a property also has a mortgage:

- Equity is reduced

- Recovery potential is limited

- Litigation becomes less attractive

Combine that with strong insurance:

👉 You’ve created a layered deterrent strategy

The Insurance Company’s Role: The “Duty to Defend”

When you have proper liability coverage, you’re not alone in a lawsuit.

Two Key Obligations

1. Duty to Indemnify

- Pays settlements or judgments (up to policy limits)

2. Duty to Defend

- Provides legal representation

- Pays attorney fees

- Handles litigation strategy

How It Works

- You notify the insurer immediately

- They evaluate coverage

- They assign legal counsel

- They manage defense and settlement

👉 Even if the claim is weak or unfounded, they still defend you

Important Limitations to Understand

Insurance is powerful—but not unlimited.

Coverage Must Apply

- General liability ≠ contract disputes

- Policy must match the claim type

No Coverage for Intentional Acts

- Fraud

- Criminal behavior

- Deliberate harm

Reservation of Rights

- Insurer may defend temporarily while investigating

Policy Limits Matter

- Once limits are exhausted, protection may end

Where to Learn More About Business Insurance

For a deeper look at business insurance options and cost comparisons, you can review resources such as:

👉 Insureon

They provide practical breakdowns of policy types and pricing across industries.

The Bottom Line: Insurance Validates Your Entire Plan

Without insurance:

- Your structure looks incomplete

- Your credibility is weakened

- Your assets are exposed

With proper insurance:

- You demonstrate responsible risk management

- You create a financial buffer against claims

- You strengthen every other layer of your plan

Final Takeaway

A complete asset protection plan is not built on documents alone.

It is built on:

✔ Structure (Trust + LLC)

✔ Strategy (Financing)

✔ Protection (Insurance)

If you skip the insurance layer, you are not protecting your assets—you are exposing them.

🔒 Insurance Is Not Optional

If you are implementing a mortgage strategy or using an irrevocable trust, insurance is not just recommended—it is required.

A properly structured plan without insurance is incomplete and may fail under legal scrutiny.

Want to see how insurance integrates with the full asset protection system?

Inside the RetireCoast Estate Planning Membership, we show you:

- How to coordinate insurance with trusts and LLCs

- How to structure mortgages correctly

- How each layer works together to protect your assets

👉 This is not theory—it’s a complete system.

Insurance is only one layer. Real protection comes from combining trusts, LLCs, insurance, and financing into a coordinated system that works together when it matters most.

Inside the RetireCoast Estate Planning Membership, you’ll gain access to the full Asset Protection Group, including tools, guides, and step-by-step strategies to help you properly structure and protect your assets.

- ✔ Irrevocable Trust planning and tools

- ✔ LLC structure and ownership strategies

- ✔ Insurance layer guidance and evaluation tools

- ✔ Mortgage and financing strategies for asset protection

- ✔ Integrated system designed to work together

Don’t leave your protection plan incomplete. Learn how all four layers work together.

FAQ

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}