You are now completing EST 103 – Understanding Probate and How to Avoid It, the third lesson in the Foundation Courses. This roadmap shows where the lesson fits within the larger RetireCoast Estate Planning Academy and what comes next.

Probate is one of the most misunderstood topics in estate planning. By the end of this lesson, you'll understand how the probate process works, why some estates require court involvement, and what planning strategies may help your family avoid unnecessary delays, costs, and stress.

- What probate is and why it exists.

- Which assets commonly pass through probate.

- Which assets may transfer outside probate.

- Why a will usually does not avoid probate.

- How probate differs from state to state.

- The role of executors and personal representatives.

- Common probate costs and delays.

- How small-estate procedures work.

- When probate may still be required.

- How trusts and beneficiary designations work together.

- Planning techniques that may reduce probate.

- How better organization helps your family after your death.

- Knowledge Check questions.

- State Small Estate Probate Shortcut Finder™.

- Real-world probate case studies.

- Professional planning tips and callouts.

- Illustrated infographics.

- Final lesson knowledge assessment.

By the time you complete EST 103, you should understand not only how probate works, but more importantly, how thoughtful estate planning can often simplify or reduce probate for your loved ones. The objective is not simply to avoid court—it is to leave behind a well-organized estate that can be administered efficiently, accurately, and according to your wishes.

Estate planning includes many legal and financial terms that may be unfamiliar. Visit the RetireCoast Estate Planning Glossary for clear, plain-English definitions that support every lesson in the Estate Planning Academy.

- Understanding Probate and How to Avoid It

- What You Will Learn in This Lesson

- What Is Probate?

- Probate Assets vs. Non-Probate Assets

- 💡 Want to Help Your Family Bypass Probate?

- The Probate Process: Step by Step

- Step 1: The Will Is Located and Reviewed

- Step 2: A Petition Is Filed With the Probate Court

- Step 3: The Court Appoints the Personal Representative

- Step 4: Heirs, Beneficiaries, and Creditors Are Notified

- Step 5: Estate Assets Are Identified and Secured

- Step 6: An Inventory and Valuation Are Prepared

- Step 7: Valid Debts and Expenses Are Paid

- Step 8: Tax Returns Are Prepared

- Step 9: Property May Be Sold or Transferred

- Step 10: The Remaining Estate Is Distributed

- Step 11: A Final Accounting Is Prepared

- Step 12: The Estate Is Closed

- How Long Does Probate Take?

- Probate Is a Process, Not a Single Event

- Looking Ahead

- Case Study: Richard Learns That an Executor’s Job Comes With Serious Responsibilities

- The Costs, Delays, and Family Burdens of Probate

- Probate Court Costs

- Attorney Fees

- Executor or Personal Representative Compensation

- Accounting and Tax Preparation Costs

- Appraisal and Valuation Expenses

- Property Maintenance During Probate

- Probate Can Delay Access to Money

- Creditor Waiting Periods

- Real Estate Can Slow the Process

- Family Conflict Can Increase Every Cost

- The Emotional Cost Is Often Overlooked

- Privacy May Be Reduced

- Probate Costs Can Reduce the Inheritance

- A Small Estate Can Still Be Complicated

- Good Planning Can Reduce the Burden

- Key Takeaway

- Looking Ahead

- Estate Planning Tools That May Help Reduce or Avoid Probate

- Why Revocable Living Trusts Have Become the Cornerstone of Modern Estate Planning

- When Probate May Still Be Necessary

- Property Left Outside a Trust

- No Beneficiary Was Named

- The Beneficiary Is a Minor

- Real Estate Was Owned Individually

- Property Is Located in Another State

- Ownership Is Unclear

- The Will Is Contested

- Beneficiaries Disagree

- Creditors Must Be Addressed

- The Estate Is Insolvent

- A Business Interest Requires Court Authority

- Taxes or Litigation Remain Unresolved

- Probate Can Provide Useful Protection

- Avoiding Probate Does Not Eliminate Administration

- Key Takeaway

- Looking Ahead

- Small Estate Procedures: When Probate May Be Simpler

- Use Our Free State Probate Finder

- Your Probate Prevention Action Plan

- Step 1: Take Inventory of Your Assets

- Step 2: Review How Each Asset Is Owned

- Step 3: Review Every Beneficiary

- Step 4: Consider Whether a Revocable Living Trust Is Appropriate

- Step 5: Organize Your Records

- Step 6: Talk With Your Family

- Step 7: Review Your Plan Regularly

- Don’t Wait for “Someday”

- Author’s Insight

- Key Takeaway

- Looking Ahead

- References

Understanding Probate and How to Avoid It

Probate is one of the most misunderstood parts of estate planning.

Many people assume that having a will means their family will avoid probate. In most cases, the opposite is true. A will usually tells the probate court how property should be distributed, but it does not automatically keep the estate out of court.

Probate is the legal process used to identify a deceased person’s assets, pay valid debts, resolve disputes, and transfer remaining property to heirs or beneficiaries. Depending on the state, the value of the estate, the type of property involved, and how the assets are titled, probate may be simple—or it may become costly, slow, and frustrating.

In this lesson, you will learn how probate works, which assets are most likely to go through probate, and which planning methods may help avoid or reduce it.

Beneficiary designations are important

You will also learn why beneficiary designations, joint ownership, transfer-on-death arrangements, and revocable living trusts can be so important. These tools do not all work the same way, and they are not appropriate in every situation, but understanding them can help you make better planning decisions.

Probate laws are different in every state. A procedure that works in Mississippi may not work the same way in California, Texas, Florida, or another state. Small-estate limits, waiting periods, real estate rules, court procedures, and available probate shortcuts can vary significantly.

For that reason, this lesson includes an interactive state probate tool. You will be able to select a state and review important information such as the small-estate limit, whether real estate may be included, common waiting periods, and key restrictions.

The goal is not to turn you into a probate attorney.

The goal is to help you recognize where probate risk may exist in your own estate and understand the steps that may make the transfer of property easier for your family.

You cannot fail this course. The quizzes and knowledge checks are included to help you confirm what you understand and identify areas you may want to review.

By the end of EST 103, you should have a clearer understanding of probate, how it affects families, and how thoughtful estate planning may reduce unnecessary court involvement.

What You Will Learn in This Lesson

By the end of EST 103, you should be able to:

- Explain what probate is and why the legal process exists.

- Identify which assets commonly pass through probate and which may transfer directly to beneficiaries.

- Understand the differences between probate and non-probate assets.

- Recognize the advantages and disadvantages of the probate process.

- Explain why simply having a will does not necessarily avoid probate.

- Understand how beneficiary designations, joint ownership, payable-on-death (POD) accounts, transfer-on-death (TOD) registrations, and revocable living trusts may reduce or avoid probate in many situations.

- Learn why probate laws differ from one state to another and why those differences matter when creating an estate plan.

- Use the interactive Small Estate Probate Shortcut Finder to explore probate rules in your state.

- Understand when a small estate affidavit or simplified probate procedure may be available.

- Recognize situations in which professional legal advice may be appropriate.

- Begin evaluating whether your current estate plan is likely to require probate and identify opportunities to simplify the transfer of your assets.

Interactive Learning Tools Included

Throughout this lesson, you’ll have access to several interactive resources designed to help you apply what you’re learning:

- Knowledge Check Survey – Assess your understanding before you begin.

- Small Estate Probate Shortcut Finder™ – Explore simplified probate rules for your state.

- Probate Risk Checklist – Identify assets that may still require probate.

- End-of-Lesson Knowledge Check – Reinforce the concepts covered in this lesson.

Remember, these quizzes are not graded. Their purpose is to help you measure your understanding and reinforce important concepts before moving on to the next lesson.

Why This Lesson Matters

Many families discover probate only after the death of a loved one. At that point, changing the outcome is often impossible. Delays, court costs, attorney fees, and administrative burdens can create additional stress during an already difficult time.

By understanding probate before it becomes an issue, you can make informed decisions that may save your family significant time, expense, and frustration while helping ensure your wishes are carried out as intended.

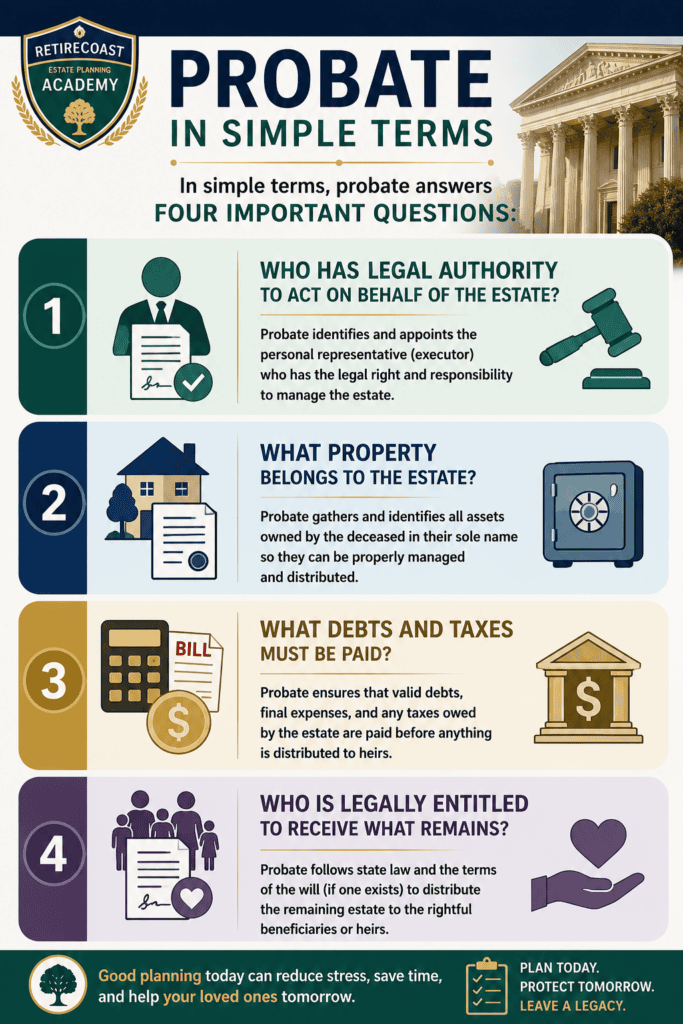

What Is Probate?

Probate is the legal process used to settle a person’s estate after death. It provides a court-supervised method for identifying assets, paying valid debts and taxes, resolving disputes when necessary, and distributing the remaining property to the rightful heirs or beneficiaries.

While the word probate often has a negative reputation, the process itself serves an important purpose. Without a legal system to verify ownership and authority, banks, investment firms, title companies, and other institutions would have no reliable way to know who has the legal right to receive a deceased person’s property.

In simple terms, probate answers four important questions:

- Who has legal authority to act on behalf of the estate?

- What property belongs to the estate?

- What debts and taxes must be paid?

- Who is legally entitled to receive what remains?

Once those questions have been answered, the estate can be closed, and the remaining assets distributed according to the deceased person’s will—or, if there is no will, according to state law.

Probate Is Not Always Required

One of the biggest misconceptions about estate planning is that every estate must go through probate.

That simply isn’t true.

Many assets transfer automatically upon death without ever becoming part of the probate estate. For example:

- Life insurance proceeds with a named beneficiary

- Retirement accounts with designated beneficiaries

- Payable-on-Death (POD) bank accounts

- Transfer-on-Death (TOD) investment accounts where permitted

- Property held in a revocable living trust

- Certain jointly owned property with rights of survivorship

These are commonly called non-probate assets because ownership transfers by contract or by operation of law rather than through the probate court.

Understanding the difference between probate and non-probate property is one of the most valuable concepts in estate planning. Simply changing how an asset is titled or adding a beneficiary designation can sometimes eliminate the need for probate for that asset.

A Will Does Not Avoid Probate

Another common misunderstanding is that creating a will allows your family to avoid probate.

In reality, a will generally works through the probate process, not around it.

A will tells the court who should receive your property and who you want to serve as the executor of your estate. Before those instructions can usually be carried out, the court must determine that the will is valid and authorize the executor to act.

This surprises many families. They spend time creating a will believing it will keep their loved ones out of court, only to discover that probate is often the very process that gives the will its legal effect.

Later in this lesson, you’ll learn why many people choose to combine a will with other estate planning tools—such as beneficiary designations and revocable living trusts—to reduce the amount of property that must pass through probate.

Probate Looks Different in Every State

Probate is governed primarily by state law, not federal law.

That means the probate process can vary considerably depending on where you live. One state may offer a simple affidavit procedure for small estates, while another may require a formal court proceeding. The dollar limits for simplified probate, waiting periods, treatment of real estate, required court filings, and filing fees all differ from state to state.

To help you understand these differences, this lesson includes the Small Estate Probate Shortcut Finder™. Select your state to see its current small-estate threshold, whether real estate may qualify, common waiting periods, and important restrictions. It’s an excellent starting point for understanding how probate may apply where you live.

Looking Ahead

Now that you understand what probate is and why it exists, the next question is equally important:

What property actually goes through probate—and what property does not?

That distinction forms the foundation of every effective estate plan and is the focus of the next section.

For EST 103, I would place the first quiz after the “What Is Probate?” section and before “Probate Assets vs. Non-Probate Assets.”

That placement works well because readers have already learned:

- What probate is

- Why it exists

- The four questions probate answers

- That not every estate goes through probate

- That a will usually does not avoid probate

- That probate laws differ by state

They have enough knowledge to answer the questions confidently, but they haven’t yet moved into the more detailed material about probate assets, costs, trusts, and avoidance strategies.

The lesson flow would look like this:

- Hero Image

- Audio Introduction

- Course Roadmap

- What You’ll Learn

- Introduction

- What Is Probate?

- Infographic – The Four Questions Probate Answers

- 🎯 Progress Check #1 (10 Questions) ← Place it here

- Probate Assets vs. Non-Probate Assets

- Probate Process (12 Steps)

- Case Study – Richard

- Costs, Delays & Family Burdens

- Probate Avoidance Tools

- Revocable Living Trust

- When Probate May Still Be Necessary

- Small Estate Procedures

- Small Estate Probate Shortcut Finder™

- Probate Prevention Action Plan

- Lesson Summary

- Key Takeaways

- Final Knowledge Check (more advanced)

- FAQ

- Membership CTA

- Survey

- References

I also recommend adding a short introduction immediately above the quiz, such as:

Progress Check #1

Before moving into the details of probate assets and avoidance strategies, take a few minutes to see how well you’ve grasped the basic concepts. This quiz isn’t graded—it’s simply an opportunity to reinforce what you’ve learned so far.

Probate Assets vs. Non-Probate Assets

One of the most valuable lessons you can learn about estate planning is that not everything you own will go through probate.

Whether an asset becomes part of your probate estate usually depends on how it is owned and whether you have named a beneficiary, not simply on the type of asset itself.

For example, two neighbors may each own a $500,000 home. One home may pass directly to a surviving spouse without probate because of the way it is titled, while the other may require months of probate because it is owned solely by the deceased owner.

The same is true for bank accounts, investment accounts, vehicles, and other property.

What Is a Probate Asset?

A probate asset is generally any asset that was owned solely by the deceased person and does not have a legal mechanism for transferring ownership automatically upon death.

These assets often require the probate court to determine who has authority to transfer ownership.

Common examples include:

- A home titled solely in one person’s name.

- A checking or savings account with no payable-on-death beneficiary.

- An investment account without a transfer-on-death designation.

- Vehicles titled only in the deceased owner’s name.

- Personal property such as jewelry, furniture, artwork, collectibles, and firearms.

- Business interests that have no succession provisions.

- Mineral rights, royalties, or other individually owned property.

These assets generally become part of the probate estate unless another legal arrangement applies.

What Is a Non-Probate Asset?

A non-probate asset transfers automatically because ownership is determined by contract or by law rather than by a probate judge.

Common examples include:

- Life insurance policies with living beneficiaries.

- IRAs and 401(k) retirement accounts with current beneficiary designations.

- Payable-on-Death (POD) bank accounts.

- Transfer-on-Death (TOD) brokerage accounts where permitted by state law.

- Property owned by a revocable living trust.

- Jointly owned property with rights of survivorship, where recognized.

- Certain annuities with named beneficiaries.

Because these assets transfer automatically, they generally do not become part of the probate estate.

Ownership Matters More Than the Asset

Many people assume that certain assets always avoid probate.

That isn’t true.

Consider these examples:

Example 1 – Bank Account

Sarah owns a checking account in her name only. She never completed a Payable-on-Death designation.

Result:

The account will likely become part of her probate estate.

Now imagine Sarah completed a POD designation naming her daughter.

Result:

Upon Sarah’s death, the bank may transfer the funds directly to her daughter after receiving the required documentation, without probate for that account.

The asset didn’t change.

Only the ownership arrangement changed.

Example 2 – Family Home

John owns his home in his individual name.

Result:

The home may require probate before ownership can be transferred.

If John instead transferred the home into his revocable living trust during his lifetime, the successor trustee could generally transfer or manage the property according to the trust agreement without the home becoming part of the probate estate.

Again, the home is the same.

Only the legal ownership changed.

Not Every Non-Probate Asset Is the Right Choice

Avoiding probate is only one goal of estate planning.

Sometimes adding a joint owner simply to avoid probate creates unintended consequences. It may expose the property to another person’s creditors, create gift tax issues in some situations, or unintentionally disinherit other family members.

Likewise, beneficiary designations should be reviewed regularly. A forgotten beneficiary designation can override the instructions in your will or trust, resulting in assets passing to someone you no longer intended to inherit them.

The goal is not merely to avoid probate.

The goal is to create an estate plan that accurately reflects your wishes while making the administration of your estate as efficient as possible.

Author’s Note

Over the years, I have spoken with many families who believed they had completed their estate planning because they had signed a will. What they often overlooked were beneficiary designations, outdated account registrations, or assets that had never been transferred into their trust.

Those small details can determine whether an asset transfers in a matter of days—or whether your family spends months working through the probate process.

That is why reviewing how your assets are titled is just as important as creating the legal documents themselves.

Looking Ahead

Now that you understand which assets may pass through probate and which may avoid it, let’s examine the probate process itself—from filing the initial petition through the final distribution of assets to heirs and beneficiaries.

💡 Want to Help Your Family Bypass Probate?

One of the primary goals of estate planning is to make the transfer of your assets as simple and efficient as possible for the people you love.

Continue through this course and you’ll learn how tools such as revocable living trusts, beneficiary designations, payable-on-death (POD) accounts, transfer-on-death (TOD) registrations, proper asset titling, and other estate planning strategies may help reduce—or in many cases avoid—the time, expense, and stress of probate.

You’ll also discover how the RetireCoast Estate Planning Membership provides interactive planning tools, document builders, checklists, and step-by-step guidance to help you create an organized estate plan and keep it up to date as your life changes.

A little planning today can make a tremendous difference for your family tomorrow.

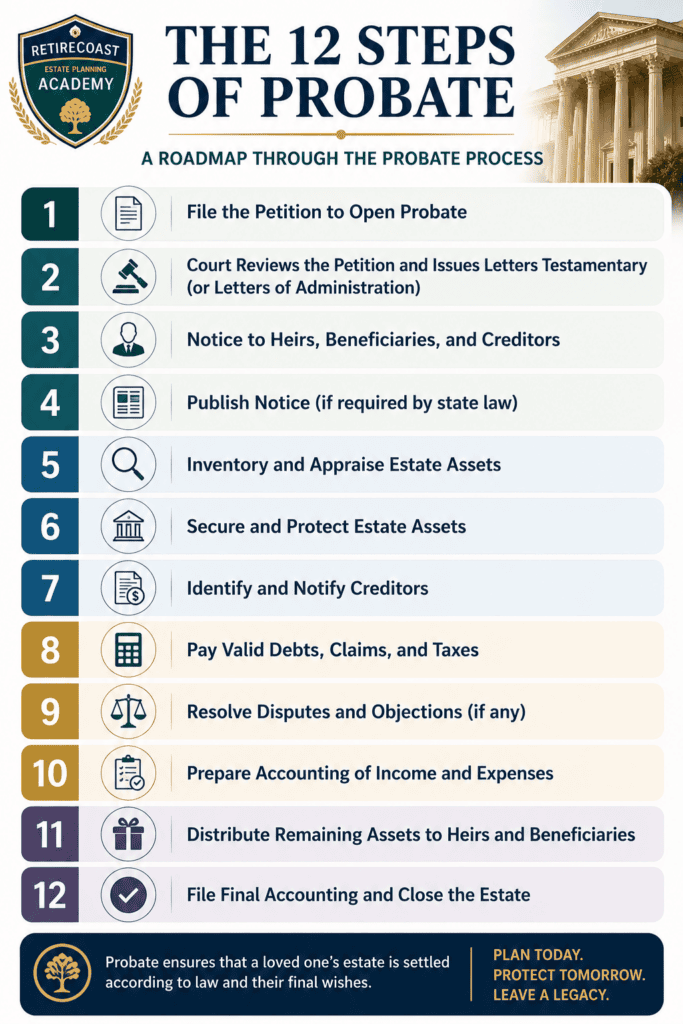

The Probate Process: Step by Step

Probate can seem intimidating because most people do not encounter it until someone close to them dies. At that point, the family may already be dealing with grief, funeral arrangements, bills, property concerns, and uncertainty about what happens next.

Understanding the basic process before it is needed can make probate feel less mysterious.

The exact steps vary by state and by the complexity of the estate, but most probate proceedings follow a similar sequence.

Step 1: The Will Is Located and Reviewed

The first task is to determine whether the deceased person left a valid will.

The original signed will may be stored:

- At home

- In a fire-resistant document box

- With an attorney

- In a safe deposit box

- With the nominated executor

- In an estate planning binder

A copy may help the family understand the deceased person’s wishes, but courts often require the original document before formally admitting it to probate.

If no valid will can be found, the estate may be treated as an intestate estate. This means state law, rather than the deceased person’s written instructions, determines who receives the probate property.

Step 2: A Petition Is Filed With the Probate Court

The person named as executor in the will generally files a petition asking the probate court to open the estate.

If there is no will, an interested person may ask the court to appoint an administrator.

The terms executor, personal representative, and administrator are sometimes used differently from one state to another. In general, each refers to the person legally authorized to manage the estate.

The court may require:

- The original will

- A certified death certificate

- A petition or application

- Information about heirs and beneficiaries

- An estimate of the estate’s value

- A filing fee

- Notices to interested parties

Step 3: The Court Appoints the Personal Representative

Being named as executor in a will does not automatically give someone authority to act.

The court usually must first approve the appointment.

Once appointed, the personal representative may receive legal documents often called:

- Letters Testamentary

- Letters of Administration

- Letters of Authority

- Letters of Appointment

The title varies by state, but the purpose is similar. These documents prove to banks, title companies, investment firms, and other institutions that the person has legal authority to act for the estate.

Without this authority, an executor may be unable to close accounts, sell property, access funds, or sign documents on behalf of the estate.

Step 4: Heirs, Beneficiaries, and Creditors Are Notified

The personal representative may be required to notify the people who have a legal interest in the estate.

This may include:

- Heirs

- Beneficiaries

- Known creditors

- Government agencies

- Interested family members

Some states also require notice to be published in a local newspaper or approved public notice source.

This gives creditors an opportunity to submit claims against the estate within a specified period.

The creditor claim period can significantly affect how quickly an estate may be closed.

Step 5: Estate Assets Are Identified and Secured

The personal representative must locate and protect the deceased person’s property.

This may include:

- Bank accounts

- Investment accounts

- Real estate

- Vehicles

- Business interests

- Personal property

- Insurance refunds

- Tax refunds

- Royalties

- Mineral interests

- Money owed to the deceased person

Property may need to be secured, insured, maintained, appraised, or stored.

For example, the personal representative may need to continue paying:

- Mortgage payments

- Property taxes

- Homeowners insurance

- Utilities

- Maintenance costs

- Vehicle insurance

- Business expenses

These expenses do not stop simply because the owner has died.

Step 6: An Inventory and Valuation Are Prepared

The court may require the personal representative to prepare an inventory of probate assets and their values.

The valuation date is often the date of death, although the exact requirements depend on state law.

Some assets are relatively easy to value. A bank statement may show the exact account balance on the date of death.

Other property may require professional help.

Examples include:

- Real estate

- Closely held businesses

- Jewelry

- Artwork

- Collectibles

- Farm equipment

- Mineral rights

- Valuable vehicles

Accurate values may also be important for estate tax, capital gains tax, insurance, and distribution purposes.

Step 7: Valid Debts and Expenses Are Paid

Before beneficiaries receive property, the estate generally must pay valid debts and administrative expenses.

These may include:

- Funeral expenses

- Medical bills

- Credit card balances

- Personal loans

- Mortgages

- Taxes

- Court costs

- Attorney fees

- Accounting fees

- Appraisal fees

- Property maintenance

- Executor or personal representative compensation

The order in which claims must be paid is often controlled by state law.

This matters when an estate does not have enough money to pay every debt.

The personal representative should not simply pay bills in the order they arrive without understanding the applicable priority rules.

Step 8: Tax Returns Are Prepared

The personal representative may need to arrange for several types of tax filings.

These can include:

- The deceased person’s final income tax return

- An estate income tax return

- State tax returns

- Federal estate tax returns for larger estates

- Gift tax returns that were previously required but not filed

- Property tax filings

- Business tax returns

Most estates do not owe federal estate tax, but that does not mean no tax work is required.

Even a modest estate may earn income after death from rent, investments, interest, or business operations.

Step 9: Property May Be Sold or Transferred

Some estate assets may need to be sold.

This can happen when:

- Cash is needed to pay debts

- The will directs a sale

- Beneficiaries cannot agree on ownership

- Property cannot easily be divided

- A business must be liquidated

- The estate lacks enough available cash

Real estate sales during probate may require court approval in some states or under some types of administration.

Other property may be transferred directly to a beneficiary after the necessary court and title requirements have been completed.

Step 10: The Remaining Estate Is Distributed

After valid debts, taxes, and expenses have been paid, the personal representative can distribute the remaining property.

If there is a valid will, distributions generally follow the instructions in that document.

If there is no will, distributions follow the state’s intestacy laws.

The personal representative should document every transfer carefully.

Beneficiaries may be asked to sign receipts confirming that they received their distributions.

Step 11: A Final Accounting Is Prepared

The court may require a final accounting showing:

- Assets received

- Income earned

- Bills paid

- Property sold

- Expenses incurred

- Distributions made

- Remaining funds

Beneficiaries may have the right to review or object to the accounting.

A well-organized estate is usually easier to account for than one with missing statements, unclear ownership, or incomplete records.

Step 12: The Estate Is Closed

Once the court is satisfied that the estate has been properly administered, the personal representative may be discharged and the probate case closed.

Closing the estate releases the personal representative from further duties, subject to any later-discovered property or unresolved legal issues.

How Long Does Probate Take?

There is no single answer.

A straightforward estate may be completed in several months. A more complicated estate may remain open for a year or longer.

Delays may be caused by:

- Required creditor waiting periods

- Missing beneficiaries

- Disputes over the will

- Real estate sales

- Tax problems

- Business ownership

- Property in multiple states

- Poor recordkeeping

- Unclear beneficiary designations

- Family disagreements

- Litigation

The size of the estate does not always determine how difficult probate will be.

A relatively small estate with poor records or family conflict may be harder to administer than a larger estate with clear documents and organized assets.

Probate Is a Process, Not a Single Event

Probate is not one hearing or one form.

It is a series of legal and administrative tasks that may continue for months.

This is why estate planning is about more than deciding who receives your property. Good planning also considers how easily someone will be able to identify, manage, and transfer that property after your death.

Looking Ahead

Now that you understand the steps involved in probate, the next section examines the most common costs, delays, and family burdens associated with the process.

These are the reasons many people decide to organize their assets and use probate-avoidance tools before a crisis occurs.

Case Study: Richard Learns That an Executor’s Job Comes With Serious Responsibilities

Richard was named as the executor of his father’s estate.

Like many people serving as an executor for the first time, Richard believed his primary responsibility was to distribute his father’s money and property to the family. Shortly after his father’s death, he gained access to his father’s checking account, which contained a substantial balance.

Believing that he would eventually inherit much of the estate anyway, Richard began using money from the account to pay several of his own personal bills. He intended to “settle up later” once everything was finished.

A few weeks later, the letters began arriving.

Credit card companies demanded payment. The bank notified him of an outstanding loan. Medical providers submitted unpaid bills. There were also final utility bills, property taxes, and funeral expenses.

Richard was shocked.

He assumed that when someone dies, their debts simply disappear.

They do not.

While most debts are not automatically transferred to family members, they generally remain obligations of the deceased person’s estate. Before heirs receive an inheritance, the estate must usually pay valid debts, taxes, and administrative expenses according to state law.

Because Richard had already spent estate funds for his own personal benefit, he created a serious problem. As executor, he had a fiduciary duty to protect the estate and administer it for the benefit of all interested parties—not for himself.

If estate funds are improperly distributed or misused before creditors and other legal obligations are satisfied, an executor may be required to restore those funds to the estate from personal assets. In some situations, additional legal consequences may also result.

Richard eventually had to work with the probate court and legal counsel to correct the mistakes and repay the estate.

Lesson Learned

Being named as an executor is an honor, but it is also a legal responsibility.

An executor should never assume estate assets belong to the heirs immediately after death. Those assets generally belong to the estate until the probate process has been completed, valid debts and expenses have been paid, and the remaining property has been lawfully distributed.

One of the most important duties of an executor is to keep estate funds completely separate from personal finances. Good records, patience, and following the probate process help protect both the beneficiaries and the executor.

These questions address common concerns families have about managing a modest estate and deciding whether professional assistance may be needed.

The Costs, Delays, and Family Burdens of Probate

Probate is not always disastrous.

In some cases, it is orderly, predictable, and completed without major conflict. However, probate can still require time, money, recordkeeping, court filings, and attention from family members who may already be dealing with grief.

The real burden of probate often comes from the combination of several smaller problems rather than one dramatic event.

A filing fee by itself may not be significant.

A short delay may not be serious.

A few hours spent locating records may not seem overwhelming.

But when court costs, attorney fees, creditor notices, property maintenance, tax filings, real estate issues, and family disagreements occur together, the process can become expensive and exhausting.

Probate Court Costs

Opening a probate estate usually requires court filings.

Depending on the state and county, expenses may include:

- Initial filing fees

- Certified copies of court documents

- Publication or legal notice costs

- Bond premiums

- Recording fees

- Appraisal fees

- Court accounting fees

- Additional petition fees

These costs are generally paid from estate assets.

The amount varies significantly by location and by the complexity of the proceeding.

A small estate may qualify for a simplified procedure with lower costs, while a formal probate administration may involve several filings and hearings.

Attorney Fees

Some families complete simple probate matters without retaining an attorney for the entire process.

Others hire legal counsel because the estate includes real estate, significant debts, family conflict, unclear documents, tax issues, or complicated ownership arrangements.

Attorney fees may be billed:

- By the hour

- As a flat fee

- According to a statutory schedule

- As a percentage or formula based on estate value

- Through a combination of these methods

The fee arrangement depends on state law and the attorney’s practice.

In some jurisdictions, attorney compensation must be approved by the court.

The need for an attorney does not necessarily mean that something has gone wrong. Probate can involve legal procedures, filing deadlines, creditor priorities, title transfers, and fiduciary responsibilities that are unfamiliar to most families.

Executor or Personal Representative Compensation

The executor or personal representative may be entitled to compensation for administering the estate.

State law, the will, or the court may determine how much compensation is allowed.

The executor’s work can include:

- Collecting records

- Communicating with beneficiaries

- Securing property

- Paying bills

- Managing accounts

- Preparing inventories

- Coordinating appraisals

- Selling assets

- Working with attorneys and accountants

- Filing tax documents

- Preparing the final accounting

Some family members choose not to accept compensation.

Others accept it because administering the estate requires substantial time and responsibility.

Executor compensation may also have income tax consequences for the person receiving it.

Accounting and Tax Preparation Costs

An estate may require professional accounting or tax assistance.

Even when no federal estate tax is owed, the estate may still need:

- The deceased person’s final income tax return

- State income tax returns

- An estate income tax return

- Business tax filings

- Property tax filings

- Documentation of asset values

- Records for beneficiaries

Rental property, investment income, business ownership, and property sales can make tax administration more complicated.

The executor may also need help determining the tax basis of inherited property and documenting values as of the date of death.

Appraisal and Valuation Expenses

Some estate property is easy to value.

A bank account balance can usually be confirmed through a statement.

Other assets may require an appraisal or professional valuation.

These may include:

- Real estate

- Privately owned businesses

- Jewelry

- Artwork

- Antiques

- Collectibles

- Vehicles

- Farm equipment

- Mineral interests

- Intellectual property

Accurate valuations may be required for court reports, tax filings, asset sales, and fair distributions among beneficiaries.

Property Maintenance During Probate

Real estate can continue generating expenses while probate is underway.

The estate may need to pay:

- Mortgage payments

- Property taxes

- Homeowners insurance

- Flood or wind insurance

- Utilities

- Lawn care

- Repairs

- Security

- Homeowners association dues

- Cleaning expenses

A vacant home may be more difficult or expensive to insure.

Deferred maintenance can reduce the property’s value.

If family members disagree about whether to sell, rent, or retain the home, costs may continue while no final decision is made.

Probate Can Delay Access to Money

Beneficiaries may not receive their inheritance immediately.

The executor usually must first determine:

- What assets belong to the estate

- Which debts are valid

- Whether taxes are owed

- Whether property must be sold

- Whether disputes exist

- Whether the court must approve a distribution

In some cases, partial distributions may be permitted before the estate closes.

However, the executor must be careful not to distribute so much that insufficient funds remain to pay debts, taxes, and administration expenses.

A beneficiary may expect money quickly, but the executor has a duty to protect the estate before making distributions.

Creditor Waiting Periods

Many states require creditors to receive notice and provide a period during which claims may be submitted.

This waiting period can delay the closing of the estate even when there are no disputes.

The executor may need to:

- Identify known creditors

- Send formal notices

- Publish notice where required

- Review submitted claims

- Accept or reject claims

- Resolve disputed debts

An executor who distributes assets too early may create personal liability if valid obligations remain unpaid.

Real Estate Can Slow the Process

A house is often the largest asset in an estate.

It can also become one of the most time-consuming.

Questions may include:

- Does the property need to be sold?

- Does a beneficiary want to keep it?

- Can that beneficiary afford the mortgage and expenses?

- Do all beneficiaries agree?

- Is court approval required?

- Are repairs needed before listing?

- Is anyone living in the property?

- Are taxes or liens unpaid?

- Is the title clear?

A property may sit vacant while these issues are resolved.

If the estate owns real estate in more than one state, an additional proceeding known as ancillary probate may be required in the other state.

Family Conflict Can Increase Every Cost

Probate becomes far more difficult when family members disagree.

Conflict may arise over:

- The validity of the will

- The choice of executor

- Distribution of personal property

- The sale of a family home

- Executor compensation

- Unequal inheritances

- Loans or gifts made during life

- Caregiving contributions

- Business ownership

- Allegations of undue influence

- Missing property or financial records

A disagreement that begins with a piece of jewelry or furniture can grow into a larger dispute about fairness, trust, or family history.

Legal fees increase when attorneys must respond to objections, prepare additional petitions, or appear at contested hearings.

The Emotional Cost Is Often Overlooked

Probate expenses are not limited to dollars.

The process may require family members to make difficult decisions while grieving.

They may need to:

- Sort through a lifetime of personal belongings

- Sell a family home

- Locate missing documents

- Contact creditors

- Resolve old family disagreements

- Manage property from another state

- Explain delays to beneficiaries

- Make decisions under court deadlines

A poorly organized estate can turn an already emotional period into a prolonged administrative burden.

Privacy May Be Reduced

Probate is generally a court process.

Depending on state and local rules, some filings may become part of the public record.

Information that may appear in court documents can include:

- The will

- Names of heirs and beneficiaries

- Estate values

- Property descriptions

- Creditor claims

- Inventories

- Accountings

- Executor information

The level of public access varies.

A revocable living trust is often administered privately, although disputes and related court proceedings can still make information public.

Probate Costs Can Reduce the Inheritance

Court expenses, legal fees, accounting fees, property carrying costs, and executor compensation are generally paid from the estate.

This means those expenses reduce the amount ultimately available to beneficiaries.

For example, imagine an estate with $300,000 in probate assets.

If the estate incurs $20,000 in administration costs, debts, maintenance, and professional fees, only the remaining amount is available for distribution.

The beneficiaries effectively bear the financial cost because the expenses reduce their inheritance.

A Small Estate Can Still Be Complicated

Many people assume that a small estate will automatically be simple.

That is not always true.

A modest estate may still involve:

- A home in the deceased person’s name

- Several creditors

- Missing records

- Family disagreements

- No valid will

- Outdated beneficiaries

- Property in another state

- A business interest

- Tax problems

Complexity is often determined by ownership, organization, and family circumstances—not merely by the estate’s dollar value.

Good Planning Can Reduce the Burden

Probate cannot always be eliminated, and avoiding it should not be the only goal of estate planning.

However, thoughtful planning may reduce the amount of property that must pass through probate and make the process easier for the property that remains.

Helpful planning steps may include:

- Creating a valid will

- Considering a revocable living trust

- Funding the trust properly

- Reviewing beneficiary designations

- Adding POD or TOD designations where appropriate

- Reviewing property ownership

- Organizing financial records

- Maintaining an estate planning binder

- Keeping debt information current

- Naming capable fiduciaries

- Discussing the plan with family members

The objective is not simply to avoid court.

The objective is to leave behind a plan that someone can understand and administer.

Key Takeaway

Probate costs more than filing fees.

It may also require time, professional assistance, property management, tax work, emotional energy, and difficult family decisions.

A well-organized estate plan can help reduce these burdens and give the people you trust clearer instructions when they need them most.

Looking Ahead

The next section examines the estate planning tools that may help assets transfer outside probate.

You will learn how beneficiary designations, payable-on-death accounts, transfer-on-death registrations, joint ownership, deeds, and revocable living trusts work—and why each tool must be used carefully.

This is not our first suggestion about legally avoiding probate, and it will not be the last.

The RetireCoast Estate Planning Academy will teach you how beneficiary designations, proper account ownership, transfer-on-death options, and properly funded trusts may help your family avoid unnecessary probate delays.

Estate Planning Tools That May Help Reduce or Avoid Probate

By now, you have seen why probate can take time, create additional expenses, and place significant responsibilities on the people you leave behind.

The good news is that many of these challenges can often be reduced—or, for certain assets, avoided altogether—with thoughtful planning.

There is no single “magic document” that keeps every asset out of probate. Instead, estate planning is like building a toolbox. Each tool serves a different purpose, and the right combination depends on your family, your assets, and the laws of your state.

Let’s look at some of the most common probate-avoidance tools.

Revocable Living Trust

For many families, a revocable living trust is one of the most effective ways to reduce probate.

Unlike a will, a revocable living trust generally allows assets that have been properly transferred into the trust to be managed and distributed by your successor trustee without going through the probate court.

A trust can also provide:

- Continuity if you become incapacitated.

- Privacy, because trusts are generally not filed with the probate court.

- Easier management of multiple properties.

- Clear instructions for distributing assets over time.

- Greater flexibility for blended families or beneficiaries with special needs.

A trust is only effective for assets that are actually transferred—or funded—into the trust. Creating the document alone is not enough.

Coming Soon in the Academy: You’ll learn how to create, fund, and maintain a revocable living trust in the Core Documents section of the Estate Planning Academy.

Beneficiary Designations

Many financial assets transfer according to the beneficiary designation you complete with the financial institution—not according to your will.

Common examples include:

- Life insurance policies

- 401(k) plans

- Traditional IRAs

- Roth IRAs

- Annuities

- Pension survivor benefits

Keeping these designations current is one of the easiest and most effective estate planning tasks you can perform.

Review them whenever you experience a major life event, such as:

- Marriage

- Divorce

- Birth or adoption of a child

- Death of a beneficiary

- Retirement

- Creation of a trust

Remember, an outdated beneficiary designation may override your will.

Payable-on-Death (POD) Accounts

Many banks allow account owners to add a Payable-on-Death (POD) beneficiary.

During your lifetime, you retain complete ownership and control of the account.

After your death, the remaining funds may pass directly to the named beneficiary without becoming part of the probate estate.

This is often one of the simplest probate-avoidance tools available for checking, savings, and certificates of deposit.

Transfer-on-Death (TOD) Registrations

Many states allow investment accounts—and in some states even real estate—to transfer through a Transfer-on-Death (TOD) registration.

Rather than becoming part of the probate estate, ownership passes directly to the named beneficiary after the required documentation is provided.

Availability varies by state and by the type of asset.

Joint Ownership

Some jointly owned property transfers automatically to the surviving owner.

Examples may include:

- Joint tenancy with rights of survivorship.

- Tenancy by the entirety (where recognized).

- Certain community property arrangements with survivorship rights.

While joint ownership can simplify transfers, it should not be used solely to avoid probate without understanding the legal, financial, and tax consequences.

Adding someone as a joint owner during your lifetime may expose the property to that person’s creditors, lawsuits, or divorce proceedings.

Transfer-on-Death Deeds

Some states permit homeowners to record a Transfer-on-Death Deed, sometimes called a Beneficiary Deed.

This allows ownership of the property to transfer directly to a named beneficiary upon death while the owner retains full control during life.

Not every state recognizes these deeds, and the rules vary considerably.

Proper Asset Titling

Sometimes avoiding probate is as simple as reviewing how assets are titled.

Many people create excellent estate planning documents but never update the ownership of their assets to match those documents.

Examples include:

- A home never transferred into the trust.

- A brokerage account with no beneficiary designation.

- A bank account titled only in one person’s name.

- A newly purchased vehicle that was never incorporated into the estate plan.

One of the most overlooked aspects of estate planning is making sure ownership matches your planning documents.

Keeping Your Plan Current

Estate planning is not a one-time event.

Your plan should be reviewed whenever life changes.

Common reasons to update your plan include:

- Buying or selling a home.

- Marriage or divorce.

- Birth of children or grandchildren.

- Death of a beneficiary.

- Starting or selling a business.

- Moving to another state.

- Retirement.

- Significant changes in your financial situation.

An estate plan that was perfect ten years ago may no longer reflect your wishes or your assets today.

Author’s Insight

One of the most common problems I see is not that people fail to create an estate plan—it is that they fail to keep it current.

A family creates a trust, signs a will, and then assumes everything is finished. Years later, they have purchased another home, opened new investment accounts, changed banks, rolled over retirement plans, or changed insurance companies.

The documents are still in the binder, but the assets no longer match the plan.

That is why I created the RetireCoast Estate Planning Membership. It encourages members to review and update their estate plans regularly rather than filing the documents away and forgetting about them.

Key Takeaway

The best probate-avoidance strategy is usually not one document.

It is a coordinated estate plan that combines the right legal documents, properly titled assets, current beneficiary designations, and regular reviews as your life changes.

Looking Ahead

In the next section, we’ll examine one of the most powerful probate-avoidance tools available to many families—the Revocable Living Trust—and explain why so many estate planning attorneys recommend it as the cornerstone of a comprehensive estate plan.

Why Revocable Living Trusts Have Become the Cornerstone of Modern Estate Planning

If you ask experienced estate planning attorneys which single planning tool has had the greatest impact on helping families reduce probate, many will answer the same way:

A properly prepared and properly funded revocable living trust.

That doesn’t mean everyone needs one.

It does mean that for millions of families, a revocable living trust has become one of the most effective ways to organize an estate and simplify what happens after death or incapacity.

More Than a Probate-Avoidance Tool

Many people think a trust exists for one purpose—to avoid probate.

While avoiding probate is often a significant benefit, a revocable living trust can provide much more.

Depending on your circumstances, it may also:

- Provide management of your assets if you become incapacitated.

- Allow your successor trustee to step in without court involvement.

- Keep much of your estate administration private.

- Simplify the management of property located in multiple states.

- Provide instructions for distributing assets over time rather than all at once.

- Help coordinate your overall estate plan with your will, powers of attorney, and beneficiary designations.

For many families, these advantages are just as valuable as avoiding probate.

The Trust Must Be Funded

One of the biggest misconceptions about living trusts is that signing the document is all that is required.

It is not.

After the trust is created, many assets must be retitled into the name of the trust or otherwise coordinated with the trust.

This process is commonly called funding the trust.

For example, you may need to:

- Transfer ownership of your home.

- Retitle certain investment accounts.

- Update financial records.

- Coordinate beneficiary designations where appropriate.

- Maintain schedules of trust assets.

A trust that is never funded may provide little or no probate-avoidance benefit for those assets that remain outside the trust.

A Trust Does Not Replace Every Estate Planning Document

Even people with a revocable living trust generally need additional planning documents.

A complete estate plan often includes:

- A Pour-Over Will

- Durable Financial Power of Attorney

- Advance Healthcare Directive

- HIPAA Authorization

- Final Disposition Instructions

- Current beneficiary designations

- An organized estate planning portfolio

These documents work together.

No single document performs every estate planning function.

Is a Revocable Living Trust Right for Everyone?

Not necessarily.

Some people own very few probate assets.

Others may qualify for simplified probate procedures under their state’s laws.

For some families, a carefully prepared will combined with beneficiary designations and proper asset ownership may accomplish their goals.

For others—particularly homeowners, families with multiple financial accounts, blended families, or individuals who value privacy and long-term organization—a revocable living trust may offer significant advantages.

The right decision depends on your assets, your family, your goals, and the laws of your state.

A Trust Is Part of a Plan

A trust should never be viewed as a stand-alone document.

It works best when it is part of a coordinated estate plan that includes:

- Clearly titled assets.

- Current beneficiary designations.

- Updated legal documents.

- Organized financial records.

- Regular reviews as your life changes.

Estate planning is not about collecting documents.

It is about creating a system that your loved ones can understand and follow when they need it most.

Looking Ahead

Future lessons in the Estate Planning Academy will continue to build your understanding of trusts and other estate planning strategies so you can make informed decisions about your own plan.

If you decide you’re ready to begin creating and organizing your estate planning documents, the RetireCoast Estate Planning Membership provides access to the Revocable Living Trust Builder, along with interactive planning tools, document builders, implementation guides, checklists, and ongoing resources designed to help you create, maintain, and update your estate plan as your life changes.

Whether you choose to prepare your own documents, work with an attorney, or use a combination of both, our goal is to help you become an informed participant in the planning process and leave your family with a well-organized estate.

When Probate May Still Be Necessary

Estate planning can reduce or avoid probate for many assets, but probate cannot always be eliminated entirely.

Even a carefully prepared estate plan may leave some property outside a trust or without a valid beneficiary designation. In other cases, court involvement may be necessary to resolve debts, confirm ownership, settle disputes, or transfer property that cannot pass automatically.

The goal of estate planning is not to pretend probate will never occur.

The goal is to reduce unnecessary probate, simplify the process when possible, and make sure your family knows what to do if court administration is required.

Property Left Outside a Trust

A revocable living trust can help avoid probate only for property properly transferred into the trust.

If a person creates a trust but never transfers ownership of the home, financial accounts, or other assets into it, those assets may still require probate.

This is one reason trust funding is so important.

A pour-over will may direct remaining assets into the trust after death, but those assets may still need to pass through probate before the trust can receive them.

No Beneficiary Was Named

Accounts that allow beneficiary designations may still become probate assets when:

- No beneficiary was named.

- The beneficiary died first.

- The designation was incomplete.

- The institution cannot identify the beneficiary.

- The estate was named as beneficiary.

- All primary and contingent beneficiaries are deceased.

This can happen with life insurance, retirement accounts, annuities, bank accounts, and investment accounts.

Naming contingent beneficiaries can reduce this risk.

The Beneficiary Is a Minor

A minor child generally cannot directly control a substantial inheritance.

If a beneficiary designation leaves money directly to a minor, court involvement may be required to establish a guardianship or custodial arrangement.

A trust can often provide a more organized way to manage the inheritance until the child reaches an appropriate age.

Real Estate Was Owned Individually

Real estate titled solely in the deceased owner’s name is one of the most common reasons probate is required.

The property may need to be transferred through probate unless another method applies, such as:

- Trust ownership

- Survivorship ownership

- A transfer-on-death deed

- A beneficiary deed

- A state small-estate real property procedure

The available options depend on state law.

Property Is Located in Another State

A person who owns real estate in more than one state may face probate in more than one jurisdiction.

The main probate proceeding usually occurs in the state where the deceased person lived.

A second proceeding, commonly called ancillary probate, may be required in the state where the additional real estate is located.

This can mean:

- More court filings

- Additional attorney fees

- More waiting periods

- Separate local procedures

- Additional administrative work

Proper trust planning may help avoid ancillary probate for real estate transferred into the trust.

Ownership Is Unclear

Probate may be needed when there is uncertainty about who legally owns an asset.

Examples include:

- An unrecorded deed

- A missing title

- Informal business ownership

- Property purchased with another person

- Assets held under an outdated name

- Conflicting account records

- Undocumented family loans

- Personal property claimed by several relatives

The court may need to determine ownership before the property can be distributed.

The Will Is Contested

A probate court may be required to resolve disputes about whether a will is valid.

A challenge may allege:

- The person lacked mental capacity.

- The will was signed improperly.

- Someone exerted undue influence.

- Fraud occurred.

- A later will exists.

- The document was altered.

- The deceased person revoked the will.

Will contests can significantly increase the time and cost of probate.

Clear documents, proper execution, and careful planning can reduce—but not always eliminate—the risk of a dispute.

Beneficiaries Disagree

Even when the will is valid, beneficiaries may disagree about how the estate should be managed.

Common disputes include:

- Whether to sell the family home

- How personal property should be divided

- Whether the executor is acting properly

- Whether an asset was a gift or a loan

- Whether one family member received too much during life

- Whether the executor should receive compensation

- Whether estate property has been lost or misused

The probate court can provide a formal process for resolving these disagreements.

Creditors Must Be Addressed

Probate may provide an organized system for notifying creditors and resolving claims.

This can be especially important when the deceased person had:

- Significant credit card debt

- Medical bills

- Business obligations

- Personal loans

- Tax debts

- Lawsuits

- Unknown creditors

The court-supervised process can help determine which debts are valid and the order in which they should be paid.

The Estate Is Insolvent

An estate is insolvent when its debts and expenses exceed the available assets.

In this situation, beneficiaries may receive little or nothing.

The personal representative must follow state law regarding creditor priorities and should not distribute property to heirs before valid obligations are resolved.

Court oversight may help protect the representative from making improper payments.

A Business Interest Requires Court Authority

A business may require immediate decisions after the owner’s death.

Someone may need authority to:

- Pay employees

- Access business accounts

- Sign contracts0

- Collect receivables

- Maintain insurance

- Sell inventory

- Manage property

- Continue or close operations

If the business succession plan is incomplete, probate court authority may be necessary before anyone can legally act.

This is why business owners need both personal estate planning and a separate business continuity plan.

Taxes or Litigation Remain Unresolved

An estate may need to remain open while tax questions, lawsuits, or other legal matters are resolved.

Examples include:

- A pending personal injury claim

- A business lawsuit

- An IRS dispute

- Unfiled tax returns

- A contested property sale

- A claim against an insurance company

- Money owed to the deceased person

These issues may delay final distribution.

Probate Can Provide Useful Protection

Probate is often discussed only as a burden, but the process can also provide important protections.

Court supervision may:

- Confirm the executor’s legal authority.

- Establish a deadline for creditor claims.

- Resolve disputes among heirs.

- Protect minor or vulnerable beneficiaries.

- Review estate accountings.

- Approve certain sales or distributions.

- Provide a formal method for closing the estate.

- Reduce uncertainty about ownership.

In a high-conflict or complicated estate, court oversight may be preferable to informal administration.

Avoiding Probate Does Not Eliminate Administration

Even when every major asset avoids probate, someone still has work to do.

The successor trustee, beneficiary, or surviving owner may need to:

- Obtain death certificates.

- Notify financial institutions.

- File tax returns.

- Pay final bills.

- Manage property.

- Transfer titles.

- Close accounts.

- Distribute personal belongings.

- Maintain records.

- Communicate with family members.

A trust avoids the probate court process for properly funded assets.

It does not eliminate the practical work of settling a person’s affairs.

Key Takeaway

Probate may still be required when property lacks a valid transfer method, ownership is unclear, debts remain unresolved, or family members disagree.

Thoughtful estate planning can reduce these risks, but it cannot guarantee that court involvement will never be necessary.

The most effective plan combines:

- Properly prepared documents

- Correct asset ownership

- Current beneficiary designations

- Trust funding

- Organized records

- Clear family communication

- Regular reviews

Looking Ahead

The next section explains simplified probate procedures and small-estate shortcuts.

You will learn why an estate that falls below a state’s dollar limit may qualify for an affidavit, summary administration, or another streamlined process—and why the presence of real estate can change the result.

Small Estate Procedures: When Probate May Be Simpler

Not every estate requires a lengthy probate proceeding.

Recognizing that many estates are relatively modest, most states have adopted one or more simplified probate procedures. These alternatives are designed to reduce court involvement, lower administrative costs, and allow heirs to settle qualifying estates more efficiently.

The requirements, however, vary significantly from one state to another.

Some states measure the value of the estate differently. Others exclude certain property from the calculation. Some allow real estate to qualify, while others limit simplified procedures to personal property only.

For that reason, there is no single nationwide “small estate” rule.

What Is a Small Estate?

A small estate is generally an estate that falls below a value established by state law and satisfies any additional legal requirements.

Depending on where you live, the law may consider:

- The total value of probate assets.

- Whether real estate is included.

- Whether debts exceed available assets.

- Whether a probate case has already been opened.

- Whether a required waiting period has passed.

- Whether all heirs agree.

- Whether a valid will exists.

Meeting the dollar limit alone does not necessarily mean the estate qualifies.

Common Types of Simplified Procedures

States use different names for these procedures.

You may encounter terms such as:

- Small Estate Affidavit

- Summary Administration

- Summary Probate

- Collection by Affidavit

- Affidavit for Collection of Personal Property

- Simplified Probate

- Petition for Summary Distribution

Although the names differ, the purpose is similar—to simplify administration for qualifying estates.

Why State Law Matters

An estate that qualifies for a simplified procedure in one state may require formal probate in another.

For example:

- One state may allow estates under a certain value to transfer personal property through an affidavit.

- Another may permit real estate to qualify under limited circumstances.

- A third may require formal probate whenever real estate is involved.

Because probate law is established by each state, you should never assume that advice given by a friend or family member applies where you live.

Small-estate rules are different in every state. A procedure that may simplify probate in one state may not be available—or may work very differently—in another.

Use the RetireCoast Small Estate Probate Shortcut Finder™ to select your state and review important information such as the small-estate limit, whether real estate may qualify, common waiting periods, and key restrictions.

Use Our Free State Probate Finder

To make this easier, we’ve created the RetireCoast Small Estate Probate Shortcut Finder™.

This free interactive tool allows you to select your state and instantly view information such as:

- Current small-estate threshold.

- Whether real estate may qualify.

- Waiting periods.

- Common simplified procedures.

- Important restrictions.

- Planning considerations.

Think of it as a starting point—not a substitute for legal advice—but an excellent way to understand how probate rules differ across the country.

Remember the Goal

While simplified probate procedures can save time and expense, the best estate plan often seeks to reduce the need for probate altogether.

As you’ve learned throughout this lesson, beneficiary designations, properly titled assets, payable-on-death accounts, transfer-on-death registrations, and revocable living trusts can often transfer assets without relying on small-estate exceptions.

Those planning strategies remain effective regardless of whether your estate qualifies as “small.”

Author’s Insight

Many people focus on staying below their state’s small-estate limit.

I encourage people to think differently.

Rather than asking, “Will my estate qualify for simplified probate?” ask “How can I organize my affairs so my family has as little court involvement as possible?”

That shift in thinking often leads to a more complete estate plan, regardless of the size of your estate.

Key Takeaway

Small-estate procedures are valuable tools, but they are not available in every situation and they differ dramatically from one state to another.

Understanding your state’s rules is important—but building an estate plan that minimizes unnecessary probate is even better.

Looking Ahead

reate teh callout Before we conclude this lesson, we’ll bring everything together by reviewing the most important probate planning principles and the practical steps you can take today to make life easier for the people you leave behind.

Your Probate Prevention Action Plan

You’ve covered a great deal of information in this lesson.

The good news is that reducing probate problems usually doesn’t happen because of one expensive legal document or one complicated strategy. More often, it happens because someone took the time to organize their affairs and make thoughtful decisions before a crisis occurred.

Whether your estate is worth $50,000 or $5 million, the same basic planning principles apply.

Step 1: Take Inventory of Your Assets

Before you can protect your estate, you need to know what you own.

Create a complete inventory of:

- Real estate

- Bank accounts

- Investment accounts

- Retirement plans

- Life insurance policies

- Vehicles

- Business interests

- Personal property

- Digital assets

- Valuable collections

- Safe deposit boxes

Knowing what you own is the foundation of every estate plan.

Step 2: Review How Each Asset Is Owned

Ask yourself:

- Is this asset owned individually?

- Is it jointly owned?

- Does it belong to my trust?

- Does it have a beneficiary designation?

- Does it have a POD or TOD designation?

Remember, how an asset is owned often determines whether it will pass through probate.

Step 3: Review Every Beneficiary

Many people spend hours preparing a will but forget to update their beneficiaries.

Review every:

- Life insurance policy

- IRA

- Roth IRA

- 401(k)

- Pension

- Annuity

- Transfer-on-death account

- Payable-on-death account

Also verify that contingent beneficiaries are listed whenever possible.

Step 4: Consider Whether a Revocable Living Trust Is Appropriate

Not everyone needs a trust.

However, homeowners, business owners, people with multiple financial accounts, blended families, or those who value privacy often find a revocable living trust to be one of the most effective planning tools available.

If you create a trust, remember that it must also be properly funded.

Step 5: Organize Your Records

One of the greatest gifts you can leave your family is organization.

Keep together:

- Estate planning documents

- Financial statements

- Insurance information

- Property records

- Business documents

- Tax returns

- Password instructions

- Contact information for advisors

A well-organized estate often settles more smoothly than one with missing paperwork and scattered records.

Step 6: Talk With Your Family

Many probate disputes begin because family members don’t understand the plan.

While you don’t have to disclose every financial detail, it is often helpful to let trusted family members know:

- Where important documents are stored.

- Who will serve as executor or trustee.

- Who should be contacted first.

- Where your estate planning binder is located.

- How to access your digital information.

- Your overall planning goals.

A short family conversation today may prevent months of confusion later.

Step 7: Review Your Plan Regularly

Estate planning is not something you complete once and forget.

Review your plan whenever you:

- Buy or sell property.

- Get married or divorced.

- Welcome a child or grandchild.

- Start or sell a business.

- Move to another state.

- Retire.

- Experience a significant financial change.

- Lose a beneficiary or fiduciary.

Your estate plan should grow and change as your life changes.

Don’t Wait for “Someday”

One of the biggest mistakes people make is believing they have plenty of time.

Unfortunately, accidents, illnesses, and unexpected events don’t follow a schedule.

Every year I speak with families who wish they had started sooner.

The best estate plan is not the perfect one.

It’s the one that is completed before it is needed.

Author’s Insight

When I began developing the RetireCoast Estate Planning Academy, I realized that most people don’t fail because they don’t care.

They fail because they don’t know where to begin.

That’s why this Academy was created—to break estate planning into understandable lessons and guide you through the process one step at a time.

Whether you complete every lesson or decide to continue with the RetireCoast Estate Planning Membership, my hope is that you leave this course with greater confidence and a clear roadmap for protecting the people you love.

Key Takeaway

Probate isn’t something to fear.

It’s something to understand.

Once you understand how probate works, you can make informed decisions that may reduce delays, lower costs, and make the administration of your estate much easier for your family.

Planning ahead isn’t about preparing for death.

It’s about taking care of the people who will one day take care of the things you’ve spent a lifetime building.

Looking Ahead

In EST 104 – Estate Planning Mistakes That Cost Families Thousands, we’ll examine the most common—and often costly—mistakes people make when preparing their estate plans. You’ll learn how seemingly small oversights can create major problems for your loved ones and how to avoid them before they happen.

References

- American Bar Association – Probate and Estate Administration Resources

- Internal Revenue Service (IRS) – Estate and Gift Tax Information

- National Conference of Commissioners on Uniform State Laws – Uniform Probate Code

- California Courts Self-Help Guide – Small Estates

- American College of Trust and Estate Counsel (ACTEC) – Estate Planning Resources

Select any question below to learn more about probate, estate administration, small-estate procedures, and common probate-avoidance strategies.

```You now have a solid understanding of one of the most misunderstood areas of estate planning. You've learned what probate is, why it exists, which assets commonly pass through probate, how the probate process works, and the planning strategies that may help reduce unnecessary court involvement for your family.