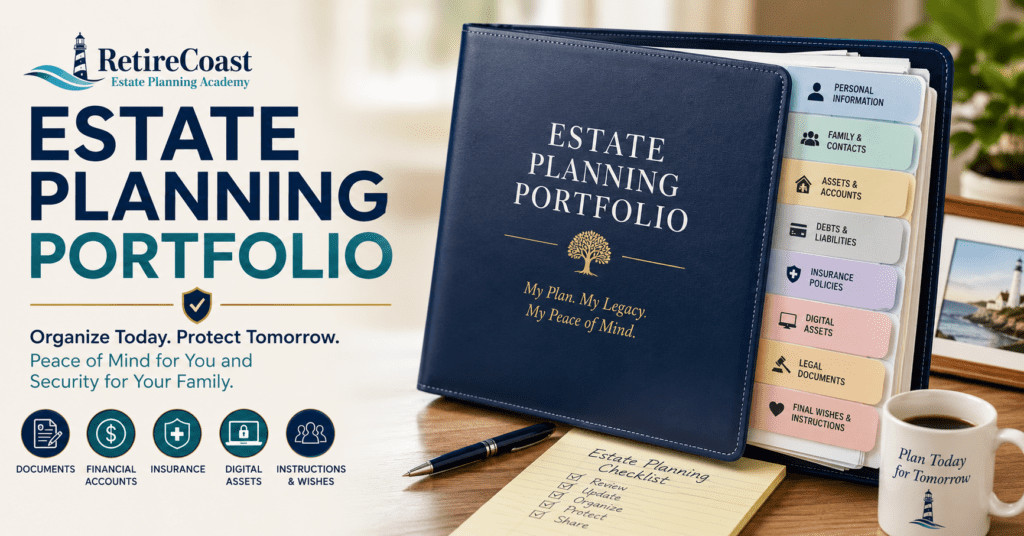

In this lesson, you will learn how to build a complete Estate Planning Portfolio that organizes every important document, financial account, insurance policy, password, contact, and personal instruction your family may need if you become incapacitated or pass away.

By the end of this Master Class, you will have a practical system for keeping your estate planning information organized, current, and easy for trusted family members and advisors to locate when it matters most.

You will also complete a short survey near the beginning of the lesson to assess your current level of preparedness. This is not a test. It simply helps you identify areas where your Estate Planning Portfolio may already be strong and areas that deserve additional attention.

Begin with a brief survey to evaluate how well your important documents, accounts, passwords, and personal information are currently organized before building your Estate Planning Portfolio.

As you work through the lesson, you will complete two short knowledge checks. They are designed to reinforce key concepts and help you build a complete, organized estate planning system—not to grade your performance.

Finish the lesson with a final knowledge check and a personalized checklist so you will know exactly what information still needs to be gathered before completing your estate planning documents or meeting with an attorney.

How to continue: When you complete this lesson, use the buttons at the bottom of the page to continue to EST 103 – Understanding Probate and How to Avoid It or return to the RetireCoast Estate Planning Academy hub to explore additional courses and resources.

You are currently studying EST 102 – Building Your Estate Planning Portfolio, the second lesson in the Foundation Courses. In this Master Class, you’ll organize the documents, accounts, policies, passwords, contacts, and instructions that form the foundation of a complete estate plan.

Estate planning includes many legal and financial terms that may be unfamiliar. Visit the RetireCoast Estate Planning Glossary for clear, plain-English definitions that support every lesson in the Estate Planning Academy.

- Introduction

- What Is an Estate Planning Portfolio?

- The Five Pillars of an Estate Planning Portfolio

- Step 4 – Inventory Your Debts and Financial Obligations

- Step 5 – Organize Your Insurance Portfolio

- Step 6 – Create Your Digital Estate Portfolio

- Step 7 – Organize Your Estate Planning Documents

- Step 8 – Record Your Final Wishes and Personal Instructions

- Step 9 – Organize Your Estate Planning Binder and Digital Portfolio

- Step 10 – How to Store and Protect Your Estate Planning Portfolio

- Step 11 – Who Should Have Access to Your Estate Planning Portfolio?

- Step 12 – Keeping Your Estate Planning Portfolio Up to Date

- References

- QUIZ

- SURVEY

- Ready to Build and Maintain Your Estate Planning Portfolio?

Introduction

Most people believe estate planning begins with creating a will or a trust. In reality, those documents are only part of the process. An estate plan is only as effective as the information that supports it. If your family cannot locate your accounts, insurance policies, passwords, property records, or important contacts, even the best legal documents may not provide the help you intended.

That is why every family should build an Estate Planning Portfolio.

An Estate Planning Portfolio is a carefully organized collection of the information your loved ones, trustee, executor, attorney, or financial advisor may need if you become incapacitated or pass away. Think of it as the instruction manual for your financial and personal life.

It brings together your legal documents, financial records, insurance information, digital assets, beneficiary designations, emergency contacts, and personal wishes into one secure, well-organized system.

Unlike a will or trust, your Estate Planning Portfolio is designed to be updated regularly. Bank accounts change, passwords are updated, insurance policies are replaced, and families grow. Your portfolio should evolve along with your life so the information is always accurate when someone needs it.

One of the greatest gifts you can leave your family is not money—it is organization.

Imagine a spouse trying to locate life insurance policies while planning a funeral. Consider an adult child searching through filing cabinets trying to determine which bank accounts exist or whether a safe deposit box is still active.

Picture a successor trustee attempting to administer a trust without knowing where investment accounts, deeds, tax returns, or business records are located.

Unfortunately, these situations happen every day.

Families often spend weeks searching for documents that could have been organized in a single afternoon.

A well-prepared Estate Planning Portfolio can dramatically reduce stress during one of life’s most difficult moments. It allows the people you trust to spend less time searching for information and more time supporting one another.

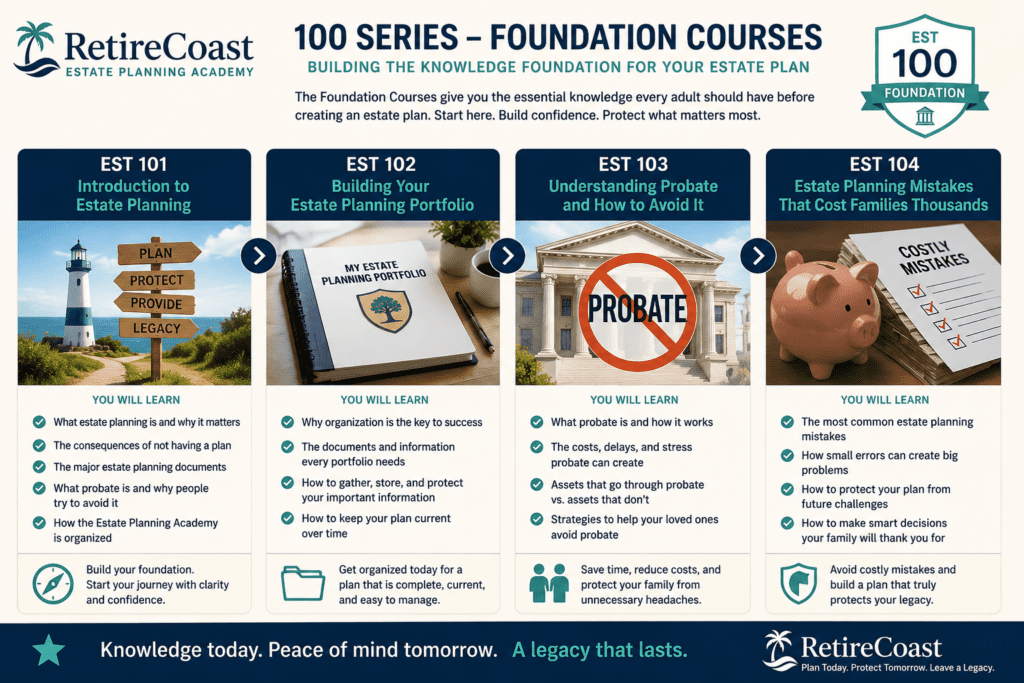

Why This Course Matters

In EST 101 – Introduction to Estate Planning, you learned why estate planning is important and how the major legal documents work together to protect you and your family.

In this second Foundation Course, you will move from understanding estate planning to actually organizing your personal information into a practical system. By the end of this lesson, you will know exactly what information belongs in an Estate Planning Portfolio, how to organize it, how to protect sensitive information, and how to keep it current throughout your lifetime.

You do not need to complete everything in a single day.

Instead, think of this lesson as building a roadmap. Every section you complete brings you one step closer to having an organized estate that will save your loved ones countless hours of frustration.

What You Will Build

During this Master Class, you will learn how to organize:

- Personal identification and family records

- Legal estate planning documents

- Financial accounts and investments

- Retirement plans and beneficiary designations

- Real estate and business interests

- Insurance policies

- Loans and other liabilities

- Digital assets and online accounts

- Password management systems

- Medical information and emergency contacts

- Final wishes and personal instructions

You’ll also learn how to securely store this information, determine who should have access to it, and establish a routine for reviewing and updating your Estate Planning Portfolio each year.

A Portfolio Is More Than a Binder

Years ago, an estate planning binder filled with paper documents was considered sufficient. While physical records remain important, today’s Estate Planning Portfolio usually includes both printed documents and secure digital records.

For example, you may have:

- A fireproof home safe containing original legal documents.

- A secure cloud storage account with scanned copies.

- A password manager that stores digital credentials.

- An encrypted flash drive containing important backups.

- Copies of key documents with your attorney or successor trustee.

Your goal is not simply to collect paperwork. Your goal is to create an organized system that allows trusted individuals to locate important information quickly when it is needed.

Remember the Purpose

Throughout this course, keep one simple question in mind:

“If I were suddenly unable to help my family tomorrow, could they easily find everything they need?”

If the answer is “yes,” your Estate Planning Portfolio is doing exactly what it was designed to do.

If the answer is “I’m not sure,” this Master Class will show you how to change that.

By the end of this lesson, you will have a clear framework for organizing every important aspect of your estate, creating one of the most valuable gifts you can leave the people you love.

What Is an Estate Planning Portfolio?

Many people believe an estate plan is simply a will or a trust stored in a safe. While those documents are extremely important, they represent only part of the information your family will need when an emergency occurs.

An Estate Planning Portfolio is a complete collection of the legal documents, financial information, account details, insurance policies, digital assets, personal instructions, and emergency contacts that allow someone else to manage your affairs if you become incapacitated or after your death.

Think of your portfolio as the owner’s manual for your life.

If a trusted family member suddenly needed to take over your financial affairs tomorrow, would they know where to begin? Would they know which bank you use, how many investment accounts you own, where your life insurance policies are located, or even how to access your email?

For many families, the answer is no.

An organized Estate Planning Portfolio answers these questions before they become emergencies.

An Estate Plan vs. an Estate Planning Portfolio

One of the biggest misunderstandings in estate planning is confusing the legal documents with the information that supports those documents.

Your estate plan contains the legal authority. Your Estate Planning Portfolio contains the practical information needed to carry out your wishes.

| Estate Plan | Estate Planning Portfolio |

|---|---|

| Will | Copies of the will and where the original is stored |

| Revocable Living Trust | Trust documents plus a list of trust assets |

| Durable Power of Attorney | Contact information for your appointed agent |

| Health Care Directive | Physicians, medications, insurance cards, and emergency contacts |

| Beneficiary Designations | A complete inventory of retirement accounts and insurance policies |

| Property Deeds | Property locations, mortgage information, insurance policies, and maintenance records |

| Legal Instructions | The information needed to carry out those instructions |

A helpful way to think about the difference is this:

- Your estate plan tells people what you want done.

- Your Estate Planning Portfolio tells them how to do it.

Both are necessary for an effective estate plan.

Why Legal Documents Alone Are Not Enough

Imagine your executor has your will but cannot find your investment accounts.

Suppose your successor trustee has your trust but has no idea where your online banking passwords are stored.

Perhaps your spouse knows you have life insurance but cannot remember which company issued the policy.

These situations create delays, unnecessary expenses, and frustration during an already emotional time.

A comprehensive Estate Planning Portfolio bridges the gap between your legal documents and your day-to-day financial life.

Who Should Create an Estate Planning Portfolio?

The simple answer is everyone.

Many people assume estate planning is only for retirees or wealthy families. In reality, every adult benefits from organizing important information.

You should have an Estate Planning Portfolio if you:

- Own a home.

- Have children or grandchildren.

- Have retirement accounts.

- Own life insurance.

- Have bank or investment accounts.

- Own a business.

- Own digital assets or online accounts.

- Have pets that depend on your care.

- Want to reduce stress for your loved ones.

- Simply want to be organized.

Even a young adult with modest assets can make life significantly easier for family members by keeping essential information in one secure location.

The Benefits of an Organized Estate Planning Portfolio

Creating an Estate Planning Portfolio provides benefits long before your estate is ever administered.

It helps you:

- Quickly locate important documents.

- Prepare for meetings with attorneys and financial advisors.

- Simplify tax preparation each year.

- Review beneficiary designations.

- Track insurance coverage.

- Monitor assets and debts.

- Update important records after major life events.

- Reduce the likelihood of forgotten accounts.

- Improve financial organization.

- Give family members confidence during emergencies.

Many people discover forgotten bank accounts, outdated beneficiaries, expired insurance policies, or missing documents while building their portfolio.

The process itself often improves the quality of their overall estate plan.

Your Portfolio Is a Living Document

Unlike a will, which may remain unchanged for several years, your Estate Planning Portfolio should be updated regularly.

Life changes constantly.

You may:

- Buy or sell a home.

- Open a new investment account.

- Change jobs.

- Start receiving Social Security.

- Retire.

- Change insurance companies.

- Welcome a new grandchild.

- Lose a loved one.

- Purchase a business.

- Update online passwords.

Every one of these events may require changes to your portfolio.

For that reason, think of your Estate Planning Portfolio as a living document rather than a one-time project.

Throughout This Course

In the pages ahead, you’ll build your Estate Planning Portfolio one section at a time.

Rather than overwhelming yourself by gathering everything at once, you’ll work through a logical process that mirrors the way professional estate planners organize client information.

By the end of this lesson, you’ll have a practical framework that can serve your family for decades, making it easier to keep important information current and readily available whenever it is needed.

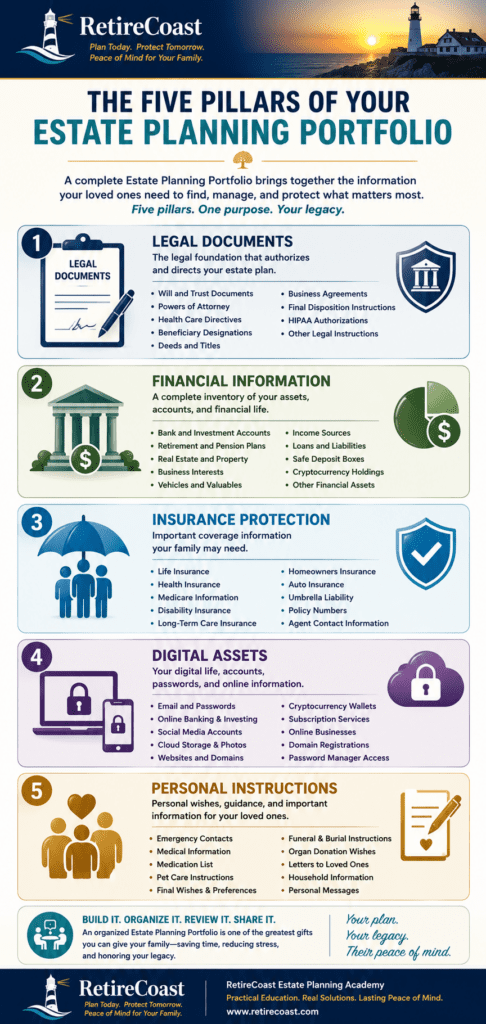

The Five Pillars of an Estate Planning Portfolio

Building an Estate Planning Portfolio may seem overwhelming at first. Fortunately, the process becomes much easier when you divide it into manageable sections.

Think of your portfolio as a house. Just as a house depends on a strong foundation and supporting walls, your Estate Planning Portfolio depends on several essential categories of information working together. If one area is missing or incomplete, your family may struggle to carry out your wishes during an emergency or after your death.

For that reason, we recommend organizing your portfolio around five core pillars.

Each pillar serves a different purpose, but together they create a complete picture of your financial and personal life.

Pillar One: Legal Documents

The first pillar contains the legal documents that authorize others to act on your behalf and direct how your estate should be administered.

These documents may include:

- Last Will and Testament

- Revocable Living Trust

- Irrevocable Trust (if applicable)

- Pour-Over Will

- Durable Financial Power of Attorney

- Health Care Power of Attorney

- Advance Health Care Directive or Living Will

- HIPAA Authorization

- Final Disposition Instructions

- Business agreements

- Property deeds

- Vehicle titles

- Beneficiary designation summaries

These are the documents most people associate with estate planning, but they are only one part of a complete Estate Planning Portfolio.

Pillar Two: Financial Information

Your family cannot manage assets they cannot identify.

The second pillar creates a complete inventory of your financial life so your executor, trustee, or loved ones know what exists and where to find it.

Examples include:

- Checking accounts

- Savings accounts

- Certificates of deposit

- Brokerage accounts

- Retirement plans

- Pension information

- Social Security information

- Real estate holdings

- Business ownership interests

- Vehicles

- Valuable personal property

- Safe deposit boxes

- Cryptocurrency holdings

- Outstanding loans

- Monthly income sources

A thorough inventory often uncovers forgotten accounts or outdated beneficiary designations that should be reviewed.

Pillar Three: Insurance Protection

Insurance is one of the most overlooked parts of an estate plan.

Without organized policy information, surviving family members may not even know coverage exists.

Your insurance section should include:

- Life insurance

- Health insurance

- Medicare information

- Disability insurance

- Long-term care insurance

- Homeowners insurance

- Flood insurance

- Windstorm insurance

- Automobile insurance

- Umbrella liability coverage

- Business insurance

- Policy numbers

- Insurance company contact information

- Agent contact information

Keeping all policy information together makes filing claims much easier during difficult times.

Pillar Four: Digital Assets

Modern estate planning extends far beyond paper documents.

Many families discover that valuable information is locked behind passwords, two-factor authentication, or online accounts that no one else can access.

Your digital portfolio may include:

- Email accounts

- Password manager information

- Online banking

- Investment websites

- Social media accounts

- Cloud storage

- Photo libraries

- Domain registrations

- Website hosting accounts

- Online businesses

- Cryptocurrency wallets

- Subscription services

- Digital reward programs

One important reminder: your Estate Planning Portfolio should identify where passwords are securely stored—not necessarily list every password. A reputable password manager is generally a safer solution than maintaining a printed password list.

Pillar Five: Personal Instructions

The final pillar brings together the information that often matters most to your family.

These instructions may not be legally binding, but they provide guidance during emotionally difficult times.

Examples include:

- Emergency contacts

- Physician information

- Medication lists

- Funeral preferences

- Burial or cremation wishes

- Organ donation instructions

- Military honors information

- Care instructions for pets

- Letters to loved ones

- Locations of important keys and safes

- Household operating information

- Family traditions and personal messages

Many families find these personal instructions to be among the most meaningful parts of an Estate Planning Portfolio because they reflect your values and help guide loved ones when difficult decisions must be made.

Why All Five Pillars Matter

Some people have excellent legal documents but no organized financial records.

Others carefully track investments but have never created a will.

Still others have everything documented except their digital assets, leaving family members unable to access important online accounts.

An effective Estate Planning Portfolio is strongest when all five pillars work together.

As you progress through this Master Class, you’ll build each pillar one step at a time. By the end of the course, you’ll have a comprehensive system that not only supports your legal estate plan but also provides your family with the practical information they need to carry out your wishes efficiently and with confidence.

What People Often Ask

1. Should my baseball card collection or coin collection be included in my Estate Planning Portfolio?

Yes—but only if the collection has meaningful financial value that can reasonably be established in today’s market.

For example, professionally graded baseball cards, rare coins, valuable stamps, fine art, or other collectibles may represent significant assets. Include a brief description, an estimated market value, where the collection is stored, and any appraisal information if available.

If the collection has primarily sentimental value or only modest resale value, simply include it under “Household Goods & Miscellaneous Personal Property.” There is no need to inventory every individual item.

2. Should I list everything that’s in my garage?

Generally, no.

Most garages contain ordinary household property such as lawn equipment, hand tools, bicycles, paint, storage containers, and seasonal decorations. These items usually do not need to be listed individually.

However, valuable items such as a classic automobile, antique tools, commercial equipment, expensive woodworking machinery, or other items worth several thousand dollars should be listed separately as estate assets.

A good rule of thumb is:

If you would insure it separately or someone would pay thousands of dollars to buy it, include it in your Estate Planning Portfolio.

3. What’s a valuable asset that people commonly forget to include?

One of the most commonly overlooked assets is a mineral interest or royalty interest.

Families often inherit mineral rights, oil and gas royalties, timber rights, or other property interests that continue producing income for decades. Because they may generate only occasional payments, they are frequently forgotten.

Other commonly overlooked assets include:

- Health Savings Accounts (HSAs)

- Retirement accounts from former employers

- Employee stock purchase plans

- U.S. Savings Bonds

- Cryptocurrency wallets

- Unclaimed property held by state governments

- Timeshares

- Intellectual property, such as patents or copyrights

Overlooking these assets can reduce the value of your estate and create unnecessary work for your executor.

4. Should I include items that have sentimental value but little financial value?

Absolutely.

Although these items may have little monetary value, they often carry tremendous emotional value and can become the source of family disagreements if your wishes are unknown.

Examples include:

- Wedding rings

- Family Bibles

- Military medals and uniforms

- Scrapbooks and photo albums

- Handmade quilts

- Family recipes

- Heirloom furniture

- Grandmother’s china

- Personal letters and journals

If there is a particular person you want to receive one of these items, consider documenting your wishes in a personal property memorandum or other written instructions that accompany your estate planning documents. Spending a few minutes identifying these special possessions today may prevent hurt feelings and family conflict tomorrow.

Some of the hardest estate decisions involve items with sentimental value rather than high financial value. Jewelry, family photographs, military medals, tools, furniture, holiday decorations, and keepsakes can create confusion or disagreement if no one knows what family members hoped to receive.

RetireCoast created this free Personal Property Request Worksheet so heirs can list personal possessions they would like you to consider during your estate planning process. It does not create a legal promise, but it can help you make thoughtful decisions and reduce misunderstandings later.

Member Advantage: A more robust version of this tool is included in the RetireCoast Estate Planning Membership. The membership version can be completed directly online and becomes part of a more complete Estate Planning Portfolio system.

Step 4 – Inventory Your Debts and Financial Obligations

When people think about estate planning, they naturally focus on what they own. Just as important, however, is understanding what they owe.

Your Estate Planning Portfolio should include a complete inventory of your debts and ongoing financial obligations. This information helps your executor, trustee, or surviving spouse understand the financial picture immediately instead of spending weeks trying to locate bills, loan statements, and creditors.

Remember, your heirs inherit your assets—but your estate is generally responsible for paying legitimate debts before assets are distributed to beneficiaries.

Why This Information Is Important

Imagine that your spouse suddenly becomes responsible for managing the household finances.

Would they know:

- Which credit cards are open?

- Where your mortgage is held?

- Whether you have a home equity line of credit?

- Which bills are automatically deducted each month?

- Whether there are outstanding personal or business loans?

Many families discover forgotten loans or recurring payments only after they continue withdrawing money from a bank account for months.

A complete debt inventory helps prevent surprises.

Debts to Include

As you build your Estate Planning Portfolio, create a list of every significant financial obligation.

This may include:

- Home mortgage

- Home equity line of credit (HELOC)

- Automobile loans

- Recreational vehicle loans

- Boat loans

- Personal loans

- Student loans

- Credit cards

- Business loans

- SBA loans

- Margin loans on investment accounts

- Tax payment plans

- Medical payment plans

- Installment contracts

For each obligation, record:

- Name of the lender

- Account number (partial numbers are acceptable)

- Approximate balance

- Monthly payment

- Interest rate (if known)

- Automatic payment information

- Contact information for the lender

Don’t Forget Automatic Payments

One of the most overlooked parts of estate planning is documenting recurring automatic payments.

Today, many households have dozens of monthly charges that occur without anyone writing a check.

Examples include:

- Mortgage payments

- Utility bills

- Internet service

- Cell phone plans

- Streaming subscriptions

- Home security monitoring

- Property management fees

- HOA dues

- Insurance premiums

- Charitable donations

- Cloud storage services

- Software subscriptions

If no one knows these payments exist, they may continue long after they should have been canceled.

Creating a recurring payment list can save your family hundreds or even thousands of dollars.

Include Monthly Household Expenses

Although this is not technically part of your estate, it is incredibly helpful for a surviving spouse or family member.

Consider maintaining a simple monthly household summary showing:

- Average electric bill

- Water and sewer

- Natural gas

- Internet

- Mobile phones

- Homeowners insurance

- Property taxes

- Vehicle insurance

- Food and groceries

- Prescription medications

- Lawn care

- Other recurring expenses

This snapshot helps survivors quickly understand what it costs to operate the household while longer-term financial decisions are being made.

Organize Supporting Documents

Keep copies of:

- Loan agreements

- Mortgage statements

- Vehicle titles

- Credit card statements

- Property tax notices

- Payment schedules

- Automatic withdrawal authorizations

You don’t need years of statements—just enough information for someone to identify the account and know where to obtain current information.

A Living Financial Snapshot

Your debt inventory should be reviewed every year.

Balances change.

Loans are paid off.

Credit cards are opened and closed.

Interest rates change.

Updating this information annually ensures your Estate Planning Portfolio remains an accurate picture of your financial life.

Looking Ahead

In a future lesson of the Estate Planning Academy, you’ll learn how to prepare a Survivor Financial Transition Plan that goes even further by estimating monthly household income, recurring expenses, and available cash flow. This practical planning tool helps a surviving spouse understand their financial position during the critical weeks immediately following a death or serious illness.

Action Step

Create a master list of every outstanding loan, credit card, and recurring financial obligation.

As you complete the list, ask yourself one important question:

“If I were suddenly unable to manage my finances, would someone else know which bills must be paid next month?”

If the answer is yes, you’re making meaningful progress toward building a complete Estate Planning Portfolio that will truly serve your family when they need it most.

Step 5 – Organize Your Insurance Portfolio

Insurance is one of the most important parts of your financial life, yet it is often one of the least organized.

Many families know insurance exists, but they do not know which companies issued the policies, where the policies are located, how much coverage is available, or who should be contacted when a claim needs to be filed.

Your Estate Planning Portfolio should contain a complete inventory of every insurance policy you own, along with enough information for your loved ones to locate the policy and contact the insurance company quickly.

Why an Insurance Inventory Matters

Insurance often provides the financial resources a family needs immediately following a death, disability, accident, or natural disaster.

Unfortunately, claims cannot be filed if no one knows the policy exists.

An organized insurance portfolio allows your family to:

- Locate policies quickly.

- Contact the correct insurance company.

- File claims without unnecessary delays.

- Verify coverage.

- Continue important insurance protection.

- Avoid missed premium payments.

- Identify policies that should be canceled after a death.

A few hours spent organizing your insurance records today could save your family weeks of frustration later.

Types of Insurance to Include

Most households have more insurance than they realize.

Your Estate Planning Portfolio should include information about every significant policy, including:

Personal Insurance

- Life insurance

- Health insurance

- Medicare

- Medicare Supplement (Medigap)

- Medicare Advantage

- Dental insurance

- Vision insurance

- Disability insurance

- Long-term care insurance

Property Insurance

- Homeowners insurance

- Condominium insurance

- Renters insurance

- Flood insurance

- Windstorm or hurricane insurance

- Personal articles policies

- Valuable jewelry riders

Vehicle Insurance

- Automobile insurance

- Motorcycle insurance

- Boat insurance

- Recreational vehicle insurance

- Golf cart insurance

- Trailer insurance

Liability Protection

- Personal umbrella liability policy

- Professional liability insurance

- Directors and Officers (D&O) insurance

- Errors and Omissions (E&O) insurance

Business Insurance

If you own a business, consider including:

- General liability

- Commercial property insurance

- Business interruption insurance

- Commercial automobile coverage

- Workers’ compensation

- Cyber liability insurance

- Key person insurance

- Buy-sell agreement funding policies

What Information Should You Record?

For each policy, include:

- Insurance company

- Policy number

- Type of coverage

- Named insured

- Coverage amount

- Deductible

- Renewal date

- Premium payment schedule

- Agent’s name

- Agent’s phone number

- Claims phone number

- Website or online account information

You don’t need to include every page of every policy in your binder. Instead, maintain a summary sheet with enough information for your family to locate the complete policy when needed.

Review Your Beneficiaries

Some insurance policies, particularly life insurance, pay directly to the named beneficiary rather than passing through your estate.

For that reason, beneficiary designations should be reviewed whenever:

- You get married.

- You divorce.

- A child is born.

- A beneficiary dies.

- You establish a trust.

- Your estate plan changes.

An outdated beneficiary designation can override the instructions in your will.

One of the easiest ways to unintentionally create problems for your heirs is to forget to update these forms after a major life event.

Keep Proof of Coverage

Store the following together:

- Policy declarations pages

- Insurance identification cards

- Recent premium statements

- Contact information for your insurance agent

- Claims instructions

- Photos or videos of valuable property (if available)

Photographs and videos can be especially helpful when filing homeowners or flood insurance claims after a natural disaster.

Annual Insurance Review

Your insurance needs change throughout your life.

Review your coverage every year and ask yourself:

- Do I have enough life insurance?

- Have I purchased expensive personal property?

- Have I remodeled my home?

- Have I changed vehicles?

- Have I started a business?

- Have I retired?

- Has my health changed?

- Have I increased my net worth enough to justify an umbrella liability policy?

Your Estate Planning Portfolio should reflect your current insurance protection—not the policies you owned years ago.

Action Step

Create a one-page Insurance Summary listing every active insurance policy, where the policy is located, and who should be contacted if a claim must be filed.

As you complete this inventory, remember that insurance is more than a financial product. It is a promise of protection for the people you care about most. Organizing your insurance information today helps ensure those promises can be fulfilled quickly when your family needs them most.

Step 6 – Create Your Digital Estate Portfolio

Twenty years ago, most important records were stored in filing cabinets and desk drawers.

Today, much of your financial life exists only in digital form.

Your bank statements may never arrive in the mail. Your investments may be managed entirely online. Your family photographs may be stored in the cloud, and your bills may be paid automatically from accounts that only you know how to access.

If your loved ones cannot access these digital assets, they may struggle to locate important information, manage your finances, or preserve treasured memories.

That is why every modern Estate Planning Portfolio should include a Digital Estate Portfolio.

What Is a Digital Estate?

A digital estate consists of every online account, electronic record, subscription, website, and digital asset that you own or control.

Some have financial value.

Others have sentimental value.

Many contain information your family will need immediately following your incapacity or death.

Your Digital Estate Portfolio should serve as a roadmap—not necessarily a list of usernames and passwords—but a guide that helps trusted individuals understand what digital assets exist and how they can be accessed legally.

Digital Assets to Include

As you build your Digital Estate Portfolio, consider documenting the following categories.

Financial Accounts

- Online banking

- Credit unions

- Brokerage accounts

- Retirement accounts

- Health Savings Accounts (HSAs)

- Cryptocurrency exchanges

- Digital wallets

- Payment services such as PayPal, Venmo, or Cash App

Communication

- Personal email accounts

- Business email accounts

- Mobile phone providers

- Messaging services

Remember that access to an email account often provides access to dozens of other online accounts through password reset links.

Cloud Storage

Many important documents now exist only in cloud storage.

Examples include:

- Google Drive

- Microsoft OneDrive

- Apple iCloud

- Dropbox

- Box

These accounts may contain tax returns, estate planning documents, photographs, business records, and other irreplaceable information.

Social Media

Document every social media account, including:

- X (formerly Twitter)

- TikTok

- YouTube

Some platforms allow memorialization or deletion after death, while others require advance planning.

Websites and Online Businesses

If you own a website or online business, include information about:

- Domain registrations

- Website hosting

- WordPress administrator accounts

- Website backups

- Email marketing systems

- Affiliate programs

- Advertising accounts

- Online stores

- Payment processors

For many families, these assets may produce ongoing income and should be treated just like any other business asset.

Digital Subscriptions

Don’t overlook recurring subscriptions.

Examples include:

- Streaming services

- Music services

- Software subscriptions

- Cloud storage plans

- Security monitoring

- Online memberships

- AI subscriptions

- Business software

Many subscriptions automatically renew each month or year.

Documenting them helps prevent unnecessary charges after your death.

Protect Your Passwords

One of the biggest mistakes people make is printing every password and placing the list inside their estate planning binder.

While this may seem convenient, it can create significant security risks.

A much better approach is to use a reputable password manager.

Your Estate Planning Portfolio should simply document:

- Which password manager you use.

- Where the master password is securely stored.

- Who is authorized to access it.

- Any emergency access instructions.

This approach provides both security and convenience.

Don’t Forget Two-Factor Authentication

Many online accounts now require two-factor authentication (2FA).

If your family cannot access the authentication device, they may be unable to log into important accounts even if they know the password.

Document:

- Authentication apps

- Security keys

- Backup codes

- Trusted devices

- Recovery methods

This information can save countless hours of frustration.

As you print the documents produced by the RetireCoast Estate Planning Membership, you'll need a secure and organized place to keep them. A dedicated estate planning binder makes it much easier for you, your family, your executor, and your attorney to quickly locate important documents when they are needed.

The binder shown here was available at the time this lesson was written for approximately $35 on Amazon. It includes tabbed dividers for organizing estate planning documents such as your will, trust, powers of attorney, health care documents, insurance information, financial records, and other important paperwork.

- Keeps your estate planning documents organized.

- Makes information easy for loved ones to locate.

- Provides labeled sections for important records.

- Can be updated as your estate plan changes.

- Works well alongside your secure digital Estate Planning Portfolio.

Consider purchasing multiple binders if you're helping family members organize their affairs. Many people buy two or three at a time so they can create Estate Planning Portfolios for both parents, a spouse, or even adult children who are beginning their own estate planning journey.

Remember: The value isn't in the binder itself—it's in the organization. A well-organized Estate Planning Portfolio can save your loved ones countless hours of searching for documents during one of the most difficult times of their lives.

Digital Photos and Family Memories

For many families, the most valuable digital assets are not financial—they are personal.

Consider documenting where you store:

- Family photographs

- Home videos

- Genealogy records

- Digital scrapbooks

- Personal journals

- Audio recordings

- Family recipes

- Scanned historical documents

These memories often become priceless after a loved one passes away.

Organize, Don’t Overcomplicate

The purpose of your Digital Estate Portfolio is not to create a technical manual.

Instead, create a simple inventory that answers four questions:

- What digital assets do I have?

- Where are they located?

- How can an authorized person gain access?

- Who should manage them?

If your family can answer those four questions, they will be in an excellent position to manage your digital estate responsibly.

Looking Ahead

In a future lesson of the Estate Planning Academy, we’ll take a much deeper look at digital estate planning, online privacy, digital inheritance, and protecting electronic assets. We’ll also introduce the RetireCoast Digital Password & Access Manager, a companion tool designed to securely organize password locations, emergency access instructions, and other critical digital information without exposing sensitive credentials.

Action Step

Create a master inventory of your online accounts, digital assets, and cloud storage locations.

Rather than trying to remember everything from memory, work through one category at a time over several days. As you complete your Digital Estate Portfolio, you’ll be protecting not only your financial assets but also the digital memories and information that tell the story of your life.

Step 7 – Organize Your Estate Planning Documents

By now, your Estate Planning Portfolio contains a growing collection of personal information, financial records, insurance policies, digital assets, and other important documents.

Now it is time to organize the legal documents that give those records meaning.

These documents provide the legal authority that allows trusted individuals to carry out your wishes if you become incapacitated or after your death.

Think of your Estate Planning Portfolio as a library.

Your financial records, insurance policies, and personal information are the books.

Your estate planning documents are the instruction manual that tells everyone how those books should be used.

Your Estate Planning Documents Work Together

One of the biggest misconceptions about estate planning is that a single document can solve every problem.

In reality, each estate planning document has a specific purpose.

Together, they form a coordinated system that protects you, your family, and your assets.

For example:

- Your Will directs how property not held in a trust should be distributed.

- Your Revocable Living Trust manages assets during your lifetime and after your death while helping your family avoid probate for properly titled assets.

- Your Durable Financial Power of Attorney authorizes someone to manage financial matters if you become incapacitated.

- Your Health Care Power of Attorney allows someone you trust to make medical decisions when you cannot.

- Your Advance Health Care Directive communicates your wishes regarding medical treatment and end-of-life care.

- Your HIPAA Authorization allows designated individuals to receive protected medical information.

- Your Beneficiary Designations control who receives many retirement accounts and life insurance policies.

- Your Transfer-on-Death (TOD) and Payable-on-Death (POD) designations allow certain assets to pass directly to named beneficiaries.

Each document complements the others.

If one document is missing or outdated, your overall estate plan may not function as intended.

Organize Documents by Category

Rather than placing documents randomly into a binder, organize them into clearly labeled sections.

Suggested categories include:

Personal Legal Documents

- Last Will and Testament

- Codicils

- Marriage certificate

- Divorce decree

- Adoption records

Trust Documents

- Revocable Living Trust

- Irrevocable Trusts

- Trust amendments

- Trust certification

- Trust funding checklist

Financial Authority

- Durable Financial Power of Attorney

- Business Power of Attorney

- Property management authorizations

Medical Planning

- Health Care Power of Attorney

- Advance Health Care Directive

- Living Will

- HIPAA Authorization

- Organ donation instructions

Property Records

- Real estate deeds

- Vehicle titles

- Boat titles

- Aircraft registrations

- Business ownership documents

Beneficiary Records

- Retirement account beneficiaries

- Life insurance beneficiaries

- Transfer-on-Death registrations

- Payable-on-Death accounts

Originals vs. Copies

Many legal documents should be maintained in their original form.

Examples include:

- Original will

- Original trust agreement (when appropriate)

- Original deeds

- Signed powers of attorney

However, your Estate Planning Portfolio should also contain copies or indicate where the originals are stored.

If the originals are kept in:

- A home safe

- A fireproof document box

- Your attorney’s office

- A bank safe deposit box

…make sure your trusted family members know how to access them.

Keep Older Versions Separate

Avoid placing outdated estate planning documents in the same binder as your current documents.

If you have replaced an old will or trust, either destroy obsolete copies (after confirming they are no longer needed) or clearly label them as “Superseded—Do Not Use.”

This helps prevent confusion if someone discovers an older document years later.

Review Documents After Major Life Events

Estate planning is not a one-time project.

Review your legal documents whenever you experience a significant life change, such as:

- Marriage

- Divorce

- Birth or adoption of a child

- Death of a beneficiary

- Retirement

- Purchase or sale of a home

- Starting or selling a business

- Significant changes in your financial situation

- Moving to another state

Even if none of these events occur, review your documents every three to five years to ensure they continue to reflect your wishes and comply with current laws.

Build an Estate Planning Document Index

One of the most helpful additions to your Estate Planning Portfolio is a simple document index.

This one-page summary should identify:

- Document name

- Date signed

- Current version

- Original document location

- Copy location

- Attorney who prepared the document (if applicable)

When someone needs a document, they can quickly locate it without searching through the entire binder.

The RetireCoast Advantage

As you continue through the Estate Planning Academy, you’ll learn how each legal document works and when it should be used.

Estate Planning Membership subscribers also have access to guided planning tools that help organize information before documents are prepared, making meetings with an attorney more efficient and reducing the likelihood that important details will be overlooked.

Action Step

Gather every estate planning document you currently have—even if you believe it is outdated.

Create a simple inventory listing each document, the date it was signed, and where the original is stored.

If you discover missing documents or outdated information, make a note to address those items as you continue through the Estate Planning Academy.

Remember, an organized Estate Planning Portfolio is more than a collection of papers. It is a practical system that gives your loved ones confidence, saves time, and helps ensure your wishes are carried out exactly as you intended.

Step 8 – Record Your Final Wishes and Personal Instructions

Estate planning is about much more than money.

It is about ensuring your family understands your wishes during one of the most emotional periods of their lives. While your will and trust determine who receives your property, they often do not answer the many practical questions your loved ones will face immediately after your death.

Your Estate Planning Portfolio should include a section devoted to your personal instructions and final wishes.

These instructions may not always be legally binding, but they can provide tremendous comfort and guidance to the people you leave behind.

Why Personal Instructions Matter

Imagine your family sitting together after your passing, trying to answer questions such as:

- Did Mom want to be buried or cremated?

- Did Dad want military honors?

- Which charity would they have wanted memorial donations sent to?

- Who should care for the family dog?

- Are there special heirlooms that should stay in the family?

- Is there a favorite hymn, song, or scripture that should be included in the service?

Without guidance, families often worry that they are making the wrong decisions.

Even simple written instructions can remove uncertainty and provide peace of mind.

```htmlComplete all four Foundation Courses to understand the essential principles of estate planning, organize your information, learn how probate works, and choose the people who will help carry out your wishes.

Learn why estate planning matters, which documents may be needed, and how a thoughtful plan helps protect your family and your legacy.

Go to EST 101 →Organize your legal documents, financial accounts, insurance information, digital assets, contacts, and personal instructions into one practical system.

Go to EST 102 →Discover what probate is, why it exists, the delays and expenses it may create, and the planning strategies that can help reduce court involvement.

Go to EST 103 →Learn how to select your attorney, financial professionals, executor, trustee, healthcare agent, financial agent, and other trusted decision-makers.

Go to EST 104 →Funeral and Memorial Preferences

Although your family may ultimately make the final decisions, documenting your preferences can be extremely helpful.

You may wish to record:

- Burial or cremation preference

- Preferred cemetery

- Existing burial plots

- Military funeral honors

- Veteran information

- Preferred funeral home

- Religious or cultural traditions

- Memorial service preferences

- Favorite music or hymns

- Scripture readings

- Charitable organizations for memorial donations

Keep these instructions with your Estate Planning Portfolio rather than your will. In many cases, a will is not read until after funeral arrangements have already been made.

Organ Donation

If you have strong feelings regarding organ and tissue donation, document them clearly.

Also consider:

- Discussing your wishes with your family.

- Including your decision in your Advance Health Care Directive.

- Confirming any state donor registration.

The most effective estate plans communicate these wishes in multiple places.

Care for Pets

For many families, pets are beloved members of the household.

Your Estate Planning Portfolio should identify:

- Who should care for each pet.

- Veterinary contact information.

- Feeding schedules.

- Medications.

- Favorite routines.

- Microchip information.

- Pet insurance policies, if any.

If your pets have significant ongoing care needs, discuss your plans with the person you hope will become their caregiver.

Family Heirlooms

Earlier in this lesson, you learned about documenting valuable assets.

This is also an excellent place to identify family heirlooms and explain why they are important.

Examples include:

- Wedding rings

- Military medals

- Family Bible

- Handmade quilts

- Antique furniture

- Grandfather clock

- Handmade furniture

- Historical photographs

- Family recipes

- Genealogy records

Whenever possible, identify who should receive these special possessions.

Personal Messages

Some of the most treasured items families receive are not financial at all.

Consider leaving:

- Letters to your spouse.

- Letters to your children.

- Letters to future grandchildren.

- Personal stories.

- Life lessons.

- Words of encouragement.

- Family history.

- Written blessings.

Many people also record short video messages or audio recordings that can be shared with future generations.

Household Information

Think about the practical information someone would need if they suddenly became responsible for your home.

Document items such as:

- Home security system instructions

- Safe location

- Spare key locations

- Alarm codes (stored securely)

- Utility providers

- Lawn care providers

- Pest control company

- Home maintenance schedules

- Vehicle maintenance records

These details may seem ordinary today, but they can save your family considerable time and frustration later.

Your Legacy Is More Than Your Assets

Most people will not remember the size of your investment account.

They will remember your values, your kindness, your traditions, and the memories you created together.

An Estate Planning Portfolio should preserve both.

Your financial legacy provides security.

Your personal legacy provides meaning.

The greatest estate plans do both.

Action Step

Begin writing down the personal instructions only you can provide.

Start with funeral preferences, pet care, and family heirlooms. Then gradually add the stories, traditions, and personal messages you hope future generations will know.

One day, these pages may become the most meaningful part of your entire Estate Planning Portfolio—not because they describe what you owned, but because they reveal who you were.

Step 9 – Organize Your Estate Planning Binder and Digital Portfolio

By now, you’ve gathered a tremendous amount of information.

You have organized your personal records, inventoried your assets and debts, documented your insurance coverage, identified your digital assets, assembled your legal documents, and recorded your personal wishes.

The next step is bringing everything together into one organized system.

Your Estate Planning Portfolio should be easy to understand, simple to update, and readily accessible to the people who may someday need it.

Think Like Your Executor

When organizing your portfolio, ask yourself one important question:

“If someone else had to manage my affairs tomorrow, could they quickly find what they need?”

Your executor, successor trustee, spouse, or adult children should not have to search through filing cabinets, desk drawers, closets, or computer files trying to piece together your financial life.

Instead, your portfolio should guide them from one section to the next in a logical order.

Use a Three-Ring Binder

One of the simplest ways to organize your Estate Planning Portfolio is with a sturdy three-ring binder.

Using tab dividers makes it easy to locate information quickly.

Suggested sections include:

- Personal Information

- Family Contacts

- Professional Advisors

- Estate Planning Documents

- Financial Accounts

- Real Estate

- Insurance Policies

- Digital Assets

- Personal Property Inventory

- Final Wishes and Personal Instructions

These sections can easily be expanded as your estate grows more complex.

Olivia and Peter decided they didn't want their four adult children wondering what they would have wanted after they were gone. Instead, once they completed their Estate Planning Portfolio, they invited the entire family to their home for a relaxed family meeting.

They began by explaining the overall structure of their estate plan, including their will, revocable living trust, powers of attorney, health care documents, insurance information, and the Estate Planning Portfolio that organized everything in one place. Rather than focusing on money, they focused on their wishes and the reasons behind their decisions.

- Who would serve as executor of their will.

- Who would become successor trustee of their trust.

- Where the Estate Planning Portfolio would be stored.

- How to locate important documents and digital records.

- How the grandchildren would be remembered.

- Special family heirlooms and sentimental possessions.

- Funeral and memorial preferences.

- How family members should work together if an emergency occurred.

One of the most meaningful parts of the conversation involved the RetireCoast Personal Property Request Worksheet. Before preparing their estate plan, each of their children completed the worksheet describing the personal items that meant the most to them. Their parents used those responses to thoughtfully distribute jewelry, family photographs, antiques, keepsakes, and other treasured possessions.

“I feel like a huge weight has been lifted from our shoulders.”

— Peter, after the family meeting

When the discussion ended, the estate planning notebooks were put away, dinner was served, and the evening became a normal family gathering filled with conversation, laughter, and shared memories. The difficult questions had already been answered while Peter and Olivia were there to explain them.

Once your Estate Planning Portfolio is complete, schedule a family meeting. Encourage everyone to listen to the RetireCoast Estate Planning Podcast before the meeting so they have a basic understanding of wills, trusts, powers of attorney, and other planning documents. The conversation will be easier, questions will be more informed, and your family will leave with confidence instead of uncertainty. Estate planning isn't just about preparing documents—it's about preparing the people you love.

Protect Original Documents

Although your binder should contain copies of important legal documents, many originals should be stored separately.

Examples include:

- Original will

- Original trust agreement

- Property deeds

- Vehicle titles

- Stock certificates

- Military discharge papers

- Birth certificates

- Marriage certificates

Your Estate Planning Portfolio should clearly indicate where each original document is stored.

Build a Digital Portfolio Too

Today’s estate plans should exist in more than one format.

In addition to your physical binder, consider creating a secure digital portfolio containing:

- Scanned legal documents

- Insurance summaries

- Financial account inventories

- Property inventories

- Important photographs

- Medical information

- Emergency contact lists

Store these files using encrypted cloud storage or another secure system that can be accessed by trusted individuals when needed.

Keep Everything Updated

An outdated portfolio can be almost as frustrating as having no portfolio at all.

Review your Estate Planning Portfolio whenever you:

- Buy or sell property.

- Open or close financial accounts.

- Change insurance companies.

- Update your will or trust.

- Change beneficiaries.

- Move to a new address.

- Marry or divorce.

- Welcome a new child or grandchild.

- Lose a loved one.

Many families choose New Year’s Day, tax season, or their birthday as an annual reminder to review everything.

Don’t Make It Too Complicated

Remember, your Estate Planning Portfolio is a practical tool—not a museum.

You do not need to save every bank statement or every utility bill.

Instead, focus on keeping current summaries, account information, and instructions that will help someone understand your financial life.

A clean, well-organized binder is far more useful than several boxes filled with decades of paperwork.

Tell Someone It Exists

One of the greatest estate planning mistakes is creating an excellent Estate Planning Portfolio and never telling anyone about it.

At a minimum, your spouse, successor trustee, executor, or another trusted family member should know:

- That your portfolio exists.

- Where it is stored.

- How to access it in an emergency.

- Who to contact if they have questions.

You don’t necessarily need to share every detail today, but you should make sure the right people know where to begin if they ever need to step into your role.

Your Estate Planning Portfolio Is a Gift

Many people think of estate planning as something they do for themselves.

In reality, it is one of the greatest gifts you can leave your family.

An organized Estate Planning Portfolio reduces confusion, prevents unnecessary delays, lowers stress, and allows your loved ones to focus on one another instead of searching for information.

Your portfolio represents years of thoughtful preparation and careful planning.

One day, it may become one of the most valuable gifts your family ever receives—not because of the papers inside, but because of the peace of mind they provide.

Action Step

Place all of your completed documents, inventories, summaries, and personal instructions into your Estate Planning Binder.

Then create a secure digital backup and schedule a recurring annual review.

Remember, your Estate Planning Portfolio is never truly finished. It grows and changes with your life, ensuring that whenever your family needs it, the information they depend on will already be organized, current, and waiting for them.

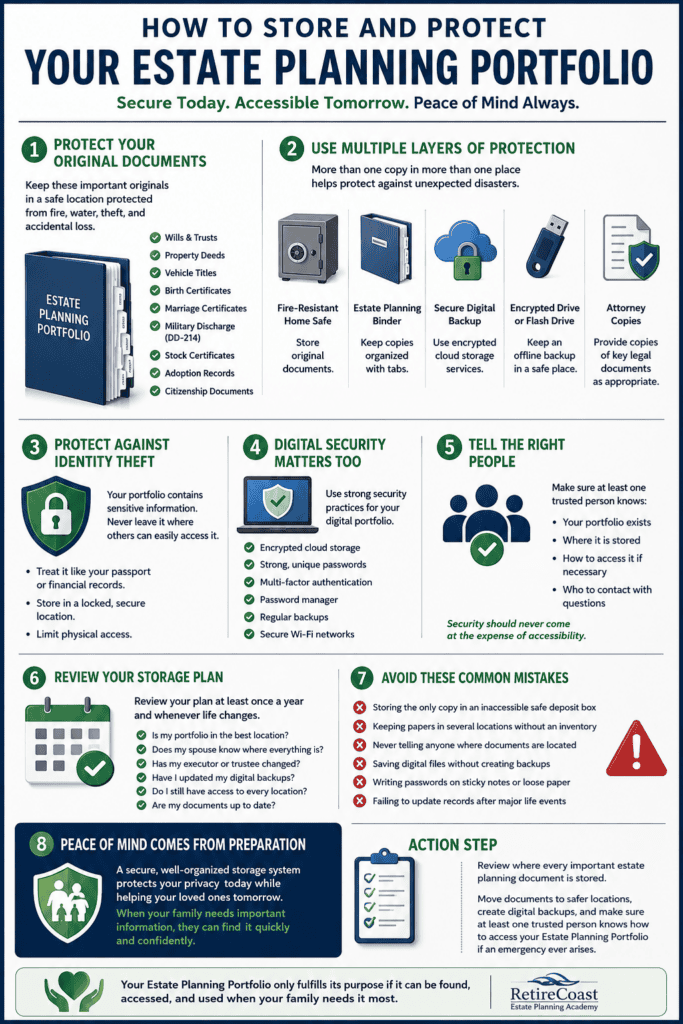

Step 10 – How to Store and Protect Your Estate Planning Portfolio

Building your Estate Planning Portfolio is a tremendous accomplishment.

The next challenge is making sure it is both secure and accessible.

Those two goals may seem contradictory, but they are equally important. A portfolio that is perfectly secure but cannot be found is of little value. Likewise, a portfolio that is easy to find but not adequately protected may expose your family to identity theft, fraud, or unauthorized access.

The goal is to strike the right balance.

Protect Your Original Documents

Certain documents should always be protected because replacing them may be difficult, expensive, or impossible.

Examples include:

- Original Last Will and Testament

- Original Trust Agreement (when applicable)

- Property deeds

- Vehicle titles

- Birth certificates

- Marriage certificates

- Military discharge papers (DD-214)

- Stock certificates

- Adoption records

- Citizenship or naturalization documents

These documents should be stored in a secure location that is protected from fire, water damage, theft, and accidental loss.

Consider Multiple Layers of Protection

Many estate planning professionals recommend using more than one storage method.

For example:

- A fire-resistant home safe for original documents.

- A working Estate Planning Binder containing copies.

- A secure digital backup stored in encrypted cloud storage.

- An encrypted external hard drive or flash drive.

- Copies of key legal documents provided to your attorney when appropriate.

Having more than one copy helps protect against unexpected disasters such as fires, floods, hurricanes, or tornadoes.

Protect Against Identity Theft

Your Estate Planning Portfolio contains sensitive information.

It may include:

- Social Security numbers

- Financial account information

- Insurance policy numbers

- Property records

- Medical information

- Password locations

For that reason, never leave your Estate Planning Portfolio sitting on a desk, bookshelf, or other location where visitors or service providers could easily access it.

Treat it with the same level of security you would give your passport or financial records.

Digital Security Matters Too

If you maintain a digital Estate Planning Portfolio, use strong security practices.

Consider:

- Encrypted cloud storage

- Strong, unique passwords

- Multi-factor authentication

- Password managers

- Regular backups

- Secure Wi-Fi networks

Avoid storing sensitive documents on public computers or unsecured devices.

Tell the Right People

Security should never come at the expense of accessibility.

If no one knows your Estate Planning Portfolio exists, your careful planning may never benefit your family.

At a minimum, make sure your spouse, executor, successor trustee, or another trusted individual knows:

- That your Estate Planning Portfolio exists.

- Where it is stored.

- How to gain access if necessary.

- Who to contact if questions arise.

You do not have to give everyone unrestricted access today, but someone should know how to locate your portfolio if an emergency occurs.

Review Your Storage Plan

As your life changes, so should your storage strategy.

Ask yourself each year:

- Is my portfolio still stored in the best location?

- Does my spouse know where everything is?

- Has my executor changed?

- Have I updated my digital backups?

- Do I still have access to every storage location?

A few minutes spent reviewing these questions each year can prevent significant problems later.

Avoid These Common Mistakes

Many families unintentionally create problems by making one of these mistakes:

- Storing the only copy of a will in an inaccessible safe deposit box.

- Keeping important papers in several different locations without an inventory.

- Never telling anyone where documents are located.

- Saving digital files without creating backups.

- Writing passwords on sticky notes or loose pieces of paper.

- Failing to update records after major life events.

Each of these mistakes can delay estate administration and increase stress for surviving family members.

Peace of Mind Comes from Preparation

The purpose of your Estate Planning Portfolio is not simply to organize documents.

It is to ensure that when your family needs important information, they can find it quickly and confidently.

A secure, well-organized storage system protects your privacy today while helping your loved ones tomorrow.

Action Step

Review where every important estate planning document is currently stored.

If necessary, move documents into safer locations, create digital backups, and make sure at least one trusted person knows how to access your Estate Planning Portfolio if an emergency ever arises.

Remember, your Estate Planning Portfolio only fulfills its purpose if it can be found, accessed, and used when your family needs it most.

Step 11 – Who Should Have Access to Your Estate Planning Portfolio?

Creating an Estate Planning Portfolio is only half the job.

The other half is making sure the right people can access it when they need to.

Many people spend years organizing their financial records, legal documents, insurance policies, and personal instructions but never tell anyone where those records are located. As a result, their carefully prepared portfolio remains hidden when their family needs it most.

The goal is to balance privacy, security, and accessibility.

Start with Your Spouse

If you are married, your spouse should usually be the first person who knows where your Estate Planning Portfolio is stored.

Although you may handle most of the household finances today, your spouse could unexpectedly become responsible for everything.

Make sure they know:

- Where your Estate Planning Binder is located.

- Where original legal documents are stored.

- How to access your digital portfolio.

- Where passwords are securely maintained.

- Who your attorney, CPA, and financial advisor are.

One conversation today can save weeks of confusion later.

Your Successor Trustee

If you have a Revocable Living Trust, your successor trustee should know:

- That the trust exists.

- Where the trust documents are located.

- How to contact your attorney.

- Where trust assets are documented.

- Where your Estate Planning Portfolio is stored.

You do not necessarily need to give your successor trustee copies of every document today, but they should know where to begin if they are ever called upon to serve.

Your Executor

Your executor has an important responsibility.

After your death, they may need immediate access to:

- Your will.

- Contact information for beneficiaries.

- Financial account inventories.

- Insurance policies.

- Funeral instructions.

- Property records.

- Outstanding debts.

- Professional advisors.

A well-organized Estate Planning Portfolio makes this responsibility far less overwhelming.

Adult Children

Should your children have access?

That depends on your circumstances.

Many families choose to:

- Tell adult children where the portfolio is stored.

- Explain how it is organized.

- Identify who has primary responsibility.

- Discuss general estate planning goals.

You do not have to disclose every financial detail if you are uncomfortable doing so.

The important thing is that someone knows how to locate your portfolio if an emergency occurs.

Agents Under Your Powers of Attorney

If you have appointed someone to act under a:

- Durable Financial Power of Attorney

- Health Care Power of Attorney

…that individual should understand their responsibilities and know where to find the information they may need if they must act on your behalf.

This is especially important if they do not live nearby.

Your Attorney and Financial Advisor

Your professional advisors should know about your Estate Planning Portfolio.

They may already have copies of some documents, but they can also help ensure:

- Your documents remain current.

- Beneficiary designations are reviewed.

- Trust funding remains complete.

- New assets are properly titled.

Your Estate Planning Portfolio becomes much more valuable when your advisors understand how it is organized.

Don’t Share Too Much

There is a difference between telling someone your portfolio exists and giving unrestricted access to every piece of sensitive information.

For example:

- Your children do not necessarily need copies of every bank statement.

- Friends generally should not know your passwords.

- Visitors should never have unrestricted access to your portfolio.

Instead, share information thoughtfully and only with people you trust.

One of the most valuable things you can do after completing your Estate Planning Portfolio is to hold a family meeting with your spouse, adult children, or other trusted loved ones. An open discussion today can prevent confusion, misunderstandings, and unnecessary stress later.

Before your meeting, encourage everyone to listen to the RetireCoast Estate Planning Podcast. Hearing the same information beforehand gives everyone a common understanding of the estate planning process, making your discussion more productive and allowing you to focus on your family’s specific plans rather than explaining basic concepts.

You will find the podcast at the end of this lesson. Ask each family member to listen before your meeting, then gather around the table with your Estate Planning Portfolio to review your wishes, answer questions, and ensure everyone understands where important documents are kept and who will be responsible for carrying out your plans.

Hold a Family Meeting

One of the best ways to introduce your Estate Planning Portfolio is during a family meeting.

Explain:

- Why you created it.

- Where it is stored.

- Who serves as executor and successor trustee.

- Where original documents are located.

- How family members should proceed if an emergency occurs.

These conversations can feel uncomfortable at first, but they often provide tremendous peace of mind for everyone involved.

One thing I've learned after talking with countless people about estate planning is this: your wishes are far more likely to change than you might expect. In fact, nearly every person I've spoken with who created their estate planning documents five or more years ago needed to make updates before their plan truly reflected their current life.

The most common changes involve assets. Someone sells a home and buys another, but never transfers the new property into their trust. They close an old 401(k), move the money into a Roth IRA at Schwab or another financial institution, yet the new account never makes it into their Estate Planning Portfolio. Others change insurance companies, open new bank accounts, purchase investment property, or simply forget to update beneficiary designations after major life events.

"An estate plan that accurately reflected your life five years ago may no longer reflect your life today."

That's one of the primary reasons I created the RetireCoast Estate Planning Membership. Estate planning isn't just about creating documents—it's about maintaining them. When your life changes, you should be able to log into your membership, update your information, generate new documents if necessary, and replace the pages in your Estate Planning Portfolio without starting over from scratch.

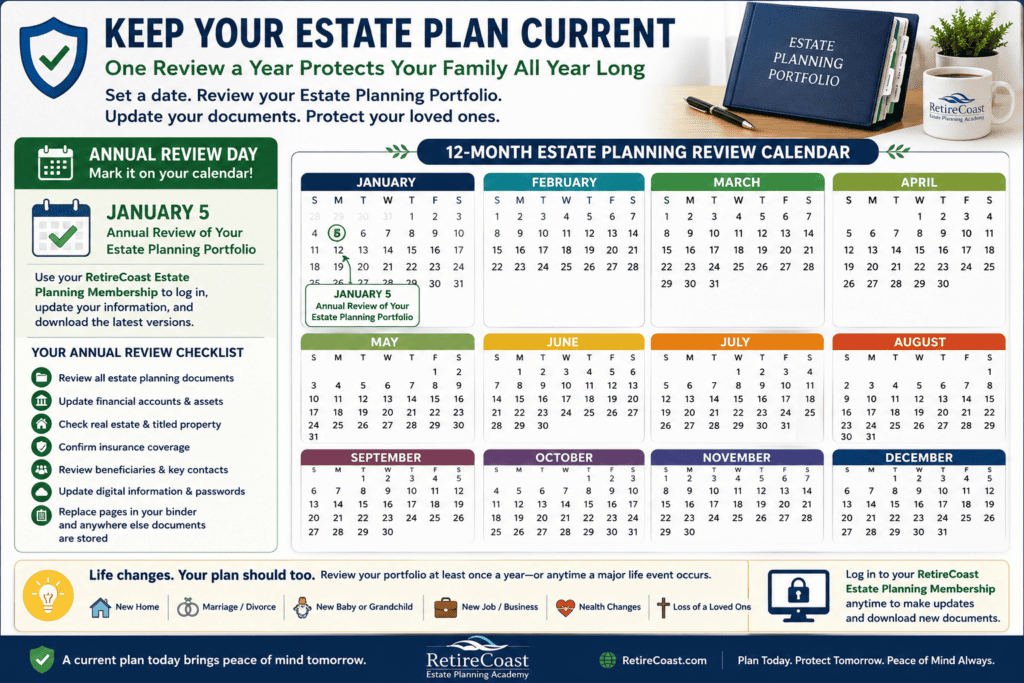

You'll also notice that throughout this lesson I recommend setting aside January 5 (or a date close to it) as your annual Estate Planning Portfolio Review Day. Why January 5? For me, the holidays are over, family has returned home—or I've returned home—and the new year has begun. It's the perfect time to review the previous year's changes before tax season gets into full swing.

I already spend time reviewing my finances and preparing for tax season, so I simply added my estate planning review to the same annual routine. During one planning session, I update my financial records, review beneficiary designations, verify my trust funding, revise my Estate Planning Portfolio if necessary, and print any updated pages for my binder. It has become one of the best habits I've developed, and I encourage you to consider doing the same.

Put an annual reminder on your calendar today. Whether you choose January 5 or another date that's meaningful to you, review your Estate Planning Portfolio every year. Log into your RetireCoast Estate Planning Membership, make any necessary updates, print replacement pages for your binder, update your digital copies, and you'll have confidence knowing your family will always have current information when they need it most.

Remember That Trust Can Change

Relationships change over time.

Someone you trusted ten years ago may no longer be the best choice today.

Review your:

- Executor.

- Successor trustee.

- Powers of attorney.

- Emergency contacts.

- Beneficiary designations.

…whenever significant life changes occur.

Action Step

Make a written list of every person who should know about your Estate Planning Portfolio.

Then ask yourself:

“If I became incapacitated tomorrow, would these people know exactly where to begin?”

If the answer is yes, you’ve taken another important step toward creating an Estate Planning Portfolio that truly protects your family.

The purpose of estate planning is not simply to prepare documents—it is to prepare people. When the right people have the right information at the right time, your planning becomes one of the greatest gifts you can leave behind.

Step 12 – Keeping Your Estate Planning Portfolio Up to Date

Congratulations.

If you’ve followed the lessons in this Master Class, you’ve built far more than a binder full of documents. You’ve created an organized Estate Planning Portfolio that can guide your family through one of life’s most difficult transitions.

But your work is not finished.

An Estate Planning Portfolio is a living document. It should grow and change as your life changes.

Life Doesn’t Stand Still

Think about everything that can change over just a few years.

You may:

- Purchase a new home.

- Sell an investment property.

- Retire.

- Welcome a grandchild.

- Start a business.

- Receive an inheritance.

- Change banks.

- Open new investment accounts.

- Move to another state.

- Lose a loved one.

Each of these events may require updates to your Estate Planning Portfolio.

If your information becomes outdated, your family could waste valuable time trying to determine what is current.

Create an Annual Review Day

One of the easiest ways to keep your portfolio current is to schedule an annual review.

Many people choose:

- New Year’s Day

- Their birthday

- Their wedding anniversary

- Tax preparation season

- The first weekend in January

Whatever date you choose, put it on your calendar and treat it like an annual financial checkup.

What Should You Review?

During your annual review, verify that the following information is still accurate.

Estate Planning Documents

- Will

- Revocable Living Trust

- Powers of Attorney

- Advance Health Care Directive

- HIPAA Authorization

- Personal Property Memorandum

Financial Information

- Bank accounts

- Brokerage accounts

- Retirement accounts