In this lesson, you'll learn how to build your own Estate Planning Team by selecting the professionals and trusted individuals who will help create, manage, and eventually carry out your estate plan. You'll discover the responsibilities of each role and how to choose the people best qualified to protect your wishes.

By the end of this lesson, you'll understand how attorneys, financial advisors, CPAs, insurance professionals, executors, trustees, healthcare agents, financial agents, and guardians each contribute to a successful estate plan—and how to make informed decisions when selecting them.

Throughout this lesson you'll also discover interactive decision-making tools available through the RetireCoast Estate Planning Membership that can help you objectively evaluate executors, trustees, powers of attorney, healthcare agents, and other fiduciaries while taking much of the emotion out of these important decisions.

Learn the roles of your estate planning attorney, financial advisor, CPA or tax professional, and insurance professional, and understand how these experts work together to help protect your estate and your family.

Discover how to choose an executor, trustee, Financial Power of Attorney, Healthcare Agent, and guardian for minor children based on qualifications, trustworthiness, and ability—not emotion or family expectations.

Learn why family communication, periodic reviews, and keeping your estate planning team informed are essential to ensuring your plan works exactly as you intend when it is needed most.

How to continue: When you complete this lesson, take the final Knowledge Check, review your action items, and then continue to the next lesson in the RetireCoast Estate Planning Master Class using the navigation buttons at the bottom of the page. You can also return to the Estate Planning Academy hub at any time to review previous lessons or explore additional estate planning resources.

You are currently studying EST 104 – Choosing Your Estate Planning Team, the fourth lesson in the Foundation Series. In this lesson, you'll learn how to build the team of professionals and trusted individuals who will help you create, protect, and eventually carry out your estate plan.

Estate planning includes many legal and financial terms that may be unfamiliar. Visit the RetireCoast Estate Planning Glossary for clear, plain-English definitions that support every lesson in the Estate Planning Academy.

- Who Should Be on Your Estate Planning Team?

- Your Estate Planning Attorney: The Quarterback of Your Planning Team

- Your Financial Advisor: Helping Your Estate Plan Work as Intended

- Your Tax Professional or CPA: Helping You Keep More of What You’ve Earned

- Your Insurance Professional: Protecting Your Estate Before It’s Needed

- Your Executor: The Person Who Carries Out Your Final Wishes

- Your Trustee: Managing Assets for the Benefit of Others

- Your Financial Power of Attorney: Someone to Act While You’re Still Alive

- Your Healthcare Agent: Speaking for You When You Cannot Speak for Yourself

- Your Guardian for Minor Children: Choosing Who Will Raise Your Children

- Bringing Your Team Together: Communication Is the Key to Success

- Lesson Summary

- Key Takeaways

- Additional Resources

Estate planning is not a do-it-yourself project that should be completed in isolation. While many people can prepare much of their own planning, one of the most important decisions you will make is choosing the right people to help you create, review, and eventually carry out your wishes.

In this lesson, you will learn who belongs on an estate planning team and the role each person plays.

You will discover when you may need an estate planning attorney, how a financial advisor and tax professional can help protect your assets, and why selecting the right executor, trustee, healthcare agent, and financial power of attorney is just as important as the documents themselves.

You’ll also learn that not everyone needs the same team. A young family with a modest estate may need only a few trusted advisors, while a business owner, investor, or retiree with substantial assets may benefit from a broader group of professionals working together.

The goal is not to create the largest team possible—it is to build the right team for your unique circumstances.

By the end of this lesson, you’ll have a practical framework for selecting qualified professionals, choosing trustworthy family members or friends for fiduciary roles, asking the right questions before making appointments, and avoiding common mistakes that can create unnecessary stress, delays, or expense for your loved ones.

A well-designed estate plan is built on more than legal documents. It is built on people you trust to protect your wishes when you can no longer speak for yourself. Choosing those people carefully is one of the most important investments you can make in your family’s future.

Author’s Note – Choosing the Right People Can Be One of the Hardest Decisions

For many people, deciding who should serve as executor, trustee, financial power of attorney, or healthcare agent is even more difficult than deciding how to distribute their assets. Family relationships, emotions, geography, age, financial experience, and personalities all play a role, making these decisions surprisingly challenging.

That’s one of the reasons I created the RetireCoast Estate Planning Membership. Inside the membership, you’ll find interactive decision-making tools that help you evaluate each fiduciary role objectively.

Rather than relying on emotion alone, the tools guide you through the qualifications, responsibilities, availability, and trustworthiness of each candidate, making it easier to select the person best suited for the job.

An added benefit is that your decision is based on a consistent process. If a family member ever asks why someone else was chosen, you’ll be able to explain that your decision was made using an objective evaluation—not favoritism or emotion.

This lesson, together with the other courses in the RetireCoast Estate Planning Master Class, is designed to give you the knowledge and confidence to make informed decisions that protect both your wishes and the people you love

Who Should Be on Your Estate Planning Team?

Many people believe estate planning begins with hiring an attorney. While an attorney is often an important member of your team, the planning process usually begins with you. No professional knows your family, your goals, your values, or your concerns better than you do.

Think of estate planning as assembling a team, with each member bringing a different area of expertise. Some people will help you create your plan, while others will eventually carry it out.

A typical estate planning team may include:

- You and, if applicable, your spouse or partner

- An estate planning attorney

- A financial advisor

- A certified public accountant (CPA) or tax professional

- An insurance professional

- Your executor or personal representative

- Your trustee

- Your financial power of attorney

- Your healthcare agent or healthcare proxy

- Successor fiduciaries to serve if your first choices are unable or unwilling to act

Not every estate requires every one of these professionals. Someone with a modest estate may only need an attorney and trusted family members to fill fiduciary roles. A business owner, investor, or high-net-worth family may benefit from a larger team that includes attorneys specializing in taxation, business succession, real estate, or asset protection.

The important point is that each person has a clearly defined responsibility. When everyone understands their role, your estate can be administered more efficiently, conflicts are reduced, and your family has a much smoother experience during an already difficult time.

Planning Tip

Don’t wait until you’re elderly or experiencing health problems to assemble your estate planning team. The best time to choose the people who will protect your interests is while you are healthy, independent, and able to carefully evaluate your options. You can always update your choices as your life changes.

What You’ll Learn Next

In the following sections, we’ll examine each member of your estate planning team individually, beginning with the professional who often coordinates the entire process—your estate planning attorney. You’ll learn what each role involves, what qualifications to look for, common mistakes to avoid, and practical tips for selecting the right person.

Your Estate Planning Attorney: The Quarterback of Your Planning Team

For most families, the estate planning attorney serves as the quarterback of the estate planning team. While you remain the decision-maker, your attorney helps ensure your wishes are translated into legally enforceable documents that comply with your state’s laws.

An estate planning attorney does much more than prepare a will. Depending on your circumstances, they may help you create a revocable living trust, durable financial power of attorney, advance healthcare directive, HIPAA authorization, beneficiary strategies, business succession plans, charitable giving plans, and other legal documents designed to protect you and your family.

What Does an Estate Planning Attorney Do?

An experienced estate planning attorney can help you:

- Explain your state’s estate and probate laws.

- Recommend the documents appropriate for your situation.

- Draft legally valid estate planning documents.

- Ensure your trust is properly funded.

- Coordinate beneficiary designations with your overall plan.

- Help reduce probate delays and unnecessary legal expenses.

- Recommend strategies to minimize taxes when appropriate.

- Update your documents as your life changes.

Their role is not to make decisions for you. Instead, they help you understand your options and prepare documents that accurately reflect your wishes.

Not Every Attorney Practices Estate Planning

One of the biggest mistakes people make is assuming every attorney is equally qualified to prepare estate planning documents.

Just as physicians specialize in different areas of medicine, attorneys often concentrate their practices in specific areas of law. A lawyer who spends most of their time handling divorces, criminal defense, or personal injury cases may have limited experience designing comprehensive estate plans.

Whenever possible, look for an attorney whose practice is focused primarily on estate planning, trusts, probate, elder law, or related fields. Their experience with these matters often means they are more familiar with changes in state law, current planning techniques, and the practical issues families encounter after someone passes away.

Questions to Ask Before Hiring an Attorney

Before selecting an estate planning attorney, consider asking questions such as:

- How much of your practice is devoted to estate planning?

- How many estate plans do you prepare each year?

- Do you create both wills and revocable living trusts?

- Will you help ensure my trust is properly funded?

- How are future updates handled?

- What happens if I move to another state?

- Will you be available to answer questions after my documents are completed?

These questions help you understand not only the attorney’s qualifications but also the level of ongoing service you can expect.

Remember: You Are the Client

Your attorney provides legal advice, but the decisions remain yours. You decide who receives your property, who serves as executor and trustee, who will care for your children, and who will make financial and healthcare decisions if you become incapacitated.

The attorney’s responsibility is to transform those decisions into documents that are legally sound and designed to accomplish your objectives.

As you continue through this lesson, you’ll see that the attorney is only one member of your estate planning team. Financial professionals, tax advisors, insurance specialists, and the fiduciaries you appoint each play an important role in helping your estate plan succeed.

Money-Saving Tip: Don’t Pay an Attorney to Teach You the Basics

For many people, working with an attorney is different from hiring someone for a fixed-price project such as landscaping or replacing a roof. Estate planning attorneys often charge by the hour, although some offer flat-fee packages for certain services.

What does that mean for you? Every hour your attorney spends explaining basic estate planning concepts, gathering information you could have prepared in advance, or waiting while you decide who should serve as your executor or trustee may increase the total cost of your estate plan.

That’s why I recommend educating yourself before your first appointment. Complete this course, continue through the other lessons in the RetireCoast Estate Planning Master Class, and, if you become a member of the RetireCoast Estate Planning Membership, use the planning tools to organize your information and prepare draft documents at your own pace from the comfort of your home.

Once you’ve completed your planning, schedule an appointment with an experienced estate planning attorney and ask them to review your work.

They can identify areas that need to be changed, answer legal questions specific to your situation, and help ensure your documents comply with your state’s laws before they are signed, witnessed, and notarized where required.

This approach often makes your meetings more productive because you arrive organized, informed, and prepared with most of the decisions already made. Even more important, you’ll understand your estate plan rather than simply signing documents someone else prepared for you.

One additional benefit is that your planning doesn’t end after your documents are signed. As your life changes, you can return to the RetireCoast membership tools to update your information, prepare revised drafts, and then have those changes reviewed by your attorney whenever appropriate. Estate planning is an ongoing process—not a one-time event.

Your Financial Advisor: Helping Your Estate Plan Work as Intended

Creating legal documents is only one part of estate planning. Your assets—retirement accounts, investment accounts, life insurance policies, bank accounts, and other financial resources—must also be coordinated with your overall plan. This is where a qualified financial advisor can provide tremendous value.

A financial advisor helps ensure that your estate plan reflects your financial reality. They can identify assets that should be transferred into a trust, review beneficiary designations, and help make certain your investments and long-term financial goals support the legacy you want to leave behind.

What Does a Financial Advisor Do?

Depending on your circumstances, a financial advisor may help you:

- Review your current investment portfolio.

- Coordinate beneficiary designations on retirement accounts and life insurance policies.

- Evaluate whether assets should be owned individually, jointly, or by your trust.

- Develop retirement income strategies.

- Plan for long-term care and healthcare expenses.

- Analyze liquidity needs so your estate has sufficient cash to pay expenses.

- Coordinate with your attorney and tax professional to implement your estate plan.

A good advisor doesn’t replace your attorney. Instead, they work alongside your attorney to ensure your financial assets are aligned with your legal documents.

Beneficiary Designations Matter

Many financial assets pass directly to a named beneficiary and never become part of your will. These include:

- Employer retirement plans such as 401(k)s

- Individual Retirement Accounts (IRAs)

- Roth IRAs

- Life insurance policies

- Certain annuities

- Transfer-on-Death (TOD) accounts

- Payable-on-Death (POD) bank accounts

If these beneficiary designations are outdated or inconsistent with your estate plan, they may override what your will or trust says. For example, naming an ex-spouse as the beneficiary of a retirement account could unintentionally transfer those assets to that person, even if your will says otherwise.

This is one of the most common—and most expensive—estate planning mistakes families make.

A Team Approach Produces Better Results

The most effective estate plans are often created when your attorney, financial advisor, and tax professional communicate with one another. Each professional views your situation from a different perspective:

- Your attorney focuses on legal documents and state law.

- Your financial advisor focuses on your investments, retirement income, and financial goals.

- Your tax professional focuses on minimizing taxes and ensuring compliance with tax laws.

When these professionals work together, they can often identify opportunities and potential problems that one person working alone might miss.

Review Your Financial Plan Regularly

Your financial situation will likely change over time. You may retire, inherit money, purchase investment property, open new retirement accounts, or change employers. Any of these events may require updates to your estate plan.

A good practice is to review your estate plan whenever you experience a significant financial change and to conduct a complete review every few years. Estate planning is most effective when your legal documents and financial strategy evolve together.

Planning Tip: Consider Working with a Fiduciary Financial Advisor

If you decide to work with a financial advisor, consider asking whether they are acting as a fiduciary when providing advice. A fiduciary is legally obligated to place your interests ahead of their own when making recommendations.

Many fiduciary advisors are compensated through a transparent fee for their planning services rather than commissions on the financial products they recommend. Other advisors may earn commissions or other forms of compensation from investment products or transactions.

That does not necessarily mean their advice is poor, but it is important to understand how your advisor is paid and whether any potential conflicts of interest could exist.

Before choosing an advisor, don’t hesitate to ask:

- Are you a fiduciary at all times or only in certain situations?

- How are you compensated?

- Do you receive commissions from investments or insurance products?

- Will you provide your fiduciary obligation in writing?

Estate planning is built on trust. The more transparent your advisor is about their responsibilities and compensation, the more confident you can be that your estate plan is designed to serve your goals—not someone else’s.

Your Tax Professional or CPA: Helping You Keep More of What You’ve Earned

Taxes can have a significant impact on your estate, especially if you own retirement accounts, investment property, a business, or highly appreciated assets. While many families won’t owe a federal estate tax, income taxes, capital gains taxes, and state taxes can still affect the amount ultimately received by your heirs.

That’s why many estate planning teams include a Certified Public Accountant (CPA) or other qualified tax professional.

What Does a Tax Professional Do?

A tax professional helps you understand the tax consequences of your estate planning decisions before they become costly mistakes. Depending on your situation, they may help you:

- Evaluate the tax consequences of gifting assets during your lifetime.

- Review capital gains implications before selling appreciated property.

- Coordinate retirement account withdrawal strategies.

- Help reduce unnecessary income taxes for your heirs.

- Advise on charitable giving strategies.

- Coordinate business succession planning from a tax perspective.

- Work with your attorney to implement tax-efficient estate planning strategies.

Their goal is not simply to prepare your annual tax return. A knowledgeable tax professional helps you understand how today’s decisions may affect your family’s financial future for years to come.

Taxes Change Frequently

One of the biggest challenges in estate planning is that tax laws rarely remain the same for long.

Congress periodically changes income tax rates, estate tax exemptions, retirement account rules, charitable deduction provisions, and many other tax-related laws. In addition, each state may have its own tax rules that affect your estate planning strategy.

Because of these frequent changes, it’s important to review your estate plan whenever significant tax legislation is enacted or when your financial circumstances change.

Working Together Creates Better Results

Your attorney writes the legal documents.

Your financial advisor helps coordinate your assets and investments.

Your tax professional evaluates the tax consequences of the decisions being made.

When these professionals communicate with one another, they often identify opportunities to reduce taxes, avoid unintended consequences, and ensure that your estate plan operates as efficiently as possible.

Don’t Wait Until Tax Season

Many people only speak with their CPA once a year while preparing their tax return. Estate planning deserves more attention than that.

If you’re planning to retire, sell a business, receive an inheritance, make substantial gifts, convert a traditional IRA to a Roth IRA, or transfer significant assets into a trust, those are all excellent times to consult your tax professional before taking action.

A brief conversation beforehand may prevent an expensive mistake that cannot easily be reversed later.

Choosing the Right Tax Professional

You’ll often hear the terms CPA, accountant, and tax advisor used interchangeably, but they are not necessarily the same. Each may provide valuable services, but their education, credentials, and scope of practice can differ.

If you own a business, rental properties, or have a more complex financial situation, I strongly recommend working with a Certified Public Accountant (CPA). CPAs are licensed professionals who meet rigorous education, examination, and continuing education requirements.

In addition to preparing tax returns, many CPAs provide tax planning, financial consulting, business advisory services, and may also serve as trusted financial advisors.

Some tax professionals also hold the designation of Enrolled Agent (EA). An Enrolled Agent is licensed by the Internal Revenue Service and is authorized to represent taxpayers before the IRS on audits, collections, and appeals. This credential reflects specialized expertise in federal tax law.

If your finances are relatively straightforward—for example, you have employment income, a home, retirement accounts, and a simple estate—you may be well served by an experienced accountant or reputable tax advisor.

The key is to choose someone with a solid reputation, current knowledge of tax law, and experience working with clients whose financial situation is similar to yours.

Whatever type of professional you select, ask about their experience, credentials, and how they stay current with changes in tax laws. The quality of the advice you receive is often more important than the title on a business card.

Your Insurance Professional: Protecting Your Estate Before It’s Needed

One of the primary goals of estate planning is preserving the assets you’ve worked a lifetime to build. Insurance plays an important role in accomplishing that goal by protecting your family from unexpected financial losses that could otherwise reduce or even eliminate a significant portion of your estate.

While many people think of insurance only as something they purchase and hope never to use, it is actually one of the foundational layers of a comprehensive estate plan.

Why Insurance Matters

Imagine spending decades building your savings only to have a major lawsuit, house fire, disability, or unexpected death create financial hardship for your family. The right insurance coverage can help provide the financial resources needed to recover from those events.

An insurance professional can help evaluate whether your current coverage is appropriate for your family’s needs and identify gaps that should be addressed.

Types of Insurance That May Be Important

Depending on your circumstances, your estate planning team may review:

- Life insurance

- Disability income insurance

- Long-term care insurance

- Homeowners insurance

- Flood insurance

- Wind and hail insurance

- Automobile insurance

- Umbrella liability insurance

- Business insurance

- Professional liability insurance (if applicable)

Not everyone needs every type of insurance. Your coverage should reflect your assets, liabilities, occupation, family responsibilities, and overall financial goals.

Life Insurance Is More Than an Inheritance

Many people purchase life insurance to replace lost income for a surviving spouse or children. However, life insurance can also help:

- Provide immediate cash to surviving family members.

- Pay funeral and burial expenses.

- Help pay debts and mortgages.

- Provide liquidity so assets don’t have to be sold quickly.

- Equalize inheritances among beneficiaries.

- Support a family business during a transition.

When used appropriately, life insurance can make administering an estate significantly easier.

Review Your Coverage Regularly

Insurance needs change throughout life.

Marriage, children, retirement, purchasing a home, starting a business, paying off a mortgage, or accumulating significant investments may all require updates to your insurance portfolio.

An annual insurance review is a good habit and should be part of your overall estate planning review process.

Insurance Is Part of Asset Protection

Think of insurance as one of the first lines of defense for your estate.

Every dollar paid by an insurance company after a covered loss is potentially one less dollar that must come from your personal savings or investment accounts. Proper insurance helps preserve the assets you’ve accumulated and reduces the financial burden on your loved ones during difficult times.

In the next lesson of the Estate Planning Academy, we’ll explore insurance planning in much greater detail and examine how different types of insurance work together to help protect your family and your estate.

❓ What People Often Ask

Do I need life insurance?

The answer depends entirely on your personal circumstances.

If you have young children, a spouse who depends on your income, or significant financial obligations such as a mortgage, life insurance may be one of the most important financial decisions you make. The proceeds can replace lost income, pay debts, fund education, and provide financial security while your family adjusts to life without you.

On the other hand, if you’re retired, financially independent, have no dependents, and your estate has sufficient assets to meet your family’s needs, you may find that life insurance is no longer necessary or that your coverage needs have changed significantly.

There is no one-size-fits-all answer. Your insurance needs should be evaluated based on your age, income, assets, debts, family responsibilities, and long-term estate planning goals.

Throughout the RetireCoast Estate Planning Master Class, we’ll revisit this topic in greater detail. In particular, Lesson EST 304 and Lesson EST 403 examine how life insurance fits into an overall estate plan, when it can provide significant value, and situations where it may no longer be needed.

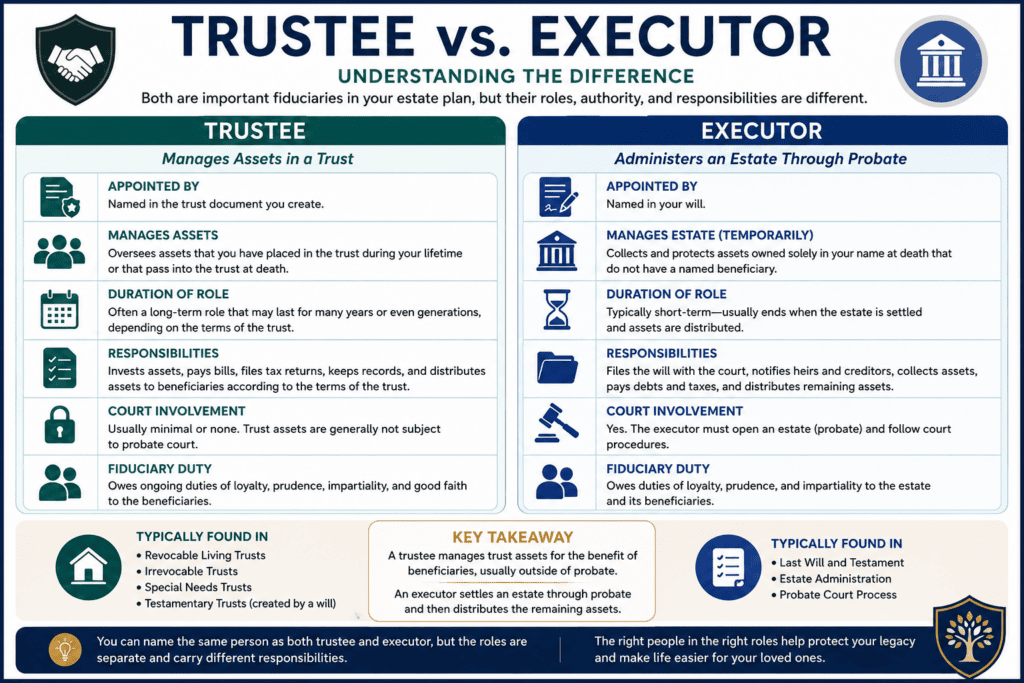

Your Executor: The Person Who Carries Out Your Final Wishes

Choosing an executor may be one of the most important decisions you make during the estate planning process. While your will expresses your wishes, your executor is the person responsible for making sure those wishes are carried out.

This role requires far more than simply distributing property. An executor has legal responsibilities, financial responsibilities, and a fiduciary duty to act in the best interests of your estate and your beneficiaries.

What Does an Executor Do?

Although the exact duties vary by state, an executor is commonly responsible for:

- Locating your original estate planning documents.

- Filing your will with the appropriate probate court.

- Identifying and protecting estate assets.

- Notifying beneficiaries and creditors.

- Paying valid debts, taxes, and estate expenses.

- Working with attorneys, accountants, and financial institutions.

- Maintaining accurate financial records.

- Distributing property according to your will.

- Closing the estate when all responsibilities have been completed.

Depending on the size and complexity of your estate, these duties may take several months—or even several years—to complete.

Who Should You Choose?

Many people automatically name their oldest child, a spouse, or another close family member as executor. While that may be the right decision, family relationship alone should not be the deciding factor.

Instead, consider whether the individual is:

- Honest and trustworthy.

- Organized and detail-oriented.

- Financially responsible.

- Able to communicate well with family members.

- Comfortable making difficult decisions.

- Willing to serve.

- Physically and mentally capable of handling the responsibilities.

- Likely to outlive you or be available when needed.

Remember, being your favorite child or closest relative does not automatically make someone the best executor.

Should You Choose a Professional?

For larger or more complicated estates, some people appoint a professional executor such as an attorney, bank trust department, or professional fiduciary.

Professional executors bring experience and objectivity to the process and can be especially helpful when:

- Family conflict is expected.

- The estate includes substantial investments.

- A business is involved.

- Multiple properties must be managed or sold.

- Beneficiaries live in different states.

- The estate is unusually complex.

The tradeoff is that professional executors generally charge fees for their services, while family members may choose to waive or reduce their compensation.

Always Name a Backup

Life changes.

The person you choose today may become unable or unwilling to serve years from now because of illness, relocation, or death.

For that reason, your will should normally name one or more successor executors who can step into the role if your first choice cannot serve.

Choosing an Executor Is About Ability, Not Emotion

Selecting an executor should never be viewed as a popularity contest or a reward for being the oldest child. Instead, think of the position as hiring someone for an important job.

The best executor is the person most capable of carrying out your wishes fairly, responsibly, and efficiently. Choosing the right individual today can spare your family unnecessary stress, delays, and conflict during one of the most difficult periods of their lives.

Choosing an executor is one of the most important decisions you’ll make when creating your estate plan. Because this person will have significant legal and financial responsibilities, it’s important to evaluate candidates objectively rather than making a decision based solely on family relationships or emotions.

The RetireCoast Estate Planning Membership includes an interactive Executor Selection Decision Tool that guides you through the evaluation process. You’ll compare potential candidates based on factors such as trustworthiness, organizational skills, financial responsibility, availability, communication skills, impartiality, and willingness to serve.

The result is a structured, objective evaluation that helps you select the individual best qualified to administer your estate. It also provides a logical framework you can use to explain your decision to family members, should questions ever arise.

Your Trustee: Managing Assets for the Benefit of Others

If your estate plan includes a revocable living trust or another type of trust, you’ll need to choose someone to serve as your trustee. While people often confuse the roles of executor and trustee, they have very different responsibilities.

An executor administers your estate through the probate process under the authority of your will. A trustee manages assets that are owned by a trust according to the instructions contained in the trust agreement.

In many estate plans, the same individual serves as both executor and trustee. In others, different people are selected because each role requires a different set of skills.

What Does a Trustee Do?

Depending on your trust, a trustee may be responsible for:

- Managing trust assets.

- Investing trust funds prudently.

- Maintaining financial records.

- Paying expenses and taxes owed by the trust.

- Making distributions to beneficiaries according to the trust’s instructions.

- Communicating with beneficiaries.

- Protecting trust property.

- Following the terms of the trust exactly as written.

Unlike an executor, whose job usually ends after the estate is settled, a trustee may continue serving for many years—or even decades.

For example, if your trust provides for young grandchildren, a child with special needs, or ongoing management of family property, your trustee could remain in that role long after your estate has been settled.

Qualities of an Effective Trustee

A good trustee should be:

- Honest and trustworthy.

- Financially responsible.

- Organized and detail-oriented.

- Able to understand legal and financial documents.

- Fair and impartial.

- Comfortable making long-term financial decisions.

- Willing to work with attorneys, accountants, and investment professionals.

- Committed to following your instructions—not their own preferences.

Perhaps most importantly, a trustee must understand that the trust assets do not belong to them. Every decision must be made for the benefit of the trust beneficiaries and in accordance with the terms of the trust.

Family Member or Professional Trustee?

Many people select an adult child, sibling, or trusted friend to serve as trustee. Others choose a bank trust department, trust company, attorney, or professional fiduciary.

A family member may better understand your family’s values and wishes, while a professional trustee offers experience, continuity, and impartiality. In some situations, people choose both—for example, naming a trusted family member to work alongside a professional trustee.

There is no universally correct answer. The best choice depends on the complexity of your trust, the personalities involved, and the long-term responsibilities your trustee will assume.

Choose Someone for the Long Term

Unlike an executor, who often serves for only a limited period, a trustee may have responsibilities that continue for many years.

Ask yourself:

- Will this person still be capable of serving 10 or 20 years from now?

- Do they have the time and organizational skills required?

- Are they comfortable handling investments and financial decisions?

- Can they remain impartial if disagreements arise among beneficiaries?

Thinking about these questions now can help prevent problems long after you’re gone.

Trustee Selection Deserves Careful Consideration

A trustee doesn’t simply safeguard money—they safeguard your legacy.

Selecting someone with integrity, sound judgment, and the willingness to faithfully follow your instructions is one of the most important decisions you’ll make during the estate planning process. Choosing wisely helps ensure your trust accomplishes exactly what you intended for the people you love.

Important Distinction: Revocable vs. Irrevocable Trusts

The discussion in this lesson is focused on selecting a trustee for a revocable living trust, which is the type of trust most families use as the foundation of their estate plan. With a revocable trust, it is common to appoint a spouse, adult child, trusted relative, or close friend as your successor trustee.

An irrevocable trust is different. Because these trusts are often created for asset protection, tax planning, charitable giving, Medicaid planning, or other specialized purposes, the choice of trustee becomes much more critical. In many cases, an independent trustee—such as a bank trust department, trust company, professional fiduciary, or other qualified third party—is the preferred choice.

Depending on the type of irrevocable trust and its purpose, appointing certain family members or friends may not be advisable and, in some situations, could undermine the planning objectives.

We’ll explore irrevocable trusts in detail in EST 503 – Advanced Trust Planning, including why they are used, how they differ from revocable trusts, and the factors that should guide your selection of an appropriate trustee.

Your Financial Power of Attorney: Someone to Act While You’re Still Alive

Many people assume estate planning is only about what happens after they die. In reality, one of the most important decisions you’ll make concerns what happens if you’re alive but unable to manage your own financial affairs.

That’s where a Financial Power of Attorney becomes essential.

By signing a Durable Financial Power of Attorney, you authorize another person—called your agent or attorney-in-fact—to act on your behalf if you become incapacitated or otherwise unable to manage your financial affairs.

Unlike an executor, who serves after your death, your financial agent serves during your lifetime.

What Can a Financial Agent Do?

The authority granted depends on the document you sign and your state’s laws, but your agent may be authorized to:

- Pay your bills.

- Manage bank accounts.

- Handle investment accounts.

- Buy or sell property if authorized.

- File tax returns.

- Collect income and benefits.

- Manage insurance matters.

- Sign contracts on your behalf.

- Conduct other financial transactions authorized by your Power of Attorney.

Some powers take effect immediately after signing, while others become effective only if you become incapacitated. Your attorney can explain which approach is appropriate for your situation.

Choose Someone You Trust Completely

This position requires an extraordinary level of trust.

Your financial agent may have access to your bank accounts, investments, and other assets. While they have a legal duty to act in your best interests, they also have significant authority.

When selecting this person, consider whether they are:

- Completely trustworthy.

- Financially responsible.

- Organized and dependable.

- Able to keep accurate records.

- Comfortable handling financial matters.

- Willing to serve.

- Able to make difficult decisions under pressure.

This is not a position to fill simply because someone is a close relative. Integrity and judgment are far more important than family hierarchy.

Consider Naming a Successor Agent

Life is unpredictable.

The person you select today may be unavailable years from now due to illness, relocation, or other circumstances.

For that reason, most attorneys recommend naming one or more successor agents who can step in if your first choice cannot serve.

This Authority Ends at Death

One of the most misunderstood aspects of a Financial Power of Attorney is its duration.

A Financial Power of Attorney automatically ends when you die.

At that point, authority transfers to your executor (if your estate is administered through a will) or your successor trustee (if your assets are held in a trust). Your financial agent no longer has the legal authority to act on your behalf after your death.

Understanding this distinction helps avoid confusion among family members and ensures that the right person is acting at the right time.

Choose Carefully

Your financial agent may one day be responsible for protecting everything you’ve worked to build while you’re unable to do so yourself.

Selecting someone with integrity, financial judgment, and the ability to act calmly under pressure is one of the most important decisions you’ll make during the estate planning process.

Family Communication Is Essential

Your decision about who will serve as your Financial Power of Attorney should be an important topic during your family meeting. While the legal document gives your chosen agent the authority to act on your behalf, it does not automatically mean every family member will understand—or agree with—your decision.

A Financial Power of Attorney may have the authority to access bank accounts, pay bills, manage investments, sell property if authorized, and make other significant financial decisions while you are alive.

If your wishes have not been clearly communicated, misunderstandings and accusations of favoritism or financial misconduct can arise, even when your agent is acting properly and in accordance with your instructions.

Whenever possible, explain why you selected a particular individual. Help your family understand that your decision was based on trust, financial ability, availability, and willingness to serve—not on who you love the most. Open communication today can prevent unnecessary conflict tomorrow.

One of the goals of estate planning is to preserve family relationships as well as family assets. A thoughtful family discussion about your Financial Power of Attorney can go a long way toward accomplishing both.

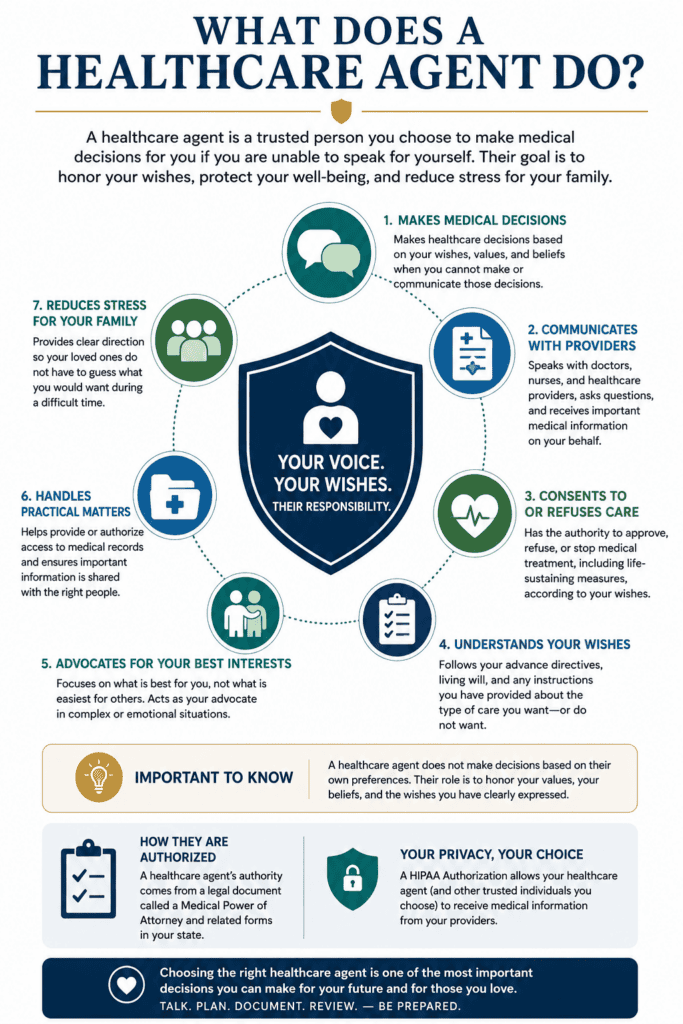

Your Healthcare Agent: Speaking for You When You Cannot Speak for Yourself

Few decisions in estate planning are as personal—or as important—as choosing the person who may make healthcare decisions on your behalf if you are unable to communicate with your doctors.

This individual is commonly called your Healthcare Agent, Healthcare Proxy, or Medical Power of Attorney, depending on your state’s laws and the documents you sign.

Unlike your Financial Power of Attorney, whose responsibilities involve managing your finances, your Healthcare Agent is responsible for helping ensure your medical wishes are honored.

What Does a Healthcare Agent Do?

If you become unable to make or communicate your own healthcare decisions, your Healthcare Agent may be authorized to:

- Speak with physicians and healthcare providers.

- Review medical information as permitted by law.

- Consent to or refuse certain medical treatments.

- Make decisions consistent with your Advance Healthcare Directive or Living Will.

- Arrange rehabilitation or long-term care services.

- Coordinate with family members and medical professionals.

- Advocate for your wishes when difficult medical decisions must be made.

Their responsibility is not to make decisions based on what they personally want. Their duty is to carry out your wishesas faithfully as possible.

Choose Someone Who Can Handle Difficult Conversations

Serving as a Healthcare Agent can be emotionally challenging.

You should choose someone who is:

- Calm under pressure.

- Emotionally mature.

- Able to communicate effectively with doctors and nurses.

- Comfortable asking questions.

- Willing to advocate for your wishes.

- Able to make difficult decisions even when family members disagree.

- Respectful of your personal values and beliefs.

This person should also be willing to honor your instructions, even if they personally would have chosen a different course of treatment.

Your Healthcare Agent Needs Guidance

Choosing the right person is only part of the process.

It’s equally important to discuss your healthcare preferences with them while you are healthy. Talk about topics such as:

- Life-support measures.

- Artificial nutrition and hydration.

- Pain management.

- Organ and tissue donation.

- Hospice care.

- Religious or personal beliefs that may affect treatment decisions.

- Quality of life considerations that are important to you.

These conversations may be uncomfortable, but they provide invaluable guidance if your Healthcare Agent is ever called upon to act.

Don’t Forget the HIPAA Authorization

Many people are surprised to learn that federal privacy laws can limit who may receive medical information about you.

A HIPAA Authorization allows the healthcare providers you designate to share your medical information with the people you choose. Without one, family members may have difficulty obtaining information about your condition, even if they are trying to help.

Your Healthcare Agent and your HIPAA Authorization often work together as part of a comprehensive incapacity plan.

```htmlComplete all four Foundation Courses to understand the essential principles of estate planning, organize your information, learn how probate works, and choose the people who will help carry out your wishes.

Learn why estate planning matters, which documents may be needed, and how a thoughtful plan helps protect your family and your legacy.

Go to EST 101 →Organize your legal documents, financial accounts, insurance information, digital assets, contacts, and personal instructions into one practical system.

Go to EST 102 →Discover what probate is, why it exists, the delays and expenses it may create, and the planning strategies that can help reduce court involvement.

Go to EST 103 →Learn how to select your attorney, financial professionals, executor, trustee, healthcare agent, financial agent, and other trusted decision-makers.

Go to EST 104 →One of the Greatest Gifts You Can Give Your Family

Making healthcare decisions for a loved one is never easy.

By selecting the right Healthcare Agent, documenting your wishes, and discussing them openly, you remove much of the uncertainty your family might otherwise face during an emotional and stressful time.

Your Healthcare Agent isn’t making decisions for you—they’re carrying out the decisions you’ve already made. That’s one of the greatest gifts you can leave the people who love you.

The HIPAA Hurdle: A Real-Life Problem That Happens Every Day

You’ve probably seen this scenario in a television drama or movie. A couple has been together for years. They share a home, own property together, and plan to get married someday. Then tragedy strikes—one partner is seriously injured or becomes unconscious.

The other partner rushes to the hospital, only to discover that doctors and nurses cannot discuss the patient’s condition in detail because of federal medical privacy laws. Without prior authorization, healthcare providers may be legally prohibited from sharing medical information, even with someone who knows the patient better than anyone else.

While every situation is different and healthcare providers may share limited information in certain circumstances, this is a very real issue that occurs every day across the United States. It can affect unmarried couples, close friends, fiancés, and even family members who have not been properly authorized.

One simple document—a HIPAA Authorization—can often prevent unnecessary frustration during an already stressful and emotional time. It allows you to identify the individuals with whom your healthcare providers may discuss your medical condition and treatment.

Don’t assume the people closest to you automatically have the legal right to receive your medical information. Make your wishes known in advance, complete the appropriate documents, and discuss them with those you’ve chosen to help you.

Your Guardian for Minor Children: Choosing Who Will Raise Your Children

For parents of minor children, choosing a guardian may be the most emotional decision in the entire estate planning process.

A guardian is the person you nominate to care for your children if both parents die or become unable to raise them. Although a court generally makes the final appointment, your written nomination provides powerful guidance and helps the court understand whom you trust to assume this responsibility.

Without a clear nomination, family members may disagree, and a judge who does not know your children or family dynamics may be required to decide who should raise them.

What Does a Guardian Do?

A guardian may become responsible for many of the decisions you currently make as a parent, including:

- Providing a safe and stable home.

- Making educational decisions.

- Arranging medical and dental care.

- Supporting your child’s emotional development.

- Encouraging family relationships.

- Providing discipline and guidance.

- Respecting your family’s values, traditions, and beliefs.

- Helping your child adjust after a devastating loss.

This responsibility may continue for years, depending on the age of your children when the guardian begins serving.

The Best Parent May Not Be the Best Money Manager

Many parents assume the same person should raise their children and manage the inheritance left for them. That is not always the best arrangement.

You may decide that one person is ideally suited to provide a loving home while another is better qualified to manage investments, approve distributions, and protect the children’s inheritance. In that case, you can nominate a guardian to care for the children and appoint a separate trustee to manage the financial assets held for them.

Dividing these roles can also create a useful system of oversight and reduce the financial burden placed on the guardian.

Questions to Consider

When evaluating potential guardians, think about:

- Does this person genuinely want to raise my children?

- Do my children already have a close relationship with them?

- Are their parenting values compatible with mine?

- Where do they live?

- Would my children need to change schools or move far from relatives?

- Are they physically and emotionally capable of raising children?

- Do they have room in their home?

- How would adding children affect their existing family?

- Would they support relationships with both sides of the family?

- Are they willing to follow the guidance I leave behind?

No candidate will be perfect. The goal is to select the person or couple most capable of providing the stability, love, and guidance your children will need.

Speak With the Person Before Naming Them

Never surprise someone with guardianship after your death.

Before naming a guardian, discuss the possibility openly. Explain why you are considering them, what responsibilities may be involved, what financial resources would be available, and what support they could expect from other family members.

Their circumstances may change over time, so revisit the conversation periodically.

Name at Least One Alternate Guardian

Your first choice may become unable or unwilling to serve because of health, divorce, relocation, age, or changes in family circumstances.

Naming one or more alternate guardians gives the court additional guidance and reduces the likelihood that family members will have to fight over the decision.

Leave More Than a Name

Your legal documents may nominate a guardian, but they cannot fully explain how you hope your children will be raised.

Consider preparing a separate letter of guidance that discusses:

- Education preferences.

- Religious or spiritual traditions.

- Family relationships you want preserved.

- Medical needs.

- Activities and interests important to each child.

- Your parenting values.

- The type of home environment you hope they will have.

This letter may not be legally binding, but it can become an invaluable source of guidance for the person entrusted with raising your children.

Choosing a guardian is difficult because no one can replace a parent. However, making a thoughtful decision now is far better than leaving that decision entirely to a court during a family crisis.

Bringing Your Team Together: Communication Is the Key to Success

Selecting the members of your estate planning team is only the first step. The next—and often overlooked—step is making sure everyone understands their role.

An estate plan is most effective when the people you’ve chosen know they’ve been selected, understand what is expected of them, and know where to find the information they’ll need when the time comes.

Too often, family members discover they’ve been named as executor, trustee, or healthcare agent only after a loved one has died or become incapacitated. That can create unnecessary stress during an already emotional time.

Tell People Before They Need to Act

Whenever possible, meet with the individuals you’ve chosen and discuss:

- Why you selected them.

- The responsibilities of their role.

- Where your estate planning documents are located.

- How to contact your attorney, CPA, financial advisor, and insurance professional.

- How to access important records when the time comes.

- Any special wishes that are not contained in your legal documents.

These conversations don’t need to reveal every detail of your estate. Instead, they help ensure everyone understands the responsibilities you’ve entrusted to them.

Hold a Family Meeting

One of the best ways to reduce future misunderstandings is to hold a family meeting after your estate plan has been completed.

During the meeting, you don’t have to disclose how much each person will inherit or discuss private financial matters. Instead, focus on explaining:

- Who you’ve appointed to serve in each fiduciary role.

- Why those individuals were selected.

- Where your important documents are stored.

- Who should be contacted first in an emergency.

- The importance of working together to carry out your wishes.

Families who communicate openly often experience fewer conflicts because expectations have already been established.

Keep Your Team Up to Date

People’s lives change.

The person you selected as executor ten years ago may now live across the country. Your trustee may have developed health issues. Your CPA may have retired. Your attorney may have changed firms.

Review your estate planning team periodically and update your documents whenever significant changes occur.

Estate Planning Is a Continuing Process

Many people think estate planning ends when they sign their documents.

In reality, signing your documents is simply the beginning.

Your estate plan should evolve as your family grows, your assets change, tax laws are updated, and the people you’ve chosen experience changes in their own lives.

The most successful estate plans are reviewed regularly—not because something is wrong, but because life never stands still.

Looking Ahead

In the next lesson, we’ll examine one of the most common reasons estate plans fail: outdated documents and missed updates. You’ll learn how small oversights—such as failing to update beneficiary designations, forgetting to transfer a new home into your trust, or neglecting to review your documents after major life events—can cost families thousands of dollars and create unnecessary complications.

By combining the right documents with the right people and a commitment to keeping your plan current, you’ll be well on your way to building an estate plan that protects both your assets and the people you love.

Simply Stated

An estate plan is only as effective as the people who carry it out.

You can have the best will, trust, powers of attorney, and healthcare documents ever written, but if you appoint the wrong executor, trustee, healthcare agent, or financial power of attorney, your family may still face unnecessary delays, disagreements, and expense.

Take your time. Choose people based on integrity, ability, judgment, and willingness to serve—not simply because they’re family or because you feel obligated.

The right team can make one of life’s most difficult times significantly easier for the people you love.

Lesson Summary

Building an estate plan involves much more than preparing legal documents. It also requires selecting the people who will help you create your plan today and the individuals who will carry out your wishes in the future. Those decisions may ultimately have a greater impact on your family’s experience than the documents themselves.

In this lesson, you learned that estate planning is a team effort. Depending on your circumstances, that team may include an estate planning attorney, financial advisor, Certified Public Accountant or tax professional, insurance professional, executor, trustee, financial power of attorney, healthcare agent, and guardian for your minor children.

Each person plays a unique role, and together they help ensure your wishes are carried out efficiently and according to your instructions.

You also learned that selecting fiduciaries should never be based solely on family relationships or emotions.

The best choices are individuals who possess integrity, sound judgment, organizational ability, financial responsibility, and a genuine willingness to serve. In many situations, the most qualified person may not be the oldest child, closest relative, or lifelong friend.

Communication is equally important. Discussing your decisions with the people you’ve selected—and, when appropriate, with your family—can prevent misunderstandings, reduce conflict, and make it easier for everyone to work together during a difficult time. An informed family is often a stronger family.

Finally, you learned that your estate planning team is not permanent. As your life changes, your family grows, professionals retire, and circumstances evolve, you should periodically review both your estate planning documents and the people you’ve chosen to carry them out.

Estate planning is an ongoing process that should grow with you throughout your lifetime.

By taking the time to build the right team today, you greatly increase the likelihood that your wishes will be honored, your loved ones will be protected, and your estate will be administered with the care and professionalism you intended.

Key Takeaways

By completing this lesson, you should now understand that:

- Estate planning is a team effort. Your attorney, financial advisor, tax professional, insurance professional, and fiduciaries each play an important role in protecting your wishes.

- You are the leader of your estate planning team. Professionals provide advice and prepare documents, but the important decisions belong to you.

- Choose an estate planning attorney with experience in trusts and estates. Not every attorney specializes in estate planning, and experience in this area matters.

- Consider working with fiduciary professionals whenever appropriate. Ask financial advisors how they are compensated and whether they are legally obligated to act in your best interests.

- A CPA or qualified tax professional can help identify tax-saving opportunities. Tax planning should be coordinated with your legal and financial planning.

- Insurance is an important part of protecting your estate. The proper coverage can preserve assets and provide financial security for your family.

- Your executor should be selected based on ability—not birth order or family expectations. Organization, integrity, and sound judgment are essential qualities.

- Your trustee has long-term responsibilities. Managing a trust often requires financial knowledge, impartiality, and a commitment to carrying out your instructions exactly as written.

- A Financial Power of Attorney protects you while you are living. Choose someone you trust completely to manage your financial affairs if you become unable to do so yourself.

- Your Healthcare Agent should understand and respect your medical wishes. Have conversations now so they can confidently advocate for your decisions later.

- A HIPAA Authorization is an essential companion document. It allows the people you choose to communicate with healthcare providers when medical privacy laws would otherwise prevent it.

- Parents of minor children should carefully choose a guardian. This may be one of the most important decisions in an entire estate plan.

- Communication helps prevent family conflict. Tell the people you’ve selected about their roles and consider holding a family meeting after your estate plan is completed.

- Review your estate planning team regularly. As life changes, your fiduciaries and professional advisors may need to change as well.

- The best estate plan combines the right documents with the right people. Either one without the other can leave your family facing unnecessary challenges.

Additional Resources

- American Bar Association – Estate Planning Resources

Guidance on selecting estate planning professionals, understanding legal documents, and planning for your family’s future. - National Association of Estate Planners & Councils (NAEPC)

Information about the estate planning profession and a directory of qualified estate planning councils throughout the United States. - Certified Financial Planner Board of Standards (CFP Board)

Learn about fiduciary financial planning and search for Certified Financial Planner™ professionals. - American Institute of Certified Public Accountants (AICPA)

Educational resources on working with Certified Public Accountants, tax planning, and financial decision-making. - National Institute on Aging – Advance Care Planning

Practical guidance on healthcare agents, advance directives, and discussing healthcare wishes with family members.

These questions address some of the most common concerns people have when selecting estate planning professionals, executors, trustees, financial agents, healthcare agents, guardians, and other trusted decision-makers.

```You’ve completed the Foundation Series. The next section of the Academy moves from understanding estate planning concepts to actually creating the core legal documents that form the heart of your estate plan.

We’ll begin with the document that many estate planning attorneys consider the cornerstone of modern estate planning—the Revocable Living Trust.

You've now learned one of the most important principles of estate planning: a successful estate plan depends not only on well-written legal documents, but also on the people you've chosen to create, manage, and carry out your wishes. Selecting qualified professionals and trustworthy fiduciaries today can save your loved ones significant stress, expense, and conflict tomorrow.

Continue your journey through the RetireCoast Estate Planning Academy by taking the next Master Class, or return to the Academy Hub to explore the complete curriculum and additional planning resources.

Ready to Build Your Own Estate Plan?

The RetireCoast Estate Planning Academy teaches you the knowledge behind estate planning. The RetireCoast Estate Planning Membership helps you put that knowledge into action with interactive decision-making tools, estate document builders, executor and trustee evaluation tools, your complete Estate Planning Portfolio, annual reviews, and dozens of practical resources designed to help you build and maintain your own estate plan.

Continue Learning with RetireCoast

Discover more from RetireCoast.com

Subscribe to get the latest posts sent to your email.

{kind=link}