Last updated on May 17th, 2026 at 01:19 pm

Short-term rentals (STRs) offer some of the most powerful tax advantages in the entire real estate industry. Between accelerated depreciation, deductible travel, and the ability to write off operational losses, a well-managed coastal rental can effectively wipe out your tax bill. This article will help you avoid short-term rental tax mistakes.

But those massive deductions come with a catch: The IRS watches short-term rental owners like a hawk.

Because the tax benefits are so lucrative, vacation rentals are a prime target for audits. A simple misunderstanding of your property’s value, how you categorize a renovation, or even how you handle a family vacation can completely unravel your tax strategy.

These aren’t just minor clerical errors. They are critical mistakes that can trigger an audit, force the IRS to reclassify your property as a personal residence, and result in thousands of dollars in back taxes and penalties.

If you want to protect your wealth, maximize your deductions legally, and keep the IRS out of your bank account, you must understand the rules of the game. Here are the three most critical tax traps that catch short-term rental owners off guard—and exactly how to avoid them.

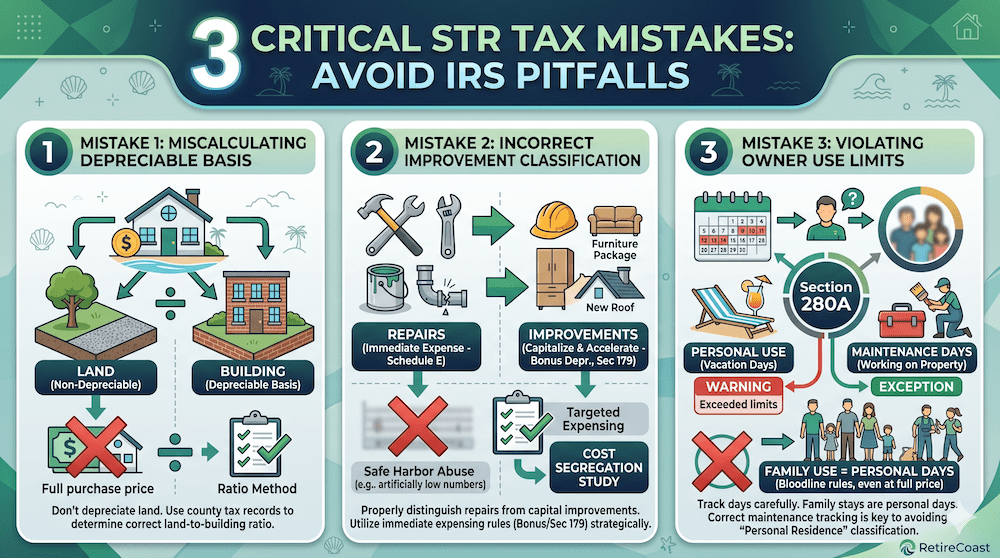

Trap #1: The Depreciation Blunder (Miscalculating Property Value)

For real estate investors, depreciation is the ultimate tax shield. The Internal Revenue Service allows you to deduct the “wear and tear” of your rental properties from your taxable income over 27.5 years. It is a massive “phantom expense”—meaning you get to claim tax deductions without actually spending any cash that year, significantly lowering your overall tax liability on your tax return.

However, there is one unbreakable tax rule: Land does not wear out, so you cannot depreciate land. You can only depreciate the physical building sitting on top of it.

The single most common mistake new short-term rental owners make is using their full purchase price, or the total assessed value listed on their property taxes, as their depreciable number. Doing so is an instant red flag for an auditor.

The Negative Outcome: The “Fully Deductible” Illusion

Sally and Bob bought a $500,000 property on the Gulf Coast to serve as a combination vacation home and short-term rental. They were excited about being able to deduct expenses against their rental income. When filing their Schedule E, their tax preparers simply used the $500,000 purchase price as their depreciable basis.

Three years later, an IRS audit flagged their rental activity. The auditor immediately noted that they had illegally depreciated the land. Because they hadn’t separated the land value, their deductions were disqualified. They were forced to pay back thousands in back taxes, plus accrued interest, for overstating their deductible expenses.

The Positive Outcome: The Ratio Method

Marcus purchased a similar $500,000 coastal property. Before claiming his deductions, he pulled the county tax assessor’s card online. The county assessed his total property at $300,000, broken down as $60,000 for “Land” and $240,000 for “Improvements” (the building).

Marcus realized the building made up exactly 80% of the total assessed value. He applied that 80% ratio to his actual $500,000 purchase price, giving him a legal, IRS-defensible depreciable basis of $400,000. When his tax return was reviewed, it passed without a single issue.

Find Your IRS-Defensible Number. Never guess your building ratio. Grab your county tax assessment card and your closing documents, and use the RetireCoast tool below to find the exact monthly depreciation deduction you are legally allowed to claim.

Monthly Depreciation Calculator

Enter the values from your county tax assessment and your actual purchase price to find your monthly deduction.

Many short-term rental owners hire contractors for repairs, cleaning, and renovations — and fully expect to deduct those expenses. But the IRS requires proper reporting before those deductions are secure.

Under current rules, if you pay a contractor $600 or more in a year, you are generally required to issue Form 1099-NEC.

Proposed regulations indicate this threshold may increase to $2,000 beginning in 2026, adjusted for inflation. However, these rules are not yet final. Until officially implemented, you should assume the $600 requirement applies.

You must obtain a completed Form W-9 before paying the contractor. Without their Taxpayer Identification Number (TIN), you cannot properly issue a 1099.

- No 1099 when required → deduction may be disallowed

- Missing or incorrect TIN → IRS CP2100A notice

- Failure to correct → potential 24% backup withholding liability

No W-9, no payment. Make this a strict policy for every contractor you hire.

Trap #2: The Renovation Write-Off Trap (Mishandling Tax Laws)

For many real estate investors, the ultimate strategy for lowering taxable income lies in the so-called short-term rental tax loophole—the ability to massively accelerate your tax deductions for furnishings and property improvements.

Under the current tax code, the Internal Revenue Service allows short-term rental owners to bypass the standard 27.5-year depreciation schedule for certain items. By utilizing bonus depreciation, Section 179 expensing, or the $2,500 De Minimis Safe Harbor, you can immediately write off the cost of appliances, furniture, and business expenses in the exact same year you buy them.

However, aggressively trying to claim expenses upfront is a massive red flag that draws immediate IRS attention. If you do not maintain detailed records or if you misunderstand the passive activity loss rules, your brilliant tax strategy will turn into an audit risk.

The Negative Outcome: The Safe Harbor Abuse

David bought a dated condo and spent $40,000 gutting it to launch his rental business. Eager to wipe out his tax liability, he tried to use the $2,500 Safe Harbor rule to immediately expense the entire project, asking his contractor to break the $40,000 into sixteen separate $2,500 invoices for things like “drywall” and “plumbing.”

An IRS audit quickly caught the discrepancy. The auditor disallowed the deductible expenses, ruling that these were capitalized structural improvements, not everyday maintenance costs. Furthermore, David hadn’t realized that even if it had worked, his resulting massive paper loss would have been trapped anyway; his high W-2 income level meant his rental losses were classified as passive losses, which cannot offset active income unless you qualify as a real estate professional. The math errors and lack of proper documentation cost him thousands in penalties.

The Positive Outcome: The Targeted Write-Off

Elena spent the same $40,000 renovating her short-term rental, but she categorized her rental expensesstrategically alongside her tax preparers. She spent $15,000 on new appliances, a living room set, and smart TVs, which she successfully wrote off in Year 1 using bonus depreciation.

The remaining $25,000 was spent on a new roof and HVAC system, which she properly capitalized over 27.5 years. By keeping clean bank statements and splitting the costs correctly, she secured a massive, legal upfront deduction on her tax return while setting up a steady stream of tax savings for the next two decades—completely avoiding any unwanted attention from the IRS.

The “Wait and Save” Strategy. Just because you can take a massive deduction today doesn’t mean you should. If you expect your business or personal income to grow, saving your depreciation for previous years (or rather, future years in a higher tax bracket) can actually save you more cash overall.

Use the decision-maker tool below to see how your shifting tax brackets impact your bottom line.

Property Improvement Depreciation

Calculate your monthly and annual deduction for property upgrades, renovations, and new furnishings.

Trap #3: The “Family Discount” Trap (Violating Owner Use Rules Under Section 280A)

The final, and often most heartbreaking, trap door for rental property owners revolves around personal use. The IRS heavily scrutinizes how much an owner actually uses their own vacation property for personal purposes under Section 280A of the Internal Revenue Code.

If you get this wrong, the IRS completely reclassifies your property. You lose your rental business status, and all those massive depreciation tax deductions we just mapped out get severely restricted to the amount of rental income you brought in (meaning you can no longer claim a loss to offset your other income).

To maintain your business status, your personal use of the property during the tax year cannot exceed the greater of:

- 14 days, OR

- 10% of the total days the property was rented to others at a fair market price.

The “Separate Household” Myth: A common mistake among short-term rental hosts is assuming that because their brother or mother is an independent adult living in a different state, they can be treated as a standard paying guest. The IRS does not care where your family lives.

Under tax laws, “family” is defined strictly by bloodline (ancestors, descendants, and siblings) and marriage. This strict definition applies completely independently of household residency and includes:

- Ancestors: Mothers, fathers, grandmothers, and grandfathers.

- Lineal Descendants: Sons, daughters, and grandchildren.

- Siblings: Brothers, sisters, half-brothers, and half-sisters.

- Spouses.

If your sister travels from across the country to rent your beach house for a week and pays the full market rate, the IRS still counts every single one of those days against your 14-day limit. Because she falls into a defined bloodline category, the government views the stay as a personal family asset, not an arm’s-length business transaction. (Note: Extended relatives like cousins, nieces, and nephews are not included in this strict definition, provided they pay full fair market rent.

The Negative Outcome: The Generous Parent

Jim and Karen rented their beach house for exactly 100 days last year, meaning their IRS personal use limit was 14 days. They stayed at the property for 10 days for their own vacation. Later that summer, they offered the house to their adult daughter for a 7-day trip. To “keep things strictly business,” they charged their daughter the full nightly rate.

During a real estate tax audit, the IRS combined Jim and Karen’s 10 days with their daughter’s 7 days, hitting 17 total personal days. The property was reclassified as a personal residence, and their ability to claim a loss on their Schedule E was completely wiped out.

The Positive Outcome: The Maintenance Exemption

John and Linda rented their rental properties for 150 days, giving them a personal use limit of 15 days. They spent 12 days on vacation at the property. In November, John drove down and spent 5 days replacing torn shingles and painting the deck.

His total days on-site were 17. However, John kept his hardware store receipts and logged those 5 days specifically as “Maintenance Days.” Because days spent actively working on or repairing the property do not count as personal use, his official tally remained at 12. He safely retained his tax status and successfully claimed his full write-offs.

(For a deeper dive into these regulations, you can review the official IRS guidelines in Topic No. 415: Renting Residential and Vacation Property or IRS Publication 527).

Calculate Your Tax Status. Don’t accidentally cross the line into “Personal Residence” territory. Input your projected rental activities below to ensure your vacation time complies with Section 280A of the tax code.

Depreciation Strategy Decision Maker

Should you take the immediate write-off or spread it out? Compare the actual cash saved based on your shifting tax brackets.

*Tip: Set Years 2-5 higher if you expect your business or W2 income to grow.

“There are no such things as tax ‘loop holes.’ Either an action is in compliance with the law, or it is not. Sometimes actions seem strange and ‘should be illegal,’ but they are not. Ignorance of the law is no excuse in court. That includes non-reporting of rental income.”

The Bottom Line: Tracking is Everything

Understanding these tax rules is only half the battle. Surviving an audit comes down to accurate records. If you are mixing your personal expenses with your business credit cards, or categorizing your STR income straight into a personal bank account, you are inviting an IRS notice. Avoid short-term rental tax mistakes.

To bulletproof your tax filings and seamlessly track your depreciation, you need a dedicated financial system. Before tax time arrives, read our companion article: How to Account for Short-Term Rental Income and Expenses: A Complete Guide for Property Owners to learn exactly how to set up your books.

Join the RetireCoast Business Membership

RetireCoast has created a Business Membership Platform designed specifically for small business creation and management. Not only do we have premium tools such as the Short Term Rental Accounting Tool, but we have tools to help you create an LLC, draft a bulletproof business plan, and much more.

Click below to visit our Business Membership page and unlock your premium toolkit.

Explore Business MembershipPODCAST

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}