Last updated on April 26th, 2026 at 05:04 pm

Introduction

If you own a short-term rental, there’s a good chance you don’t actually know how your property is performing.

That may sound surprising—but it’s extremely common.

Most owners look at one number: the deposit they receive from their property manager or booking platform. If money is coming in, things must be going well… right?

Not necessarily.

Short-term rental accounting is more than just tracking deposits. To truly understand your property, you need to look at income, expenses, and performance together—not in isolation.

This guide will walk you through a simple, practical way to understand your numbers without turning you into an accountant.

- Introduction

- What is a Short-Term Rental (Vacation Home)?

- Personal Use of STR

- An Introduction to Short-Term Rental Accounting

- The Three Layers of Short-Term Rental Accounting

- Understanding Your Property Manager Statement

- What Your Property Manager Statement Shows

- Why It Feels Like the “Answer”

- What the Statement Does NOT Show

- The Most Common Mistake

- How to Use the Statement the Right Way

- Why Property Managers Still Add Value

- Transition to the Next Step

- What Are Owner-Paid Expenses?

- Why Owners Miss Them

- Why These Expenses Matter

- Key Categories to Track

- Why This Matters for Taxes

- A Better Approach

- The Real Goal

- Some Expenses Must Be Depreciated

- Rental Performance Metrics That Actually Matter

- Simple vs Formal Accounting: What Most Owners Actually Need

- How Property Managers Account for Owner Income and Expenses

- GAAP Concepts (Simplified for Short-Term Rental Owners)

- Accounting Systems Compared

- Next Section

- IRS Considerations (High-Level Overview)

- What Comes Next

- Why Most Short-Term Rental Owners Get It Wrong

- Mistake #1: Focusing Only on Deposits

- Mistake #2: Ignoring Owner-Paid Expenses

- Mistake #3: No Consistent Tracking System

- Mistake #4: Misunderstanding Tax Rules

- Mistake #5: Treating It Like a Side Activity

- The Result

- The Better Approach

- Where Most Owners Get Stuck

- That Is Exactly Why We Built a Tool

- Final Thought

- How RetireCoast Helps Short-Term Rental Owners

- Quiz

- FAQ

- PODCAST

Considering the potential consequences of failing to properly account for income and expenses, I wanted to clearly explain what is permitted, what is not, and how to approach it the right way.

This article is designed to be used alongside our premium Business Membership tools, which can significantly improve how short-term rental owners record, organize, and report their financial activity.

What is a Short-Term Rental (Vacation Home)?

We will use the terms short-term rental and vacation home interchangeably in this article—because most people do.

A short-term rental is the official designation used by government agencies to describe a property that is rented for short durations, typically less than 31 days. Properties rented for longer than 30 days are generally classified as long-term rentals and are treated differently for both accounting and tax purposes.

This article focuses specifically on properties rented for under 31 days, which is where most short-term rental accounting complexity—and opportunity—exists.

Vacation Home vs. Short-Term Rental

In everyday conversation, many owners refer to these properties as:

- Vacation homes

- Vacation rentals

- Beach homes or second homes

While the terminology varies, the key distinction for this guide is simple:

👉 The property must generate rental income from third parties (not relatives or personal use).

Many owners use their properties personally and rent them when they are not in residence. This hybrid use is extremely common—but it introduces important considerations for accounting and tax treatment, which we will cover later in this guide.

How Short-Term Rentals Are Managed

Short-term rentals can be operated in two primary ways:

1. Self-Managed

Owners list and manage the property themselves using platforms like:

- Airbnb

- VRBO

This approach offers more control but requires time, effort, and active management.

2. Professionally Managed

Owners hire a property management company to handle:

- Bookings

- Guest communication

- Cleaning and maintenance

- Pricing and marketing

A good property manager can simplify operations significantly and help create a more consistent guest experience.

Why This Matters for Accounting

As you will see throughout this article, how your property is managed directly impacts your short-term rental accounting.

A property manager can:

- Provide structured monthly statements

- Help document income and expenses

- Support your position that the property is actively used for income

This can be especially important when demonstrating to the IRS that your property qualifies for allowable deductions.

To be treated as an income-producing property, your short-term rental must generate legitimate rental income from third parties and be operated with the intent to produce income.

How you manage the property—whether directly or through a property manager—can play a role in supporting proper classification and maintaining accurate records.

The RetireCoast STR Income & Expense Review Tool helps you bring everything together in one place so you can track income, expenses, and cash flow with clarity and confidence.

This premium tool is available as part of the RetireCoast Business Membership for owners who want more control, better organization, and a clearer picture of their rental business.

Personal Use of STR

Every day you, your family, or your friends stay in the property without paying rent represents an opportunity cost.

👉 That is income your property could have generated—but didn’t.

If you want to fully understand your property’s performance, it helps to estimate not only what you earn—but also what you could have earned.

The calculator below gives you a practical way to see the potential revenue impact of personal stays. This is not meant to discourage personal use—it’s simply a tool to give you a clearer view of your property’s full earning potential.

At the end of the day, it’s your property—and your decision.

An Introduction to Short-Term Rental Accounting

The sections below will introduce you to how to properly account for income and expenses for your property.

Before we go further, it’s important to understand one key point:

👉 Not every expense is deductible—and even allowable deductions may not apply to every owner.

Short-term rental accounting is influenced by several factors, including:

- How often the property is rented

- How often is it used personally

- How the property is managed

- How well income and expenses are documented

This guide is designed to help you understand the process, not to replace professional tax or legal advice. The goal is to give you a clear framework so you can avoid common mistakes and better understand how IRS rules apply to your situation.

Why This Matters

Failing to properly account for your short-term rental can lead to:

- Missed deductions

- Incorrect reporting

- Increased audit risk

- Poor investment decisions

On the other hand, a well-organized approach allows you to:

- Track true performance

- Support your tax position

- Make informed decisions about your property

The Good News

The good news is that short-term rental accounting does not have to be complicated.

With a simple, consistent system:

- You can track your income and expenses clearly

- You can understand how your property is performing

- You can stay organized throughout the year—not just at tax time

Use the Resources Available to You

There are resources available to help you make informed decisions.

Your first step—after reviewing this article and using the RetireCoast Business Membership tools—is to discuss your specific situation with a qualified professional:

- If you already own a property, review your numbers and plans with your CPA

- If you are considering purchasing a short-term rental, speak with a real estate agent experienced in income-producing properties

- You can also consult official guidance directly from the Internal Revenue Service (IRS) using the references provided later in this guide

Taking the time to confirm your approach with the right resources can help you avoid costly mistakes and ensure your property is structured and managed correctly from the start.

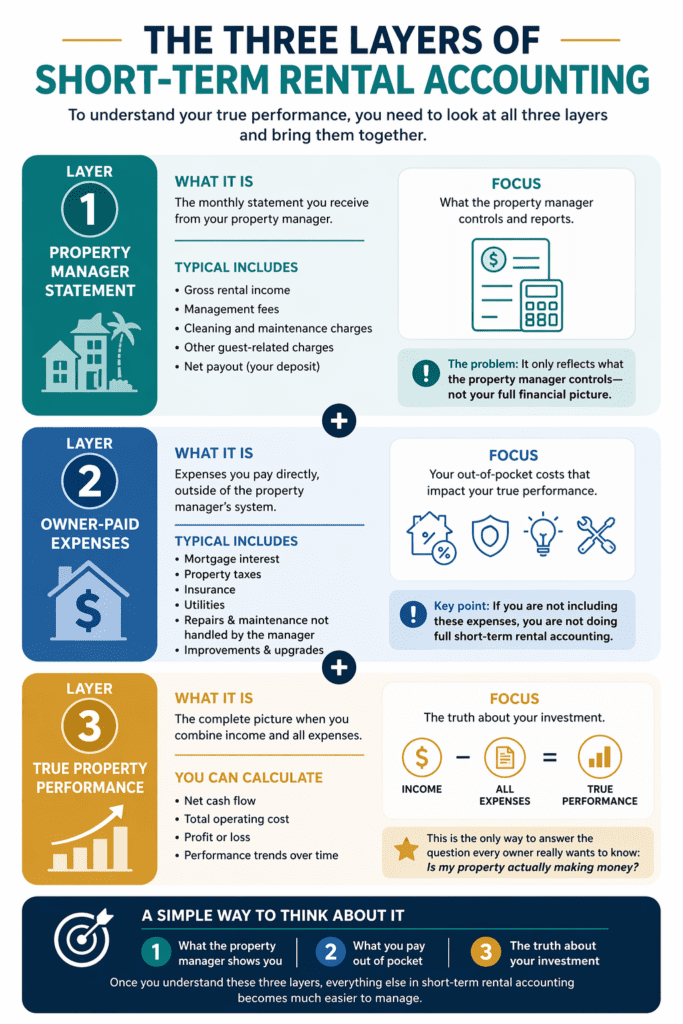

The Three Layers of Short-Term Rental Accounting

To properly understand short-term rental accounting, you need to think in layers.

Most owners only look at one piece of the puzzle—usually the money they receive each month. But that number alone does not tell you whether your property is actually performing well.

To get a clear picture, you need to look at three separate layers of information and then bring them together.

Layer 1: Property Manager Statement

This is where most short-term rental owners start.

If you use a property manager, you will typically receive a monthly statement showing:

- Gross rental income

- Management fees

- Cleaning and maintenance charges

- Net payout (your deposit)

This statement is structured and easy to read, which is why many owners rely on it as their primary financial reference.

👉 The problem:

It only reflects what the property manager controls—not your full financial picture.

Layer 2: Owner-Paid Expenses

The second layer is where many owners lose track of their true numbers.

These are expenses you pay directly, outside of the property manager’s system:

- Mortgage interest

- Property taxes

- Insurance

- Utilities

- Repairs not handled by the manager

- Improvements and upgrades

These costs can be significant—and if they are not tracked consistently, your understanding of your property’s performance will be incomplete.

👉 Key point:

If you are not including these expenses, you are not doing full short-term rental accounting.

Layer 3: True Property Performance

The third layer is where everything comes together.

This is the point where you combine:

- Rental income

- Property manager expenses

- Owner-paid expenses

From this, you can calculate:

- Net cash flow

- Total operating cost

- Profit or loss

- Performance trends over time

This is the only way to answer the question every owner really wants to know:

👉 Is my property actually making money?

Why These Three Layers Matter

When you separate and then combine these layers, several important things happen:

- You eliminate confusion between deposits and profit

- You gain visibility into where your money is going

- You can make better decisions about pricing, expenses, and improvements

- You create a clear record for tax reporting

Most importantly, you move from guessing to understanding.

A Simple Way to Think About It

- Layer 1: What the property manager shows you

- Layer 2: What you pay out of pocket

- Layer 3: The truth about your investment

Once you understand these three layers, everything else in short-term rental accounting becomes much easier to manage.

Understanding Your Property Manager Statement

For many short-term rental owners, the property manager statement is the primary financial document they review each month.

It’s structured, consistent, and easy to understand—which is exactly why it can also be misleading if viewed in isolation.

What Your Property Manager Statement Shows

A typical statement from a property manager will include:

- Gross rental income (total bookings collected)

- Management fees (percentage or fixed fee)

- Cleaning fees

- Maintenance and repair charges

- Other guest-related costs

- Net payout (the amount deposited into your account)

This document is valuable because it provides a clear summary of what happened operationally during the month.

Why It Feels Like the “Answer”

When you receive your monthly deposit, it’s natural to think:

👉 “This is what my property made.”

After all:

- It’s real money

- It hits your bank account

- It’s tied to bookings and activity

But this is where many owners unintentionally misunderstand their numbers.

What the Statement Does NOT Show

Your property manager’s statement does not include your full financial picture.

It typically excludes:

- Mortgage payments (especially the interest portion)

- Property taxes

- Insurance premiums

- Utilities (in many cases)

- Capital improvements or upgrades

- Long-term maintenance costs

These are often your largest expenses—and they exist completely outside the manager’s reporting system.

The Most Common Mistake

The biggest mistake short-term rental owners make is simple:

👉 They confuse their deposit with their profit.

For example:

- Monthly deposit: $3,200

- Owner-paid expenses: $2,800

- Actual cash flow: $400

Without including all expenses, it’s easy to overestimate performance and make decisions based on incomplete information.

How to Use the Statement the Right Way

Your property manager’s statement is still extremely useful—it just needs to be used correctly.

Think of it as:

👉 Layer 1 of your short-term rental accounting system

Use it to:

- Track rental income trends

- Understand operational costs

- Verify bookings and occupancy

- Monitor management performance

But always combine it with your owner-paid expenses to get the full picture.

Why Property Managers Still Add Value

Despite its limitations, a good property manager provides significant advantages:

- Consistent monthly reporting

- Organized tracking of income and operational expenses

- Documentation that supports your income activity

- Professional management of bookings and guests

In many cases, having a property manager also helps demonstrate that your property is being operated with the intent to generate income—an important factor for tax treatment.

Transition to the Next Step

Now that you understand what your property manager statement does—and does not—show, the next step is to fill in the missing piece:

Owner-Paid Expenses: The Missing Piece

If you want to understand how your short-term rental is really performing, you have to go beyond the property manager’s statement.

That means tracking the expenses you pay yourself.

These owner-paid expenses are the missing piece in short-term rental accounting because they often represent a large share of the property’s real cost, but they do not appear on the monthly statement from your property manager.

What Are Owner-Paid Expenses?

Owner-paid expenses are costs connected to the property that you pay directly, outside of the property manager’s system.

Common examples include:

- Mortgage interest

- Property taxes

- Insurance premiums

- Utilities

- Internet or cable

- Repairs you arrange directly

- Supplies purchased outside the manager’s system

- HOA dues or condo fees

- Licensing or permit fees

- Professional services such as bookkeeping or tax preparation

Some of these costs occur every month. Others show up only a few times a year. Both need to be tracked.

Why Owners Miss Them

These expenses are easy to overlook because they are spread across different places:

- Bank accounts

- Credit cards

- Utility bills

- Insurance invoices

- Mortgage statements

Because of this, many owners know what they received from the property manager but do not have a single place showing what they spent.

That creates a false sense of profitability.

Why These Expenses Matter

A short-term rental may look profitable based on deposits alone, but once owner-paid expenses are included, the result can be very different.

For example:

- Net deposit from property manager: $4,700

- Mortgage interest: ($1,450)

- Insurance: ($325)

- Utilities: ($410)

- Owner-paid repairs: ($550)

Actual cash flow: $1,965

This is why owner-paid expenses are essential to understanding:

- true cash flow

- total operating cost

- long-term performance

- accurate financial reporting

Key Categories to Track

Mortgage Interest

Often one of the largest expenses, and important for both performance tracking and tax reporting.

Insurance

Short-term rental properties often require specialized coverage.

Utilities

Electricity, water, internet, and other services can vary significantly month to month.

Repairs and Maintenance

Both small and large repairs should be tracked consistently.

Taxes, Fees, and Dues

Property taxes, HOA dues, and permits are part of the true cost of ownership.

Why This Matters for Taxes

Not every expense is deductible, and not every deduction applies to every owner.

The goal is not to decide that on your own.

The goal is to track everything clearly and then review it with your CPA.

Good records make tax reporting easier and help avoid missed deductions or reporting errors.

A Better Approach

Instead of trying to reconstruct everything at tax time, use a simple monthly process:

- Review your property manager statement

- Gather your owner-paid expenses

- Organize them into consistent categories

- Compare total expenses against income

- Review the results

This does not need to be complicated. It just needs to be consistent.

The Real Goal

The goal is not just to track expenses.

The goal is to understand your property.

Once you combine your property manager statement with your owner-paid expenses, you will finally see how your short-term rental is actually performing. That is when better decisions become possible.

Some Expenses Must Be Depreciated

Pay close attention to this section.

Not all expenses can be deducted in the year they are incurred. The IRS has specific rules for how real property and certain major expenses must be handled, and in many cases, those costs must be depreciated over time rather than deducted all at once.

What This Means for You

Certain larger expenses—such as:

- Remodels

- Major upgrades

- Structural improvements

- Furniture and equipment (in some cases)

may need to be spread out over multiple years instead of being treated as a simple expense in the current year.

This can have a significant impact on:

- Your taxable income

- Your reported profit or loss

- How your property performs on paper

Why This Matters

Many short-term rental owners assume that any money spent on the property can be deducted immediately.

That is not always the case.

Improperly classifying these expenses can:

- Reduce allowable deductions in the current year

- Create issues if reviewed by the IRS

- Distort your understanding of true performance

We Cover This in Detail Separately

This topic is important enough that we created a dedicated article to walk through it in detail, including:

- How depreciation works for real property

- How to handle major expenses correctly

- How personal use affects your ability to deduct expenses

➡️ https://retirecoast.com/3short-term-rental-tax-mistakes/

That article also includes three free tools to help you:

- determine the correct depreciation basis for your property

- Evaluate how major expenses should be treated

- understand how personal use may limit deductions

Keep It Simple Here

For now, the key takeaway is this:

👉 Not every expense is treated the same, and some must be handled over time rather than immediately.

As you build your short-term rental accounting system, focus on:

- tracking all expenses clearly

- separating routine costs from major improvements

- working with your CPA to classify them correctly

The deeper rules are covered in the article above, and it is well worth reviewing before making assumptions about what you can deduct.

We created a dedicated guide that explains how depreciation works, how to handle major expenses, and how personal use can affect your ability to claim deductions.

It also includes three free tools to help you calculate depreciation basis and evaluate property usage correctly.

Rental Performance Metrics That Actually Matter

Once you understand your income and expenses, the next step in short-term rental accounting is measuring how your property is actually performing.

Many short-term rental owners focus only on total income or monthly deposits. While those numbers are important, they do not tell the full story.

To properly evaluate your short-term rental property, you need to track a few key performance metrics.

Occupancy Rate

Occupancy rate measures how often your property is rented compared to how often it is available.

It is typically calculated as:

- total rental days divided by total available days

For example:

- 180 rental days out of 300 available days = 60% occupancy

This metric helps you understand:

- demand for your property

- seasonal trends

- whether your pricing strategy is working

A high occupancy rate does not always mean higher profit—but it is a critical indicator of rental activity.

Revenue Per Rental Day

Instead of only tracking total gross income, it is important to understand how much your property earns per booked night.

This is often referred to as:

👉 Revenue per rental day

It helps you:

- compare performance across different months

- evaluate pricing decisions

- identify underperforming periods

For example:

- $6,000 monthly income over 20 booked nights = $300 per night

This metric provides better insight than total income alone.

Gross Income vs Net Cash Flow

Many short-term rental owners focus on gross income, but your real performance depends on cash flow.

- Gross income = total rental income before expenses

- Net cash flow = income after all expenses

This is where your earlier work becomes important.

Once you combine:

- property manager statements

- owner-paid expenses

you can calculate your true cash flow and understand your actual return.

Impact of Personal Use

Personal use directly affects performance.

Every day the property is used for personal purposes:

- reduces total rental days

- reduces gross income potential

- may affect tax treatment

Tracking the number of days used for personal use versus rental use is essential for both performance analysis and tax reporting.

Why These Metrics Matter

Tracking these metrics allows you to:

- evaluate the effectiveness of your rental operations

- make informed pricing decisions

- identify opportunities to increase income

- control expenses and improve efficiency

- better prepare for tax time and reporting

Without these metrics, you are relying on incomplete information.

The Goal

The goal is not just to track income and expenses.

The goal is to understand how your property performs over time.

When you combine:

- accurate records

- consistent tracking

- meaningful metrics

You move from simply owning a short-term rental to actively managing a short-term rental business.

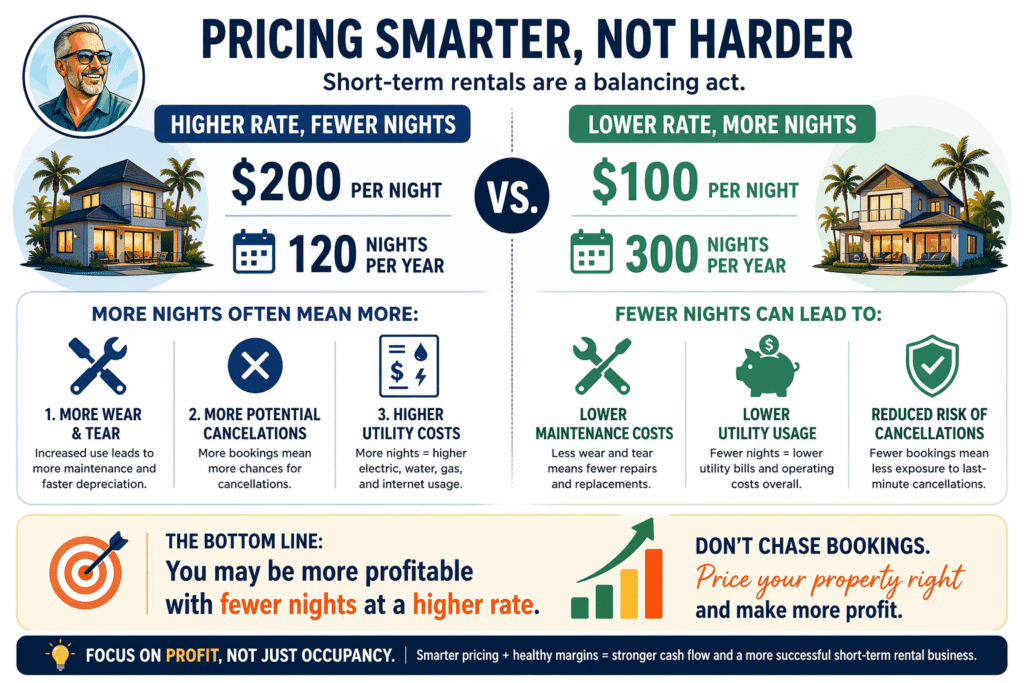

You can charge the market rate for a property—say $200 per night—and book 120 nights per year, or you can lower your rate to $100 and book 300 nights per year.

At first glance, higher bookings may seem better. But more nights often mean:

1. More wear and tear on your property 2. Greater exposure to cancellations 3. Higher utility and operating costs

Fewer, higher-priced bookings can lead to:

– Lower maintenance costs – Reduced utility usage – Less operational stress

👉 The bottom line: You may be more profitable with fewer nights at a higher rate.

Don’t chase bookings. Price your property correctly—and focus on profit, not just occupancy.

Simple vs Formal Accounting: What Most Owners Actually Need

At this point, you understand your income, your expenses, and the key metrics that drive performance.

The next question is:

👉 How should you actually track all of this?

The answer depends on how complex your short-term rental operation is—but for most owners, the solution is simpler than you might think.

Cash Accounting (The Most Common Approach)

Most short-term rental owners use a method called cash accounting.

This simply means:

- Income is recorded when it is received

- Expenses are recorded when they are paid

For example:

- A rental payment received in June is recorded in June

- A repair paid in July is recorded in July

This method aligns closely with:

- your bank account

- your cash flow

- how most people naturally think about money

Why Cash Accounting Works for Most Owners

Cash accounting is widely used because it is:

- simple to understand

- easy to maintain

- aligned with real cash flow

- sufficient for many tax reporting situations

For most short-term rental owners, especially those with one or two properties, this approach provides all the clarity needed to:

- track income and expenses

- prepare for tax time

- evaluate performance

Accrual Accounting (More Advanced)

A more advanced method is accrual accounting.

This approach records:

- income when it is earned

- expenses when they are incurred

Even if the money has not yet been received or paid.

For example:

- A booking in December for a January stay may be recorded in December

- An invoice received in one month but paid later may still be recorded earlier

When Accrual Accounting Makes Sense

Accrual accounting is typically used when:

- You own multiple short-term rental properties

- Your rental activity has grown into a larger business,

- You need more detailed financial reporting

- You are working closely with a CPA or financial advisor

It provides a more precise financial picture, but it also requires more structure and effort.

Simple vs Accurate: Finding the Right Balance

Many short-term rental owners assume they need complex accounting systems from the start.

That is usually not necessary.

👉 The goal is not to make accounting complicated.

👉 The goal is to make your numbers clear.

A simple system that you actually use every month is far more valuable than a complex system you avoid.

What the IRS Cares About

From a tax perspective, the IRS is less concerned with which method you choose and more concerned with:

- consistency in your reporting

- proper documentation

- accurate records of income and expenses

Whether you use a simple spreadsheet, a tool, or accounting software, the key is maintaining:

- accurate records

- clear categorization

- proper documentation

A Practical Approach for Most Owners

For most short-term rental owners, the best approach is:

- Use a simple system (like cash accounting)

- track income and expenses monthly

- maintain detailed records

- review performance regularly

- work with a CPA when needed

This approach gives you:

- clarity

- flexibility

- confidence in your numbers

Where This Leads Next

Now that you understand how to track your income and expenses, the next step is to connect this process to broader accounting principles that help keep everything consistent and reliable.

👉 Up next: GAAP Concepts (Simplified for Property Owners)

- Simple and easy to use

- Matches your bank account activity

- Focuses on real cash flow

- Ideal for most short-term rental owners

- More detailed financial tracking

- Matches income with related expenses

- Used by larger or growing rental businesses

- Often requires accounting software or CPA support

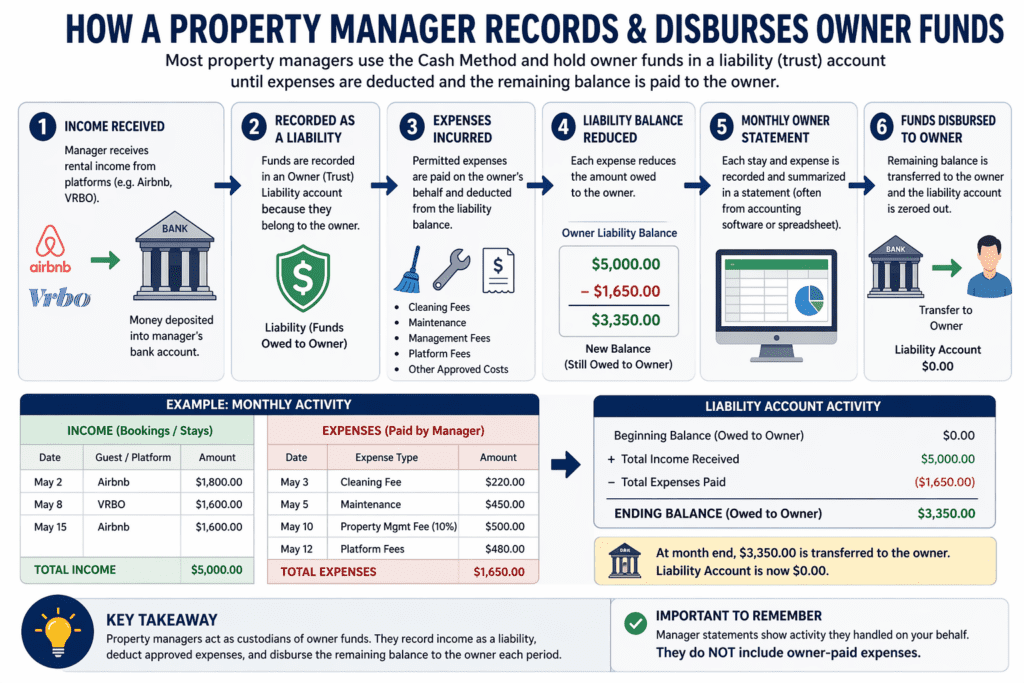

How Property Managers Account for Owner Income and Expenses

Most property managers structure their accounting systems with one key assumption:

👉 Most clients own one or a small number of short-term rental properties

Because of this, they typically use a cash-based approach for reporting activity to owners.

How the Process Works

When a property manager receives rental income from platforms like Airbnb or VRBO, that money is not recorded as their income.

Instead:

- It is recorded as a liability (funds owed to the property owner)

- These funds are typically held in a trust or owner account

As expenses are incurred, the manager deducts approved costs from that balance, including:

- Property management fees

- Cleaning fees

- Maintenance costs

- Platform or service fees (depending on structure)

Each deduction reduces the amount owed to the owner.

Monthly Owner Statement

Property managers track:

- Each booking or stay

- Each expense charged to the property

- The remaining balance owed to the owner

This activity is summarized in a monthly statement, often generated from accounting software or exported into a spreadsheet.

Year-End Tax Reporting (Important)

At the end of the tax year, the property manager will typically issue an IRS Form 1099-MISC (or 1099-NEC, depending on structure).

👉 This form often reports 100% of the gross income received from rental platforms such as Airbnb or VRBO—not just the amount you received after expenses.

This is where many short-term rental owners get confused.

The IRS sees the gross income, not your net deposit.

What This Means for You

It is your responsibility as the property owner to:

- Report the full amount of rental income (typically on Schedule E)

- Apply your deductible expenses against that income

- Maintain proper documentation and records

This includes both:

- Expenses shown on the property manager statement

- Owner-paid expenses not shown by the manager

How RetireCoast Helps

This is exactly where most owners struggle—and where mistakes can happen.

👉 The RetireCoast STR Income & Expense Review Tool, available through the Business Membership, helps you:

- Organize gross income correctly

- Combine manager-reported and owner-paid expenses

- Calculate true cash flow and taxable income

- Prepare for tax time with clear, structured records

Key Takeaway

Property manager statements show what was handled on your behalf.

👉 They do not show your full financial picture—or your final taxable result.

That is why combining all income and expenses in one system is essential for accurate short-term rental accounting.

GAAP Concepts (Simplified for Short-Term Rental Owners)

You do not need to be an accountant to manage a short-term rental successfully.

However, understanding a few basic accounting principles can help you avoid costly mistakes and keep your numbers clear and consistent.

These concepts come from what is known as GAAP (Generally Accepted Accounting Principles), but we will keep this simple and practical.

Matching Income and Expenses

One of the most important concepts is:

👉 Match income with the expenses required to generate it

In practical terms, this means:

- If your property generates income in a given period

- You should include the expenses related to that income in the same period

For example:

- Rental income in July

- Cleaning, maintenance, and utilities are tied to those stays

When you match these correctly, you get a more accurate picture of your property’s performance.

Consistency Matters

Consistency is more important than complexity.

Choose a system and use it the same way every time:

- Same categories for income and expenses

- Same method of tracking (cash or accrual)

- Same process each month

This helps you:

- Compare performance over time

- identify trends

- reduce errors

Inconsistent tracking leads to confusion and unreliable data.

Proper Documentation

The IRS does not expect perfection—but it does expect documentation.

This includes:

- receipts for expenses

- bank statements

- Property Manager Statements

- invoices and service records

👉 Good documentation supports your tax return and reduces risk if your records are reviewed.

Separate Business and Personal Activity

Because a short-term rental is treated as a business, it is important to separate:

- personal expenses

- rental-related expenses

This often means:

- using a separate bank account

- clearly identifying personal use vs rental use

- avoiding mixing personal and business transactions

This separation makes accounting easier and improves accuracy.

Understand Classification

How your property is classified affects everything:

- deductible expenses

- depreciation

- tax treatment

As discussed earlier:

- personal use

- rental use

- number of days

All play a role in how the IRS views your property.

Keep It Practical

You do not need to apply every accounting rule perfectly.

👉 You do need to be consistent, organized, and accurate.

If you:

- Track all income

- track all expenses

- maintain documentation

- Review your numbers regularly

You are already applying the most important principles of good accounting.

The Real Benefit

When you follow these basic concepts:

- your financial records become clearer

- your tax preparation becomes easier

- your decisions become more informed

- your risk of costly mistakes is reduced

In short, you move from guessing…

👉 to understanding your short-term rental as a real business.

Accounting Systems Compared

| Tool | Cost | Best For | Key Strength | Limitations |

|---|---|---|---|---|

| RetireCoast STR Tool | Included with Membership | STR owners who want simple clarity | Combines manager + owner expenses into true cash flow | Not a full double-entry accounting system |

| Wave | $0/month | Sole proprietors | Free, simple accounting | Limited partnership tracking |

| Stessa | $0/month | Real estate owners | Schedule E categories built-in | Not ideal for partnerships |

| QuickBooks Online | $35/month | Multi-member LLCs | Full accounting + CPA integration | Higher cost, more complex |

| Xero | $29/month | LLCs and partnerships | Strong accounting at lower cost | Learning curve |

| Baselane | $0/month | New landlords | Banking + bookkeeping combined | Less robust for complex accounting |

Throughout the year, transactions from the property’s bank account automatically flow into the system, making it easy to track income and expenses without manual entry.

At year-end, the author’s CPA is given access to the account and can download the data directly to prepare the tax return, including Schedule E reporting.

👉 Wave is completely free for core accounting features. They also offer optional paid services such as payroll and upgraded features, but most short-term rental owners will find the free version more than sufficient.

Next Section

👉 IRS Considerations (High-Level Overview)

This will connect everything you’ve learned to how your rental activity is actually reported and taxed.

Many short-term rental properties are subject to local sales taxes, lodging taxes, or hotel taxes. When you report rental activity at the local level, that information can be shared with the IRS.

Likewise, if you report income to the IRS but fail to comply with local tax obligations, local authorities may identify discrepancies. In many cases, platforms like Airbnb and VRBO already collect and remit certain taxes—and they report transaction activity.

Today, data matching and AI-driven analysis are being used to identify gaps in reporting. Some cities actively monitor rental platforms and even listings on sites like Facebook Marketplace to locate unreported short-term rental activity.

👉 The bottom line: avoiding proper accounting and reporting is not worth the risk.

Accurate records, proper documentation, and consistent reporting are essential for protecting your investment and avoiding costly penalties.

IRS Considerations (High-Level Overview)

Understanding how your short-term rental is viewed by the IRS is an essential part of short-term rental accounting.

This section is not meant to replace professional tax advice. Instead, it provides a practical overview of how your rental activity is generally treated and why proper tracking matters.

Reporting Rental Income

All income generated from your short-term rental must be reported on your tax return.

This typically includes:

- income received from platforms like Airbnb and VRBO

- direct bookings

- cleaning fees and other charges paid by guests

In most cases, this income is reported on Schedule E as part of your tax return.

👉 Even if you do not receive the full amount (because fees are deducted), the IRS may still see the gross income, especially if a Form 1099 is issued.

Deductible Expenses

Short-term rental owners can generally deduct ordinary and necessary expenses related to operating the property.

These may include:

- property management fees

- cleaning fees

- maintenance costs

- utilities

- insurance premiums

- mortgage interest

- property taxes

- platform fees and service fees

- professional services such as accounting or legal fees

These deductions reduce your taxable rental income and ultimately your overall tax liability.

Depreciation (Brief Overview)

Depreciation allows you to deduct the cost of your property over time.

For most residential rental property:

- The building (not the land) is depreciated over 27.5 years

Depreciation can significantly reduce your taxable income, even if your property is producing positive cash flow.

👉 Because this topic can be complex, we cover it in detail in a separate guide (linked earlier in this article).

Personal Use and Allocation Rules

If you use the property for personal purposes, the IRS requires you to:

- Track the number of rental days vs personal use days

- , and allocate expenses based on usage

These rules can affect:

- How much can you deduct

- whether your property is classified as a rental property or a personal residence

- Your overall tax treatment

👉 This is one of the most common areas where short-term rental owners make mistakes.

Passive Activity Loss Rules

In many cases, rental activity is considered a passive activity by the IRS.

This means:

- rental losses may not always be used to offset other income (like W-2 wages)

- Deductions may be limited based on your income level

However, exceptions may apply depending on:

- your level of involvement (material participation)

- your income

- how your rental activity is structured

Recordkeeping and Documentation

The IRS expects short-term rental owners to maintain:

- accurate records of income and expenses

- receipts and invoices

- Property Manager Statements

- bank statements

- documentation of personal vs rental use

👉 Good recordkeeping is one of the most important ways to reduce errors and avoid problems at tax time.

Why This Matters

When you combine:

- proper tracking

- consistent accounting

- clear documentation

You are better positioned to:

- Reduce your tax burden legally

- support your deductions

- avoid costly mistakes

- simplify tax preparation

The Practical Takeaway

You do not need to master every IRS rule.

👉 You do need to track everything clearly and consistently.

That is the foundation of good short-term rental accounting—and the key to staying compliant while maximizing the benefits available to you.

What Comes Next

👉 Why Most Short-Term Rental Owners Get It Wrong

This section will bring everything together and highlight the common mistakes your readers are likely already making.

Why Most Short-Term Rental Owners Get It Wrong

By now, you have seen how short-term rental accounting actually works.

But here is the reality:

👉 Most short-term rental owners are not doing this correctly.

Not because it is difficult—but because they are missing key pieces.

Mistake #1: Focusing Only on Deposits

Many owners look at the amount transferred from their property manager and assume that is their profit.

It is not.

That number:

- does not include owner-paid expenses

- does not reflect total operating costs

- does not show true cash flow

👉 This is the most common mistake—and the most misleading.

Mistake #2: Ignoring Owner-Paid Expenses

Expenses like:

- mortgage interest

- property taxes

- insurance premiums

- utilities

- repairs

are often tracked separately—or not tracked at all.

Without these, you do not have:

- accurate financial records

- a clear understanding of your rental activity

- a reliable view of your investment

Mistake #3: No Consistent Tracking System

Many short-term rental owners rely on:

- scattered bank statements

- emails and receipts

- Property Manager Reports

But no single system that brings everything together.

This leads to:

- confusion at tax time

- missed deductions

- inaccurate reporting

Mistake #4: Misunderstanding Tax Rules

Common misunderstandings include:

- assuming all expenses are deductible immediately

- ignoring depreciation rules

- not tracking personal use correctly

- misunderstanding how taxable income is calculated

These mistakes can:

- increase your tax liability

- Reduce allowable deductions

- create issues with your tax return

Mistake #5: Treating It Like a Side Activity

Even though short-term rentals generate income, many owners treat them casually.

In reality:

👉 A short-term rental is a business.

Without:

- accurate records

- proper documentation

- consistent review

it becomes difficult to:

- measure performance

- manage costs

- prepare for tax season

The Result

When these mistakes add up, owners often:

- overestimate profitability

- underestimate expenses

- miss tax benefits

- face unnecessary stress during tax preparation

The Better Approach

The solution is not complicated.

It comes down to:

- tracking all income (not just deposits)

- tracking all expenses (including owner-paid costs)

- using a consistent system

- reviewing your numbers regularly

👉 When you do this, everything changes.

You gain:

- clarity

- control

- confidence

Where Most Owners Get Stuck

Most owners understand this in theory.

But in practice, they struggle to:

- organize their data

- combine multiple sources

- track everything consistently

- make sense of the numbers

That Is Exactly Why We Built a Tool

This is the gap the RetireCoast STR Income & Expense Review Tool is designed to fill.

It helps you:

- bring together property manager statements and owner-paid expenses

- Organize income and expenses into clear categories

- calculate true cash flow and performance

- Prepare for tax time with accurate records

Final Thought

Short-term rental accounting is not about being perfect.

👉 It is about being organized and consistent.

When you have the right system in place, your property becomes easier to manage, easier to understand, and far more valuable as an investment.

How RetireCoast Helps Short-Term Rental Owners

By now, you have a clear understanding of how short-term rental accounting works—and why so many owners struggle to get it right.

The challenge is not knowing what to do.

👉 The challenge is having a simple, reliable way to do it consistently.

The Problem Most Owners Face

Short-term rental owners often deal with:

- Property manager statements in one place

- owner-paid expenses in another

- bank accounts and credit cards spread across multiple sources

- no single system that brings everything together

At tax time, this usually turns into:

- searching for documents

- estimating missing expenses

- relying heavily on a CPA to reconstruct the numbers

A Better Way to Manage Your Rental

The RetireCoast STR Income & Expense Review Tool was created to solve this exact problem.

It gives you a simple way to:

- Organize gross income from your rental activity

- Combine property manager statements with owner-paid expenses

- Categorize deductible expenses clearly

- calculate true cash flow—not just deposits

- maintain accurate records throughout the year

Built for Real Owners

This tool is designed specifically for:

- short-term rental owners

- vacation rental property owners

- clients working with property managers

- real estate investors who want clarity without complexity

It is not designed to replace full accounting software.

👉 It is designed to give you a clear, practical view of your property’s performance.

Works Alongside Your Accounting System

Whether you use:

- a simple system like Wave or Stessa

- a full accounting platform like QuickBooks or Xero

- or no system at all

the RetireCoast tool works as a performance and organization layer that helps you:

- understand your numbers

- identify gaps

- Prepare clean data for your CPA

Part of the Business Membership

The STR Income & Expense Review Tool is included in the RetireCoast Business Membership.

This membership is designed for owners who want:

- better organization

- more control over their finances

- clearer insight into their investment performance

- tools that simplify complex processes

Take the Next Step

If you want to move beyond guesswork and start managing your short-term rental with clarity and confidence:

👉 Explore the Business Membership and access the STR Income & Expense Review Tool.

Final Thought

Short-term rental ownership can be a great investment—but only if you understand your numbers.

When you:

- track income correctly

- account for all expenses

- apply consistent systems

you turn your property from a guessing game…

👉 into a well-managed, income-producing asset.

- ✔ STR Income & Expense Review Tool

- ✔ Organized tracking for rental income and expenses

- ✔ Clear visibility into true cash flow and performance

- ✔ Tools designed specifically for short-term rental owners

- ✔ Guidance to help you prepare for tax time with confidence

- ✔ Ongoing access to new tools and updates

Quiz

FAQ

PODCAST

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}